|

市場調查報告書

商品編碼

2073212

亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

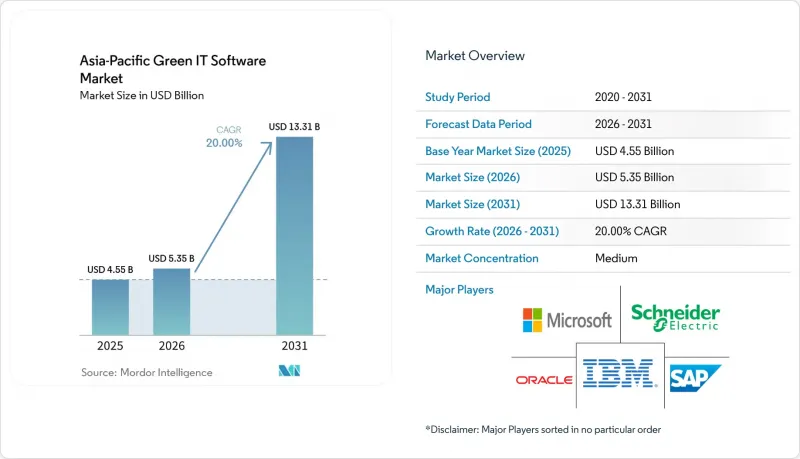

根據 Mordor Intelligence 預測,亞太地區綠色 IT 軟體市場規模將從 2025 年的 45.5 億美元成長到 2026 年的 53.5 億美元,然後在 2031 年達到 133.1 億美元,2026 年至 2031 年的複合年成長率為 20.00%。

本報告按交付方式(軟體和服務)、部署方式(雲端、混合等)、公司規模(大型企業和中小企業)、解決方案類型(碳管理和計算軟體等)、最終用戶行業(資訊技術和電信等)以及地區進行細分。市場預測以美元計價。

亞太地區綠色IT軟體市場趨勢及洞察。

亞太地區的ESG資訊揭露義務

強制性資訊揭露法規正在亞太地區綠色IT軟體市場催生最強勁的需求基礎。這是因為迫在眉睫的合規期限迫使企業正式建立報告流程,而不是推遲對平台的投資。中國將於2026年啟動A股上市公司的首個強制性資訊揭露週期,這使得資訊揭露準備成為許多大型企業的短期管理重點。在日本,監理進程也取得了進展,金融廳於2026年2月26日最終確定了符合日本證券監理委員會(SSBJ)要求的資訊揭露標準,為主要上市公司提供了更清晰的報告義務時間表。新加坡和澳洲在實施氣候變遷報告方面已取得進一步進展,進一步強化了該全部區域合規要求日益嚴格、準備時間日益縮短的趨勢。這一系列進展意義重大,因為軟體的選擇現在越來越接近提交截止日期。這使得那些提供現成模板、強大的實施支援和完善的審計追蹤功能的供應商更具優勢。此外,每項新規的生效都會帶動首次購買者和回頭客的購買量激增,這將加速亞太地區綠色IT軟體市場的商業性擴張。

利用人工智慧實現永續性數據收集自動化

人工智慧正在提升亞太地區綠色IT軟體市場的價值提案,因為它減少了跨多個框架收集、分類和映射資訊所需的人工工作量。 2026年5月,SAP發布了一款新的永續發展人工智慧代理,其中包括旨在支援現有永續發展工作流程中的監管合規性和供應鏈碳排放智慧的工具。同年,IBM也利用Envizi的功能擴展了其可操作的排放計算工具,使認證的排放因子能夠整合到現有的電子表格和企業流程中。 Workiva在2026年進一步加強了在企業發展,這反映出企業對能夠支援更廣泛區域部署的自動化報告的需求日益成長。隨著自動化程度的提高,企業只需付出極少的額外努力即可採用新的框架,從而促使採購重點轉向在單一環境中整合資料擷取、揭露審查和管治管理的平台。這種轉變正在推動亞太地區的綠色IT軟體市場超越狹隘的合規用例,並走向更廣泛的業務部署。

亞太地區報告架構和分類系統碎片化

亞太地區綠色IT軟體市場成長速度持續受到監管碎片化問題的限制。這是因為跨境營運的公司往往面臨不同的時間表、保障要求和報告定義。儘管經合組織強調到2025年該地區將更加重視永續發展相關資訊揭露,但各國的具體做法在範圍和重點上仍存在差異。日本的資訊揭露流程是基於符合日本永續發展標準委員會(SSBJ)的標準,而新加坡則透過當地監管管道實施其自身的報告和保障框架。這導致採購階段出現猶豫,因為買家在決定進行多年部署之前,需要確認平台能夠同時適應多個不同的規則。當供應商網路跨越多個市場,並且對轉型活動、重要性或保障深度採用不同的定義時,這個問題會變得更加複雜。即使需求強勁,由於每次新的部署都需要額外的映射、客製化和法律審查,亞太地區綠色IT軟體市場的成長效率仍然較低。

細分市場分析

到2025年,軟體將佔市場佔有率的63.47%,這意味著訂閱式平台仍將是亞太地區綠色IT軟體市場的主要收入來源。買家之所以青睞軟體,是因為訂閱模式能夠實現更快的更新、更清晰的審計追蹤以及更有效地管理週期性報告。此外,資訊揭露框架的頻繁變更使得靜態的、基於企劃為基礎的工作方式逐漸變得不切實際,從而推動了對平台的需求。當客戶尋求集中式的資料收集、計算、審核和最終資訊揭露環境時,軟體供應商將從中受益。因此,亞太地區ESG和永續發展軟體產業的這一領域正變得越來越依賴營運報告需求,而非一次性的諮詢服務。

預計2026年至2031年間,服務市場將以22.96%的複合年成長率成長,這反映了首次在新披露司法管轄區披露資訊的公司的短期需求。許多公司在能夠自信地使用該平台之前,仍然需要協助進行差距評估、資料準備驗證、揭露框架解讀以及首次揭露週期的準備工作。因此,在新報告階段的前12-24個月,具備實施和託管支援能力的軟體供應商將擁有更大的優勢。隨著時間的推移,隨著內部團隊熟悉流程和管治機制的穩定,客戶通常會轉向更多自助式使用。這意味著,儘管軟體仍將是亞太地區綠色IT軟體市場的長期基礎,但服務可以加速初始階段的採用。

預計到2025年,基於雲端的部署將佔亞太地區綠色IT軟體市場佔有率的61.94%,這印證了在報告法規快速變化的背景下,買家仍然傾向於靈活的交付方式。雲端系統使企業能夠更新模板、管理變更並部署新的運算邏輯,而無需像內部升級那樣等待漫長的時間。這在亞太地區的綠色IT軟體市場尤其重要,因為多個國家的報告系統正在同步開發。混合部署也正在興起,一些跨國公司希望在靠近現場運作的地方收集敏感數據,同時在管治進行集中分析。這一趨勢表明,部署決策越來越受到治理需求的驅動,而非單一的技術偏好。

預計從2026年到2031年,本地部署將以21.59%的複合年成長率成長,這意味著在資料管理要求日益嚴格的機構中,本地部署將保持強勁的市場佔有率。金融機構、政府企業和國防製造商通常需要對資料儲存、傳輸和系統存取進行更嚴格的控制。在這些情況下,選擇本地或私人環境的原因與其說是便利,不如說是監管和政策的限制。因此,儘管雲端仍然佔據更大的收入基礎,但本地部署的成長原因與雲端有所不同。亞太地區的綠色IT軟體市場正因資料主權而進一步分散,如果供應商想要同時服務大型跨國公司和受嚴格監管的國內機構,就需要靈活的架構。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 亞太地區強制性ESG資訊揭露

- 透過雲端遷移降低軟體的碳排放強度

- 資料中心電力效率和冷卻最佳化優先事項

- 供應商網路面臨報告範圍 3 的壓力

- 利用人工智慧實現永續性數據收集自動化

- 綠色採購與企業成本和聲譽目標息息相關

- 市場限制因素

- 亞太地區報告架構與分類體系的碎片化

- 與傳統企業系統進行高階整合工作

- 供應商系統與業務系統之間的資料品質差距

- 永續發展分析師短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

- 價格分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按解決方案類型

- 碳管理和運算軟體

- ESG報告和合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源和資源最佳化軟體

- 按最終用戶行業分類

- 資訊科技/通訊

- 銀行、金融服務和保險(BFSI)

- 製造業

- 能源公用事業

- 零售與電子商務

- 政府

- 衛生保健

- 建築和基礎設施

- 其他終端用戶產業

- 國家

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Schneider Electric SE

- Oracle Corporation

- Salesforce, Inc.

- Workiva Inc.

- Wolters Kluwer NV

- Sphera Solutions, Inc.

- EcoVadis SAS

- Diligent Corporation

- Persefoni AI Inc.

- Greenly SAS

- Enablon, a Wolters Kluwer Company

- Benchmark Digital Partners LLC

- Cority Software Inc.

- Intelex Technologies ULC

- Siemens AG

- Cisco Systems, Inc.

- Accenture PLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific green IT software market size is expected to grow from USD 4.55 billion in 2025 to USD 5.35 billion in 2026 and is forecast to reach USD 13.31 billion by 2031 at 20.00% CAGR over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, Hybrid, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and More), End-User Industry (Information Technology and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Green IT Software Market Trends and Insights

ESG Disclosure Mandates Across Asia-Pacific

Mandatory disclosure rules are creating the strongest current demand base for the Asia-Pacific green IT software market because compliance deadlines now require companies to formalize reporting processes instead of delaying platform investment. China moved toward its first mandatory reporting cycle for A-share listed companies in 2026, which made disclosure readiness a near-term operating priority for a large corporate base. Japan also advanced the regulatory path when the Financial Services Agency finalized SSBJ-aligned disclosure standards on February 26, 2026, giving large listed companies a clearer timetable for reporting obligations. Singapore and Australia were already further along in climate reporting rollout, which reinforced a wider regional pattern of rising compliance depth and shorter preparation windows. This sequence matters because software selection now happens closer to the filing deadline, which favors vendors with ready-built templates, stronger implementation support, and established audit trails. It also supports faster commercial scale for the Asia-Pacific green IT software market because each regulatory activation creates another concentrated wave of first-time and repeat buyers.

AI-Enabled Automation of Sustainability Data Capture

AI is improving the value case for the Asia-Pacific green IT software market because it reduces the manual effort needed to gather, classify, and map information across multiple frameworks. SAP announced new sustainability AI agents in May 2026, including tools intended to support regulatory readiness and supply chain carbon intelligence inside existing sustainability workflows. IBM also expanded practical emissions accounting tools in 2026 with Envizi capabilities that brought recognized emissions factors into existing spreadsheets and enterprise processes. Workiva continued to strengthen its Asia-Pacific commercial presence in 2026, which reflects growing enterprise demand for reporting automation that can support broader regional expansion. As automation improves, companies can add new frameworks with less extra labor, and that changes buying priorities toward platforms that combine data ingestion, disclosure review, and governance controls in one environment. This shift helps the Asia-Pacific green IT software market move beyond narrow compliance use cases and toward broader operating adoption.

Fragmented Asia-Pacific Reporting Frameworks and Taxonomies

Fragmented rules still limit the pace of the Asia-Pacific green IT software market because companies operating across borders often face different timelines, assurance needs, and reporting definitions. The OECD highlighted the region's widening focus on sustainability-related disclosure in 2025, but country approaches still differ in scope and emphasis. Japan's disclosure path is moving under SSBJ-aligned standards, while Singapore applies its own reporting and assurance structure through local regulatory channels. This creates hesitation during procurement because buyers want proof that a platform can adjust to several rulebooks at once before they commit to a multi-year rollout. The problem becomes more difficult when supplier networks span several markets and use different definitions for transition activity, materiality, or assurance depth. Even when demand stays strong, the Asia-Pacific green IT software market grows less efficiently when every new rollout needs extra mapping, customization, and legal review.

Other drivers and restraints analyzed in the detailed report include:

- Scope 3 Reporting Pressure on Supplier Networks

- Cloud Migration Lowering Software Carbon Intensity

- High Integration Effort With Legacy Enterprise Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 63.47% of the market in 2025, which shows that recurring platforms remain the main commercial base for the Asia-Pacific green IT software market. Buyers favored software because subscription models give them faster updates, clearer audit trails, and better control over repeat reporting cycles. Platform demand also rose because disclosure frameworks now change more frequently, which makes static project-based work less practical over time. Software providers benefit when customers want one environment for data capture, calculation, review, and final disclosure output. This part of the Asia-Pacific ESG and sustainability software industry has therefore become more closely tied to operational reporting needs than to one-time advisory engagement.

Services are projected to expand at a 22.96% CAGR from 2026 to 2031, which reflects the near-term needs of first-time filers across newly covered jurisdictions. Many companies still need help with gap assessments, data readiness checks, framework interpretation, and first-cycle disclosure preparation before they can use a platform with confidence. That is why software vendors with implementation and managed support capabilities are better placed during the first 12 to 24 months of a new reporting phase. Over time, customers usually move toward more self-service use as internal teams gain process familiarity and governance routines become stable. This means services can accelerate initial adoption even while software remains the long-run anchor of the Asia-Pacific green IT software market.

Cloud-based deployment accounted for 61.94% of the Asia-Pacific green IT software market share in 2025, confirming that buyers still prefer flexible delivery when reporting rules change quickly. Cloud systems help enterprises receive template updates, control changes, and new calculation logic without waiting for lengthy internal upgrade schedules. This matters in the Asia-Pacific green IT software market because several national reporting systems are being developed simultaneously. Hybrid deployment is also gaining ground because some multinationals want centralized analytics in the cloud while keeping sensitive data collection closer to site operations. That pattern shows that deployment decisions are increasingly based on governance needs rather than on a single technology preference.

On-premise deployment is projected to expand at a 21.59% CAGR from 2026 to 2031, indicating a durable niche among institutions with stricter data control requirements. Financial institutions, state-linked firms, and defense-adjacent manufacturers often need stronger control over storage, transfer, and system access. In these cases, the preference for on-premise or private environments is shaped less by convenience and more by regulatory and policy constraints. This segment therefore grows for a different reason than cloud, even though cloud still holds the larger revenue base. The Asia-Pacific green IT software market is becoming more segmented by data sovereignty, which means vendors need flexible architecture if they want to serve both large multinational buyers and tightly regulated domestic institutions.

Complete Report Scope:

- By offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End-User Industry

- Information Technology and Telecommunications

- Banking, Financial Services, and Insurance (BFSI)

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare

- Construction and Infrastructure

- Other End-User Industries

- By Country

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- IBM Corporation

- Microsoft Corporation

- SAP SE

- Schneider Electric SE

- Oracle Corporation

- Salesforce, Inc.

- Workiva Inc.

- Wolters Kluwer N.V.

- Sphera Solutions, Inc.

- EcoVadis SAS

- Diligent Corporation

- Persefoni AI Inc.

- Greenly SAS

- Enablon, a Wolters Kluwer Company

- Benchmark Digital Partners LLC

- Cority Software Inc.

- Intelex Technologies ULC

- Siemens AG

- Cisco Systems, Inc.

- Accenture PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ESG Disclosure Mandates Across Asia-Pacific

- 4.2.2 Cloud Migration Lowering Software Carbon Intensity

- 4.2.3 Data Center Power Efficiency and Cooling Optimization Priorities

- 4.2.4 Scope 3 Reporting Pressure on Supplier Networks

- 4.2.5 AI-Enabled Automation of Sustainability Data Capture

- 4.2.6 Green Procurement Linked to Enterprise Cost and Reputation Goals

- 4.3 Market Restraints

- 4.3.1 Fragmented Asia-Pacific Reporting Frameworks and Taxonomies

- 4.3.2 High Integration Effort With Legacy Enterprise Systems

- 4.3.3 Data Quality Gaps Across Supplier and Operational Systems

- 4.3.4 Shortage of Sustainability Analytics Talent

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance (BFSI)

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

- 5.6 By Country

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 South Korea

- 5.6.5 Australia

- 5.6.6 Singapore

- 5.6.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 Schneider Electric SE

- 6.4.5 Oracle Corporation

- 6.4.6 Salesforce, Inc.

- 6.4.7 Workiva Inc.

- 6.4.8 Wolters Kluwer N.V.

- 6.4.9 Sphera Solutions, Inc.

- 6.4.10 EcoVadis SAS

- 6.4.11 Diligent Corporation

- 6.4.12 Persefoni AI Inc.

- 6.4.13 Greenly SAS

- 6.4.14 Enablon, a Wolters Kluwer Company

- 6.4.15 Benchmark Digital Partners LLC

- 6.4.16 Cority Software Inc.

- 6.4.17 Intelex Technologies ULC

- 6.4.18 Siemens AG

- 6.4.19 Cisco Systems, Inc.

- 6.4.20 Accenture PLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年) 2026年全球數位測量和圖解決方案市場報告

2026年全球數位測量和圖解決方案市場報告 2026-2030年全球數位化製造軟體市場

2026-2030年全球數位化製造軟體市場