|

市場調查報告書

商品編碼

2073183

法國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)France Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

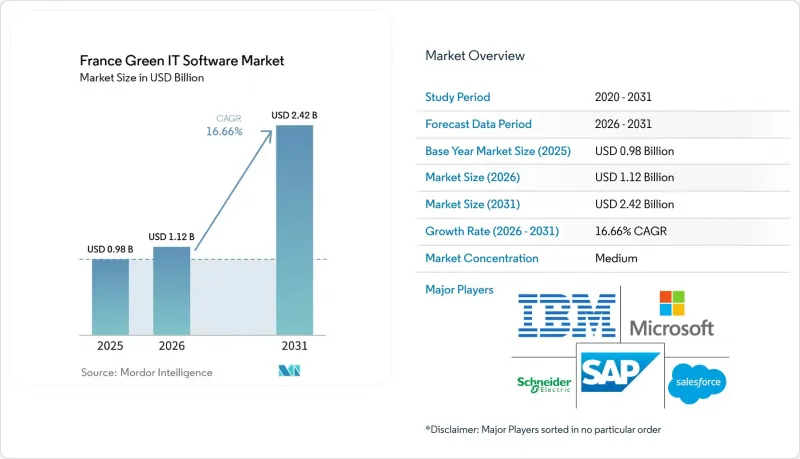

根據 Mordor Intelligence 預測,法國綠色 IT 軟體市場將從 2025 年的 9.8 億美元成長到 2026 年的 11.2 億美元,到 2031 年將達到 24.2 億美元,2026 年至 2031 年的複合年成長率為 16.66%。

本報告按交付方式(軟體和服務)、部署方式(雲端、本地部署、混合部署)、企業規模(大型企業和中小企業)、解決方案類型(碳管理和計算軟體、能源相關軟體等)以及最終用戶(IT和電信、銀行、金融服務和保險、製造業等)進行細分。市場預測以美元計價。

法國綠色IT軟體市場趨勢與洞察

歐盟和法國面臨越來越大的脫碳資訊揭露壓力

法國在落實《企業永續性報告指令》(CSRD)相關義務方面領先許多其他歐洲國家,這使得當地企業在選擇平台或準備永續發展報告資料方面的時間更加緊迫。由於主要上市公司已於2025年根據新框架提交報告,其他大型企業也計劃在2026年提交2025會計年度的報告,因此,對與排放計算、環境和社會報告系統(ESRS)映射以及支持鑑證的記錄保存相關的軟體需求仍然強勁。綜合指令I將義務範圍縮小至超過新增員工人數和收入閾值的公司,導致部分中型企業的短期需求減少。儘管如此,法國綠色IT軟體市場仍在持續受益,因為符合資格的公司會透過採購和合規性審計向供應商索取永續發展數據。法國金融市場管理局(AMF)的監管以及對符合審計標準的揭露要求,持續推動著能夠進行資料品質追蹤、控制支援和第三方鑑證記錄保存的軟體的發展。

企業對IT排放視覺化的需求日益成長

法國綠色IT軟體市場正受益於對環境影響測量的迫切需求,因為企業再也無法忽視其數位化營運對環境的影響。根據法國環境與能源管理署(ADEME)和法國能源政策研究中心(ARCEP)的研究,法國數位產業佔該國碳足跡的4.4%(2,950萬噸二氧化碳當量),其中資料中心佔46%,終端佔50%。預計到2025年,接入公共電網的資料中心的電力消耗將接近1太瓦時(TWh),高於2024年的0.8太瓦時,這凸顯了加強基礎設施使用監測和改善報告系統的必要性。 ARCEP的2025年環境調查預測,Orange、Bouygues Telecom、SFR和Iliad這四家公司的範圍2排放總合將達到39.7萬噸二氧化碳當量,儘管全國排放有所下降,但仍將同比成長4.2%。這進一步強調了特定產業追蹤工具的必要性。儘管法國的低碳電網使國內與電力相關的排放相對較低,但法國綠色 IT 軟體市場的許多公司卻被迫更加重視使用進口數位服務、依賴海外託管以及更廣泛的範圍 3 計算。

遺留環境中的 IT 和設施資料碎片化

法國綠色IT軟體市場面臨的一個長期挑戰是,許多公司仍缺乏涵蓋其所有IT設備、設施和託管環境的準確資產級數據。 ESRS E1報告要求提供伺服器、網路硬體、設備和能源使用情況的詳細輸入數據,但傳統的IT服務管理系統在設計之初並未考慮這種等級的環境測量。 ARCEP的2025年環境調查顯示,即使是已經習慣結構化報告的大型通訊業者,在收集詳細的設備級數據方面仍面臨挑戰。 ADEME更新了其2025年針對託管IT和電信服務的調查方法,但中小企業和私營部門的採用率仍參差不齊。這意味著,如果資產帳簿不完整、電錶規格不統一或資料基礎設施不足以滿足報告要求,則軟體的價值可能無法充分發揮。

細分市場分析

預計到2025年,軟體收入將佔總收入的76.14%,這表明訂閱式平台仍然是法國綠色IT軟體市場的主要支出類別。碳核算、ESG報告、永續發展資料管理和能源最佳化主要透過SaaS模式提供。這種模式允許供應商集中更新報告規則,從而減少客戶的維護工作。這種模式在法國尤其有效,因為法國的報告義務不斷變化,企業希望在資訊揭露要求變更時盡可能減少手動調整。因此,法國綠色IT軟體產業繼續秉持「軟體優先」的理念,因為與一次性的內部開發相比,定期更新的平台能夠更有效地應對監管變化。

服務業仍然至關重要,因為軟體通常需要實施、諮詢服務和受控報告支援才能交付可靠的結果。預計到2031年,服務業的複合年成長率將達到16.91%,使其成為法國綠色IT軟體市場成長最快的領域。許多公司仍然缺乏能夠界定排放範圍、協調方法論並準備符合審計要求的工作流程的內部永續發展專家。Schneider Electric在其最新的《2026-2030影響》報告中指出,其諮詢網路擁有超過4000名顧問,這表明大型企業客戶在實施過程中需要大規模的支援。此外,小規模的專業公司也在這個領域找到了自己的定位,因為法國的中型客戶往往更傾向於符合國家報告規範的在地化指導和實際操作的實施支援。

到2025年,基於雲端的部署將佔法國綠色IT軟體市場64.17%的佔有率,這證實了供應商管理的交付模式仍然是許多企業買家的首選。其主要優勢不僅在於便利性,還在於能夠適應ESRS規則、分類揭露和報告範本的持續更新,而無需經歷漫長的內部升級週期。對許多公司而言,SaaS模式縮短了部署時間,並減輕了本已不堪重負的IT團隊的負擔。因此,即使報告要求日益複雜,雲端交付在法國綠色IT軟體市場仍佔據核心地位。

預計到2031年,混合部署將以17.02%的複合年成長率成長。主要原因是受監管行業對永續發展數據的處理和儲存日益成長的控制需求。銀行、保險、政府和醫療保健行業的使用者通常更傾向於使用國內或嚴格控制的基礎設施來儲存敏感的營運和報告資料。這種需求正在推動混合架構的發展,該架構將雲端的柔軟性與本地管理要求相結合。本地部署仍然存在於工業和國防相關環境中,但隨著供應商專注於基於雲端和混合的產品戰略,其作用正在逐漸減弱。 OVHcloud等供應商提供的自主雲端和私有雲端解決方案也有助於彌合合規性要求與外部託管便利性之間的差距。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業對IT排放視覺化的需求日益成長

- 歐盟和法國在脫碳方面面臨越來越大資訊揭露的壓力

- 拓展雲端成本和能源最佳化的應用場景。

- 企業採購商的永續性採購要求

- 實現整個 IT 資產組合的 ESG 報表自動化

- 利用人工智慧進行工作負載最佳化,以提高資料中心效率

- 市場限制因素

- IT 和設施資料分佈在整個遺留環境中

- 中型企業內部碳計量成熟度較低

- 與現有 ITSM、ERP 和雲端堆疊整合的複雜性。

- 優先將預算分配給核心網路安全和雲端項目

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體

- 服務

- 不同的發展

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 按解決方案類型

- 碳管理和運算軟體

- ESG報告和合規軟體

- 永續性資料管理平台

- 脫碳規劃軟體

- 能源和資源最佳化軟體

- 最終用戶

- 資訊科技/通訊

- BFSI

- 製造業

- 能源公用事業

- 零售與電子商務

- 政府

- 衛生保健

- 建築和基礎設施

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Salesforce, Inc.

- Microsoft Corporation

- SAP SE

- IBM Corporation

- Schneider Electric SE

- ServiceNow, Inc.

- Accenture plc

- Oracle Corporation

- Workiva Inc.

- Sphera Solutions, Inc.

- Persefoni AI, Inc.

- Watershed Technologies, Inc.

- Plan A Solutions GmbH

- Sweep SAS

- Greenly SAS

- Plan A Solutions GmbH

- Emitwise Ltd.

- Enablon SAS

- EcoVadis SAS

- Siemens AG

- Wolters Kluwer NV

- Dakota Software Corporation

- InnoGreen Technologies

- Sopra Steria

- OneStop ESG

- Tata Consultancy Services

第7章 市場機會與未來展望

According to Mordor Intelligence, the france green IT software market is expected to grow from USD 0.98 billion in 2025 to USD 1.12 billion in 2026, and reach USD 2.42 billion by 2031, at a CAGR of 16.66% over 2026-2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, and Energy and More), End User (IT and Telecom, BFSI, Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

France Green IT Software Market Trends and Insights

Strengthening EU and France Decarbonization Disclosure Pressure

France moved ahead of many other European countries in implementing CSRD-related obligations, which gave local enterprises less time to delay platform selection and data preparation for sustainability reporting. Large listed companies had already begun filing under the new framework in 2025, and other large companies are reporting in 2026 for the financial year 2025, which kept software demand tied to emissions accounting, ESRS mapping, and assurance-ready records. The Omnibus I Directive narrowed the mandatory scope to companies above the new employee and turnover thresholds, and that change reduced part of the direct mid-market pipeline in the short term. Even so, the France green IT software market still benefits when in-scope companies push sustainability data requests into their supplier base through procurement and compliance reviews. Oversight from the AMF and the need for audit-grade disclosures continue to favor software that can trace data quality, support controls, and prepare records for third-party assurance.

Rising Corporate Demand For IT Emissions Visibility

The France green IT software market is gaining from a basic measurement need, because the environmental weight of digital operations is now harder for enterprises to ignore. The ADEME and ARCEP study showed that the French digital sector accounted for 4.4% of the national carbon footprint, or 29.5 MtCO2e, with data centers contributing 46% and terminals 50% of that total. Electricity use at data centers connected to the public transmission network reached almost 1 TWh in 2025, up from 0.8 TWh in 2024, underscoring the need for closer monitoring of infrastructure use and stronger reporting controls. ARCEP's 2025 environmental survey also showed that Orange, Bouygues Telecom, SFR, and Iliad recorded aggregate scope 2 emissions of 397,000 tCO2e, a 4.2% year-on-year increase even as national emissions declined, reinforcing the case for sector-specific tracking tools. France's low-carbon grid keeps domestic electricity emissions comparatively low, but that pushes many companies to focus more closely on imported digital use, overseas hosting exposure, and broader scope 3 accounting within the France green IT software market.

Fragmented IT and Facilities Data Across Legacy Environments

A persistent constraint in the France green IT software market is that many companies still do not have clean, asset-level data across IT equipment, facilities, and hosting environments. ESRS E1 reporting needs detailed inputs for servers, network hardware, devices, and energy use, but legacy IT service management systems were not built for that level of environmental measurement. ARCEP's 2025 environmental survey showed that equipment-level granularity remains difficult, even for large telecommunications operators already accustomed to structured reporting. ADEME updated its methodological framework for hosted IT and cloud services in 2025, yet adoption remains uneven across smaller operators and private environments. This means software value can fall short when inventories are incomplete, energy meters are inconsistent, and the underlying data structure is weaker than the reporting requirement.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cloud Cost and Energy Optimization Use Cases

- Sustainability Procurement Requirements From Enterprise Buyers

- Integration Complexity With Existing ITSM, ERP, and Cloud Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 76.14% of revenue in 2025, indicating that subscription platforms remain the core spending category in the France green IT software market. Carbon accounting, ESG reporting, sustainability data management, and energy optimization are primarily delivered through SaaS models that enable vendors to centrally update reporting rules and reduce client maintenance work. That model is useful in France, where reporting obligations continue to change, and enterprises want fewer manual adjustments each time disclosure expectations shift. The France green IT software industry therefore keeps leaning toward software first, because recurring platforms can absorb regulatory updates more efficiently than one-off internal builds.

Services are still important because implementation, advisory work, and managed reporting support are often needed before software can produce reliable results. Services are projected to grow at a 16.91% CAGR through 2031, making them the fastest-growing segment of the France green IT software market. Many companies still lack internal sustainability specialists who can structure emissions boundaries, align methods, and prepare audit-ready workflows. Schneider Electric's advisory network, which exceeded 4,000 consultants in its 2026 Impact 2030 update, shows the scale of support that large enterprise customers are seeking around these deployments. Smaller specialist firms are also finding room in this segment because mid-sized French clients often prefer local guidance tied to national reporting practices and practical onboarding.

Cloud-based deployment captured 64.17% of the France green IT software market size in 2025, which confirms that vendor-managed delivery is the preferred model for many enterprise buyers. The main advantage is not only convenience, but also the ability to handle continuous updates in ESRS rules, taxonomy disclosures, and reporting templates without long internal upgrade cycles. For many enterprises, the SaaS approach also shortens implementation and reduces the burden on already stretched IT teams. This keeps cloud delivery at the center of the France green IT software market even as reporting needs become more complex.

Hybrid deployment is projected to grow at a 17.02% CAGR through 2031, mainly because regulated sectors need more control over where sustainability data is processed and stored. Banking, insurance, government, and healthcare users often want domestic or tightly governed infrastructure for sensitive operational and reporting data. This demand is sustaining hybrid architectures that mix cloud flexibility with local control requirements. On-prem deployments still exist in industrial and defense-linked settings, but their role is gradually narrowing as vendors focus more on cloud- and hybrid-based product paths. Sovereign and private cloud arrangements from providers such as OVHcloud are also helping bridge the gap between compliance concerns and the convenience of external hosting.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By End User

- IT and Telecom

- BFSI

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Government

- Healthcare

- Construction and Infrastructure

- Other End-User Industries

List of Companies Covered in this Report:

- Salesforce, Inc.

- Microsoft Corporation

- SAP SE

- IBM Corporation

- Schneider Electric SE

- ServiceNow, Inc.

- Accenture plc

- Oracle Corporation

- Workiva Inc.

- Sphera Solutions, Inc.

- Persefoni AI, Inc.

- Watershed Technologies, Inc.

- Plan A Solutions GmbH

- Sweep SAS

- Greenly SAS

- Plan A Solutions GmbH

- Emitwise Ltd.

- Enablon SAS

- EcoVadis SAS

- Siemens AG

- Wolters Kluwer N.V.

- Dakota Software Corporation

- InnoGreen Technologies

- Sopra Steria

- OneStop ESG

- Tata Consultancy Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Corporate Demand for IT Emissions Visibility

- 4.2.2 Strengthening EU and France Decarbonization Disclosure Pressure

- 4.2.3 Expansion Of Cloud Cost And Energy Optimization Use Cases

- 4.2.4 Sustainability Procurement Requirements From Enterprise Buyers

- 4.2.5 Automation Of ESG Reporting Across IT Asset Portfolios

- 4.2.6 AI-Driven Workload Optimization For Data Center Efficiency

- 4.3 Market Restraints

- 4.3.1 Fragmented IT And Facilities Data Across Legacy Environments

- 4.3.2 Limited Internal Carbon Accounting Maturity In Mid-Market Firms

- 4.3.3 Integration Complexity With Existing ITSM, ERP, And Cloud Stacks

- 4.3.4 Budget Prioritization Toward Core Cybersecurity And Cloud Projects

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Intensity of Competitive Rivalry

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of New Entrants

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Solution Type

- 5.4.1 Carbon Management and Accounting Software

- 5.4.2 ESG Reporting and Compliance Software

- 5.4.3 Sustainability Data Management Platforms

- 5.4.4 Decarbonization Planning Software

- 5.4.5 Energy and Resource Optimization Software

- 5.5 By End User

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Government

- 5.5.7 Healthcare

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Salesforce, Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 SAP SE

- 6.4.4 IBM Corporation

- 6.4.5 Schneider Electric SE

- 6.4.6 ServiceNow, Inc.

- 6.4.7 Accenture plc

- 6.4.8 Oracle Corporation

- 6.4.9 Workiva Inc.

- 6.4.10 Sphera Solutions, Inc.

- 6.4.11 Persefoni AI, Inc.

- 6.4.12 Watershed Technologies, Inc.

- 6.4.13 Plan A Solutions GmbH

- 6.4.14 Sweep SAS

- 6.4.15 Greenly SAS

- 6.4.16 Plan A Solutions GmbH

- 6.4.17 Emitwise Ltd.

- 6.4.18 Enablon SAS

- 6.4.19 EcoVadis SAS

- 6.4.20 Siemens AG

- 6.4.21 Wolters Kluwer N.V.

- 6.4.22 Dakota Software Corporation

- 6.4.23 InnoGreen Technologies

- 6.4.24 Sopra Steria

- 6.4.25 OneStop ESG

- 6.4.26 Tata Consultancy Services

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)

中國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區綠色IT軟體:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印尼綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)越南綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)馬來西亞綠色IT軟體:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲綠色IT軟體:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年) 2026年全球數位測量和圖解決方案市場報告

2026年全球數位測量和圖解決方案市場報告 2026-2030年全球數位化製造軟體市場

2026-2030年全球數位化製造軟體市場