|

市場調查報告書

商品編碼

2073270

能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Digital Workplace In Energy and Utilities - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

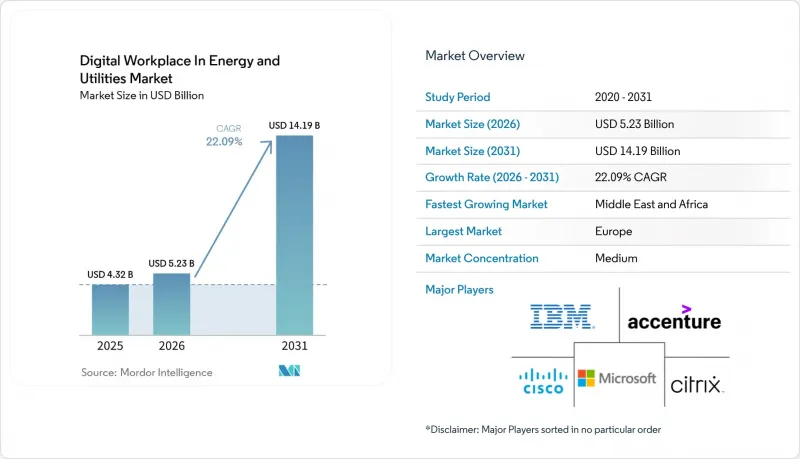

根據 Mordor Intelligence 預測,能源和公共產業行業的數位化工作場所市場規模將從 2025 年的 43.2 億美元和 2026 年的 52.3 億美元成長到 2031 年的 141.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 2.09%。

本報告按元件[解決方案(整合通訊與協作、統一端點管理、企業行動管理等)和服務]、部署模式(雲端、本地部署等)、組織規模(大型企業和中小企業)以及地區進行細分。市場規模和預測均以美元計價。

公共產業的趨勢和洞察。

混合型和分散式勞動力的數位化

儘管完全遠距辦公的比例已從先前的高峰有所下降,但公共產業仍在持續成長,這主要得益於混合辦公模式的興起。預計到2026年,62%的企業將強制要求員工固定到崗,高於2025年的49%。這表明,企業現在需要能夠同時支援辦公室、現場和分散式團隊的訪問、線上狀態、日程安排和協作的工具。實際辦公室利用率與目標辦公室利用率之間的差距從2025年的25個百分點縮小到2026年的18個百分點,每週工作3-4天的員工比例也增加了19個百分點,達到55%。這表明,結構化的混合辦公模式正在成為一種成熟的營運模式,而不再只是臨時調整。這對能源和公共產業行業的數位化工作場所至關重要,因為公共產業、電網營運商和能源服務公司必須在一個統一的、管治的平台上協調辦公室員工、現場工作人員和受監管的工作流程。能夠將終端控制、協作和員工視覺性整合到同一環境中的供應商,在吸引企業新投資方面具有強大的優勢。

人工智慧驅動的搜尋和知識搜尋

從關鍵字搜尋到基於人工智慧的知識搜尋的轉變正在改變企業建立數位化工作的方式。亞馬遜雲端服務 (AWS) 於 2026 年 6 月正式發布了 Bedrock Managed Knowledge Base,為企業提供了一種無需自行管理複雜向量資料庫即可部署知識搜尋系統的方法。能源和公共產業行業的數位化工作場所也面臨類似的壓力,因為現場和辦公室使用者在日常工作流程中越來越需要基於權限存取技術文件、維護記錄和政策內容。儘管經營團隊期望生成式人工智慧能夠推動成長,但其應用仍處於成熟階段,知識搜尋和管治仍是大規模部署的障礙。因此,人工智慧搜尋不再被視為可選的高級功能,隨著企業內部代理的使用範圍不斷擴大,在架構層面整合知識的平台正在獲得優勢。

網路安全和資料主權問題

網路安全和資料主權仍然是能源和公共產業行業數位化工作場所普及速度的主要限制因素。富士通在2026年5月發布的報告顯示,只有8%的組織能夠在部署後控制人工智慧系統的學習和運作方式,凸顯了隨著工作場所資料輸入人工智慧工具,管治風險會迅速升級。在歐洲,將於2026年8月2日生效的歐盟人工智慧法案將進一步明確職場人工智慧的義務,包括員工通知要求和相關系統的日誌保留要求。這些要求延長了審計週期,促使採購方優先考慮那些能夠提供更強大的控制、可審計性和區域託管選項的平台。為了應對這一壓力,Orange Business於2026年3月在其位於法國的自有託管基礎設施上推出了「即時協作」服務,這表明合規性的複雜性以及產品設計正在影響供應商的市場定位。

細分市場分析

預計到2025年,解決方案將佔總收入的64.38%,而能源和公共產業領域的數位化工作場所預計將實現最高成長率,到2031年複合年成長率將達到22.93%。這表明,買家更傾向於選擇整合通訊、終端管治、行動性、工作流程自動化和知識存取等功能的解決方案套件,而非單一功能工具。整合通訊與協作、統一終端管理、企業行動管理、員工體驗平台、工作流程自動化和虛擬桌面基礎架構均屬於此範疇,並且是新部署的主要投資目標。因此,能源和公共產業領域的數位化工作場所市場正朝著平台整合而非工具基礎架構碎片化的方向發展。

到2025年,服務將佔據剩餘的市場佔有率,隨著解決方案部署需要管治、調優、變更管理和託管支持,服務的角色將變得日益關鍵。在能源和公共產業行業的數位化工作場所,對服務的需求正從基本的部署任務轉向對人工智慧管治、工作流程最佳化和員工體驗管理的長期支援。 Unily於2026年6月發布的「Indi」只需一條自然語言提示即可產生管治的內網環境,這展示了解決方案供應商如何提升客戶所需的部署後服務和配置支援等級。隨著工作場所平台自主功能的擴展,企業將需要持續監控而非一次性設置,這將促使服務採用率的提高。這種轉變將使能夠同時支援軟體層和周邊營運模式的供應商和合作夥伴受益。

區域分析

到2025年,歐洲將在公共產業佔據31.52%的佔有率,成為基準年最大的區域貢獻者。德國、英國和法國將繼續是主要的需求中心,而荷蘭和北歐國家也將透過提升數位化成熟度來支持市場發展。根據德國資訊科技協會(Bitkom)的研究,到2026年,41%的德國公司將在其業務流程中使用人工智慧,高於2025年的17%,而已採用人工智慧的公司中有77%表示其競爭力得到了顯著提升。 2026年6月,Atos和微軟將基於代理的安全人工智慧部署擴展到Atos在54個國家的56,000名員工。這表明,即使在合規要求日益提高的情況下,歐洲大型企業仍在推動大規模採用人工智慧。歐盟人工智慧法律為該地區的趨勢增添了新的要素,因為現在在職場部署人工智慧需要更加重視員工通知、日誌記錄和課責管治。

北美仍然是能源和公共產業領域數位化工作場所需求的第二大市場,這得益於其成熟的雲端基礎設施、協作軟體的廣泛應用以及企業在人工智慧方面的高額投入。亞太地區緊隨其後,其中以中國、日本、印度和韓國主導。在這些國家,大規模的工業和技術生態系統為辦公室和現場應用場景的工作場所現代化提供了支援。印度憑藉其強大的IT服務基礎設施繼續發揮重要作用,而日本和韓國對可擴展至生產和營運環境的終端和工作流程工具的需求也在不斷成長。南美洲的市場基數小規模,但成長迅速,巴西和哥倫比亞在雲端定價更親民以及行動優先的工作方式擴大目標客戶群方面處於領先地位。

儘管中東和非洲地區在2025年的基數較小,但預計到2031年,公共產業將達到最高成長率,複合年成長率(CAGR)將達到23.65%。這一成長得益於政府主導的雲端運算投資、國家級人工智慧專案以及大中小型企業數位化應用的不斷普及。微軟沙烏地阿拉伯Azure資料中心區域已於2026年1月正式上線,為受監管產業拓展了本地資料儲存選擇,並增強了波灣合作理事會(GCC)的雲端運算應用環境。在非洲,政府主導的數位化計畫和不斷擴大的行動寬頻存取也在推動數位化應用。尤其是在南非、奈及利亞、肯亞和埃及,以現場作業為主的產業可以從行動優先的工作場所平台中獲益。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 混合型和分散式勞動力的數位化

- 對取得安全關鍵知識的需求

- OT和IT工作流程的整合

- 人工智慧驅動的搜尋和知識搜尋

- 為現場負責人打造「行動優先」的工作環境

- 監管壓力對符合審計要求的合作構成挑戰

- 市場限制因素

- 舊有系統和身分碎片化

- 網路安全和資料主權問題

- 現場負責人和承包商的採用率很低。

- OT和企業應用程式整合的複雜性

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 整合通訊與協作

- 整合端點管理

- 企業行動管理

- 員工體驗平台與內網

- 工作流程自動化與知識管理

- 虛擬桌面基礎架構與雲端電腦

- 服務

- 解決方案

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 北歐的

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- IBM Corporation

- Accenture plc

- Cisco Systems, Inc.

- Omnissa, Inc.

- Citrix Systems, Inc.

- HCL Technologies Limited

- Wipro Limited

- Infosys Limited

- NTT DATA Group Corporation

- Capgemini SE

- DXC Technology Company

- Atos SE

- AvePoint, Inc.

- Unily Group Ltd

- Claromentis Limited

- Workai Sp. z oo

- Nutanix, Inc.

- SAP SE

- Oracle Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the digital workplace in energy and utilities market size is projected to expand from USD 4.32 billion in 2025 and USD 5.23 billion in 2026 to USD 14.19 billion by 2031, registering a CAGR of 22.09% between 2026 and 2031.

This report is Segmented by Component [Solutions (Unified Communication and Collaboration, Unified Endpoint Management, Enterprise Mobility Management, and More), and Services], Deployment Mode (Cloud, On-Premise, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Digital Workplace In Energy and Utilities Market Trends and Insights

Hybrid and Distributed Workforce Digitization

The digital workplace in energy and utilities market continues to gain from the normalization of hybrid work, even though fully remote work has fallen from its earlier peak. In 2026, 62% of organizations mandate fixed in-office days, up from 49% in 2025, indicating that enterprises now need tools that support access, presence, scheduling, and collaboration across office, field, and distributed teams simultaneously. The gap between actual and target office utilization narrowed to 18 percentage points in 2026 from 25 in 2025, and employees attending 3-4 days per week rose by 19 percentage points to 55%, indicating that structured hybrid work is becoming an operating model rather than a temporary adjustment. In the digital workplace in energy and utilities market, this matters because utilities, grid operators, and energy service firms must now coordinate office staff, field crews, and regulated workflows within a single, governed platform. Vendors that can combine endpoint control, collaboration, and workforce visibility in the same environment are better placed to win new enterprise spending.

AI-Assisted Search and Knowledge Retrieval

The shift from keyword search to AI-based knowledge retrieval is changing how organizations structure digital work. Amazon Web Services made Bedrock Managed Knowledge Base generally available in June 2026, giving enterprises a way to deploy retrieval systems for their proprietary data without managing the complexity of vector databases themselves. The digital workplace in energy and utilities market is responding to the same pressure, as frontline and office users increasingly need permission-aware access to technical documents, maintenance records, and policy content within daily workflows. Executives expect generative AI to support growth, but deployment maturity remains low, which shows that knowledge retrieval and governance are still limiting scaled adoption. As a result, AI search is no longer treated as an optional premium feature, and the platforms that unify knowledge at the architecture layer are gaining an advantage as enterprise agent use expands.

Cybersecurity and Data Sovereignty Concerns

Cybersecurity and data sovereignty remain major constraints on deployment speed in the digital workplace in energy and utilities market. Fujitsu reported in May 2026 that only 8% of organizations can control how their AI systems learn and behave after deployment, underscoring how quickly governance exposure can widen as workplace data feeds AI tools. In Europe, the EU AI Act will start to make workplace AI obligations more concrete, including worker notification requirements and log retention expectations for relevant systems, effective from August 2, 2026. These requirements lengthen review cycles and push buyers to favor platforms that offer stronger control, auditability, and regional hosting options. Orange Business responded to this pressure in March 2026 with the launch of Live Collaboration on sovereign infrastructure in France, which shows that compliance complexity is now shaping vendor positioning as much as product design.

Other drivers and restraints analyzed in the detailed report include:

- OT and IT Workflow Convergence

- Safety-Critical Knowledge Access Demand

- Legacy Systems and Identity Fragmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 64.38% of revenue in 2025 and are also projected to record the fastest 22.93% CAGR through 2031 in the digital workplace in energy and utilities market. This shows that buyers are prioritizing integrated suites over narrow point tools as they connect communication, endpoint governance, mobility, workflow automation, and knowledge access. Unified communication and collaboration, unified endpoint management, enterprise mobility management, employee experience platforms, workflow automation, and virtual desktop infrastructure all sit within this layer, making it the core spending destination for new deployments. The digital workplace in energy and utilities market is therefore moving toward platform consolidation rather than a more fragmented tool base.

Services represented the balance of the market in 2025, and their role is becoming more important as solution rollouts now require governance, tuning, change management, and managed support. In the digital workplace of the energy and utilities industry, service demand is shifting away from basic implementation work toward long-term support for AI governance, workflow optimization, and employee experience management. Unily's June 2026 launch of Indi, which generates governed intranet environments from a single natural-language prompt, shows how solution providers are raising the level of post-deployment service and configuration support that customers will need. As autonomous features expand inside workplace platforms, services are likely to become stickier because organizations will need ongoing oversight instead of one-time setup. That shift favors vendors and partners that can support both the software layer and the operational model around it.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

Europe held 31.52% of the digital workplace market share in energy and utilities in 2025, making it the largest regional contributor in the base year. Germany, the United Kingdom, and France remained the main demand centers, while the Netherlands and the Nordic countries added support through stronger digital maturity. Bitkom found that 41% of German companies used AI in business processes in 2026, up from 17% in 2025, and that 77% of AI adopters reported a measurable improvement in their competitive position. Atos and Microsoft expanded secure agentic AI deployment to 56,000 Atos employees across 54 countries in June 2026, which shows that large European enterprises are moving ahead with scaled activation even as compliance expectations rise. The EU AI Act is adding another layer to this regional profile, as workplace AI deployment now requires greater attention to worker notification, logging, and accountable governance.

North America remained the second-largest demand pool in the digital workplace in energy and utilities market because of its mature cloud base, strong collaboration software footprint, and high level of AI-related enterprise spending. Asia-Pacific ranked next, led by China, Japan, India, and South Korea, where large industrial and technology ecosystems support workplace modernization across both office and frontline use cases. India continues to matter through its deep IT services base, while Japan and South Korea create additional demand for endpoint and workflow tools that can extend into production and operational settings. South America is growing from a smaller base, with Brazil and Colombia leading adoption as cloud affordability and mobile-first work patterns widen the addressable customer pool.

The Middle East and Africa held a smaller base in 2025, but it is projected to record the fastest 23.65% CAGR through 2031 in the digital workplace in energy and utilities market. Growth is being supported by sovereign cloud investment, national AI programs, and expanding digital adoption among both large enterprises and SMEs. Microsoft's Saudi Arabia Azure datacenter region reached general availability in January 2026, which improved local data residency options for regulated industries and strengthened cloud deployment conditions across the Gulf Cooperation Council. Across Africa, adoption is also gaining support from state-led digitization programs and wider mobile broadband access, especially in South Africa, Nigeria, Kenya, and Egypt, where field-intensive sectors can benefit from mobile-first workplace platforms.

- Microsoft Corporation

- IBM Corporation

- Accenture plc

- Cisco Systems, Inc.

- Omnissa, Inc.

- Citrix Systems, Inc.

- HCL Technologies Limited

- Wipro Limited

- Infosys Limited

- NTT DATA Group Corporation

- Capgemini SE

- DXC Technology Company

- Atos SE

- AvePoint, Inc.

- Unily Group Ltd

- Claromentis Limited

- Workai Sp. z o.o.

- Nutanix, Inc.

- SAP SE

- Oracle Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid and Distributed Workforce Digitization

- 4.2.2 Safety-Critical Knowledge Access Demand

- 4.2.3 OT and IT Workflow Convergence

- 4.2.4 AI Assisted Search and Knowledge Retrieval

- 4.2.5 Mobile First Enablement for Field Personnel

- 4.2.6 Regulatory Pressure for Audit Ready Collaboration

- 4.3 Market Restraints

- 4.3.1 Legacy Systems and Identity Fragmentation

- 4.3.2 Cybersecurity and Data Sovereignty Concerns

- 4.3.3 Low Adoption Among Field and Contractor Users

- 4.3.4 Integration Complexity Across OT and Enterprise Apps

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Colombia

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Netherlands

- 5.4.3.7 Nordics

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Southeast Asia

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Israel

- 5.4.5.5 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Kenya

- 5.4.6.5 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Accenture plc

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Omnissa, Inc.

- 6.4.6 Citrix Systems, Inc.

- 6.4.7 HCL Technologies Limited

- 6.4.8 Wipro Limited

- 6.4.9 Infosys Limited

- 6.4.10 NTT DATA Group Corporation

- 6.4.11 Capgemini SE

- 6.4.12 DXC Technology Company

- 6.4.13 Atos SE

- 6.4.14 AvePoint, Inc.

- 6.4.15 Unily Group Ltd

- 6.4.16 Claromentis Limited

- 6.4.17 Workai Sp. z o.o.

- 6.4.18 Nutanix, Inc.

- 6.4.19 SAP SE

- 6.4.20 Oracle Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)