|

市場調查報告書

商品編碼

2073232

中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Middle East and Africa Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

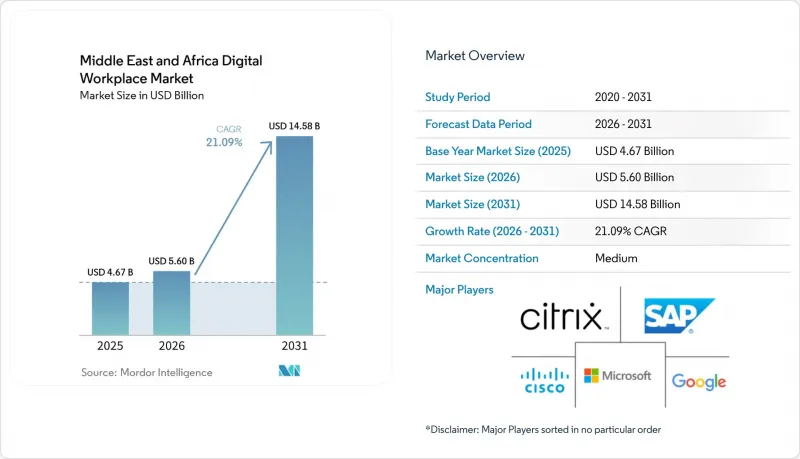

根據 Mordor Intelligence 預測,中東和非洲的數位工作場所市場規模將從 2025 年的 46.7 億美元和 2026 年的 56 億美元成長到 2031 年的 145.8 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 21.09%。

本報告按組件(解決方案和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、最終用戶行業(IT和電信、銀行、金融服務和保險、醫療保健、政府和公共部門、教育等)以及地區進行細分。市場規模和預測均以美元計價。

中東和非洲數位化工作場所市場的趨勢和洞察

分散式企業對混合辦公模式的需求日益成長

在中東和非洲地區,混合辦公模式已不再局限於短期僱用安排,而是成為許多大型企業的基本營運需求。在中東和非洲的數位化工作場所市場,這種需求在同時管理大規模專案現場、多個辦公室、現場團隊和跨境營運的組織中最為強烈。沙烏地阿拉伯大型企劃的部署進一步提升了遠端辦公地點、指揮中心和總部之間持續協調的需求,以維持協作和設備管理。思科在沙烏地阿拉伯的大規模業務擴張計畫(包括對雲端服務、資料中心、本地生產計畫和人工智慧人才發展的支援)強化了互聯工作場所環境所需的基礎設施。在南非和奈及利亞等非洲市場,企業在評估工作場所平台時,往往更重視員工在不同辦公地點之間的流動性,而非居家遠距辦公。因此,能夠整合通訊、終端管理、多語言支援和安全存取等功能的供應商,在中東和非洲的數位化工作場所市場中佔據了有利地位,有望抓住新引進週期。

加速將工作場所基礎架構遷移到雲端

在中東和非洲的數位化辦公市場,雲端遷移正日益被視為一項合規性和營運模式的決策,而不僅僅是成本問題。在沙烏地阿拉伯和阿拉伯聯合大公國(阿拉伯聯合大公國),由於政府部門、銀行和其他受監管機構需要本地託管認證以及對敏感資料實施更嚴格的管控,一些公司的雲端遷移進程較為緩慢。微軟已確認,沙烏地阿拉伯東部地區將於2026年第四季開始支援客戶的工作負載。這將為雲端工作負載和辦公室應用增加一個國內可用區,從而降低這些障礙。 e&enterprise 的 OneCloud 服務也反映了阿拉伯聯合大公國的類似轉變,該國正在開發由政府主導的超大規模基礎設施,以支援其國內資料中心環境中的雲端和人工智慧工作負載。隨著這些選擇的增加,更多買家將能夠在不影響資料居住要求或服務連續性的前提下,實現其生產力套件的現代化。因此,對於那些先前因監管原因而不得不採用傳統本地部署模式的組織而言,採用雲端原生辦公平台也變得更加容易。

各國數位基礎設施的品質參差不齊。

各國基礎設施品質差異巨大,導致中東和非洲數位化辦公市場在準備程度上有顯著差異。微軟發布的《2026 年第一季全球人工智慧應用報告》揭示了數位化準備和可靠存取的鮮明對比:南非工作年齡人口對生成式人工智慧的採用率高達 23.1%,而奈及利亞僅為 10.1%。隨著供應商將業務拓展到海灣合作理事會 (GCC) 國家和南非以外的地區,這種差異直接影響辦公室軟體市場,因為這些供應商往往需要在雲端優先架構中採用低頻寬、混合或離線部署等方案。電力不穩定和寬頻品質波動會導致部署週期延長、使用者體驗下降,並降低協作密集型工作負載的可靠性。儘管買家可能仍需要最新的工具,但在運作難以保障的市場中,實際部署的風險仍然很高。因此,即使企業對相關產品表現出明顯的興趣,潛在的市場機會也遠未達到其應有的水平。

細分市場分析

到2025年,該解決方案將在中東和非洲的數位化工作場所市場佔據69.56%的佔有率,從而在全部區域確立主導地位。這一地位反映了市場對整合套件的持續需求,該套件將通訊、終端管理、行動辦公、員工支援、工作流程工具和桌面虛擬化整合到一個統一的管理環境中。隨著企業要求減少供應商數量、簡化介面並加強對分散員工的管治,中東和非洲的數位化工作場所市場正朝著平台整合的方向發展。買家也面臨著保持其工作場所管理結構可審計性的壓力,這自然促使他們傾向於選擇綜合解決方案堆疊,而不是分散的獨立產品。虛擬桌面基礎架構 (VDI) 和雲端PC工具在政府、銀行以及石油和天然氣行業越來越受歡迎,透過本地託管和集中管理,有助於緩解資料儲存和存取方面的擔憂。

預計從2026年第四季開始,微軟在沙烏地阿拉伯東部地區的雲端PC和託管桌面將得到更廣泛的應用,尤其是在那些先前一直在等待本地服務可用才擴展其雲端工作環境的企業中。到2025年,服務將佔據剩餘的30.44%市場佔有率,這表明實施、託管支援和諮詢服務對於企業部署仍然至關重要。許多企業仍然缺乏必要的內部團隊來全面部署策略層、使用者體驗流程、整合和安全控制。即使解決方案套件佔據了大部分收入,服務仍然至關重要,因為如果沒有強大的設置和營運支持,單靠軟體購買幾乎沒有任何價值。此外,來自阿拉伯聯合大公國的海外託管服務供應商日益成長的興趣表明,隨著部署規模和複雜性的增加,中東和非洲地區數位化工作場所市場服務層的競爭正在加劇。

預計到2025年,雲端運算將佔據63.19%的市場佔有率,中東和非洲數位化工作場所市場的雲端運算採用率預計到2031年將以22.56%的複合年成長率成長。本地超大規模區域的出現進一步提振了成長前景,解決了合規性要求與可擴展雲端營運之間長期存在的衝突。對於許多買家,尤其是政府部門和受監管行業而言,本地託管的可用性已將雲端運算從單純的政策問題轉變為現代化的實際途徑。微軟的「沙烏地阿拉伯東部」區域將增強企業在需要本地資料駐留和業務永續營運計畫的雲端工作場所部署方面的信心。

對於需要空氣間隙環境並對系統和數據進行更嚴格物理控制的政府部門、國防機構以及石油和天然氣公司而言,本地部署仍然至關重要。這意味著中東和非洲的數位化工作場所市場不會採用單一的部署模式,因為安全態勢和運作環境仍然會因買家類型而異。混合配置也越來越受到大型企業的青睞,這些企業出於延遲和管理方面的考慮,希望將某些工作負載保留在本地,同時又希望藉助雲端編配進行協作和分析。當營運技術 (OT) 和辦公室技術 (IT) 需要共存但又無法共用相同託管模型時,這種趨勢尤其明顯。經過認證的雲端安全標準繼續青睞那些能夠證明其可審計性、彈性和本地服務支援的供應商,這進一步鞏固了準備充分的供應商在中東和非洲數位化工作場所市場的地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 分散式企業對混合式辦公解決方案的需求日益成長

- 加速將職場基礎架構遷移到雲端

- 對安全終端和身分管理的需求日益成長。

- 擴大員工體驗平台和數位化入口的應用

- 拓展工作流程自動化與知識管理的應用場景。

- 受法規環境中對虛擬桌面基礎架構 (VDI) 和雲端 PC 的需求日益成長

- 市場限制因素

- 各國數位基礎設施品質存在差異

- 預算限制和較長的企業銷售週期

- 資料主權和跨境合規的複雜性

- 碎片化的舊有應用程式環境和整合負擔

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 整合通訊與協作

- 統一端點管理

- 企業行動管理

- 員工體驗平台與內網

- 工作流程自動化與知識管理

- 虛擬桌面基礎架構與雲端電腦

- 服務

- 解決方案

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 衛生保健

- 製造業

- 零售

- 政府/公共部門

- 教育

- 能源公用事業

- 法律與專業服務

- 其他終端用戶產業

- 按地區

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 肯亞

- 其他非洲國家

- 中東

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Google LLC

- International Business Machines Corporation

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- SAP SE

- Oracle Corporation

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Samsung Electronics Co., Ltd.

- Zoho Corporation Pvt. Ltd.

- ServiceNow, Inc.

- Jamf Holding Corp.

- Sophos Group plc

- Fortinet, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the middle east and Africa digital workplace market size is projected to expand from USD 4.67 billion in 2025 and USD 5.6 billion in 2026 to USD 14.58 billion by 2031, registering a CAGR of 21.09% between 2026 and 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Government and Public Sector, Education, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Middle East and Africa Digital Workplace Market Trends and Insights

Rising Demand for Hybrid Work Enablement Across Distributed Enterprises

Hybrid work in the region has moved beyond a short-term work arrangement and now functions as a structural operating requirement for many large employers. In the Middle East and Africa digital workplace market, this demand is strongest among organizations that manage large project sites, multiple offices, field teams, and cross-border operations simultaneously. Mega-project activity in Saudi Arabia has reinforced the need for continuous coordination among remote sites, command centers, and headquarters to sustain collaboration and device management. Cisco's broader Saudi expansion in 2025, including cloud services, data centers, local manufacturing plans, and support for AI talent development, strengthened the infrastructure needed for connected workplace environments. In African markets such as South Africa and Nigeria, workforce mobility across dispersed operating locations often matters more than home-based remote work when organizations evaluate workplace platforms. Vendors that combine communications, endpoint governance, multilingual usability, and secure access are therefore better placed to win new rollout cycles in the Middle East and Africa digital workplace market.

Accelerating Cloud Migration of Workplace Infrastructure

Cloud migration is increasingly being treated as a compliance and operating model decision rather than only a cost discussion across the Middle East and Africa digital workplace market. Saudi Arabia and the UAE had previously slowed some enterprise adoption because ministries, banks, and other regulated organizations needed proof of local hosting and tighter control over sensitive data. Microsoft confirmed that its Saudi Arabia East region will be available for customer workloads from Q4 2026, which reduces this friction by adding in-country availability zones for cloud workloads and workplace applications. e& enterprise's OneCloud offer reflected the same shift in the UAE, where sovereign hyperscale infrastructure has been positioned to support cloud and AI workloads inside local data center environments. As these options expand, more buyers can modernize productivity suites without weakening residency compliance or service continuity. The result is that cloud-native workplace platforms are becoming easier to justify for organizations that had stayed on older on-premises models for regulatory reasons.

Uneven Digital Infrastructure Quality Across Countries

Infrastructure quality still varies widely across countries, creating uneven readiness in the Middle East and Africa digital workplace market. Microsoft's Global AI Diffusion Report for Q1 2026 placed South Africa at 23.1% generative AI adoption among working-age people, while Nigeria stood at 10.1%, highlighting clear differences in digital readiness and reliable access. This gap affects workplace software directly because cloud-first architectures often require low-bandwidth, hybrid, or offline-capable variants as vendors expand beyond the GCC and South Africa. Power instability and uneven broadband quality can lengthen implementation timelines, weaken user experience, and reduce reliability for collaboration-heavy workloads. Buyers may still want modern tools, but practical deployment risk stays higher in markets where uptime is harder to maintain. This keeps the addressable opportunity below its full potential even when enterprise interest is visible.

Other drivers and restraints analyzed in the detailed report include:

- Growing Need for Secure Endpoint and Identity Control

- Increasing Adoption of Employee Experience Platforms and Digital Front Doors

- Budget Constraints and Long Enterprise Sales Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 69.56% of the Middle East and Africa digital workplace market share in 2025, making them the clear lead component across the region. This position reflects sustained demand for integrated suites that combine communications, endpoint management, mobility, employee support, workflow tools, and desktop virtualization in one controlled environment. The Middle East and Africa digital workplace market is moving toward platform consolidation as organizations seek fewer vendors, fewer interfaces, and clearer governance across distributed workforces. Buyers also face growing pressure to keep workplace controls auditable, which naturally favors broader solution stacks over disconnected point products. Virtual desktop infrastructure and cloud PC tools are gaining more attention in government, banking, and oil and gas, where local hosting and centralized control help reduce residency and access concerns.

Microsoft's Saudi Arabia East region is expected to support a broader wave of cloud PC and managed desktop deployments from Q4 2026 onward, especially among organizations that waited for local availability before expanding cloud-based work environments. Services accounted for the remaining 30.44% of the market in 2025, indicating that implementation, managed support, and advisory work remain necessary for enterprise adoption. Many organizations still lack the in-house teams needed to configure policy layers, user journeys, integrations, and security controls at full deployment scale. This is why services continue to matter even when solution suites dominate revenue, because the software purchase alone rarely delivers value without strong setup and operating support. Rising interest from foreign managed service providers in the United Arab Emirates also suggests that the services layer of the Middle East and Africa digital workplace market is becoming more competitive as rollout size and complexity increase.

Cloud accounted for 63.19% of the market in 2025, and the Middle East and Africa digital workplace market size for cloud deployment is projected to expand at a 22.56% CAGR through 2031. The growth case improved as local hyperscale zones reduced the long-standing conflict between compliance needs and scalable cloud operations. For many buyers, especially in ministries and regulated sectors, the availability of local hosting changed cloud from a policy issue into a practical modernization path. Microsoft's Saudi Arabia East region will give organizations more confidence in cloud-based workplace rollouts that need local data residency and continuity planning.

On-premises deployment still matters for ministries, defense entities, and oil and gas operators that require air-gapped environments or tighter physical control over systems and data. This means the Middle East and Africa digital workplace market will not adopt a single deployment model, as security posture and operating context still differ widely by buyer type. Hybrid setups are also gaining ground among large enterprises that want cloud-based orchestration for collaboration and analytics but keep selected workloads on site for latency or control reasons. That pattern is especially relevant where operational technology and office technology need to coexist without sharing the same hosting model. Certified cloud security standards also continue to favor providers that can demonstrate auditability, resilience, and local service support, which strengthens the position of well-prepared vendors in the Middle East and Africa digital workplace market.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- Middle East

List of Companies Covered in this Report:

- Microsoft Corporation

- Google LLC

- International Business Machines Corporation

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- SAP SE

- Oracle Corporation

- Dell Technologies Inc.

- HP Inc.

- Lenovo Group Limited

- Samsung Electronics Co., Ltd.

- Zoho Corporation Pvt. Ltd.

- ServiceNow, Inc.

- Jamf Holding Corp.

- Sophos Group plc

- Fortinet, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Hybrid Work Enablement Across Distributed Enterprises

- 4.2.2 Accelerating Cloud Migration of Workplace Infrastructure

- 4.2.3 Growing Need for Secure Endpoint and Identity Control

- 4.2.4 Increasing Adoption of Employee Experience Platforms and Digital Front Doors

- 4.2.5 Expansion of Workflow Automation and Knowledge Management Use Cases

- 4.2.6 Rising Demand for Virtual Desktop Infrastructure and Cloud PC in Regulated Environments

- 4.3 Market Restraints

- 4.3.1 Uneven Digital Infrastructure Quality Across Countries

- 4.3.2 Budget Constraints and Long Enterprise Sales Cycles

- 4.3.3 Data Sovereignty and Cross-Border Compliance Complexity

- 4.3.4 Fragmented Legacy Application Environments and Integration Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Middle East

- 5.5.1.1 Saudi Arabia

- 5.5.1.2 United Arab Emirates

- 5.5.1.3 Turkey

- 5.5.1.4 Israel

- 5.5.1.5 Rest of Middle East

- 5.5.2 Africa

- 5.5.2.1 South Africa

- 5.5.2.2 Egypt

- 5.5.2.3 Nigeria

- 5.5.2.4 Kenya

- 5.5.2.5 Rest of Africa

- 5.5.1 Middle East

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Google LLC

- 6.4.3 International Business Machines Corporation

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Citrix Systems, Inc.

- 6.4.6 SAP SE

- 6.4.7 Oracle Corporation

- 6.4.8 Dell Technologies Inc.

- 6.4.9 HP Inc.

- 6.4.10 Lenovo Group Limited

- 6.4.11 Samsung Electronics Co., Ltd.

- 6.4.12 Zoho Corporation Pvt. Ltd.

- 6.4.13 ServiceNow, Inc.

- 6.4.14 Jamf Holding Corp.

- 6.4.15 Sophos Group plc

- 6.4.16 Fortinet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)