|

市場調查報告書

商品編碼

2073265

北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

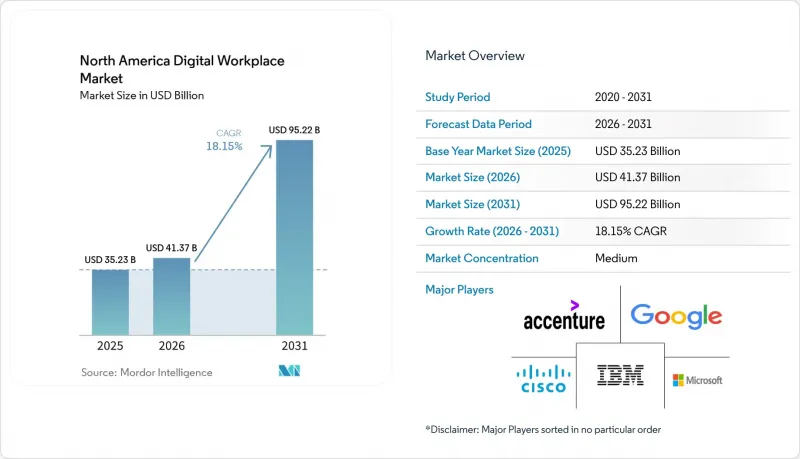

根據 Mordor Intelligence 預測,北美數位工作場所市場規模將從 2025 年的 352.3 億美元和 2026 年的 413.7 億美元成長到 2031 年的 952.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 18.15%。

本報告按組件(解決方案和服務)、部署模式(雲端、本地部署等)、組織規模(大型企業和中小企業)、最終用戶行業(IT和電信、銀行、金融服務和保險、醫療保健、製造業、零售業、政府和公共部門等)以及地區進行細分。市場預測以價值(美元)表示。

北美數位化工作場所市場的趨勢與洞察

混合辦公和彈性辦公模式的廣泛採用。

混合辦公模式已成為北美數位化工作場所市場中一種成熟的營運模式,持續支撐著對協作和員工支援平台的穩定需求。在加拿大,到2026年3月,56%的專業表示混合辦公是他們首選的工作方式,這表明柔軟性已成為員工的一項長期期望,而不僅僅是一種臨時調整。這一趨勢推動了分散式團隊持續使用基於雲端的通訊工具、文件存取工具和數位服務工具。有了核心的混合辦公基礎設施,企業可以比徹底改造平台更輕鬆地添加日程安排、分析和人工智慧輔助工具。這一趨勢支持現有客戶持續擴展平台,並透過升級和新用戶採用推動了北美數位化工作場所市場的成長。

人工智慧驅動的協作和自動化實施

人工智慧驅動的協作目前是北美數位化工作場所市場最強勁的成長引擎之一。這是因為企業正在實際營運中應用這項技術,而不僅僅是進行有限的試用。據微軟稱,從2025年3月到2026年3月,Microsoft 365生態系統中的有效用戶數量同比成長了15倍,北美地區49%的Copilot對話用於支援分析、問題解決和創造性「自主工作推出」(Autonomous Accenture )進一步加速了這項變革,將管治人工智慧擴展到IT、人力資源、客戶關係管理、財務、法律和保全行動等各個領域,惠及約2億企業員工。因此,北美數位化工作場所市場正朝著人工智慧編配的方向發展,其價值不在於孤立的聊天或搜尋功能,而在於系統級的、管治的執行。領導力也至關重要,微軟的研究表明,管理者主導的人工智慧應用能夠顯著提升員工對職場中基於代理的人工智慧的信任度,並增強他們對人工智慧價值的認知。

終點增殖和ID碎片化

終端數量激增和身分碎片化仍然是北美數位化工作場所市場面臨的重大障礙。這是由於分散式應用、自帶設備辦公室 (BYOD) 策略和人工智慧代理的快速成長,其發展速度超過了基於管治的管理能力。 Orchid Security 2026 年的一項研究發現,57% 的企業應用程式在中央身分提供者之外進行身分驗證,40% 的企業帳戶屬於已不再活躍於人力資源系統的使用者。該報告還顯示,非人類身分通常在目錄範圍之外和集中管理之外運行,這增加了與自主工具擴展相關的風險。儘管 NIST 網路安全框架和員工指南的更新現在更直接地反映了管理非人類身分和分散式員工隊伍風險的必要性,但在複雜的企業環境中實施這些措施仍然進展緩慢。這增加了補救成本,延緩了平台部署,使得能夠將身分管治直接整合到工作場所環境(而不是將其作為單獨的整合層)的供應商更具吸引力。

細分市場分析

至2025年,數位化工作場所解決方案將佔北美數位化工作場所市場69.32%的佔有率。這表明支出正從單獨的支援活動顯著轉向整合軟體平台。預計到2031年,這些解決方案的複合年成長率將達到18.56%,使其成為北美數位化工作場所市場成長最快的細分領域。這一趨勢反映了企業對整合協作、分析、工作流程自動化和人工智慧支援等功能於單一商業架構的環境的需求。 Microsoft 365、Google Workspace和ServiceNow在這項轉變中發揮核心作用,因為買家可以在已部署的平台內擴展功能,而無需管理多個獨立的工具。因此,北美數位化工作場所產業的平台層正在創造更多價值,因為持續的授權擴展比一次性軟體部署更容易擴展。

Accenture公司在74.3萬個席位上部署Microsoft 365 Copilot的案例清晰地詮釋了這個模式:人工智慧功能無需增加員工總數即可提高每個席位的收入。服務在北美數位化工作場所市場中繼續發揮至關重要的作用,尤其是在遷移、整合、管治、終端編程和變更支援方面。然而,隨著常規部署任務的標準化和平台支援的增強,服務的價值構成正向高附加價值解決方案轉變。能夠提供管治諮詢、加速部署和衡量營運成果的供應商,相比專注於通用部署的公司更具優勢。因此,儘管以解決方案為中心的收入結構正在北美數位化工作場所市場中發展,但對於複雜、合規驅動且大規模的員工結構變更而言,服務仍然至關重要。

到2025年,雲端將佔北美數位化工作場所市場61.18%的佔有率,預計到2031年將以18.78%的複合年成長率成長。這一成長率略高於北美整體數位化工作場所市場的成長速度,印證了雲端正在成為主導交付架構。其主要原因並非空泛而談,而是切實可行的:領先的供應商現在首先透過基於雲端的訂閱環境交付最新的協作、自動化和人工智慧功能。微軟代理生態系統的擴展和ServiceNow人工智慧平台的發布都印證了這個趨勢。這是因為產品開發現在與雲端原生交付模式和定期功能更新緊密相關。對於採購者而言,這減少了單獨升級專案的需求,並為分散的員工提供了更一致的體驗。

在政府機構、製造業以及其他具有嚴格站點層級控制、依賴傳統舊有應用程式或特定產業資料要求的環境中,本地部署仍然至關重要。美國網路安全與基礎設施安全局 (CISA) 的可信任網路連接架構持續影響聯邦政府如何在安全環境中建構雲端存取和遠端連接,這也是為什麼一些組織即使在現代化過程中也堅持採用更受控的部署模式的原因之一。混合部署仍然十分重要,因為許多公司需要工作負載可移植性和分階段遷移路徑,而不是立即替換現有基礎設施。從這個意義上講,混合部署不僅僅是一個臨時橋樑,也是組織平衡新的雲端功能和傳統作業系統的永續營運模式。因此,儘管北美數位化工作場所產業正持續向雲端主導架構轉型,但在風險、合規性或業務連續性至關重要的領域,混合架構仍有其存在的空間。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大強制性混合式和彈性工作安排

- 人工智慧驅動的協作和自動化實施

- 以員工體驗為重點,實現工作場所現代化

- 以雲端優先的方式實現工作場所標準化

- 分散式辦公環境中安全與合規的現代化

- 北美跨境管理型工作場所外包

- 市場限制因素

- 終點增殖和ID碎片化

- 傳統協作技術堆疊之間整合的複雜性

- 中小企業的預算敏感性

- 對變革的疲勞和使用者對採用的抵制

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 整合通訊與協作

- 整合端點管理

- 企業移動性與管理

- 員工體驗平台與內網

- 工作流程自動化與知識管理

- 虛擬桌面基礎架構與雲端電腦

- 服務

- 解決方案

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 衛生保健

- 製造業

- 零售

- 政府/公共部門

- 教育

- 能源公用事業

- 法律與專業服務

- 其他終端用戶產業

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- IBM Corporation

- Accenture plc

- Cisco Systems, Inc.

- Google LLC

- Citrix Systems, Inc.

- DXC Technology Company

- Cognizant Technology Solutions Corporation

- Hewlett Packard Enterprise Development LP

- NTT DATA Group Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- Atos SE

- Unisys Corporation

- Capgemini SE

- Oracle Corporation

- Salesforce, Inc.

- VMware, Inc.

- ServiceNow, Inc.

- Zoom Communications, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america digital workplace market size is projected to expand from USD 35.23 billion in 2025 and USD 41.37 billion in 2026 to USD 95.22 billion by 2031, registering a CAGR of 18.15% between 2026 and 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America Digital Workplace Market Trends and Insights

Rising Hybrid and Flexible Work Mandates

Hybrid work has become a durable operating model in the North America digital workplace market, and it continues to support steady demand for collaboration and employee support platforms. In Canada, 56% of professionals ranked hybrid as their preferred work mode in March 2026, which shows that flexibility remains a standing workforce expectation rather than a short-lived adjustment. This preference keeps cloud-based communication, document access, and digital service tools in regular use across distributed teams. Once the core hybrid infrastructure is in place, organizations can add scheduling, analytics, and AI support tools with less friction than a full platform replacement. That dynamic supports recurring platform expansion inside existing accounts and helps the North America digital workplace market grow through upgrades as much as through first-time deployments.

AI-Enabled Collaboration and Automation Adoption

AI-enabled collaboration is now one of the strongest growth engines in the North America digital workplace market because enterprises are using it for real work rather than limited trials. Microsoft reported that active agents inside the Microsoft 365 ecosystem grew 15 times year over year between March 2025 and March 2026, and 49% of Copilot conversations in North America supported cognitive work such as analysis, problem-solving, and creative tasks. Microsoft also highlighted Accenture plc's 743,000-seat Copilot deployment, where data from 200,000 users showed 97% completed routine tasks 15 times faster and 53% reported significant productivity gains. ServiceNow reinforced this shift in May 2026 when it launched Autonomous Workforce and extended governed AI across IT, HR, CRM, finance, legal, and security operations for nearly 200 million enterprise employees. The North America digital workplace market is therefore moving toward AI orchestration, where value comes from governed execution across systems rather than from isolated chat or search features. Leadership behavior also matters because Microsoft found that manager-led AI adoption materially lifts employee trust and perceived value from agentic AI in the workplace.

Endpoint Sprawl and Identity Fragmentation

Endpoint sprawl and identity fragmentation remain major barriers in the North America digital workplace market because distributed applications, BYOD policies, and AI agents expand faster than governance controls. Orchid Security found in 2026 that 57% of enterprise applications were authenticated outside a central identity provider, while 40% of enterprise accounts belonged to users no longer active in HR systems. The same report also showed that non-human identities often operate without directory coverage or centralized oversight, which raises the risk of scaling autonomous tools. NIST's cybersecurity framework updates and workforce guidance now more directly reflect the need to manage non-human identities and distributed workforce risk, but implementation across complex enterprise environments still lags. This creates added remediation cost, slows platform rollout, and increases the appeal of vendors that can build identity governance directly into workplace environments rather than leaving it as a separate integration layer.

Other drivers and restraints analyzed in the detailed report include:

- Employee Experience-Led Workplace Modernization

- Cloud-First Workplace Standardization

- Integration Complexity Across Legacy Collaboration Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital workplace solutions accounted for 69.32% of the North America digital workplace market in 2025, indicating that spending is heavily centered on integrated software platforms rather than standalone support activities. Solutions are also projected to grow at a 18.56% CAGR through 2031, making them the fastest-growing component of the North America digital workplace market. This pattern reflects enterprise demand for environments that combine collaboration, analytics, workflow automation, and AI support within a single commercial structure. Microsoft 365, Google Workspace, and ServiceNow are central to this shift because they let buyers expand functionality within an installed platform rather than managing multiple separate tools. The North America digital workplace industry is therefore seeing more value captured at the platform layer, where recurring license expansion is easier to scale than one-time software deployment work.

Accenture plc's 743,000-seat Microsoft 365 Copilot rollout illustrates this model, as AI features can increase revenue per seat without requiring growth in the total employee count. Services still retain an important role in the North America digital workplace market, especially for migration, integration, governance, endpoint programs, and change support. However, the value mix inside services is shifting upward as routine implementation work becomes more standardized and more platform-assisted. Providers that can advise on AI governance, accelerate adoption, and measure operational outcomes are better placed than firms focused mainly on commodity implementation. This leaves the North America digital workplace market with a solutions-heavy revenue structure, while services remain essential for complex, compliance-driven, and large-scale workforce change.

Cloud accounted for 61.18% of the North America digital workplace market in 2025 and is forecast to expand at an 18.78% CAGR through 2031. That pace slightly exceeds the broader North America digital workplace market and confirms that cloud is taking the lead as the preferred delivery architecture. The main reason is practical rather than abstract, leading vendors now to deliver their newest collaboration, automation, and AI capabilities first through cloud-based subscription environments. Microsoft's expanding agent ecosystem and ServiceNow's AI platform releases both support that direction, since product development is now closely tied to cloud-native delivery and regular feature updates. For buyers, this reduces the need for separate upgrade projects and supports more consistent experiences across distributed workforces.

On-premises deployment still matters in government, manufacturing, and other settings with strict site-level control, reliance on legacy applications, or sector-specific data requirements. CISA's Trusted Internet Connections architecture continues to shape how secure federal environments structure cloud access and remote connectivity, which helps explain why some organizations maintain more controlled deployment models even as they modernize. Hybrid deployment remains important because many enterprises need workload portability and staged transition paths rather than immediate replacement of existing estates. In that sense, hybrid is not only a temporary bridge but also a durable operating model for organizations balancing new cloud features with older operational systems. The North America digital workplace industry, therefore, continues to move toward cloud leadership, while still leaving room for mixed architectures in sectors where risk, compliance, or operational continuity carry more weight.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Microsoft Corporation

- IBM Corporation

- Accenture plc

- Cisco Systems, Inc.

- Google LLC

- Citrix Systems, Inc.

- DXC Technology Company

- Cognizant Technology Solutions Corporation

- Hewlett Packard Enterprise Development LP

- NTT DATA Group Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- Atos SE

- Unisys Corporation

- Capgemini SE

- Oracle Corporation

- Salesforce, Inc.

- VMware, Inc.

- ServiceNow, Inc.

- Zoom Communications, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hybrid and Flexible Work Mandates

- 4.2.2 AI-Enabled Collaboration and Automation Adoption

- 4.2.3 Employee Experience-Led Workplace Modernization

- 4.2.4 Cloud-First Workplace Standardization

- 4.2.5 Security and Compliance Modernization Across Distributed Workforces

- 4.2.6 Cross-Border Managed Workplace Outsourcing in North America

- 4.3 Market Restraints

- 4.3.1 Endpoint Sprawl and Identity Fragmentation

- 4.3.2 Integration Complexity Across Legacy Collaboration Stacks

- 4.3.3 Budget Sensitivity in Small and Medium-Sized Enterprises

- 4.3.4 Change Fatigue and User Adoption Resistance

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 IBM Corporation

- 6.4.3 Accenture plc

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Google LLC

- 6.4.6 Citrix Systems, Inc.

- 6.4.7 DXC Technology Company

- 6.4.8 Cognizant Technology Solutions Corporation

- 6.4.9 Hewlett Packard Enterprise Development LP

- 6.4.10 NTT DATA Group Corporation

- 6.4.11 Tata Consultancy Services Limited

- 6.4.12 Wipro Limited

- 6.4.13 Atos SE

- 6.4.14 Unisys Corporation

- 6.4.15 Capgemini SE

- 6.4.16 Oracle Corporation

- 6.4.17 Salesforce, Inc.

- 6.4.18 VMware, Inc.

- 6.4.19 ServiceNow, Inc.

- 6.4.20 Zoom Communications, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)