|

市場調查報告書

商品編碼

2073267

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Asia-Pacific Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

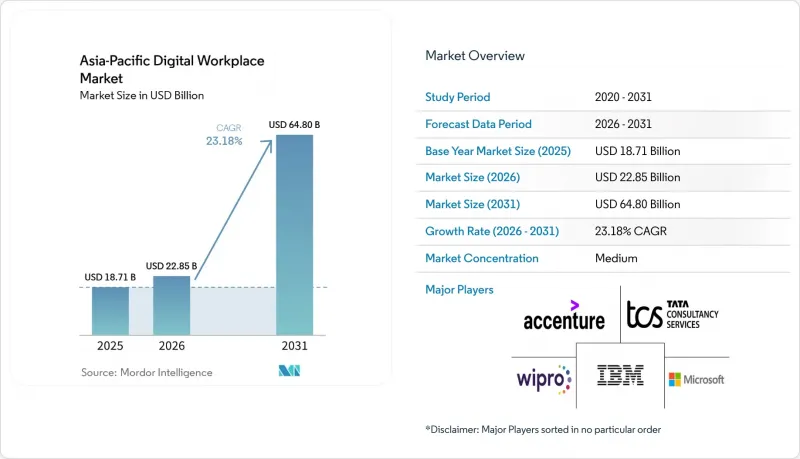

根據 Mordor Intelligence 預測,亞太地區的數位化工作場所市場規模預計將從 2025 年的 187.1 億美元成長到 2026 年的 228.5 億美元,然後在 2031 年達到 648 億美元,2026 年至 2031 年的複合成長率為 23.18%。

本報告按組件(解決方案和服務)、部署模式(雲端、本地部署等)、組織規模(大型企業和中小企業)、最終用戶行業(IT和電信、醫療保健、製造業、零售業、政府和公共部門、教育等)以及地區進行細分。市場預測以美元計價。

亞太地區數位化工作場所市場的趨勢和洞察。

大型企業中混合辦公模式的建立

混合辦公模式已不再是臨時階段,而是正在塑造亞太地區大型企業的長期辦公室設計。這推動了亞太地區數位化辦公室市場的蓬勃發展。其驅動力源自於企業對持續協作、設備管理、工作流程存取和員工支援的需求,無論員工是在辦公室還是遠距辦公。需求模式不再局限於視訊會議和通訊,企業越來越需要一種能夠連接知識、批准、服務請求和團隊間協作的「連接層」。微軟在《2026年工作趨勢指數》中指出,企業正在圍繞人工智慧驅動的工作模式重建其營運模式,並強調需要能夠支援分散式團隊和工作流程協作的數位化工具。這一趨勢對亞太地區的數位化辦公室市場意義重大,因為即使是那些要求員工在辦公室辦公的企業,也仍然需要能夠在實體辦公室和數位化辦公室之間無縫切換。因此,企業持續投資於能夠在單一營運環境中支援溝通、知識存取和工作流程連續性的平台。

遷移到雲端託管的員工體驗堆疊

隨著企業對持續更新的數位化工作場所平台的需求日益成長,而非僅依賴週期性升級,雲端採用正在加速發展。這推動了亞太地區數位化工作場所市場的發展,因為人工智慧功能、政策變更和安全控制可以透過SaaS原生環境更有效率地交付。 2026年6月,微軟報告稱,Infosys、TCS和Wipro在不到六個月的時間內聯合為超過30萬名員工部署了Microsoft 365 Copilot。這表明,當業務優勢顯而易見時,大型企業會以驚人的速度實現雲端工作場所軟體的標準化。這種快速的採用速度意義重大,因為它不僅反映了軟體的普及,也體現了企業對雲端產品在提升工作場所生產力、管治和人工智慧存取方面的日益成長的信心。此外,許多受監管的買家現在不再將雲端視為一種管理上的妥協,而是將其視為一種能夠更快部署和簡化管理的切實可行的手段,這也支撐了亞太地區數位化工作場所市場的發展。因此,雲端託管的員工體驗堆疊正成為大型企業和新興中型企業選擇平台時的核心要素。

傳統識別碼、設備和應用程式的激增

舊有系統的激增是工作場所轉型的一大障礙,因為許多公司仍然在身分、設備和應用層之間缺乏有效連接。這削弱了亞太地區的數位化工作場所市場,因為買家往往需要先解決底層技術環境問題,才能充分發揮新工作場所平台的價值。 2026年6月,IBM宣布擴大與ServiceNow的合作夥伴關係,旨在實現舊有應用程式的現代化和企業資料的組織。這表明,基礎設施的組織仍然是大規模人工智慧和工作場所部署的一大障礙。這個問題不僅僅是技術層面的;系統的無序擴張會減緩策略標準化進程,增加支援負擔,並損害跨團隊和跨國使用者體驗的一致性。 HCLTech與Team Global Express於2026年1月開展的一個專案也強調了在推動更廣泛的服務轉型之前,需要整合多供應商環境。除非更多組織能夠緩解這種複雜性,否則亞太地區的數位化工作場所市場將繼續面臨引進週期延長和實施結果差異化的問題。

細分市場分析

到2025年,解決方案將佔據亞太地區數位化工作場所市場68.26%的佔有率。這表明,軟體平台仍然是買家實現工作場所環境現代化的主要基礎。這一主導地位反映了一種趨勢:企業更傾向於使用整合工具,在單一架構內管理溝通、工作流程自動化、知識存取和員工支持,而不是使用單獨的獨立產品。在亞太地區的數位化工作場所市場,對解決方案的需求集中在整合通訊、員工體驗平台、工作流程自動化、企業內網功能以及知識管理層,這些功能既能支援日常生產力,又能支援系統化的服務交付。隨著工作場所平台價值的提升(使用者無需切換上下文即可在不同任務之間切換),買家越來越希望這些功能能夠作為單一的整合系統運作。因此,該解決方案類別繼續佔據亞太地區數位化工作場所市場的最大佔有率,尤其對於那些希望在多個業務部門和國家/地區實現營運模式標準化的公司而言。

此外,隨著數位化工作場所計畫擴展到終端控制、工作流程路由和人工智慧支援等領域,解決方案配置的多樣化程度也不斷提高。虛擬桌面基礎架構 (VDI) 和雲端 PC 工具正重新受到客戶的關注,這些客戶尋求安全存取、策略一致性以及簡化分散式團隊的管理。隨著企業需要對設備、身分和應用程式進行協調而非並行和孤立的控制,整合終端管理與協作和工作流程平台之間的聯繫也日益緊密。儘管亞太地區數位化工作場所市場的服務領域規模仍然較小,但其重要性卻絲毫未減,因為部署規模、整合需求和變更管理要求變得越來越複雜,超出了企業內部團隊的能力範圍。 HCLTech 於 2026 年 1 月與 Team Global Express 簽署的協議表明,單一的託管工作場所合約如何能夠實現供應商整合、簡化支持,並在大規模組織內創建更統一的營運環境。

預計到2025年,雲端運算將佔亞太地區數位化工作場所市場佔有率的64.83%,並將以23.72%的複合年成長率持續成長至2031年。這證實了雲端運算正成為大多數新型工作場所部署的標準選擇。主要原因是,與傳統的本地部署模式相比,雲端環境能夠更快地部署人工智慧功能、進行策略變更並改善協作功能。這在亞太地區的數位化工作場所市場至關重要,因為工作場所工具必須隨著使用者行為、管治規則和人工智慧用例的變化而不斷發展。此外,採用雲端運算為供應商提供了一種更直接的方式來維護產品效能,並向大規模的用戶群交付新功能,而無需經歷漫長的本地升級週期。這些優勢在亞太地區尤其重要,因為該地區的企業正尋求在營運成熟度各異的多個國家/地區擴展其數位化員工體驗計畫。

雲端標準化的步伐也反映在企業發展趨勢上。 2026年6月,微軟報告稱,Infosys、TCS和Wipro在不到六個月的時間內聯合為超過30萬名員工部署了Microsoft 365 Copilot。這表明,當企業需求與平台準備就緒度相符時,基於雲端的辦公室工具可以快速部署。在一些政府機構和高度監管的行業中,本地部署仍然至關重要,因為這些機構的資料處理法規仍然嚴格,內部控制要求難以變更。因此,混合部署仍然是亞太地區數位化辦公市場的遷移模式,尤其適用於那些在分階段進行現代化改造並同時保留部分本地工作負載的大型企業。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 大型企業中混合辦公模式的建立

- 遷移到雲端託管的員工體驗堆疊

- 以安全性為首要任務的工作空間整合。

- 人工智慧驅動的工作流程調整與知識獲取

- 資產密集型產業現場工作人員的數位化

- 基於結果的數位化員工體驗採購

- 市場限制因素

- 遺留身分、裝置和應用程式的無序擴張

- 協作工具和工作流程工具之間的整合債務

- DEX管理與實施管治的技能差距

- 對隱私、主權和跨境資料的擔憂

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 整合通訊與協作

- 整合端點管理

- 企業移動性與管理

- 員工體驗平台與內網

- 工作流程自動化與知識管理

- 虛擬桌面基礎架構與雲端電腦

- 服務

- 解決方案

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 衛生保健

- 製造業

- 零售

- 政府/公共部門

- 教育

- 能源公用事業

- 法律與專業服務

- 其他終端用戶產業

- 按地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- IBM Corporation

- Microsoft Corporation

- Accenture PLC

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- HCL Technologies Limited

- NTT DATA Group Corporation

- Infosys Limited

- DXC Technology Company

- Fujitsu Limited

- Hewlett Packard Enterprise Company

- Capgemini SE

- Kyndryl Holdings, Inc.

- Unisys Corporation

- Citrix Systems, Inc.

- Atlassian Corporation

- Salesforce, Inc.

- ServiceNow, Inc.

- Kissflow Inc.

- Simpplr Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific digital workplace market size is expected to grow from USD 18.71 billion in 2025 to USD 22.85 billion in 2026 and is forecast to reach USD 64.8 billion by 2031 at 23.18% CAGR over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, Healthcare, Manufacturing, Retail, Government and Public Sector, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Digital Workplace Market Trends and Insights

Hybrid Work Permanence Across Large Enterprises

Hybrid work has moved beyond a temporary policy and now shapes long-term workplace design across large organizations in the region. This is keeping the Asia-Pacific digital workplace market active because enterprises need consistent collaboration, device management, workflow access, and employee support across office and remote settings. The demand pattern is no longer limited to video meetings or messaging, because companies increasingly want a connected layer that links knowledge, approvals, service requests, and team coordination. Microsoft stated in its 2026 Work Trend Index that firms are rebuilding their operating models around AI-enabled work, underscoring the need for digital tools that support coordination across distributed teams and workflows. This trend is important for the Asia-Pacific digital workplace market because firms with fixed office attendance still need employees to move between physical and digital tasks without friction. As a result, spending remains focused on platforms that can support communication, knowledge access, and workflow continuity in a single operating environment.

Shift To Cloud-Hosted Employee Experience Stacks

Cloud deployment is gaining ground as enterprises increasingly seek digital workplace platforms that are continuously updated rather than delivered through periodic upgrade cycles. This is strengthening the Asia-Pacific digital workplace market because AI functionality, policy changes, and security controls are now delivered more efficiently through SaaS-native environments. Microsoft reported in June 2026 that Infosys, TCS, and Wipro together scaled Microsoft 365 Copilot to more than 300,000 employees in under six months, demonstrating how quickly large organizations are standardizing on cloud-based workplace software when the business case is clear. That pace of rollout matters because it reflects not only software adoption, but also confidence in cloud delivery for workplace productivity, governance, and AI access. The Asia-Pacific digital workplace market is also supported by the fact that many regulated buyers now see cloud as a practical route to faster deployment and simpler administration rather than a compromise on control. This makes cloud-hosted employee experience stacks central to platform selection across both large enterprises and emerging mid-market buyers.

Legacy Identity, Device, and Application Sprawl

Legacy sprawl remains a major brake on workplace transformation because many enterprises still operate with disconnected identity, device, and application layers. This weakens the Asia-Pacific digital workplace market because buyers often need to address the underlying technology estate before they can fully realize the value of new workplace platforms. IBM said in June 2026 that its expanded work with ServiceNow is specifically targeting legacy application modernization and enterprise data readiness, indicating that foundational cleanup remains a real barrier to scaled AI and workplace deployment. The problem is not only technical, because sprawl also slows policy standardization, increases support effort, and makes user experience less consistent across teams and countries. HCLTech's January 2026 engagement with Team Global Express also highlighted the need to consolidate a multi-vendor environment before broader service transformation could move ahead. Until more organizations reduce this complexity, the Asia-Pacific digital workplace market will continue to face slower implementation cycles and uneven adoption outcomes.

Other drivers and restraints analyzed in the detailed report include:

- Security-First Workspace Consolidation

- AI-Enabled Workflow Orchestration and Knowledge Access

- Integration Debt Across Collaboration and Workflow Tools

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 68.26% of the Asia-Pacific digital workplace market in 2025, which shows that software platforms remain the primary layer through which buyers are modernizing workplace environments. This dominance reflects the enterprise's preference for integrated tools that manage communication, workflow automation, knowledge access, and employee support within a single architecture rather than through separate point products. In the Asia-Pacific digital workplace market, solution demand centers on unified communications, employee experience platforms, workflow automation, intranet capabilities, and knowledge management layers that support both daily productivity and structured service delivery. Buyers increasingly want these capabilities to work as a single, connected system because the value of a workplace platform rises when users can move between tasks without switching context. That is why the solutions category continues to hold the largest weight in the Asia-Pacific digital workplace market, especially in enterprises that are standardizing operating models across multiple business units and countries.

The solutions mix is also broadening, as digital workplace programs now touch endpoint control, workflow routing, and AI-assisted support. Virtual desktop infrastructure and cloud PC tools are drawing renewed attention where clients want secure access, policy consistency, and simpler management for distributed teams. Unified endpoint management is increasingly linked to collaboration and workflow platforms, as enterprises seek device, identity, and application controls to work together rather than in parallel silos. The services side of the Asia-Pacific digital workplace market remains smaller, but it remains important when deployment scale, integration needs, and change management requirements become too complex for internal teams to handle alone. HCLTech's January 2026 engagement with Team Global Express shows how a single managed workplace scope can be used to consolidate vendors, simplify support, and create a more unified operating environment across a large organization

Cloud held 64.83% of the Asia-Pacific digital workplace market in 2025 and is projected to expand at a 23.72% CAGR through 2031, confirming that cloud has become the default route for most new workplace deployments. The main reason is that cloud environments allow enterprises to introduce AI features, policy changes, and collaboration improvements faster than on-premises models can typically support. In the Asia-Pacific digital workplace market, this matters because workplace tools must evolve continuously as user behavior, governance rules, and AI use cases change. Cloud deployment also gives vendors a more direct way to maintain product performance and deliver new functionality across large user bases without long local upgrade cycles. These advantages are especially relevant in regions where firms are trying to scale digital employee experience programs across multiple countries with different operational maturity levels.

The pace of cloud standardization is visible in enterprise behavior. Microsoft reported in June 2026 that Infosys, TCS, and Wipro together expanded Microsoft 365 Copilot to more than 300,000 employees in under six months, demonstrating how quickly cloud-based workplace tools can be rolled out when enterprise demand aligns with platform readiness. On-premises deployment still has relevance in parts of government and highly regulated industries where data-handling rules remain strict and internal control requirements are harder to change. Hybrid deployment, therefore, continues to function as a transition model in the Asia-Pacific digital workplace market, especially for large enterprises that are modernizing gradually while keeping some local workloads in place.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- IBM Corporation

- Microsoft Corporation

- Accenture PLC

- Tata Consultancy Services Limited

- Wipro Limited

- Cognizant Technology Solutions Corporation

- HCL Technologies Limited

- NTT DATA Group Corporation

- Infosys Limited

- DXC Technology Company

- Fujitsu Limited

- Hewlett Packard Enterprise Company

- Capgemini SE

- Kyndryl Holdings, Inc.

- Unisys Corporation

- Citrix Systems, Inc.

- Atlassian Corporation

- Salesforce, Inc.

- ServiceNow, Inc.

- Kissflow Inc.

- Simpplr Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Hybrid Work Permanence Across Large Enterprises

- 4.3.2 Shift to Cloud-Hosted Employee Experience Stacks

- 4.3.3 Security-First Workspace Consolidation

- 4.3.4 AI-Enabled Workflow Orchestration and Knowledge Access

- 4.3.5 Frontline Worker Digitization in Asset-Intensive Industries

- 4.3.6 Outcome-Based Procurement for Digital Employee Experience

- 4.4 Market Restraints

- 4.4.1 Legacy Identity, Device, and Application Sprawl

- 4.4.2 Integration Debt Across Collaboration and Workflow Tools

- 4.4.3 Skills Gaps in DEX Administration and Adoption Governance

- 4.4.4 Privacy, Sovereignty, and Cross-Border Data Concerns

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 South Korea

- 5.5.5 Australia and New Zealand

- 5.5.6 Southeast Asia

- 5.5.7 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Microsoft Corporation

- 6.4.3 Accenture PLC

- 6.4.4 Tata Consultancy Services Limited

- 6.4.5 Wipro Limited

- 6.4.6 Cognizant Technology Solutions Corporation

- 6.4.7 HCL Technologies Limited

- 6.4.8 NTT DATA Group Corporation

- 6.4.9 Infosys Limited

- 6.4.10 DXC Technology Company

- 6.4.11 Fujitsu Limited

- 6.4.12 Hewlett Packard Enterprise Company

- 6.4.13 Capgemini SE

- 6.4.14 Kyndryl Holdings, Inc.

- 6.4.15 Unisys Corporation

- 6.4.16 Citrix Systems, Inc.

- 6.4.17 Atlassian Corporation

- 6.4.18 Salesforce, Inc.

- 6.4.19 ServiceNow, Inc.

- 6.4.20 Kissflow Inc.

- 6.4.21 Simpplr Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)