|

市場調查報告書

商品編碼

2073266

南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

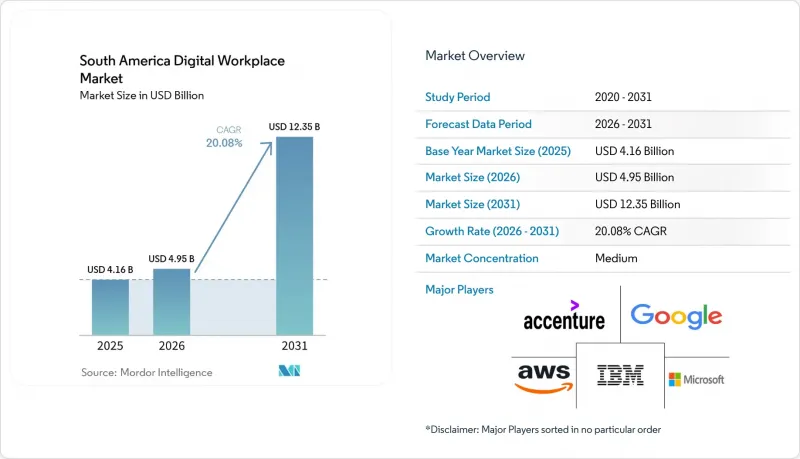

據 Mordor Intelligence 稱,2025 年南美洲數位工作場所市場價值為 41.6 億美元,預計到 2031 年將達到 123.5 億美元,而 2026 年為 49.5 億美元,預測期(2026-2031 年)的複合年成長率為 20.08%。

本報告按組件(解決方案和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、最終用戶行業(IT和電信、銀行、金融服務和保險、醫療保健、製造業、零售業、政府和公共部門等)以及地區進行細分。市場預測以美元計價。

南美數位化工作場所市場的趨勢與洞察

在企業營運中擴大混合辦公模式的採用

對於該地區的許多公司而言,混合辦公正從臨時措施轉變為更穩定的營運模式,南美數位工作場所市場也越來越依賴日常工作流程決策,而非臨時緊急支出。這種需求的影響遠不止於協作軟體,雇主需要為在家庭、分店和總部等不同環境間切換的員工提供安全存取、設備管理、身分管理、工作流程文件和政策追蹤等功能。這種營運模式也凸顯了將溝通、文件存取、核准和基本員工支援整合到單一系統中的平台的重要性,這也是平台整合在南美數位工作場所市場持續發展的原因之一。主要經濟體正式推出的遠距和混合辦公法規也促使雇主尋求能夠持續支援跨團隊記錄保存、批准和管治的系統。這項需求凸顯了整合式工作場所平台相對於獨立工具的價值,尤其是在雇主必須管理分散的員工、敏感資料和日常合規任務的情況下。因此,混合辦公不僅在南美洲數位工作場所市場擴大了用戶群體,也提高了買家對每個實施方案的功能期望。

協作與虛擬工作空間堆疊的雲端遷移

雲端遷移仍然是南美數位化工作場所市場的主要成長要素,因為它透過將協作、儲存、身分管理和安全控制部署在共用的雲端基礎設施上,促進了工作場所平台的擴展。微軟宣布將在三年內投資147億巴西雷亞爾(約29億美元)用於巴西的雲端和人工智慧基礎設施建設,這反映了微軟對該地區企業需求和本地服務交付能力的長期信心。此類投資的實際影響在於,隨著企業將核心工作場所功能遷移到雲端環境,與延遲、容錯性和資料本地性相關的障礙得以減少。這項變更對南美洲數位化工作場所市場意義重大,因為隨著底層基礎設施問題更容易解決,買家更有可能同時實現協作、分析、工作流程和員工服務工具的現代化。雲端遷移也鼓勵更多供應商進入市場,因為企業可以利用大規模的組合,而不是依賴單一的本地部署架構。在接下來的幾年裡,這一趨勢將確保雲端主導合約在南美數位工作場所市場中繼續佔據核心地位,尤其是在受監管的使用案例中本地基礎設施可靠性不斷提高的國家。

整合舊有應用程式的複雜性

在南美洲數位化工作場所市場,舊有應用程式整合仍是一大阻礙因素。許多公司仍在運行過時的HR、薪資、文件管理和業務系統,這些系統並非為現代雲端工作流程而設計。即使公司希望部署新的協作、自動化或員工服務工具,通常也需要中間件、自訂介面或分階段遷移計劃,才能使新平台與現有資料和核准流程整合。這導致部署延遲、專案成本增加,並使買家對大規模部署更加謹慎,尤其是在工作場所專案涉及敏感員工記錄或受監管流程的情況下。對於擁有多年建構的多個系統的大型組織而言,這個問題更為突出,阻礙了南美數位化工作場所市場強勁需求的快速轉化為實際部署。此外,由於供應商必須先解決資料映射、存取控制和流程重新設計等問題,客戶才能充分利用平台的價值,因此支出正轉向長期服務合約。因此,儘管南美數位化工作場所市場持續保持強勁成長,但整合的複雜性目前正在減緩許多企業專案的實施速度和獲利能力。

細分市場分析

2025年,解決方案將佔據南美洲數位化工作場所市場64.93%的佔有率。這表明買家仍然優先考慮整合通訊、文件、工作流程和員工工具的核心軟體平台。這一領先地位也反映了企業客戶傾向於選擇少數策略性套件而非分散的獨立工具的趨勢,後者會帶來單獨登入、支援和管治的負擔。在南美洲數位化工作場所市場,這一趨勢正在推動能夠將協作、生產力、分析和自動化整合到單一商業模式中的供應商的發展。 SAP報告稱,到2025年,南美55%的決策者計劃增加對人工智慧的投資,這凸顯了市場正向更全面的解決方案套件轉變,在這些套件中,人工智慧功能被整合到日常營運中,而不是作為單獨的產品出售。

預計到2031年,解決方案市場將以20.48%的複合年成長率成長,並且這一類別將繼續在南美數位化工作場所市場的新契約活動中佔據核心地位。雖然服務市場佔有率目前仍然較小,但隨著工作場所平台變得更加智慧和互聯,其重要性日益凸顯,客戶需要部署、整合、變更管理和持續支援。 Kyndryl公司於2026年4月發布了其人工智慧驅動的「工作場所數位雙胞胎」解決方案,這表明服務型公司正在擺脫對勞動力的依賴型交付模式,並將工作場所監控、預測和營運改進作為更廣泛的平台模式的一部分。這種轉變表明,數位化工作場所行業不再涇渭分明地分類為軟體和服務兩部分,因為大規模合約越來越依賴軟體和服務。從長遠來看,能夠將軟體深度與可靠的交付、管治和營運支援相結合,涵蓋整個工作場所環境的供應商,將成為南美洲數位化工作場所市場的主導者。

到2025年,雲端將佔據南美數位化工作場所市場58.32%的佔有率,並將成為成長最快的採用模式,到2031年複合年成長率將達到20.64%。這一主導地位反映出該地區正在發生明顯的轉變,即轉向能夠更輕鬆地擴展以適應分散式團隊、行動用戶和不斷成長的數據需求的平台,而無需承擔全部區域本地環境帶來的沉重維護負擔。南美數位化工作場所市場的雲端採用持續受益於本地基礎設施的加強。隨著延遲和地域性問題得到有效控制,買家更願意考慮將敏感的協作和工作流程功能部署在雲端平台上。微軟在巴西投資147億雷亞爾(約29億美元),透過強化企業雲端和人工智慧採用的基礎環境,正在推動這項轉變。

在南美洲數位化工作場所市場,混合部署仍然至關重要,因為一些公司需要分階段遷移,以確保特定工作負載能夠靠近其內部系統和敏感資料管理結構。對於那些運行無法快速遷移的傳統應用程式的組織,或者行業法規和內部政策仍然建議在過渡期間採用混合架構的組織而言,這一點尤其重要。雖然本地部署的相對重要性正在下降,但在一些政府機構、關鍵職能部門以及處於數位現代化早期階段的組織中,本地部署仍然存在。哥倫比亞佔該地區數位化企業總數的12.8%,也對雲端服務有著強勁的需求。許多數位化原生企業受傳統舊有系統的影響較小,因此更有可能儘早採用現代化的協作和安全工具。因此,雲端仍然是整個南美數位化工作場所市場的主要成長引擎,而混合部署則為分階段而非一次性完成現代化的客戶提供了一個切實可行的橋樑。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在企業營運中擴大混合辦公模式的採用

- 優先發展端點和身分管理,並將安全性放在首位。

- 協作與虛擬工作空間堆疊的雲端遷移

- 擴展託管式數位化工作場所外包

- 由於資料居住要求和主權法規,本地化面臨壓力。

- 人工智慧驅動的員工體驗和工作流程編配

- 市場限制因素

- 整合舊有應用程式的複雜性

- 缺乏職場數位化和終端安全方面的技能

- 跨境合規要求的差異

- 農村地區網路連線有限且網路品質參差不齊

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 整合通訊與協作

- 整合端點管理

- 企業移動性與管理

- 員工體驗平台與內網

- 工作流程自動化與知識管理

- 虛擬桌面基礎架構與雲端電腦

- 服務

- 解決方案

- 部署模式

- 雲

- 混合

- 現場

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 衛生保健

- 製造業

- 零售

- 政府/公共部門

- 教育

- 能源公用事業

- 法律與專業服務

- 其他終端用戶產業

- 按地區

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- International Business Machines Corporation

- Accenture PLC

- Google LLC

- Amazon Web Services, Inc.

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- Oracle Corporation

- SAP SE

- Hewlett Packard Enterprise Development LP

- DXC Technology Company

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- Kyndryl Holdings, Inc.

- Unisys Corporation

- Atos SE

- Cognizant Technology Solutions Corporation

- Globant SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america digital workplace market size was valued at USD 4.16 billion in 2025 and estimated to grow from USD 4.95 billion in 2026 to reach USD 12.35 billion by 2031, at a CAGR of 20.08% during the forecast period (2026-2031).

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Digital Workplace Market Trends and Insights

Rising Hybrid Work Adoption in Enterprise Operations

Hybrid work has moved from a temporary arrangement to a more stable operating model for many enterprises in the region, keeping the South America digital workplace market closely linked to everyday workflow decisions rather than one-time emergency spending. The demand effect extends beyond collaboration software alone, because employers need secure access, managed devices, identity controls, workflow documentation, and policy tracking for staff who move between home, branch, and central-office settings. This operating model also underscores the importance of platforms that connect communication, file access, approvals, and basic employee support within a single system, which helps explain the continued platform consolidation across the South America digital workplace market. Formal remote and hybrid work rules in major economies are also pushing employers toward systems that can consistently support records, approvals, and governance across teams. That requirement underscores the value of integrated workplace platforms over isolated tools, especially when employers must manage distributed staff, sensitive data, and recurring compliance tasks. As a result, hybrid work is not only expanding seat counts in the South America digital workplace market, but also widening the capabilities buyers expect from each deployment.

Cloud Migration of Collaboration and Virtual Workspace Stacks

Cloud migration remains a central growth force in the South America digital workplace market because workplace platforms are easier to scale when collaboration, storage, identity, and security controls sit on shared cloud infrastructure. Microsoft announced a BRL 14.7 billion (USD 2.9 billion) investment over 3 years in cloud and AI infrastructure in Brazil, reflecting long-term confidence in regional enterprise demand and local service capacity. The practical effect of investments like this is that enterprises face fewer barriers tied to latency, resilience, and data locality when moving core workplace functions into cloud environments. That shift matters in the South America digital workplace market because buyers often refresh collaboration, analytics, workflow, and employee service tools at the same time once the base infrastructure question becomes easier to solve. Cloud migration also supports broader vendor participation, as enterprises can mix large platform suites with specialized tools rather than relying on a single on-premises architecture. Over the next few years, this pattern should keep cloud-led contracts at the center of the South America digital workplace market, especially in countries where local infrastructure has become more credible for regulated use cases.

Legacy Application Integration Complexity

Legacy application integration remains one of the main restraints on the South America digital workplace market because many enterprises still run older HR, payroll, document, and line-of-business systems that were not built for modern cloud workflows. Even when companies want to deploy new collaboration, automation, or employee service tools, they often need middleware, custom interfaces, or phased migration plans before new platforms can work with existing data and approval flows. This slows implementation, raises project costs, and makes buyers more cautious about large-scale rollouts, especially when workplace programs touch sensitive employee records or regulated processes. The problem is more serious in large organizations where several systems have been layered over time, which limits how quickly the South America digital workplace market can convert strong demand into completed deployments. It also shifts spending toward longer service engagements, because vendors must solve data mapping, access control, and process redesign before the customer can use the full platform value. As a result, the South America digital workplace market continues to grow strongly, but integration complexity still delays adoption speed and margin realization across many enterprise projects.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Employee Experience and Workflow Orchestration

- Security-First Endpoint and Identity Management Prioritization

- Skills Shortage in Workplace Digitalization and Endpoint Security

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions captured 64.93% of the South America digital workplace market in 2025, indicating that buyers still place the greatest weight on core software platforms that unify communication, files, workflows, and employee-facing tools. This lead also reflects the way enterprise customers now prefer fewer strategic suites rather than scattered point tools that create separate logins, support, and governance burdens. In the South America digital workplace market, this pattern supports vendors that can combine collaboration, productivity, analytics, and automation within a single commercial model. SAP reported in 2025 that 55% of South American decision-makers planned to increase AI investment, which supports the move toward richer solution suites where AI features are embedded into everyday work rather than sold as separate products.

Solutions are projected to expand at a 20.48% CAGR through 2031, which keeps this category at the center of new contract activity in the South America digital workplace market. Services remain smaller in share, but they continue to grow in importance as customers need implementation, integration, change management, and ongoing support as workplace platforms become more intelligent and connected. Kyndryl's April 2026 launch of its AI-powered Digital Twin for the Workplace shows how service-oriented firms are moving beyond labor-based delivery to offer workplace monitoring, prediction, and operational improvement as part of the wider platform model. That shift suggests the digital workplace industry is no longer splitting neatly between software and services, as large deals increasingly depend on both. Over time, the stronger vendors in the South America digital workplace market are likely to be those that can pair software depth with credible delivery, governance, and operational support across the full workplace environment.

Cloud held 58.32% of the South America digital workplace market share in 2025, and cloud is also the fastest-growing deployment mode with a 20.64% CAGR through 2031. This leadership reflects a clear regional shift toward platforms that can scale more easily across distributed teams, mobile users, and growing data needs without the heavier maintenance burden of fully local environments. The South America digital workplace market for cloud deployment continues to benefit from stronger local infrastructure, as buyers are more willing to place sensitive collaboration and workflow functions on cloud platforms when latency and locality concerns are easier to manage. Microsoft's BRL 14.7 billion (USD 2.9 billion) investment in Brazil supports that change by strengthening the underlying environment for enterprise cloud and AI adoption.

Hybrid deployment still holds an important place in the South America digital workplace market because some enterprises need a staged path that keeps selected workloads closer to internal systems or sensitive data controls. This is especially relevant where organizations run older applications that cannot be moved quickly, or where sector rules and internal policy still favor a mixed architecture during transition. On-premises deployment is losing relative weight, but it remains present in parts of government, critical operations, and organizations that are still early in digital modernization. Colombia's role as host to 12.8% of the region's digital firms also supports cloud-oriented demand, because many digital-native businesses adopt modern collaboration and security tools earlier and with less legacy friction than older enterprises. The result is that cloud remains the main growth engine across the South America digital workplace market, while hybrid serves as a practical bridge for customers modernizing in stages rather than in one step.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- Hybrid

- On-Premises

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

List of Companies Covered in this Report:

- Microsoft Corporation

- International Business Machines Corporation

- Accenture PLC

- Google LLC

- Amazon Web Services, Inc.

- Cisco Systems, Inc.

- Citrix Systems, Inc.

- Oracle Corporation

- SAP SE

- Hewlett Packard Enterprise Development LP

- DXC Technology Company

- Capgemini SE

- Tata Consultancy Services Limited

- Infosys Limited

- Wipro Limited

- Kyndryl Holdings, Inc.

- Unisys Corporation

- Atos SE

- Cognizant Technology Solutions Corporation

- Globant S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hybrid Work Adoption in Enterprise Operations

- 4.2.2 Security-First Endpoint and Identity Management Prioritization

- 4.2.3 Cloud Migration of Collaboration and Virtual Workspace Stacks

- 4.2.4 Expansion of Managed Digital Workplace Outsourcing

- 4.2.5 Localization Pressure From Data Residency and Sovereignty Rules

- 4.2.6 AI-Assisted Employee Experience and Workflow Orchestration

- 4.3 Market Restraints

- 4.3.1 Legacy Application Integration Complexity

- 4.3.2 Skills Shortage in Workplace Digitalization and Endpoint Security

- 4.3.3 Fragmented Cross-Border Compliance Requirements

- 4.3.4 Limited Rural Connectivity and Uneven Network Quality

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 Hybrid

- 5.2.3 On-Premises

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Chile

- 5.5.4 Colombia

- 5.5.5 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 International Business Machines Corporation

- 6.4.3 Accenture PLC

- 6.4.4 Google LLC

- 6.4.5 Amazon Web Services, Inc.

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Citrix Systems, Inc.

- 6.4.8 Oracle Corporation

- 6.4.9 SAP SE

- 6.4.10 Hewlett Packard Enterprise Development LP

- 6.4.11 DXC Technology Company

- 6.4.12 Capgemini SE

- 6.4.13 Tata Consultancy Services Limited

- 6.4.14 Infosys Limited

- 6.4.15 Wipro Limited

- 6.4.16 Kyndryl Holdings, Inc.

- 6.4.17 Unisys Corporation

- 6.4.18 Atos SE

- 6.4.19 Cognizant Technology Solutions Corporation

- 6.4.20 Globant S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)