|

市場調查報告書

商品編碼

2073109

碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Carbon-Intelligent Remote Work and Digital Workplace Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

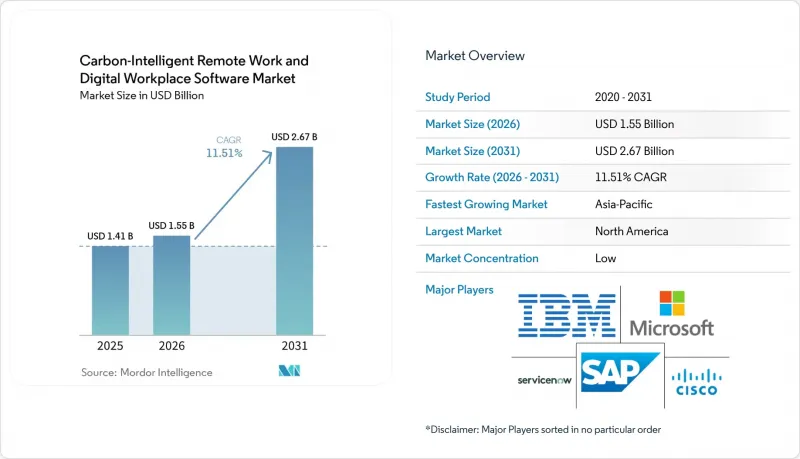

根據 Mordor Intelligence 預測,碳智慧遠距辦公和數位化工作場所軟體市場將從 2025 年的 14.1 億美元和 2026 年的 15.5 億美元成長到 2031 年的 26.7 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按元件(軟體平台、服務)、部署模式(雲端、本地部署、混合部署)、企業規模(大型企業等)、應用程式(協作和數位化工作場所體驗等)、最終用戶(IT和通訊業等)以及地區進行細分。市場預測以美元計價。

全球低碳智慧遠距辦公和數位化工作場所軟體市場趨勢及洞察

混合辦公模式正變得越來越普遍。

混合辦公模式仍然是推動低碳遠距辦公和數位化工作場所軟體市場發展的結構性驅動力。這是因為雇主仍然需要可靠的系統來確保協作、考勤安排、數位化存取和工作流程的連續性。到了2026年,62%的組織機構規定員工每週必須到辦公室辦公的天數,高於前一年的49%。同時,每週工作3-4天的員工比例上升至55%。 2026年4月進行的另一項調查凸顯了員工意願與實際職場行為之間的明顯差距:62%的受訪者認為增加在家工作以降低能源成本是合理的,但只有20%的受訪者真正這樣做。這一差距意義重大,因為如果沒有能夠將日程安排、通勤模式、地點選擇和能源使用情況整合到單一營運記錄中的軟體,組織機構就無法將混合辦公模式轉化為可衡量的成本和碳減排成果。因此,「低碳遠距辦公和數位化工作場所軟體市場」受益於多年的業務轉型,而非對以往職場環境中斷的臨時應對措施。能夠將混合工作管理與可審計的碳核算相結合的供應商處於更有利的地位,因為買家越來越希望找到一個既能支持員工調整又能支援資訊揭露準備的單一系統。

擴展人工智慧驅動的工作流程編配

隨著企業從孤立的AI工具轉向支援跨職能營運的協作系統,AI編配正成為碳智慧遠距辦公和數位化工作場所軟體市場中最顯著的競爭優勢之一。 2026年5月,一款新一代編配平台發布,該平台定位為企業管理眾多AI代理的“代理控制平面”,並遵循通用的管治規則。同樣在2026年5月,一款新的永續發展AI代理商發布,計畫於2026年底正式上線。 Beta測試將碳排放場景的模擬時間從一天縮短至20分鐘,並將GHS分類的人工工作量減少了高達80%。這項進展意義重大,因為AI工作流程層還能產生流程日誌、資源記錄和運作訊號,有助於在同一軟體環境中衡量和報告碳排放。正是由於這種協同效應,碳智慧遠距辦公和數位化工作場所軟體市場正在蓬勃發展。企業可以透過強調生產力的提升和對資訊揭露的支持來證明其投資的合理性。從長遠來看,將編配視為員工管理和永續發展功能共用基礎設施的供應商,比將碳管理工具與其營運軟體分開的供應商更有優勢。

與傳統身分管理和協作系統進行複雜整合。

由於先進的工作場所平台需要同時連接眾多傳統企業系統,傳統系統的複雜性仍然是「碳智慧遠距辦公和數位化工作場所軟體市場」推廣應用的主要障礙。根據一份2025年現代化報告,35%的IT決策者認為技術債和傳統系統的複雜性是現代化的主要限制因素,而54%的決策者表示,他們推動現代化是為了將傳統工作負載與雲端原生平台整合。這項挑戰不僅限於基礎設施,因為大型企業通常維護多個身分識別提供者和過時的目錄環境,這使得它們難以與現代工作場所工具無縫整合。這對「碳智慧遠距辦公和數位化工作場所軟體市場」的影響尤其顯著,因為這些平台通常需要在不同的存取模式下存取人力資源系統、設施管理系統、資產管理系統、協作數據和ERP記錄。 2025年企業整合調查還指出,與傳統資料庫的連接以及數據標準不匹配是主要的整合挑戰,這反映了更廣泛的“數據摩擦”,阻礙了整合工作場所和碳排放報告的普及。低估這項負擔的組織往往會面臨引進週期延長和價值實現延遲的問題。因此,整合架構、現成連接器和存取設計與產品功能同等重要。

細分市場分析

到2025年,軟體平台將佔總收入的81.13%,在「碳智慧遠距辦公和數位化工作場所軟體市場」中佔據絕對領先地位。這種集中度反映的是企業的採購行為,而非狹隘的功能偏好,因為大多數大型企業傾向於先將工作場所功能整合到其主要軟體環境中,然後再添加專用工具。因此,「碳智慧遠距辦公和數位化工作場所軟體市場」仍然圍繞著那些已經支援協作、工作流程、身分管理以及業務資料在整個企業範圍內流動的平台。這一趨勢也有利於能夠提供更廣泛的營運層供應商,因為買家更傾向於為現有企業系統添加模組,而不是建立一個獨立的、隔離的環境。這種以平台為中心的結構表明,客戶在選擇如今也需要滿足碳排放報告要求的工作場所軟體時,仍然優先考慮系統連續性、共用管治以及減少整合帶來的摩擦。

此外,軟體平台市場預計到2031年將以12.13%的複合年成長率成長,顯示這一關鍵組成部分正在加速發展,而非因自身發展而放緩。排放代理就是一個典型的例子,它們將碳足跡模擬、法規遵循、標籤任務和職場安全工作流程整合到更廣泛的企業平台中,而不是作為獨立應用程式運作。排放API也推動類似的趨勢,使公司和供應商能夠將排放計算直接整合到現有工作流程中,而無需用戶使用單獨的介面。從實際角度來看,隨著組織在單一核心環境中建立排放基準、計畫歷史記錄和終端記錄,切換成本將增加,「碳智慧遠端辦公和數位化工作場所軟體市場」將逐漸變得更加平台化。雖然服務部分仍然很重要,因為大規模主導需要客製化、變更管理和複雜的整合支持,但其主要作用是實現更廣泛平台的價值,而不是改變軟體的重心。

到2025年,基於雲端的部署將佔「碳智慧遠距辦公和數位化工作場所軟體市場」收入的67.14%,成為該市場的主要交付模式。這一主導地位反映了基於SaaS的工作場所工具的成熟,以及企業對跨地域、跨裝置和跨業務部門可擴展存取的需求日益成長。此外,雲端環境使供應商能夠以最小的升級延遲向現有基本客群交付新的AI功能、報告更新和工作場所改進。因此,「碳智慧遠距辦公和數位化工作場所軟體市場」將繼續依賴雲端作為尋求更快部署和更便捷的跨站點訪問的組織的預設入口點。在成熟的企業市場中,這一趨勢尤其明顯,因為數位化協作套件和雲端工作流程軟體已成為日常營運的一部分。

預計到2031年,混合部署將以13.43%的複合年成長率成長,顯示資料處理和報告的準確性正日益影響架構決策。 《碳永續報告直接指南》(CSRD)要求同時進行基於市場和基於位置的排放報告,一些公司正鼓勵在混合環境中保留部分碳數據處理和匹配工作。雲端提供者的調查方法在此問題上並不總是一致,這為在多重雲端環境中維護本地處理層提供了實際理由。根據2026年的雲端報告,近三分之一的受訪者認為成本最佳化和排放碳同等重要,47%的歐洲受訪者表示已製定明確的永續發展計畫。在銀行、國防和政府機構等產業,本地部署仍然至關重要,因為這些產業對資料居住和管理的要求仍然很嚴格。因此,「碳智慧遠距辦公和數位化工作場所軟體市場」在雲端採用率不斷提高的同時,也為混合設計提供了空間,以支援審計合規性和碳數據準確性。

區域分析

2025年,北美地區佔全球銷售額的39.12%,引領「碳智慧遠距辦公和數位化工作場所軟體市場」。該地區受惠於對雲端原生工作場所平台的早期投資,以及企業對Microsoft 365和Google Workspace的廣泛採用。美國仍然是最大的國內市場,因為大型企業已經經營著廣泛的協作和工作流程環境,這使它們能夠以最小的營運影響實施新的碳排放和永續性相關功能。 2026年1月,微軟在Sustainability Manager中正式發布了產品碳足跡(Product Carbon Footprint)功能,並增強了其現有企業軟體基礎架構中的碳排放運算能力。此外,將於2026年生效的加州氣候資訊揭露法規,也增加了對能夠整合排放報告、風險文件和內部營運數據的軟體的迫切需求。

2025年,歐洲仍是全球第二大區域市場,也是監管最主導的地區。 2026年4月,德國聯邦統計局宣布,2025年約有25%的員工至少偶爾在家工作,顯示遠程辦公的規模與正式的報告要求密切相關。法國環境與能源管理署(ADEME)針對遠程辦公碳排放所做的努力,也促使人們更有系統地思考如何將遠距辦公納入更廣泛的碳計量實務中。德國、英國、法國、義大利和西班牙繼續保持其作為主要國內市場的地位,同時大型企業的需求強勁,且氣候相關資訊揭露勢頭強勁。此外,歐盟人工智慧法加強了對產品的審查,要求對職場的分析(包括對員工的推論)進行更謹慎的設計和記錄。

預計到2031年,亞太地區的複合年成長率將達到13.83%,成為市場規模成長最快的地區。印度和中國是絕對成長的最大貢獻者,這主要得益於大規模企業基礎架構中企業軟體支出的不斷成長。隨著上市公司逐步滿足更正式的ESG(環境、社會和治理)資訊揭露要求,日本和韓國的需求也正在增強。仲量聯行指出,到2026年,亞太地區的全員到崗率將位居全球之首。這表明,該地區的需求特徵與歐美市場有所不同,歐美市場的軟體需求通常與辦公室能源最佳化和終端電源管理密切相關。儘管南美洲和中東及非洲的市場規模仍然小規模,但巴西和阿拉伯聯合大公國因其在推動大型企業更廣泛的永續發展資訊揭露框架方面發揮的重要作用而脫穎而出。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 混合辦公模式正變得越來越普遍。

- 企業對整合式員工體驗平台的需求

- 擴展人工智慧驅動的工作流程編配

- 工作場所對碳排放的可視化和最佳化需求日益成長。

- 與數位業務報告相關的合規壓力

- 財務營運轉型與永續性的融合

- 市場限制因素

- 與傳統身分和協作系統進行複雜整合。

- 對資料隱私和員工監控的擔憂

- 先進平台的總擁有成本高

- 碳數據零散且基準品質差

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體平台

- 服務

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 按公司規模

- 大公司

- 小型企業

- 透過使用

- 協作與數位化工作場所體驗

- 員工福祉與生產力分析

- 工作流程自動化與流程編配

- 碳資訊、追蹤和報告

- 最佳化終端效能和資源

- 最終用戶

- IT/通訊

- BFSI

- 製造業

- 能源公用事業

- 零售與電子商務

- 建築和基礎設施

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- International Business Machines Corporation

- SAP SE

- ServiceNow, Inc.

- Broadcom Inc.

- Citrix Systems, Inc.

- Workiva Inc.

- Schneider Electric SE

- Hewlett Packard Enterprise Company

- Google LLC

- Cisco Systems, Inc.

- Accenture plc

- Eviden

- DXC Technology Company

- Tata Consultancy Services Limited

- Cognizant Technology Solutions Corporation

- Wipro Limited

- Infosys Limited

- Capgemini SE

- Unisys Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the carbon-Intelligent remote work and Digital Workplace Software Market size is projected to expand from USD 1.41 billion in 2025 and USD 1.55 billion in 2026 to USD 2.67 billion by 2031, registering a CAGR of 11.51% between 2026 and 2031.

This report is Segmented by Component (Software Platform, and Services), Deployment Model (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises, and More), Application (Collaboration and Digital Workplace Experience, and More), End User (IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Carbon-Intelligent Remote Work and Digital Workplace Software Market Trends and Insights

Rising Hybrid Work Persistence

Hybrid work remains a structural driver of the Carbon-Intelligent Remote Work and Digital Workplace Software Market, as employers still need a reliable system for collaboration, attendance planning, digital access, and workflow continuity. In 2026, 62% of organizations mandated a fixed number of in-office days, up from 49% a year earlier, while the share of employees attending the office 3 to 4 days per week rose to 55%. Another study in April 2026 found that 62% of respondents considered it sensible to work more from home to reduce energy costs, while only 20% currently do so, highlighting a clear gap between employee preferences and actual workplace behavior. That gap matters because organizations cannot turn hybrid work into measurable cost and carbon outcomes without software that connects schedules, commuting patterns, location choices, and energy use into a single operating record. The Carbon-Intelligent Remote Work and Digital Workplace Software Market is therefore benefiting from a multi-year operating shift rather than a short-lived response to earlier workplace disruption. Vendors that can link hybrid work management with auditable carbon accounting are in a stronger position, as buyers increasingly want a single system to support both employee coordination and disclosure readiness.

Expansion of AI-Powered Workflow Orchestration

AI orchestration is becoming one of the clearest competitive differentiators in the Carbon-Intelligent Remote Work and Digital Workplace Software Market, as enterprises move away from isolated AI tools toward coordinated systems that can execute work across functions. In May 2026, the next generation of an orchestration platform was unveiled and positioned as an agentic control plane for enterprises managing large fleets of AI agents under common governance rules. New sustainability AI agents were also announced in May 2026, targeting general availability by the end of 2026, and beta testing reduced carbon scenario simulation time from 1 day to 20 minutes while cutting manual GHS classification effort by up to 80%. These moves matter because AI workflow layers also generate process logs, resource records, and operational signals that are useful for carbon measurement and reporting within the same software environment. The Carbon-Intelligent Remote Work and Digital Workplace Software Market is gaining from that overlap because enterprises can justify the investment through both productivity gains and disclosure support. Vendors that treat orchestration as shared infrastructure for workforce and sustainability functions are building a stronger long-term position than vendors that keep carbon tools separate from operational software.

Complex Integration With Legacy Identity and Collaboration Stack

Legacy complexity remains a major adoption barrier for the Carbon-Intelligent Remote Work and Digital Workplace Software Market because advanced workplace platforms must connect to many older enterprise systems simultaneously. A 2025 modernization report found that 35% of IT decision-makers cited technical debt and legacy complexity as the main constraint on modernization, while 54% were pursuing modernization to integrate legacy workloads with cloud-native platforms. The challenge is wider than infrastructure because large enterprises often maintain multiple identity providers and older directory environments that are harder to federate cleanly with modern workplace tools. The Carbon-Intelligent Remote Work and Digital Workplace Software Market is affected more sharply because these platforms often need access to HR systems, facilities systems, asset management systems, collaboration data, and ERP records under different access models. Research in 2025 on enterprise integration also identified legacy database connections and inconsistent data standards as key integration issues, reflecting the broader data friction that slows unified workplace and carbon reporting deployments. Organizations that underestimate this burden often face longer implementation cycles and slower value realization, which is why integration architecture, pre-built connectors, and access design matter as much as product functionality.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise Demand for Unified Employee Experience Platforms

- Growing Need for Workplace Carbon Visibility And Optimization

- Data Privacy and Employee Monitoring Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software Platform accounted for 81.13% of revenue in 2025, giving it a clear lead in the Carbon-Intelligent Remote Work and Digital Workplace Software Market share. That concentration reflects enterprise buying behavior more than a narrow feature preference because most large organizations place workplace functions inside a primary software environment before adding specialist tools. The Carbon-Intelligent Remote Work and Digital Workplace Software Market, therefore, remains centered on platforms that already support collaboration, workflows, identity, and the movement of operational data across the business. This pattern also favors vendors that can offer a broader operating layer, as buyers prefer to add modules to existing enterprise systems rather than create another isolated environment. The platform-heavy structure shows that customers still value system continuity, shared governance, and reduced integration friction when choosing workplace software that now also addresses carbon reporting requirements.

Software Platform is also projected to expand at a 12.13% CAGR through 2031, indicating the leading component is still gaining traction rather than slowing under its own weight. Sustainability agents are a good example because they embed footprint simulation, regulatory readiness, labeling tasks, and workplace safety workflows within a broader enterprise platform rather than a standalone application. Emissions APIs support the same direction by allowing enterprises and software vendors to embed emissions calculations directly into existing workflows, rather than forcing users into a separate interface. In practical terms, the Carbon-Intelligent Remote Work and Digital Workplace Software Market becomes increasingly platform-led over time because switching costs rise as organizations build emissions baselines, scheduling histories, and endpoint records within a single core environment. The services segment remains important because large deployments still need customization, change management, and complex integration support, but its role is mainly to enable broader platform value rather than displace the software center of gravity.

Cloud-based deployment accounted for 67.14% of revenue in 2025, making it the dominant delivery model in the Carbon-Intelligent Remote Work and Digital Workplace Software Market. This lead reflects the maturity of software-as-a-service workplace tools and the preference for scalable access across locations, devices, and business units. Cloud environments also help vendors release new AI features, report updates, and introduce workplace enhancements to installed customer bases with fewer upgrade delays. The Carbon-Intelligent Remote Work and Digital Workplace Software Market has therefore continued to rely on the cloud as the default entry point for organizations seeking faster rollouts and easier cross-site access. That position is especially strong in mature enterprise markets where digital collaboration suites and cloud workflow software are already part of daily operations.

Hybrid deployment is projected to grow at a 13.43% CAGR through 2031, indicating that data processing and reporting precision are gaining influence in architectural decisions. It was noted that CSRD requires both market-based and location-based emissions reporting, which has pushed some enterprises to keep part of their carbon data processing or reconciliation in hybrid environments. Cloud provider methodologies have not always aligned equally on this issue, which creates a practical reason to retain local processing layers in multi-cloud environments. A 2026 cloud report found that nearly 1 out of 3 respondents considered cost optimization and carbon emissions reduction equal priorities, while 47% of European respondents reported defined sustainability programs. On-premise deployment still holds a place in banking, defense, and government settings where data residency and control requirements remain strict, so the Carbon-Intelligent Remote Work and Digital Workplace Software Market is expanding cloud usage while also creating more room for hybrid designs that support audit readiness and carbon data accuracy.

Complete Report Scope:

- By Component

- Software Platform

- Services

- By Deployment Model

- Cloud-Based

- On-Premise

- Hybrid

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By Application

- Collaboration and Digital Workplace Experience

- Employee Wellbeing and Productivity Analytics

- Workflow Automation and Process Orchestration

- Carbon Intelligence, Tracking and Reporting

- Endpoint Performance and Resource Optimization

- By End User

- IT and Telecom

- BFSI

- Manufacturing

- Energy and Utilities

- Retail and E-Commerce

- Construction and Infrastructure

- Government and Public Sector

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America accounted for 39.12% of revenue in 2025, making it the leading region in the Carbon-Intelligent Remote Work and Digital Workplace Software Market. The region benefited from early investment in cloud-native workplace platforms and deeper enterprise use of Microsoft 365 and Google Workspace. The United States remained the largest national market because large enterprises already operated broad collaboration and workflow environments that could absorb new carbon and sustainability features with less disruption. Microsoft brought Product Carbon Footprint to general availability in January 2026 within Sustainability Manager, strengthening carbon accounting capability inside an established enterprise software base. California's climate disclosure rules, taking effect in 2026, also expanded the practical need for software that can connect emissions reporting, risk documentation, and internal operating data.

Europe was the second-largest regional segment in 2025, and it remained the most regulation-driven part of the market. Germany's Federal Statistical Office stated in April 2026 that 25% of all employed persons worked from home at least occasionally in 2025, showing the scale of telework that now intersects with formal reporting expectations. France's ADEME-linked telework carbon work also supported more structured thinking about how remote work should be integrated into broader carbon accounting practices. Germany, the United Kingdom, France, Italy, and Spain remained the leading national markets because each combined large enterprise demand with stronger momentum for climate-related disclosures. The EU AI Act also added another layer of product scrutiny, requiring workplace analytics that involve employee inferences to be designed and documented with greater care.

Asia-Pacific is projected to grow at a 13.83% CAGR through 2031, making it the fastest-growing geography in the market size outlook. India and China are providing the largest absolute growth contribution because enterprise software spending is expanding across large business bases. Japan and South Korea are also strengthening demand as listed companies move into more formal ESG disclosure expectations. JLL stated in 2026 that APAC led globally in full in-office attendance rates, giving the region a different demand profile from Western markets, as software needs are often more closely tied to office energy optimization and endpoint power management. South America, the Middle East, and Africa remain smaller markets, but Brazil and the United Arab Emirates stand out because both are advancing broader sustainability disclosure frameworks for large enterprises.

- Microsoft Corporation

- International Business Machines Corporation

- SAP SE

- ServiceNow, Inc.

- Broadcom Inc.

- Citrix Systems, Inc.

- Workiva Inc.

- Schneider Electric SE

- Hewlett Packard Enterprise Company

- Google LLC

- Cisco Systems, Inc.

- Accenture plc

- Eviden

- DXC Technology Company

- Tata Consultancy Services Limited

- Cognizant Technology Solutions Corporation

- Wipro Limited

- Infosys Limited

- Capgemini SE

- Unisys Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Hybrid Work Persistence

- 4.2.2 Enterprise Demand for Unified Employee Experience Platforms

- 4.2.3 Expansion of AI-Powered Workflow Orchestration

- 4.2.4 Growing Need for Workplace Carbon Visibility and Optimization

- 4.2.5 Compliance Pressure From Digital Operations Reporting

- 4.2.6 Shift Toward FinOps and Sustainability Convergence

- 4.3 Market Restraints

- 4.3.1 Complex Integration With Legacy Identity and Collaboration Stacks

- 4.3.2 Data Privacy and Employee Monitoring Concerns

- 4.3.3 High Total Cost of Ownership for Advanced Platforms

- 4.3.4 Fragmented Carbon Data and Weak Baseline Quality

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platform

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Collaboration and Digital Workplace Experience

- 5.4.2 Employee Wellbeing and Productivity Analytics

- 5.4.3 Workflow Automation and Process Orchestration

- 5.4.4 Carbon Intelligence, Tracking and Reporting

- 5.4.5 Endpoint Performance and Resource Optimization

- 5.5 By End User

- 5.5.1 IT and Telecom

- 5.5.2 BFSI

- 5.5.3 Manufacturing

- 5.5.4 Energy and Utilities

- 5.5.5 Retail and E-Commerce

- 5.5.6 Construction and Infrastructure

- 5.5.7 Government and Public Sector

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 International Business Machines Corporation

- 6.4.3 SAP SE

- 6.4.4 ServiceNow, Inc.

- 6.4.5 Broadcom Inc.

- 6.4.6 Citrix Systems, Inc.

- 6.4.7 Workiva Inc.

- 6.4.8 Schneider Electric SE

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Google LLC

- 6.4.11 Cisco Systems, Inc.

- 6.4.12 Accenture plc

- 6.4.13 Eviden

- 6.4.14 DXC Technology Company

- 6.4.15 Tata Consultancy Services Limited

- 6.4.16 Cognizant Technology Solutions Corporation

- 6.4.17 Wipro Limited

- 6.4.18 Infosys Limited

- 6.4.19 Capgemini SE

- 6.4.20 Unisys Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)