|

市場調查報告書

商品編碼

2073231

歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Europe Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

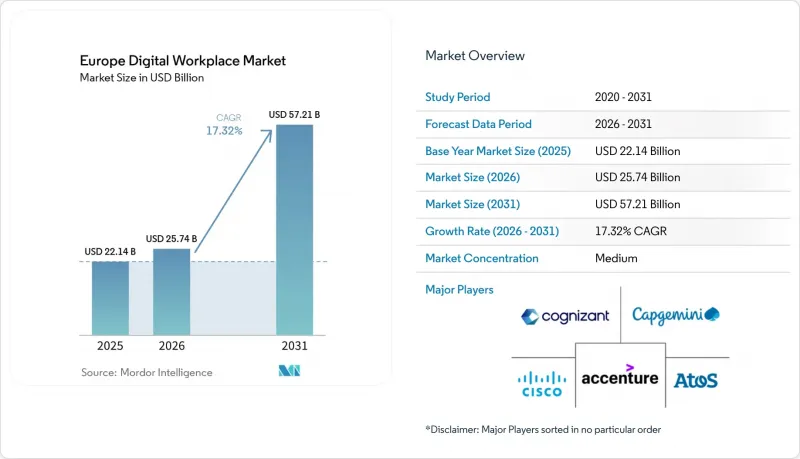

根據 Mordor Intelligence 預測,歐洲數位工作場所市場規模預計將在 2025 年達到 221.4 億美元,2026 年達到 257.4 億美元,到 2031 年達到 572.1 億美元,2026 年至 2031 年的複合年成長率為 17.32%。

本報告按組件(解決方案和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、最終用戶行業(IT和電信、銀行、金融服務和保險、醫療保健、製造業、政府和公共部門、教育等)以及地區進行細分。市場規模和預測均以美元計價。

歐洲數位化工作場所市場的趨勢與洞察

繼續推行混合辦公和遠距辦公模式

隨著混合辦公模式逐漸融入眾多歐洲雇主的業務發展、團隊合作和人才管理方式,歐洲數位化工作場所市場日益關注的是長期的工作場所重塑,而非短期的業務永續營運支出。這種轉變推動了對雲端協作、虛擬桌面存取、終端控制和工作流程工具的需求成長,以確保員工在家中、辦公室和行動辦公室環境中獲得一致的體驗。企業採購行為也正在改變。企業不再僅僅追求通訊功能,而是更重視跨分散式團隊的存取管治、設備可見性和高品質支援。隨著混合辦公模式的日益普及,許多組織開始意識到,各種工具的混雜使用會造成營運摩擦、削弱策略執行力並推高支援成本,從而催生了對平台整合的新需求。這一趨勢有助於解釋為何歐洲數位化工作場所市場的支出正從孤立的獨立產品轉向更全面的工作場所套件。隨著混合辦公模式成為日常業務實踐不可或缺的一部分,對能夠支援柔軟性且不影響安全性、監控或易用性的整合式數位化工作場所平台的需求也變得更加迫切。

企業正在轉向員工體驗平台和去中心化體驗分析。

歐洲數位化工作場所市場的發展也受到企業日益關注員工體驗平台和數位化員工體驗衡量的推動,因為雇主希望簡化工作場所技術的管理和使用。企業正在摒棄被動式服務模式(即IT團隊在問題發生後才做出回應),轉而建構能夠持續監控終端、工作流程和支援訊號的環境。這種轉變至關重要,因為糟糕的使用者體驗不僅影響IT部門的滿意度,還會影響跨部門的生產力、人才保留率和工具採用率。數位化體驗平台(DEX平台)的重要性日益凸顯,因為它們有助於在工作流程瓶頸、應用程式過度使用、終端效能下降和支援不足等問題升級為更大的營運難題之前,識別這些問題。商業性影響同樣重要,因為能夠識別未充分利用的許可證和冗餘工具的買家更有可能整合供應商,並將預算重新投入到能夠帶來可衡量結果的更全面的套件中。因此,歐洲數位化工作場所市場正朝著整合分析、自動化和服務可見性的整合平台發展,而不是將它們作為單獨的層級提供。

舊有應用程式的激增及其整合的複雜性。

在歐洲數位化工作場所市場,舊有應用程式的氾濫仍然是最持久的營運障礙。這是因為許多公司仍在管理龐大且分散的軟體資產,這些資產並非為建構單一現代化的員工環境而設計。這個問題不僅限於軟體過時,還包括資料模型脫節、協作層冗餘以及身分結構碎片化等問題,所有這些都會延緩合約簽訂後的轉型進程。當企業嘗試對這些環境進行現代化改造時,整合計畫往往會被推遲,使用者部署速度也會變慢,服務成本會增加,跨地域和跨部門的支援一致性也會受到影響。這種延遲還會導致另一個問題:業務部門通常會在正式遷移工作仍在進行時就採用非正式工具,這進一步加劇了下一階段整合的複雜性。因此,工作場所轉型的真正成本往往更多地取決於將遺留工作流程、應用程式和資料結構整合為整體所需的工作量,而不是平臺本身的成本。這項限制在歐洲數位化工作場所市場尤其重要,因為該市場中的企業在嚴格的監管下進行大量工作,並力求在不中斷營運的情況下現代化。

細分市場分析

到2025年,解決方案將佔各細分市場的64.58%,這顯示軟體平台仍是歐洲整體數位化工作場所市場的主要支出領域。這一比例反映了市場對整合通訊與協作、整合終端管理、工作流程自動化、知識管理、虛擬桌面基礎架構以及數位化員工體驗工具的持續需求。在許多合約中,軟體獲得的直接投資比交付支援更多,因為採購公司仍在建立其工作場所技術棧的功能層。這一趨勢也表明,許多公司仍在確定哪些工作場所功能應在平台層面進行標準化,然後再全面建立長期服務架構。短期內,歐洲數位化工作場所市場的解決方案細分市場將繼續受益於雇主對通訊、工作流程、支援和合規性等方面的全面編配的需求。

儘管服務在直接收入佔有率方面落後於解決方案,但它們仍然發揮著至關重要的作用。這是因為許多工作場所程式需要整合、遷移、維運管理和管治支援才能在實際業務環境中運作軟體。隨著環境變得日益複雜,服務供應商不再僅僅需要部署許可證;他們必須將工作場所套件與安全控制、身分管理系統和舊有應用程式整合。這意味著服務層扮演著更具策略性的角色,尤其是當客戶需要特定產業的部署、自主託管設計或穩定的部署後維運支援時。因此,歐洲數位化工作場所產業並非簡單地轉向純產品模式,因為軟體的優勢和服務深度正日益相互補充。從長遠來看,歐洲數位化工作場所市場中最具韌性的供應商很可能是那些能夠將核心工作場所軟體與部署技能、管治支援和生命週期管理打包成單一整合提案的供應商。

預計到2031年,雲端採用率將以19.78%的複合年成長率成長,成為歐洲數位化工作場所市場成長最快的部署模式。這反映出企業正從資本密集的本地部署環境向可更快更新、更統一管理分散式員工隊伍的平台進行廣泛轉變。企業也利用雲端來縮短引進週期、提高終端可見性,並在包括辦公室、遠端和行動辦公室在內的各種工作環境中集中執行策略。對於許多買家而言,雲端採用如今已成為與合規規劃同等重要的關鍵議題,因為資料儲存位置、可審計性和服務彈性與基礎架構的柔軟性同等重要。這些因素使得雲端成為歐洲數位化工作場所市場建構新工作場所和進行大規模現代化改造的首選方案。

微軟於 2025 年 2 月完成歐盟資料邊界的建設,進一步強化了依賴微軟生產力工具和雲端環境的受監管雇主遷移到雲端的必要性。這是因為這些客戶現在擁有更清晰的區域處理路徑來處理其關鍵工作場所的工作負載。在國防、關鍵基礎設施和某些金融服務等嚴格控制的環境中,本地部署仍然有價值,因為隔離仍然是採購的必要條件。然而,中間方案正日益轉向混合架構,該架構將對特定工作負載的本地控制與雲端的可擴展性相結合,以實現協作、分析和服務管理。這意味著部署選擇不再是簡單的二選一,而是設計合規驅動型架構的挑戰。隨著這些趨勢的持續發展,能夠支持自主混合模式的供應商預計將在歐洲數位化工作場所市場佔據更大的新契約佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建立混合辦公和遠距辦公模式

- 企業向員工體驗平台和分散式帳本分析的遷移

- 商用應用程式和終端用戶運算的雲端遷移

- GDPR、資料主權和「安全設計」要求

- 歐盟人工智慧法律與管治—合規的職場自動化

- 對與可衡量的生產力、情緒和體驗相關的遙測數據的需求

- 市場限制因素

- 擴展和整合舊有應用程式的複雜性

- 跨境工作流程中資料居住要求的限制

- 中型企業轉型總成本高

- 工具的激增會導致使用者疲勞和抵制變革。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 整合通訊與協作

- 整合端點管理

- 企業行動管理

- 員工體驗平台與內網

- 工作流程自動化與知識管理

- 虛擬桌面基礎架構與雲端電腦

- 服務

- 解決方案

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 衛生保健

- 製造業

- 零售

- 政府/公共部門

- 教育

- 能源公用事業

- 法律與專業服務

- 其他終端用戶產業

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 北歐的

- 俄羅斯

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- Atos SE

- Capgemini SE

- Cisco Systems, Inc.

- Cognizant Technology Solutions Corporation

- Computacenter plc

- DXC Technology Company

- Fujitsu Limited

- Getronics Holding BV

- HCL Technologies Limited

- Hewlett Packard Enterprise Company

- IBM Corporation

- Infosys Limited

- Kyndryl Holdings, Inc.

- NTT DATA Group Corporation

- SAP SE

- ServiceNow, Inc.

- SoftwareOne Holding AG

- Tata Consultancy Services Limited

- Telefonica, SA

- Wipro Limited

- Zensar Technologies Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe digital workplace market size is projected to be USD 22.14 billion in 2025, USD 25.74 billion in 2026, and reach USD 57.21 billion by 2031, growing at a CAGR of 17.32% from 2026 to 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecommunications, BFSI, Healthcare, Manufacturing, Government and Public Sector, Education, and More), and Geography. The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Europe Digital Workplace Market Trends and Insights

Sustained Adoption of Hybrid and Remote Work Models

Hybrid work is now embedded in how many European employers organize operations, team collaboration, and talent management, so the Europe digital workplace market is increasingly tied to long-term workplace redesign rather than short-term continuity spending. That shift is expanding demand for cloud collaboration, virtual desktop access, endpoint control, and workflow tools that keep employee experience consistent across home, office, and mobile environments. It also changes buying behavior, because companies no longer look only for communication features and now place greater weight on access governance, device visibility, and support quality across distributed teams. As hybrid work matures, many organizations are discovering that a patchwork of tools creates operational friction, weakens policy enforcement, and raises support costs, which is pushing fresh demand for platform consolidation. This pattern helps explain why spending is moving toward broader workplace suites instead of isolated point products in the Europe digital workplace market. The longer hybrid work remains part of normal operating practice, the stronger the case becomes for integrated digital workplace platforms that can support flexibility without losing security, oversight, or usability.

Enterprise Shift to Employee Experience Platforms and DEX Analytics

The Europe digital workplace market is also being driven by a stronger enterprise focus on employee experience platforms and digital employee experience measurement, as employers seek to make workplace technology easier to manage and use. Organizations are moving away from reactive service models in which IT teams respond only after issues arise and instead building environments where endpoints, workflows, and support signals are monitored continuously. That shift matters because poor user experience now affects not only IT satisfaction but also productivity, retention, and tool adoption across departments. DEX platforms are gaining relevance because they help companies identify workflow bottlenecks, application fatigue, poor endpoint performance, and support gaps before those issues grow into larger operational problems. The commercial impact is equally important because buyers who can see underused licenses or overlapping tools are more likely to consolidate vendors and reinvest budgets into broader suites with measurable results. This is pushing the European digital workplace market toward platforms that combine analytics, automation, and service visibility rather than offering those functions as separate layers.

Legacy Application Sprawl and Integration Complexity

Legacy application sprawl remains the most persistent operating barrier in the Europe digital workplace market, because many enterprises still manage large, uneven software estates that were not built to work as one modern employee environment. The problem runs beyond old software alone, since it also includes disconnected data models, duplicated collaboration layers, and fragmented identity structures that slow transformation after contracts are signed. When organizations try to modernize these environments, integration timelines often stretch, delaying user rollouts, increasing service costs, and weakening support consistency across locations and departments. That delay also creates a second problem: business units often adopt unofficial tools while formal migration work is still underway, adding more complexity to the next phase of consolidation. As a result, the true cost of workplace transformation is often shaped less by the target platform itself and more by the effort required to connect legacy workflows, applications, and data structures into a usable whole. This restraint is especially important in the European digital workplace market, where enterprise buyers want modernization without disrupting tightly regulated, high-volume operations.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Migration of Workplace Applications and End-User Computing

- GDPR, Data Sovereignty, and Security by Design Requirements

- Data Residency Constraints Across Cross-Border Workflows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions retained 64.58% of the component segment in 2025, which shows that software platforms remained the main spending center across the Europe digital workplace market. This weight reflects continued demand for unified communication and collaboration, unified endpoint management, workflow automation, knowledge management, virtual desktop infrastructure, and digital employee experience tools. Buyers are still building out the functional layer of the workplace stack, so software receives more direct investment than delivery support in many contracts. That pattern also suggests that many enterprises are still defining which workplace capabilities they want to standardize at the platform level before long-term service structures fully settle. In the near term, the solutions side of the Europe digital workplace market should continue to benefit from employers seeking broader orchestration across communication, workflow, support, and compliance.

Services remain important even though they sit behind solutions in terms of direct revenue share, because many workplace programs depend on integration, migration, managed operations, and governance support to turn software into operational business environments. As estates grow more complex, service providers are increasingly asked to connect workplace suites with security controls, identity systems, and legacy applications rather than simply deploy licenses. This gives the services layer a more strategic role, especially where clients need sector-specific implementation, sovereign hosting design, or steady operational support after rollout. The Europe digital workplace industry is therefore not moving toward a simple product-only model, because software strength and service depth increasingly reinforce each other. Over time, the most resilient vendors in the Europe digital workplace market are likely to be those that can package core workplace software with implementation skill, governance support, and lifecycle management under one coordinated offer.

Cloud is projected to grow at a 19.78% CAGR through 2031, making it the fastest-moving deployment mode within the Europe digital workplace market. This reflects a broad shift away from capital-intensive on-premises environments toward platforms that can be updated more quickly and managed more consistently across dispersed workforces. Enterprises are also using cloud to shorten deployment cycles, improve endpoint visibility, and simplify policy delivery across office, home, and mobile work settings. For many buyers, cloud adoption now sits alongside regulatory planning, because data location, auditability, and service resilience matter as much as infrastructure flexibility. These factors have made the cloud the leading path for new workplace builds and for major refresh cycles in the Europe digital workplace market.

Microsoft's completion of the EU Data Boundary in February 2025 strengthened the migration case for regulated employers that rely on Microsoft productivity and cloud environments, because those customers gained a clearer regional processing path for core workplace workloads. On-premises deployments still hold value in tightly controlled settings such as defense, critical infrastructure, and some financial services operations, where isolation remains a procurement requirement. Even so, the middle ground is increasingly shifting toward hybrid structures that combine local control for selected workloads with cloud elasticity for collaboration, analytics, and service management. This makes deployment choice less of a binary decision and more of a compliance-informed architecture exercise. As that dynamic plays out, providers that can support sovereign hybrid models are likely to capture a larger share of incremental contract value across the Europe digital workplace market.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-Premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By End-User Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-User Industries

- By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- Accenture plc

- Atos SE

- Capgemini SE

- Cisco Systems, Inc.

- Cognizant Technology Solutions Corporation

- Computacenter plc

- DXC Technology Company

- Fujitsu Limited

- Getronics Holding B.V.

- HCL Technologies Limited

- Hewlett Packard Enterprise Company

- IBM Corporation

- Infosys Limited

- Kyndryl Holdings, Inc.

- NTT DATA Group Corporation

- SAP SE

- ServiceNow, Inc.

- SoftwareOne Holding AG

- Tata Consultancy Services Limited

- Telefonica, S.A.

- Wipro Limited

- Zensar Technologies Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustained Adoption of Hybrid and Remote Work Models

- 4.2.2 Enterprise Shift to Employee Experience Platforms and DEX Analytics

- 4.2.3 Cloud Migration of Workplace Applications and End-User Computing

- 4.2.4 GDPR, Data Sovereignty, and Security By Design Requirements

- 4.2.5 EU AI Act and Governance-Ready Workplace Automation

- 4.2.6 Demand for Measurable Productivity, Sentiment, and Experience Telemetry

- 4.3 Market Restraints

- 4.3.1 Legacy Application Sprawl and Integration Complexity

- 4.3.2 Data Residency Constraints Across Cross-Border Workflows

- 4.3.3 High Total Cost of Transformation for Mid-Market Firms

- 4.3.4 User Fatigue From Tool Proliferation and Change Resistance

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-User Industries

- 5.5 By Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Nordics

- 5.5.8 Russia

- 5.5.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Atos SE

- 6.4.3 Capgemini SE

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Cognizant Technology Solutions Corporation

- 6.4.6 Computacenter plc

- 6.4.7 DXC Technology Company

- 6.4.8 Fujitsu Limited

- 6.4.9 Getronics Holding B.V.

- 6.4.10 HCL Technologies Limited

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 IBM Corporation

- 6.4.13 Infosys Limited

- 6.4.14 Kyndryl Holdings, Inc.

- 6.4.15 NTT DATA Group Corporation

- 6.4.16 SAP SE

- 6.4.17 ServiceNow, Inc.

- 6.4.18 SoftwareOne Holding AG

- 6.4.19 Tata Consultancy Services Limited

- 6.4.20 Telefonica, S.A.

- 6.4.21 Wipro Limited

- 6.4.22 Zensar Technologies Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)