|

市場調查報告書

商品編碼

2073262

數位化工作場所:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Digital Workplace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

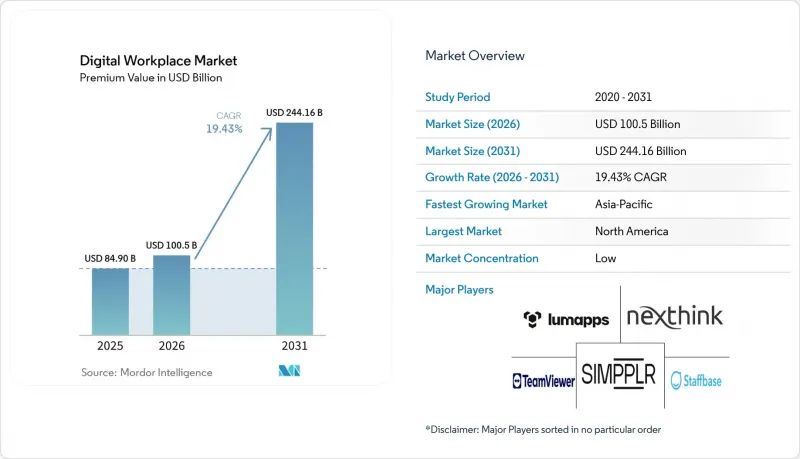

根據 Mordor Intelligence 預測,數位工作場所市場規模預計將在 2025 年達到 849 億美元,2026 年達到 1,005 億美元,到 2031 年達到 2,441.6 億美元,2026 年至 2031 年的複合年成長率為 19.43%。

本報告按組件(解決方案和服務)、部署模式(雲端、本地部署、混合部署)、組織規模(大型企業和中小企業)、最終用戶行業(IT和電信、銀行、金融服務和保險、醫療保健、製造業、零售業、政府和公共部門、教育等)以及地區進行細分。市場預測以美元計價。

全球數位化工作場所市場趨勢與洞察

人工智慧驅動的協作和工作流程自動化正在推動企業採用這些技術。

人工智慧驅動的協作正從有限的試點階段走向企業級廣泛應用,而這項轉變目前是數位化工作場所市場最強勁的需求推動要素。從2025年3月到2026年3月,Microsoft 365生態系統中活躍的人工智慧代理商數量年增了15倍,大型企業的成長更是高達18倍。這顯示人工智慧在現有工作場所平台中的應用正在迅速加深。微軟的研究也發現,在2026年2月記錄的超過10萬次Copilot對話中,有49%的對話輔助完成了分析、問題解決、評估和創造性思考等認知任務。這表明人工智慧的應用範圍正在擴展,不再局限於簡單的文檔撰寫,而是擴展到更多增值任務。這對數位化工作場所市場具有重大意義,因為買家越來越傾向於選擇從一開始就將人工智慧整合到協作、文件和工作流程環境中的平台。這一趨勢增加了轉換成本,也提高了將人機協作置於產品藍圖核心的供應商續約的可能性。此外,隨著數位化工作場所市場進入更成熟的採用階段,功能的深度變得比單純的產品廣度更重要。

基於代理的人工智慧和企業搜尋連接器的擴展正在重新定義工作場所架構。

基於代理的人工智慧正在拓展數位化工作場所市場的角色,使其不再只是生產力工具的集合,而是能夠跨企業系統進行推理、資訊搜尋和任務執行的智慧層。微軟於 2026 年 6 月正式發布了 Work IQ API,建立了一個共用智慧層,使代理程式能夠存取上下文資訊並在 Microsoft 365 資料和應用程式中運行。於 2026 年 1 月發布的 Nexthink Spark 對 IT 問題的首次回應解決率達到了 77%,並且能夠在兩分鐘內自主解決一級問題。這表明,基於代理的模型已經能夠處理數位化工作場所市場中相當一部分的服務活動。因此,企業搜尋不再只是資訊搜尋功能,而是正在成為任務、審核、支援和內容處理等執行流程中不可或缺的一部分。隨著這種模式的日益普及,缺乏強大的 ERP、HR、ITSM 和通訊工具連接器生態系統的供應商將越來越難以維持其核心地位。在預測期內,能夠建立自己的連接器和更強大的編配功能的供應商可能會在數位化工作場所市場中佔據更有利的地位。

資料隱私、網路安全和合規風險正在延長採購週期。

資料隱私和網路安全仍然是數位化工作場所市場中最持久的摩擦點。隨著人工智慧工具能夠存取訊息、文件、工作流程和員工記錄,這一趨勢尤其明顯。思科的《2026 年資料隱私基準調查》報告顯示,56% 的組織仍然沒有專門的人工智慧管治委員會,這凸顯了隨著工作場所工具日益自動化,管理方面存在明顯的差距。微軟的《2025 年數位防禦報告》也指出,人工智慧驅動的自動化網路釣魚和多階段攻擊鏈正在加劇遠端存取環境的壓力,導致分散式數位化工作場所部署相關的營運風險增加。這些問題在銀行、金融和保險 (BFSI) 以及醫療保健等高度監管的行業中尤為關鍵,因為在這些行業,買家通常要求供應商在簽訂合約前滿足 SOC 2 Type II、ISO 27001、FedRAMP 和 HIPAA 等相關控制要求。因此,進入數位化工作場所市場的供應商面臨銷售週期延長、文件要求更加嚴格以及成本增加等挑戰。此外,能夠展現出成熟的管治結構、審計能力和區域合規支援的供應商,將在採購過程中獲得先發優勢。

細分市場分析

預計到2025年,解決方案將佔總收入的63.89%,並在2031年之前以20.62%的複合年成長率成長。這表明解決方案在數位化工作場所市場中佔據更大的佔有率,並且其成長速度高於整體市場。這一趨勢表明,數位化工作場所市場的買家仍然傾向於軟體主導的現代化改造,而非僅提供服務。市場對能夠將協作、員工溝通、工作流程存取和終端控制整合到單一營運層的平台需求最高。在數位化工作場所市場,能夠將人工智慧功能直接整合到這些核心模組中,而不是將自動化作為單獨的附加元件銷售的供應商更受青睞。這一趨勢也增強了系統更新的經濟效益,因為一旦工作流程邏輯、權限和內容模型建置完成,替換系統將帶來更大的破壞性。

此外,數位化工作場所產業對能夠幫助企業適應向 Windows 10 過渡以及雲端管理終端興起的解決方案越來越感興趣。由於微軟將於 2026 年 4 月停止對 Windows 365 的 Windows 10 鏡像庫的支持,已經使用虛擬桌面環境 (VDI) 的企業很難推遲基於 Windows 11 的雲端 PC 部署計劃。這項變化正在推動數位化工作場所市場對 VDI、雲端 PC 管理和統一終端控制的需求。服務仍然至關重要,因為大型企業通常需要外部支援來配置、保護和管治跨多個工具的基於代理的工作流程。然而,數位化工作場所市場的核心價值在於能夠將協作、自動化和終端管理整合到單一產品環境中的供應商。

預計到2025年,雲端技術將佔據52.38%的市場佔有率,並在2031年之前以20.70%的複合年成長率持續成長,鞏固其在數位化工作場所市場的主導地位,並繼續作為主要交付模式。雲端技術之所以能夠推動數位化工作場所市場的發展,是因為它支援更快的資源配置、更頻繁的功能更新,以及更方便地在用戶群中部署人工智慧功能。此外,雲端技術還允許供應商以在分散的本地環境中難以實現的方式整合分析、管治和支援功能。因此,數位化工作場所市場的成長與工作負載的深度遷移以及現有合約中用戶數量的增加密切相關。隨著買家對其雲端套件進行標準化,這將加強與供應商的關係。

另一方面,數位化工作場所市場並未完全轉向統一的雲端模式。在資料儲存和管理要求仍然嚴格的國防、政府和部分金融服務領域,本地部署仍扮演著重要角色。對於那些需要在傳統ERP、文件或身分管理系統之上進行雲端協作的公司而言,混合架構仍然至關重要。如果供應商能夠透過單一控制平台管理這兩種系統,數位化工作場所市場將從中受益。微軟正在支援混合模式,而非單純的「純雲端」模式,其方法是將向Windows 11的過渡、Windows 365的推出以及裝置安全且更緊密地整合在一起。未來,數位化工作場所市場將更加重視那些能夠讓最終用戶和IT團隊在管理混合環境時感受到與管理雲端環境時一樣一致的供應商。

區域分析

2025年,北美繼續保持領先地位,佔據數位化工作場所市場佔有率的42.16%,這主要得益於供應商的高度集中、企業內部廣泛的雲端採用以及人工智慧賦能的生產力工具的快速部署。大部分支出來自美國,隨著Windows 10於2025年10月停止支持,引發了一系列設備升級、終端管理更新以及向雲端PC遷移的連鎖反應,這一趨勢將在2026年繼續影響採購趨勢。加拿大和墨西哥在專業服務和金融服務等領域不斷推動跨境平台標準化,進一步推動了區域需求。北美的數位化工作場所市場依然強勁,企業正積極將人工智慧功能、管治管理和員工體驗目標融入更廣泛的平台決策中。因此,該地區不僅在收入方面,而且在那些通常會影響整個數位化工作場所市場的產品的早期採用模式方面,都繼續保持著重要的地位。

預計到2031年,亞太地區將以23.18%的複合年成長率成長,使其成為預測期內對數位化工作場所市場貢獻最大的地區。這一成長主要得益於政府主導的數位化進程、中小企業的廣泛參與,以及已開發經濟體和新興經濟體對「雲端優先」工作場所架構的採用。印度憑藉其大規模的IT服務基礎設施和日益增強的本土企業環境,為市場做出了貢獻,這些企業環境正日益具備大規模部署雲端交付工作場所工具的能力。日本、韓國、澳洲和紐西蘭憑藉其企業高度成熟的數位化水平,為數位化工作場所市場提供了支持。東南亞雖然仍處於早期階段,但憑藉針對當地營運環境量身定做的行動優先SaaS模式,正在迅速發展。在整個全部區域,數位化工作場所市場受益於買家尋求更快的部署速度和更簡化的管理,而無需建立大規模的本地基礎設施。

由於強勁的需求,歐洲仍然是數位化工作場所市場的關鍵區域,但供應商的選擇越來越受到隱私、主權和合規性等因素的影響。德國就是一個鮮明的例子。根據德國資訊科技協會(Bitkom)的報告,預計到2026年,將有41%的德國公司積極使用人工智慧,高於2024年的17%,但77%的公司仍然認為資料保護要求是主要障礙。在南美洲,受巴西和阿根廷金融服務、零售和技術需求的推動,市場正在發展,但貨幣壓力和通訊基礎設施的差異可能會減緩部署速度。中東地區正受益於沙烏地阿拉伯和阿拉伯聯合大公國的大規模公共和企業數位化專案。另一方面,非洲仍處於起步階段,但南非、奈及利亞、肯亞和埃及等國在結構上與採用行動原生SaaS相契合。總的來說,這些地區表明,雖然對數位化工作場所市場的需求是全球性的,但仍存在一些區域性特徵,合規性、基礎設施和工作環境將影響採用速度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 混合辦公和分散式辦公室的普及和建立。

- 遷移到雲端和 SaaS 工作場所套件

- 增加數位化員工體驗的投資

- 人工智慧驅動的協作和工作流程自動化

- Windows 10 終端更新、Windows 11 部署以及遷移到雲端 PC。

- 對智慧體人工智慧和企業搜尋連接器的增強

- 市場限制因素

- 資料隱私、網路安全和合規風險

- 舊有應用程式和整合複雜性

- 工具的激增和數位摩擦

- 人工智慧管治與人才發展之間的差距。

- 產業價值鏈分析

- 監理情勢

- 資料保護與數位化工作場所管治

- 職場中有關人工智慧和員工監控的規定

- 技術展望

- GenAI 副駕駛和代理編配

- 整合端點管理與自癒式IT

- 雲端電腦、虛擬桌面基礎架構和設備即服務

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 整合通訊與協作

- 整合端點管理

- 企業移動性與管理

- 員工體驗平台與內網

- 工作流程自動化與知識管理

- 虛擬桌面基礎架構與雲端電腦

- 服務

- 解決方案

- 部署模式

- 雲

- 現場

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 衛生保健

- 製造業

- 零售

- 政府/公共部門

- 教育

- 能源公用事業

- 法律與專業服務

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 北歐的

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 東南亞

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Product Launches and Platform Upgrades

- Partnerships and Alliances

- 併購

- Geographic Expansion

- 市佔率分析

- 公司簡介

- TeamViewer SE

- Nexthink SA

- LumApps SAS

- Staffbase GmbH

- Simpplr Inc.

- Appspace Inc.

- Haiilo GmbH

- Powell Software SAS

- Igloo Software Inc.

- Interact Software Group Limited

- Claromentis Ltd.

- Axero Solutions LLC

- Invotra Limited

- Jostle Corporation

- Passageways, Inc.

- InvolveSoft, Inc.

- Robin Powered, Inc.

- eXo Platform SAS

- Liferay, Inc.

- Lakeside Software, LLC

- ControlUp Technologies Ltd.

- Flexxible Information Technology, SL

- Kissflow Inc.

- United Planet GmbH

- Workgrid Software LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the digital workplace market size is projected to be USD 84.90 billion in 2025, USD 100.50 billion in 2026, and reach USD 244.16 billion by 2031, growing at a CAGR of 19.43% from 2026 to 2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (IT and Telecom, BFSI, Healthcare, Manufacturing, Retail, Government and Public Sector, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Workplace Market Trends and Insights

AI-Powered Collaboration and Workflow Automation Drive Enterprise Adoption

AI-powered collaboration has moved from limited pilots to broad enterprise use, and that shift is now the strongest demand driver in the digital workplace market. Active AI agents in the Microsoft 365 ecosystem grew 15x year over year between March 2025 and March 2026, and the increase was 18x among large enterprises, indicating how quickly adoption is deepening within established workplace platforms. Microsoft also found that 49% of more than 100,000 Copilot conversations in February 2026 supported cognitive work such as analysis, problem-solving, evaluation, and creative thinking, suggesting that AI is being used for higher-value work rather than just simple drafting. This matters for the digital workplace market because buyers are increasingly choosing platforms that embed AI into collaboration, document, and workflow environments from the start. That preference raises switching costs and improves renewal potential for vendors whose road maps are centered on human-AI teamwork. It also makes feature depth more important than simple product breadth as the digital workplace market moves into a more mature adoption phase.

Agentic AI and Enterprise Search Connector Expansion Redefine Workplace Architecture

Agentic AI is widening the role of the digital workplace market from a set of productivity tools into a layer that can reason, retrieve information, and complete work across enterprise systems. Microsoft released Work IQ APIs into general availability in June 2026, creating a shared intelligence layer that lets agents access context and act across Microsoft 365 data and applications. Nexthink Spark, launched in January 2026, achieved a 77% first-contact resolution rate for IT issues and resolved Level 1 issues autonomously in under 2 minutes, demonstrating that agent-based models can already handle a meaningful share of service activity in the digital workplace market. The practical result is that enterprise search is no longer just a retrieval feature, because it is becoming part of the execution path for tasks, approvals, support, and content handling. Vendors that lack strong connector ecosystems for ERP, HR, ITSM, and communication tools will find it harder to remain central as this model spreads. Vendors that build proprietary connectors and stronger orchestration capabilities are likely to gain a more durable position in the digital workplace market over the forecast period.

Data Privacy, Cybersecurity, and Compliance Exposure Extend Procurement Cycles

Data privacy and cybersecurity remain the most persistent sources of friction in the digital workplace market, especially as AI tools gain access to messages, files, workflows, and employee records. Cisco reported in its 2026 Data Privacy Benchmark Study that 56% of organizations still lack a dedicated AI governance committee, which leaves a clear control gap as workplace tools become more autonomous. Microsoft also documented in its 2025 Digital Defense Report that AI-automated phishing and multi-stage attack chains are increasing pressure on remote-access environments, thereby raising the operating risk of distributed digital workplace deployments. These issues matter most in regulated fields such as BFSI and healthcare, where buyers often require SOC 2 Type II, ISO 27001, FedRAMP, and HIPAA-related controls before contract award. The result is longer sales cycles, greater documentation requirements, and higher costs for vendors serving the digital workplace market. It also gives providers that can demonstrate mature governance, audit readiness, and regional compliance support an early edge in the buying process.

Other drivers and restraints analyzed in the detailed report include:

- Rising Hybrid and Distributed Work Normalization Creates Platform Replacement Demand

- Cloud and SaaS Workplace Suite Migration Widens the Addressable Market

- Legacy Application and Integration Complexity Limits Deployment Velocity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for 63.89% of revenue in 2025 and are projected to grow at a 20.62% CAGR through 2031, indicating they held a larger share of the digital workplace market and are expanding faster than the overall market. This pattern shows that buyers in the digital workplace market still prefer software-led modernization over service-only engagements. Demand is strongest where platforms combine collaboration, employee communication, workflow access, and endpoint control into a single operating layer. The digital workplace market is rewarding vendors that can embed AI capabilities directly into these core modules rather than selling automation as a detached add-on. That preference also strengthens renewal economics, because once workflow logic, permissions, and content models are embedded, replacement becomes more disruptive.

The digital workplace industry is also seeing greater interest in solutions that help organizations navigate the Windows 10 transition and the rise of cloud-managed endpoints. Microsoft retired Windows 10 gallery images for Windows 365 in April 2026, making it harder for organizations already using virtual desktop environments to defer Windows 11-oriented cloud PC planning. That change supports demand for VDI, cloud PC management, and unified endpoint control inside the digital workplace market. Services still matter because large enterprises often need outside help to configure, secure, and govern agentic workflows that span several tools. Even so, the center of value in the digital workplace market remains with solution vendors that can pull collaboration, automation, and endpoint administration into a single product environment.

Cloud held 52.38% of deployments in 2025 and is projected to expand at a 20.70% CAGR through 2031, giving it the leading position in the digital workplace market and confirming that it remains the dominant delivery model. The cloud segment leads the digital workplace market because it supports faster provisioning, more frequent feature updates, and simpler distribution of AI capabilities across user groups. It also allows vendors to unify analytics, governance, and support functions in ways that are harder to replicate across disconnected local installations. As a result, growth in the digital workplace market is increasingly tied to deeper workload migration and wider seat expansion inside existing contracts. This makes vendor relationships more durable once a buyer has standardized on a cloud suite.

At the same time, the digital workplace market is not moving to a fully uniform cloud model. On-premises deployments still serve defense, government, and some financial services environments where residency and control requirements remain strict. Hybrid architectures continue to matter for enterprises that need cloud collaboration on top of legacy ERP, file, or identity systems, and the digital workplace market benefits when vendors can manage both sides through one control plane. Microsoft has linked Windows 11 migration, Windows 365 adoption, and device security more closely, supporting a blended approach rather than a simple cloud-only narrative. Over time, the digital workplace market is likely to reward providers that can make hybrid administration feel as consistent as cloud administration for end users and IT teams.

Complete Report Scope:

- By Component

- Solutions

- Unified Communication and Collaboration

- Unified Endpoint Management

- Enterprise Mobility and Management

- Employee Experience Platforms and Intranet

- Workflow Automation and Knowledge Management

- Virtual Desktop Infrastructure and Cloud PC

- Services

- Solutions

- By Deployment Mode

- Cloud

- On-premises

- Hybrid

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises

- By End-user Industry

- IT and Telecommunications

- BFSI

- Healthcare

- Manufacturing

- Retail

- Government and Public Sector

- Education

- Energy and Utilities

- Legal and Professional Services

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Nordics

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Israel

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Kenya

- Rest of Africa

- North America

Geography Analysis

North America held 42.16% of the digital workplace market share in 2025, maintaining its lead due to its dense vendor base, deep enterprise cloud adoption, and faster adoption of AI-enabled productivity tools. The United States drives most of that spending, and the October 2025 end of support for Windows 10 created a linked cycle of device refreshes, endpoint management renewals, and cloud PC migrations that continues to shape procurement in 2026. Canada and Mexico add to regional demand by standardizing cross-border platforms in sectors such as professional and financial services. The digital workplace market remains strongest in North America, where enterprises are willing to integrate AI features, governance controls, and employee experience goals into broader platform decisions. That keeps the region important not only for revenue, but also for early product adoption patterns that often influence the wider digital workplace market.

Asia-Pacific is projected to expand at a 23.18% CAGR through 2031, making it the fastest-growing regional contributor to the digital workplace market over the forecast period. Growth is supported by government-backed digitalization, broad SME participation, and the spread of cloud-first workplace architectures across both developed and emerging economies. India contributes through a large IT services base and a domestic enterprise environment that is increasingly able to absorb cloud-delivered workplace tools at scale. Japan, South Korea, Australia, and New Zealand support the digital workplace market through strong enterprise digital maturity, while Southeast Asia is earlier in adoption but moving quickly, with mobile-first SaaS models aligning with local operating conditions. Across the region, the digital workplace market benefits from buyers seeking faster deployment and simpler administration without building large local infrastructure stacks.

Europe remains a meaningful region for the digital workplace market because demand is strong, but vendor choice is shaped more heavily by privacy, sovereignty, and compliance concerns. Germany provides a clear example, as Bitkom reported that 41% of German companies actively use AI in 2026, up from 17% in 2024, while 77% still cite data protection requirements as a major hurdle. South America is developing through demand for financial services, retail, and technology in Brazil and Argentina, though currency pressure and connectivity gaps can slow the rollout pace. The Middle East is benefiting from large public and enterprise digital programs in Saudi Arabia and the UAE, while Africa is still early but structurally aligned with mobile-native SaaS adoption in countries such as South Africa, Nigeria, Kenya, and Egypt. Taken together, these regions show that the digital workplace market is global in demand, but still local in how compliance, infrastructure, and workforce conditions shape adoption speed.

- TeamViewer SE

- Nexthink SA

- LumApps SAS

- Staffbase GmbH

- Simpplr Inc.

- Appspace Inc.

- Haiilo GmbH

- Powell Software SAS

- Igloo Software Inc.

- Interact Software Group Limited

- Claromentis Ltd.

- Axero Solutions LLC

- Invotra Limited

- Jostle Corporation

- Passageways, Inc.

- InvolveSoft, Inc.

- Robin Powered, Inc.

- eXo Platform SAS

- Liferay, Inc.

- Lakeside Software, LLC

- ControlUp Technologies Ltd.

- Flexxible Information Technology, S.L.

- Kissflow Inc.

- United Planet GmbH

- Workgrid Software LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Hybrid and Distributed Work Normalization

- 4.3.2 Cloud and SaaS Workplace Suite Migration

- 4.3.3 Growing Investment in Digital Employee Experience

- 4.3.4 AI-Powered Collaboration and Workflow Automation

- 4.3.5 Windows 10 Endpoint Refresh, Windows 11 Adoption, and Cloud PC Migration

- 4.3.6 Agentic AI and Enterprise Search Connector Expansion

- 4.4 Market Restraints

- 4.4.1 Data Privacy, Cybersecurity, and Compliance Exposure

- 4.4.2 Legacy Application and Integration Complexity

- 4.4.3 Tool Sprawl and Digital Friction

- 4.4.4 AI Governance and Workforce Enablement Gaps

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.6.1 Data Protection and Digital Workplace Governance

- 4.6.2 Workplace AI and Employee Monitoring Rules

- 4.7 Technological Outlook

- 4.7.1 GenAI Copilots and Agent Orchestration

- 4.7.2 Unified Endpoint Management and Self-Healing IT

- 4.7.3 Cloud PC, VDI, and Device-as-a-Service

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Unified Communication and Collaboration

- 5.1.1.2 Unified Endpoint Management

- 5.1.1.3 Enterprise Mobility and Management

- 5.1.1.4 Employee Experience Platforms and Intranet

- 5.1.1.5 Workflow Automation and Knowledge Management

- 5.1.1.6 Virtual Desktop Infrastructure and Cloud PC

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Energy and Utilities

- 5.4.9 Legal and Professional Services

- 5.4.10 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Nordics

- 5.5.3.8 Russia

- 5.5.3.9 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Kenya

- 5.5.6.5 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.2.1 Product Launches and Platform Upgrades

- 6.2.2 Partnerships and Alliances

- 6.2.3 Mergers and Acquisitions

- 6.2.4 Geographic Expansion

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TeamViewer SE

- 6.4.2 Nexthink SA

- 6.4.3 LumApps SAS

- 6.4.4 Staffbase GmbH

- 6.4.5 Simpplr Inc.

- 6.4.6 Appspace Inc.

- 6.4.7 Haiilo GmbH

- 6.4.8 Powell Software SAS

- 6.4.9 Igloo Software Inc.

- 6.4.10 Interact Software Group Limited

- 6.4.11 Claromentis Ltd.

- 6.4.12 Axero Solutions LLC

- 6.4.13 Invotra Limited

- 6.4.14 Jostle Corporation

- 6.4.15 Passageways, Inc.

- 6.4.16 InvolveSoft, Inc.

- 6.4.17 Robin Powered, Inc.

- 6.4.18 eXo Platform SAS

- 6.4.19 Liferay, Inc.

- 6.4.20 Lakeside Software, LLC

- 6.4.21 ControlUp Technologies Ltd.

- 6.4.22 Flexxible Information Technology, S.L.

- 6.4.23 Kissflow Inc.

- 6.4.24 United Planet GmbH

- 6.4.25 Workgrid Software LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

亞太地區數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)南美洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)泰國數位化工作場所市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)能源和公共產業行業的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)中東和非洲的數位化工作場所:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)歐洲數位化工作場所:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)碳智慧型遠距辦公和數位化工作場所軟體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 2026年全球託管式數位化工作場所服務市場報告

2026年全球託管式數位化工作場所服務市場報告 數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)

數位化工作場所市場:2026-2032年全球市場預測(按服務類型、應用、產業、組織規模和部署類型分類)