|

市場調查報告書

商品編碼

2072684

東南亞LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)Southeast Asia LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

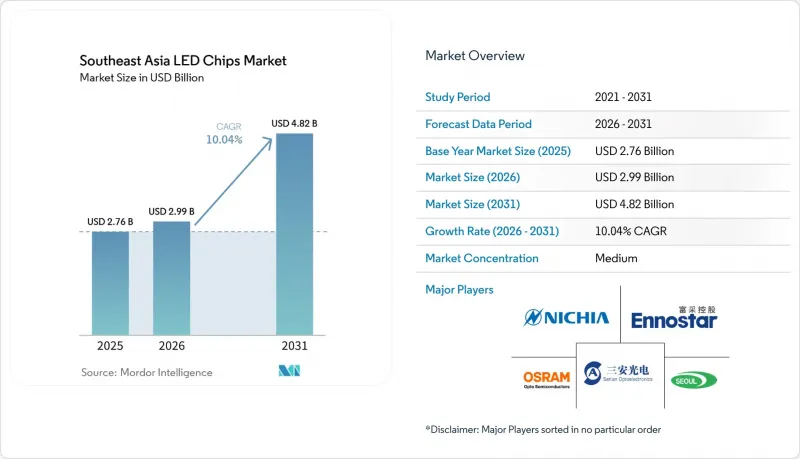

據 Mordor Intelligence 稱,東南亞 LED 晶片市場在 2025 年的價值為 27.6 億美元,預計到 2031 年將達到 48.2 億美元,而 2026 年為 29.9 億美元,2026 年至 2031 年預測期內的複合成長率為 10.04%。

本報告按LED晶片技術(傳統LED、Mini-LED、Micro-LED)、半導體材料(GaN/InGaN、AlGaInP及其他半導體材料)、應用領域(通用照明、汽車照明、背光/顯示器、家用電子電器、工業/特殊照明)和國家進行細分。市場預測以以金額為準(百萬美元)為單位。

東南亞LED晶片市場趨勢與洞察

擴大政府對節能照明的獎勵

政策支持的能源效率提升措施仍是東南亞LED晶片市場短期需求成長的最顯著推動要素。新加坡的「能源效率津貼計畫」(Energy Efficiency Grant )已從2026年4月延長至2027年3月,隨後擴展至所有行業,直至2028年3月,該計劃為投資於預先批准的LED照明設備的中小企業提供高達70%的補貼。該計劃意義重大,因為它不僅降低了採購成本,還為符合條件的照明系統設定了更高的技術標準,從而增加了對高性能晶片的需求。在區域層面,東協能源中心正在推動採用統一的最低能源效率標準(MEPS),即每瓦80流明,用於非定向LED燈,促使成員國朝著更一致的能源效率標準邁進。隨著這些法規得到更嚴格的執行,更換週期正從簡單地更換燈泡轉向升級到採用更優晶片配置的高效系統。這一趨勢將為東南亞LED晶片市場提供更永續的銷售量基礎。這是因為與消費者在電子設備上的隨意支出相比,政策驅動的需求較少依賴短期消費週期。

汽車中LED大燈的普及應用日益廣泛

在東南亞LED晶片市場,汽車產業正成為規格主導需求最強勁的領域。在預測期內,該領域已成為成長最快的應用領域,其成長動力不僅源自於LED的替代,更源自於向自我調整和像素化照明系統的轉變,這些系統需要更高密度和更精確的晶片陣列。根據ams OSRAM最新發布的2026年產品和策略更新,汽車照明平台被定位為公司轉型為數位光電過程中的核心成長領域,尤其是在像素化照明和智慧照明架構領域。該公司於2026年3月推出的基於EVIYOS平台的超高效微型LED陣列,也體現了此設計路徑的成熟,顯示車規級晶片的研發正在向其他高價值應用領域延伸。隨著汽車製造商將更先進的頭燈功能引入主流平台,市場需求正轉向那些具備熱穩定性、光束精度和更長認證週期的晶片。這種轉變提高了進入門檻,使得汽車產業在東南亞 LED 晶片市場中比標準照明產業擁有更大的利潤來源。

對外延晶片製造的高額資本投入

資本密集度仍是東南亞LED晶片市場在地供應進一步擴張的主要障礙。根據Mordor Intelligence對亞太地區LED外延設備的調查,一套先進的200mm批量MOCVD系統仍需數百萬美元的投資,其中包括測量、廢氣處理和晶圓處理等費用。這項成本負擔對新參與企業東協市場的企業構成重大障礙,因為該地區的需求前景不如台灣、韓國和中國那麼明朗。即使有獎勵計劃可以抵消部分初始成本,晶圓廠仍需要承擔較長的折舊免稅額週期、服務合約和耗材費用。因此,待開發區的投資正在放緩,外延產能仍集中在擁有充足資金和強大客戶關係的成熟企業手中。這也意味著,儘管東南亞LED晶片市場的組裝、封裝和下游設計領域預計將實現強勁成長,但上游晶圓製造領域的成長速度預計不會與之持平。因此,供應鏈不斷改善,但核心晶片製造能力仍然嚴重依賴特定地區少數幾家大型公司。

細分市場分析

預計到2025年,傳統LED將佔東南亞LED晶片市場82.34%的銷售額,持續維持其在東南亞LED晶片市場的穩固中心地位。這一地位反映了商業和住宅照明市場的強勁需求,在這些市場中,成熟的磷光體轉換平台在大規模更換專案中仍能提供成本、可靠性和發光效率的最佳平衡。此外,東協地區能源效率標準的日益嚴格也促進了這一細分市場的發展,因為升級改造通常從已滿足採購和合規要求的成熟產品開始。實際上,儘管東南亞LED晶片市場的技術格局不斷變化,但這仍然確保了傳統產品的銷售上限。

在東南亞,Mini-LED 對 LED 晶片產業的轉型具有重要的戰略意義。由於其與成熟的氮化鎵 (GaN) 供應鏈距離較近,可以利用現有的製造技術實現規模化生產,同時也能進軍利潤更高的應用領域,例如顯示器背光和高階照明系統。 Micro-LED 是成長最快的技術細分市場,預計到 2031 年的複合年成長率 (CAGR) 將達到 12.04%,這表明東南亞 LED 晶片市場已經超越了傳統照明領域。最強勁的需求來自於那些優先考慮像素控制、亮度密度和緊湊型光學設計的應用,尤其是在汽車和先進顯示器應用領域。根據 ams OSRAM 的企業藍圖,最初為智慧汽車照明開發的 Micro-LED 平台,如今正擴展到相關的光電應用領域,從而支援東南亞 LED 晶片市場更廣泛的轉型發展軌跡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大政府對節能照明的獎勵

- 智慧家庭和物聯網照明的廣泛應用。

- 加速東協各國首都的城市基礎建設項目建設

- 汽車LED大燈的廣泛應用

- Mini-LED背光供應鏈本地化

- 新加坡和馬來西亞微型LED試點生產的興起

- 市場限制因素

- 外延晶片製造需要大量資金投入。

- 鎵、銦等主要原物料價格波動

- 熟練光電子工程師的供需失衡

- 與污水和化學品處置相關的環境合規成本

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- LED晶片技術

- 傳統LED

- Mini-LED

- Micro-LED

- 透過半導體材料

- GaN/InGaN

- AlGaInP

- 其他半導體材料

- 透過使用

- 一般照明

- 車

- 背光/顯示器

- 家用電子產品

- 工業/特殊照明

- 國家

- 印尼

- 馬來西亞

- 菲律賓

- 新加坡

- 泰國

- 越南

- 東南亞其他地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Epistar Corporation

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- HC SemiTek Corporation

- Everlight Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lumileds Holding BV

- Bridgelux, Inc.

- Kingbright Electronic Co., Ltd.

- Opto Tech Corporation

- Lextar Electronics Corporation

- Dominant Opto Technologies Sdn. Bhd.

- NationStar Optoelectronics Co., Ltd.

- AIXTRON SE

- Coherent Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the southeast asia LED chips market size was valued at USD 2.76 billion in 2025 and is estimated to grow from USD 2.99 billion in 2026 to reach USD 4.82 billion by 2031, at a CAGR of 10.04% during the forecast period 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN / InGaN, Algainp, and Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting / Displays, Consumer Electronics, and Industrial / Specialty Lighting), and Country. The Market Forecasts are Provided in Terms of Value (USD Million).

Southeast Asia LED Chips Market Trends and Insights

Expanding Government Incentives for Energy-Efficient Lighting

Policy-backed efficiency upgrades remain the clearest near-term demand driver for the Southeast Asia LED chips market. Singapore's Energy Efficiency Grant was extended from April 2026 to March 2027 and then expanded to all sectors through March 2028, with support of up to 70% for SMEs that invest in pre-approved LED lighting equipment.That program matters not only because it lowers purchase cost, but also because it sets a higher technology floor for qualifying lighting systems, which lifts demand for better-performing chips. At the regional level, the ASEAN Center for Energy has been pushing harmonized MEPS for non-directional LED lamps at 80 lumens per watt, which is helping member states move toward a more consistent efficiency baseline.As those rules are enforced more consistently, replacement cycles are shifting from simple lamp swaps toward higher-efficacy systems with a better chip mix. That dynamic gives the Southeast Asia LED chips market a more durable volume base because policy demand is less dependent on short consumer cycles than discretionary electronics spending.

Growth in Automotive LED Headlamp Adoption

Automotive is becoming the most specification-driven demand center in the Southeast Asia LED chips market. The segment is already the fastest-growing application in the forecast period, and the reason is not just LED replacement, but the move toward adaptive and pixelated lighting systems that require denser and more precise chip arrays. ams OSRAM's 2026 product and strategy updates show that automotive lighting platforms are now being treated as a core growth area within its digital photonics transition, especially in pixelated and intelligent lighting architectures. The company's March 2026 launch of an ultra-efficient micro-LED array built on its EVIYOS platform also shows how automotive-grade chip development is spilling into adjacent high-value uses, which confirms the maturity of this design path. As vehicle makers push more advanced headlamp functions into mainstream platforms, demand is shifting toward chips that support thermal stability, beam precision, and long qualification cycles. That change raises entry barriers and gives the Southeast Asia LED chips market a stronger profit pool in automotive than in standard illumination.

High Capital Expenditure for Epitaxial Wafer Fabrication

Capital intensity remains a major barrier to deeper local supply expansion in the Southeast Asia LED chips market. Mordor Intelligence's coverage of Asia-Pacific LED epitaxy equipment shows that advanced 200 mm batch MOCVD tools still require multi-million-dollar investment per unit when metrology, abatement, and wafer handling are included. That cost burden is difficult for new entrants in ASEAN markets because demand visibility is not yet as deep as it is in Taiwan, South Korea, or China. Even when incentive programs offset part of the upfront cost, fabs still need to absorb long depreciation cycles, service contracts, and consumable expenses. This slows greenfield investment and keeps epitaxial capacity concentrated among well-funded incumbents with established customer relationships. It also means the Southeast Asia LED chips market can grow strongly in assembly, packaging, and downstream design without seeing the same pace of expansion in upstream wafer fabrication. The result is a supply chain that keeps improving, but still depends heavily on a limited group of regional leaders for core chip-making capacity.

Other drivers and restraints analyzed in the detailed report include:

- Rising Penetration of Smart Homes and IoT-Enabled Lighting

- Accelerating Urban Infrastructure Projects Across ASEAN Capitals

- Price Volatility in Key Raw Materials Such as Gallium and Indium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs accounted for 82.34% of revenue in 2025, which kept them firmly at the center of the Southeast Asia LED chips market. That position reflected the strength of commercial and residential lighting demand, where mature phosphor-converted platforms still offer the best mix of cost, reliability, and efficacy for large replacement programs. The segment also benefited from stricter efficiency enforcement across ASEAN, because upgrades often began with established products that already met procurement and compliance requirements. In practical terms, that gave conventional products a strong volume floor even as the technology mix in the Southeast Asia LED chips market continued to shift.

Mini-LED occupies a transitional role that is strategically important for the Southeast Asia LED chips industry. It sits close enough to established GaN supply chains to scale through existing manufacturing know-how, but it also opens access to better-margin uses in display backlighting and premium lighting systems. Micro-LED is the fastest-growing technology sub-segment, with a 12.04% CAGR through 2031, which shows that the Southeast Asia LED chips market is already moving beyond the limits of conventional illumination. The strongest pull is coming from applications that value pixel control, brightness density, and compact optical design, especially in automotive and advanced display use cases. Company roadmaps from ams OSRAM show that micro-LED platforms first developed for intelligent automotive lighting are now being carried into adjacent photonics uses, which supports the wider migration path described in the Southeast Asia LED chips market.

Complete Report Scope:

- By LED Chip Technology

- Conventional LEDs

- Mini-LED

- Micro-LED

- By Semiconductor Material

- GaN / InGaN

- AlGAInP

- Other Semiconductor Materials

- By Application

- General Lighting

- Automotive

- Backlighting / Displays

- Consumer Electronics

- Industrial / Specialty Lighting

- By Country

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of Southeast Asia

List of Companies Covered in this Report:

- Nichia Corporation

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Epistar Corporation

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- HC SemITek Corporation

- Everlight Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lumileds Holding B.V.

- Bridgelux, Inc.

- Kingbright Electronic Co., Ltd.

- Opto Tech Corporation

- Lextar Electronics Corporation

- Dominant Opto Technologies Sdn. Bhd.

- NationStar Optoelectronics Co., Ltd.

- AIXTRON SE

- Coherent Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Government Incentives for Energy-Efficient Lighting

- 4.2.2 Rising Penetration of Smart Homes and IoT-Enabled Lighting

- 4.2.3 Accelerating Urban Infrastructure Projects Across ASEAN Capitals

- 4.2.4 Growth in Automotive LED Headlamp Adoption

- 4.2.5 Localization of Mini-LED Backlight Supply Chains

- 4.2.6 Emerging Micro-LED Pilot Production in Singapore and Malaysia

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for Epitaxial Wafer Fabrication

- 4.3.2 Price Volatility in Key Raw Materials such as Gallium and Indium

- 4.3.3 Supply-Demand Imbalance for Trained Optoelectronics Workforce

- 4.3.4 Environmental Compliance Costs for Wastewater and Chemical Disposal

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Country

- 5.4.1 Indonesia

- 5.4.2 Malaysia

- 5.4.3 Philippines

- 5.4.4 Singapore

- 5.4.5 Thailand

- 5.4.6 Vietnam

- 5.4.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Osram Opto Semiconductors GmbH

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Epistar Corporation

- 6.4.5 Cree LED, Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 San'an Optoelectronics Co., Ltd.

- 6.4.9 HC SemiTek Corporation

- 6.4.10 Everlight Electronics Co., Ltd.

- 6.4.11 Toyoda Gosei Co., Ltd.

- 6.4.12 Lumileds Holding B.V.

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Kingbright Electronic Co., Ltd.

- 6.4.15 Opto Tech Corporation

- 6.4.16 Lextar Electronics Corporation

- 6.4.17 Dominant Opto Technologies Sdn. Bhd.

- 6.4.18 NationStar Optoelectronics Co., Ltd.

- 6.4.19 AIXTRON SE

- 6.4.20 Coherent Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類

LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類