|

市場調查報告書

商品編碼

2066499

LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

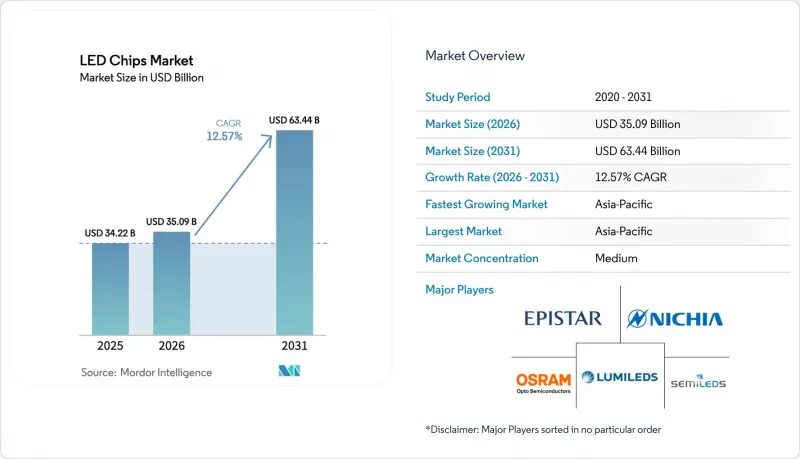

根據 Mordor Intelligence 預測,LED 晶片市場規模將從 2025 年的 334.7 億美元和 2026 年的 361.5 億美元成長到 2031 年的 565.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 9.38%。

本報告按LED晶片技術(傳統LED、Mini-LED等)、半導體材料(GaN/InGaN、AlGaInP等)、應用領域(通用照明、汽車、背光/顯示器、家用電子電器等)和地區(北美、歐洲、亞太、南美等)進行細分。市場預測以美元(USD)為單位。

全球LED晶片市場趨勢與洞察

顯示器OEM廠商向Mini-LED背光過渡

2025年至2026年間,Mini-LED背光技術從高階電視和顯示器的利基市場走向主流。這使得LCD面板在對比度和峰值亮度方面能夠達到與OLED媲美的性能,同時在大螢幕應用中保持成本優勢。 TCL在2026年CES展會上發布的第二代「超量子點Mini-LED」面板,採用了數千顆經過精確篩選的晶片,亮度接近HDR1000水平,迫使競爭對手在性能上迎頭趕上,否則將面臨市場佔有率流失的風險。三星、LG Display和京東方等廠商擴大了面板產能,採用了晶片級封裝技術,每次封裝可封裝多達1000顆晶片。這縮短了組裝時間,並提高了良率。目前,每塊高階面板消耗的晶片數量遠超同系列側入式面板,因此,即使通用產品的平均售價(ASP)下降,滿足嚴格電流密度和散熱要求的供應商仍能維持價格。

中型車輛廣泛採用LED頭燈

2025年,歐洲自我調整光束法規與中國消費者對高階設計的需求融合,推動了LED照明技術從豪華車領域迅速擴展到大眾市場。日亞化學和英飛凌的雙LED投影模組將遠近光功能整合於單一緊湊組件中,在保持車規級可靠性的同時,將成本降低到中階車型也能採用的水平。小糸東和法雷奧等主要燈具製造商也拓展了其專門針對電動車(EV)的產品線,電動車依靠節能照明來延長續航里程,即使晶片尺寸不斷縮小,市場對節能照明的需求依然強勁。

亞洲地區由於供應過剩,平均售價(ASP)持續下降。

2025年至2026年間,中國大陸和台灣晶圓產能擴張速度再次超過市場需求成長,導致通用晶片價格下跌,並給運作老舊MOCVD生產線的二線廠商帶來壓力。 2025年初,由於住宅照明需求疲軟以及台灣廠商採取激進的定價策略,廠商試圖提價的努力失敗,市場壓力進一步加大。一些晶圓廠陷入損益平衡點以下,加速了產業重組,例如三安光電收購Lumileds以及Inari Amertron收購Lumileds。供應過剩導致LED晶片市場兩極化:通用照明領域價格競爭激烈,而汽車、顯示器和專業細分市場則保持著較高的利潤率,因為性能而非每流明價格成為選擇供應商的決定性因素。

細分市場分析

至2025年,傳統LED仍將佔據LED晶片市場83.40%的佔有率。這是因為在照明和標誌等大規模生產領域,成熟的供應鏈和久經考驗的可靠性仍然勝過新型架構的效能優勢。從2025年到2026年,高階電視和顯示器中Mini-LED的日益普及意味著,儘管每塊面板的晶片數量增加了一個數量級,晶片尺寸也縮小了,但供應商仍能免受平均售價(ASP)壓力的影響。

預計年複合成長率將達到11.23%的MicroLED晶片,在2026年國際消費電子展(CES)上,已從原型階段過渡到用於擴增實境(AR)眼鏡的商用參考模組。 JBD的「Hummingbird II Polychrome」投影機在展會上榮獲創新獎。儘管目前MicroLED晶片的良率仍維持在70-85%左右,但近期與多晶片排列和人工智慧缺陷檢測相關的專利正在縮小其與Mini-LED的成本差距。隨著製程的日趨成熟,MicroLED可望進軍高亮度市場。

區域分析

預計到2025年,亞太地區將以62.46%的市佔率主導LED晶片市場。這主要得益於中國大陸、台灣、韓國和日本等地外延晶圓產能的集中,以及諸如印度「UJALA」計畫等大規模需求創造計畫。該項目截至2025年1月已分發了3.687億個燈泡。三安光電在廈門營運著全球最大的MOCVD設備叢集之一,在通用型燈具晶片領域佔據價格優勢。同時,台灣晶元光電專注於為汽車和高階顯示器提供高性能晶片。韓國三星LED和LG Innotek則透過其面板業務創造價值,這兩家公司供應mini-LED和micro-LED背光,為區域生態系統提供從藍寶石晶棒錠切割到成品模組出口的全方位支援。東南亞正崛起為第二個製造地,首爾半導體與越南OMINSU公司計畫於2025年進行的技術轉移合作便是例證。這將鞏固越南作為西方品牌「中國+1」籌資策略供應商的地位。此外,該地區預計到2031年將以11.97%的複合年成長率成長,這得益於不斷加快的都市化以及政府持續採購智慧城市路燈。

即使北美和歐洲市場加起來,它們在LED晶片市場中所佔佔有率也遠小於其他地區。但隨著針對藍光危害、循環經濟設計和在地採購的監管日益嚴格,市場對高階LED晶片的需求正穩定成長。由於美國可能對中國產LED元件徵收高達145%的關稅,像Fusion Optix這樣的公司已經開始將產能整合到位於佛蒙特州的LEDdynamics公司,以避免進口成本。歐盟的生態設計指令以及強制性的EPREL註冊,正在推動照明設備向更高效、壽命數據更可靠的晶片轉型,這使得能夠提供嚴格光生物學測試結果的供應商更具優勢。同時,採用自我調整遠光燈的豪華汽車項目正在擴大奧地利、德國和荷蘭生產的高可靠性晶片的市場。這些結構性因素表明,區域買家將繼續專注於差異化裝置而非通用裝置,即使在持續的全球價格壓力下,預計銷售額仍將保持中等個位數的成長。

儘管南美、中東和非洲的LED安裝量仍然較小,但市政當局對路燈的更新換代以及電網覆蓋範圍的擴大,正在為LED晶片創造極具吸引力的新興市場。在巴西,政府對LED照明燈具的競標規定了國內採購比例的標準,這使得需求集中在能夠以優惠條件從亞太地區採購晶片的區域封裝製造商身上。同時,海灣合作理事會(GCC)成員國正在資助建設示範性智慧城市走廊,這些走廊指定使用可調光白光和連網燈具。非洲各國政府正在試行以UJALA為藍本的大宗採購項目,但由於規模有限,其單價高於印度和中國。供應商面臨各種各樣的安全標準和標籤法規,從新加坡的「強制性能源標籤計畫」到南非的NRCS電氣認證,這不僅使物流變得複雜,也有助於遏制低品質產品的傾銷。隨著政策日益協調一致,電力普及率不斷提高,預計未來十年這些地區在全球 LED 晶片市場中的總合將持續成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 主要經濟體的能源效率法規

- 顯示器OEM廠商向Mini-LED背光技術的轉型

- 中型車輛中LED頭燈的普及率不斷提高

- 將智慧照明與物聯網平台整合

- 採用晶片上量子點架構實現更廣色域

- 採用氮化鎵/鑽石基板降低熱阻

- 市場限制因素

- 由於亞洲地區供應過剩,平均售價(ASP)持續下降

- 微型LED的大規模生產需要大量資金投入。

- 鎵和稀土元素供應鏈的脆弱性

- 歐洲對藍光危害有嚴格的規定

- 產業供應鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- LED晶片技術

- 傳統LED

- Mini-LED

- Micro-LED

- 透過半導體材料

- GaN/InGaN

- AlGaInP

- 其他半導體材料

- 透過使用

- 一般照明

- 車

- 背光/顯示器

- 家用電子產品

- 工業/特殊照明

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.(Samsung LED)

- ams-OSRAM AG

- Cree LED, an SGH Company

- Lumileds Holding BV

- LG Innotek Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Epistar Corporation

- San'an Optoelectronics Co., Ltd.

- HC SemiTek Corporation

- Bridgelux, Inc.

- Ennostar Inc.

- Toyoda Gosei Co., Ltd.

- Rohm Co., Ltd.

- Genesis Photonics Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the lED chips market size is projected to expand from USD 33.47 billion in 2025 and USD 36.15 billion in 2026 to USD 56.59 billion by 2031, registering a CAGR of 9.38% between 2026 to 2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and More), Semiconductor Material (GaN/InGaN, Algainp, and More), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and More), and Geography (North America, Europe, Asia Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global LED Chips Market Trends and Insights

Display OEM Shift to Mini-LED Backlighting

Mini-LED backlighting moved from a niche to the mainstream in premium televisions and monitors during 2025-2026, allowing LCD panels to rival OLEDs on contrast ratio and peak brightness while retaining cost advantages in large formats. TCL's second-generation Super Quantum Dot Mini-LED sets launched at CES 2026 embedded thousands of tightly binned chips, pushing luminance near HDR1000 levels and forcing rivals to catch up on performance or risk share loss. Samsung, LG Display, and BOE expanded panel capacity and adopted chip-scale packaging, which places up to 1,000 dies per pulse, trimming assembly time and improving yields. Because each premium panel now consumes far more chips than an edge-lit equivalent, suppliers that meet stringent current-density and thermal demands defend pricing even as commodity ASPs slide.

Rising Adoption of LED Headlamps in Mid-Segment Vehicles

LED penetration leaped from luxury to volume car segments once European adaptive-beam regulations converged with Chinese consumer demand for premium aesthetics in 2025. Nichia and Infineon's bi-LED projector module combines high- and low-beam functions into a single compact assembly, reducing costs enough for mid-segment models while ensuring automotive-grade reliability. Major lamp makers such as Koito and Valeo expanded lines dedicated to electric vehicles that rely on energy-saving lighting to extend driving range, lifting chip demand despite unit size reductions.

Persistent ASP Erosion Due To Asian Overcapacity

Chinese and Taiwanese wafer expansions once again outran demand growth in 2025-2026, dragging commodity chip prices lower and squeezing second-tier producers operating aging MOCVD lines. Attempts to raise prices in early 2025 fizzled as soft residential lighting demand and aggressive Taiwanese offers undercut the market. Marginal fabs fell below cash costs, prompting consolidation moves such as San'an Optoelectronics' acquisition of Lumileds and Inari Amertron's acquisition of Lumileds. The oversupply reinforces a bifurcated LED chips market, with cut-throat pricing in general lighting but firmer margins in automotive, display, and specialty niches where performance, not lumen cost, dictates vendor selection.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates in Major Economies

- Quantum-Dot On-Chip Architectures Enabling Wider Color Gamut

- High Capital Expenditure for Micro-LED Mass Transfer

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs maintained an 83.40% market share of LED chips in 2025 because entrenched supply chains and proven reliability still outweigh the performance advantages of newer architectures in high-volume lighting and signage. Mini-LED adoption in premium televisions and monitors during 2025-2026 pushed chip counts per panel up by an order of magnitude, cushioning suppliers against ASP pressure even as die size shrank.

Micro-LED chips, forecast to expand at an 11.23% CAGR, moved from prototyping into commercial reference modules for augmented-reality glasses at CES 2026, where JBD's Hummingbird II Polychrome projector earned an Innovation Award. Despite mass-transfer yields hovering at 70-85%, recent patents covering multi-chip placement and AI-based defect detection are narrowing the cost gap with mini-LED, positioning micro-LED to penetrate high-luminance niches as processes mature.

Geography Analysis

Asia Pacific dominated the LED chips market with a 62.46% share in 2025, supported by concentrated epitaxial wafer capacity across China, Taiwan, South Korea, and Japan, and by large-scale demand programs such as India's UJALA scheme, which had distributed 368.7 million bulbs by January 2025. San'an Optoelectronics operates one of the world's largest clusters of MOCVD tools in Xiamen, enabling price leadership on commodity lamp dies, while Epistar in Taiwan has focused on high-performance chips for automotive and premium displays. South Korea's Samsung LED and LG Innotek capture value from internal panel divisions that specify mini-LED and micro-LED backlighting, anchoring a regional ecosystem that stretches from sapphire ingot slicing to complete module export. Southeast Asia is emerging as a secondary manufacturing hub, illustrated by Seoul Semiconductor's 2025 technology-transfer alliance with OMINSU Vietnam, which positions Vietnam as a supplier to brands in Europe and North America seeking China-plus-one sourcing. The region's forecast CAGR of 11.97% through 2031 is also underpinned by rising urbanization and sustained government procurement of smart-city street lighting.

North America and Europe together account for a much smaller portion of the LED chips market, but deliver steady premium demand as regulations tighten on blue-light hazard, circular-economy design, and local content. Potential United States tariffs of up to 145% on Chinese LED components have already pushed companies such as Fusion Optix to consolidate Vermont-based LEDdynamics capacity as a hedge against import costs. The European Union's Ecodesign directive, coupled with mandatory EPREL registration, is steering luminaires toward higher-efficacy chips and documented lifetime data, rewarding suppliers that can demonstrate rigorous photobiological testing. At the same time, premium automotive programs adopting adaptive-beam headlamps provide a growing market for high-reliability dies manufactured in Austria, Germany, and the Netherlands. These structural factors are expected to keep regional buyers focused on differentiated rather than commodity devices, anchoring mid-single-digit revenue growth even as global price pressure persists.

South America, the Middle East, and Africa have smaller installed bases, yet municipal street-lighting retrofits and expanding grid access create an attractive frontier for the LED chip market. Brazilian state tenders for LED luminaires require domestic-content thresholds that channel demand toward regional packagers able to source dies from Asia Pacific on favorable terms, while Gulf Cooperation Council nations fund showcase smart-city corridors that specify tunable-white and connected lamps. African governments are piloting bulk-procurement programs modeled on UJALA, though the limited scale keeps unit prices higher than in India or China. Vendors face fragmented safety and labeling rules ranging from Singapore's Mandatory Energy Labeling Scheme to South Africa's NRCS electrical approvals that complicate logistics but also deter the dumping of low-quality product. As policy harmonization improves and electricity access expands, these regions are projected to increase their combined share of the global LED chip market over the next decade.

- Nichia Corporation

- Samsung Electronics Co., Ltd. (Samsung LED)

- ams-OSRAM AG

- Cree LED, an SGH Company

- Lumileds Holding B.V.

- LG Innotek Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Epistar Corporation

- San'an Optoelectronics Co., Ltd.

- HC SemiTek Corporation

- Bridgelux, Inc.

- Ennostar Inc.

- Toyoda Gosei Co., Ltd.

- Rohm Co., Ltd.

- Genesis Photonics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-Efficiency Mandates in Major Economies

- 4.2.2 Display OEM Shift to Mini-LED Backlighting

- 4.2.3 Rising Adoption of LED Headlamps in Mid-Segment Vehicles

- 4.2.4 Smart Lighting Integration With IoT Platforms

- 4.2.5 Quantum-Dot On-Chip Architectures Enabling Wider Color Gamut

- 4.2.6 GaN-on-Diamond Substrates Reducing Thermal Resistance

- 4.3 Market Restraints

- 4.3.1 Persistent ASP Erosion Due to Asian Overcapacity

- 4.3.2 High Capital Expenditure for Micro-LED Mass Transfer

- 4.3.3 Gallium and Rare-Earth Supply Chain Vulnerabilities

- 4.3.4 Stringent Blue-Light Hazard Regulations in Europe

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Samsung LED)

- 6.4.3 ams-OSRAM AG

- 6.4.4 Cree LED, an SGH Company

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 Epistar Corporation

- 6.4.9 San'an Optoelectronics Co., Ltd.

- 6.4.10 HC SemiTek Corporation

- 6.4.11 Bridgelux, Inc.

- 6.4.12 Ennostar Inc.

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 Rohm Co., Ltd.

- 6.4.15 Genesis Photonics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類

LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類 LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年

LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年