|

市場調查報告書

商品編碼

2063853

亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia Pacific LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

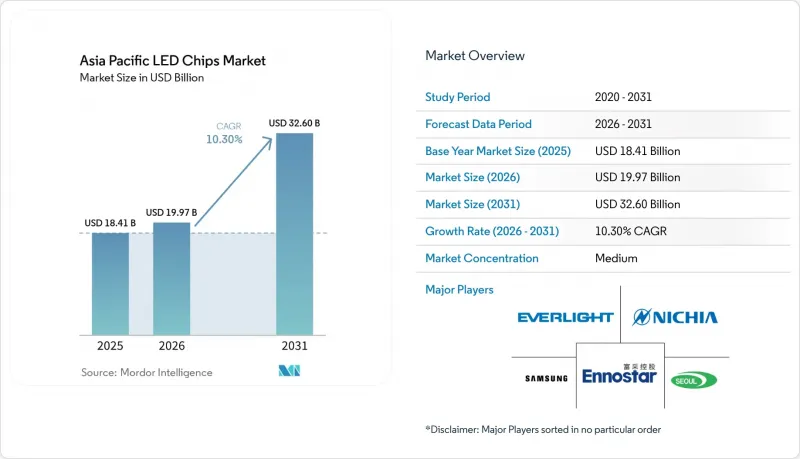

根據 Mordor Intelligence 預測,亞太地區 LED 晶片市場規模預計將從 2025 年的 184.1 億美元成長到 2026 年的 199.7 億美元,然後在 2031 年達到 326 億美元,2026 年至 2031 年的複合年成長率為 10.3%。

本報告按LED晶片技術(傳統LED、Mini-LED、Micro-LED)、半導體材料(GaN/InGaN、AlGaInP及其他半導體材料)、應用領域(通用照明、汽車及其他)和地區(中國、日本、印度、韓國、東南亞及其他亞太地區)進行細分。市場預測以美元計價。

亞太地區LED晶片市場趨勢及洞察。

政府主導的「印度製造」LED晶片製造獎勵措施

印度的生產連結獎勵計畫計畫對經認證的LED組件增量銷售額提供4-6%的獎勵,旨在鼓勵現有工廠擴建和新建晶圓廠,從而將國內增值率從不足20%大幅提升至80%。獲批的申請者已承諾投資超過10億美元,這將為全球晶片製造商實現採購多元化、降低對單一國家的依賴鋪平道路。成功的關鍵在於同時投資於氮化鎵(GaN)外延設備、熟練人才和配套基礎設施,這些領域目前正日益成為政策優先考慮的重點。

東南亞摩托車的電動化

在越南、泰國和印度尼西亞,電動滑板車和電動機車已成為城市交通的主要方式,這導致對節能型LED大燈、尾燈和儀錶群的需求激增。雖然自我調整光束和日間行車燈的普及增加了每輛車所需的晶片數量,但熱帶氣候對散熱性能提出了更高的要求。汽車製造商傾向於採用模組化LED組件,以降低組裝複雜性和保固成本,這為擁有強大散熱設計能力的晶片供應商創造了巨大的利潤空間。

6吋GaN外延片的供需不匹配

LED、功率元件和射頻元件製造商正在爭奪有限的6英寸GaN晶圓產能,而向8英寸生產線過渡的延遲進一步加劇了這種緊張局面。價格波動和分配風險正在擠壓那些沒有自有外延設施或戰略供應合約的晶片製造商的利潤空間。這些趨勢正在加速中國大陸、台灣和韓國的垂直整合,但同時也提高了依賴商用晶圓的無晶圓廠設計公司的進入門檻。

細分市場分析

預計到2025年,傳統LED仍將維持80.36%的市場佔有率,憑藉低於0.10美元/晶片的可靠每流明成本優勢,支撐著亞太地區LED晶片市場的規模。 Mini-LED陣列透過支援電視和顯示器中數千個局部調光區域,同時避免了像micro-LED那樣需要進行大規模批量傳輸的負擔,正在開闢高階中階市場。高階電視製造商正在將螢幕大小從43英寸擴展到100英寸,增加了每個面板的晶片數量,從而為高價值的晶片分級和溫度控管服務創造了機會。 micro-LED晶片的出貨量目前仍不到5%,但正以14.34%的複合年成長率成長,這主要得益於用於超大尺寸電視的直下式顯示器和擴增實境(AR)穿戴式裝置的先導計畫。隨著micro-LED產能的提高,掌握了六標準差傳輸良率和平行雷射設備的供應商有望將其最初的技術優勢轉化為可觀的收入。

通用型傳統LED的價格壓力持續擠壓毛利率,各大晶圓廠正透過晶圓自動化處理並引進大型反應器來分攤固定成本。在電視背光領域,mini-LED的最佳應用範圍正在擴大。這是因為知名品牌正在將量子點和高密度LED矩陣結合,以實現媲美OLED的對比度,而且該領域的成長潛力遠超預測期。 Micro-LED架構的每流明功耗是mini-LED的2到3倍,但亞太地區的LED晶片市場仍更注重可靠的交貨時間而非尖端技術,因此micro-LED產能的擴張正以謹慎而穩健的步伐進行。中國、韓國和台灣的技術藍圖正在逐步設定良率提升的里程碑,目標是2028年實現99.9999%的傳輸性能。這有望成為大規模應用的關鍵轉折點。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高階電視機中Mini-LED背光技術的廣泛應用

- 政府主導的「印度製造」LED晶片製造獎勵措施

- 消毒系統中對UV-C LED晶片的需求不斷成長

- 東南亞摩托車的電動化

- 磷光體的微型LED架構,可降低每流明成本。

- 企業淨零排放目標正在加速工業LED的維修。

- 市場限制因素

- 在大批量微型LED轉移中保持穩定產量的挑戰。

- 6吋GaN外延片的供需不匹配

- 新創公司交叉授權財產權的障礙

- 稀土元素磷光體價格波動會影響晶片的利潤率。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型分類的LED晶片技術

- 傳統LED

- Mini-LED

- Micro-LED

- 透過半導體材料

- GaN/InGaN

- AlGaInP

- 其他半導體材料

- 透過使用

- 一般照明

- 車

- 背光/顯示器

- 家用電子產品

- 工業/特殊照明

- 按地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, an SGH Company

- Epistar Corporation

- EVERLIGHT Electronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lumileds Holding BV

- NationStar Optoelectronics Co., Ltd.

- Lite-On Technology Corporation

- TYNTEK Corporation

- Lextar Electronics Corporation

- Bridgelux, Inc.

- Ams-OSRAM AG

- Rohinni, LLC

- PlayNitride Inc.

- HC SemiTek Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia pacific lED chips market size is expected to grow from USD 18.41 billion in 2025 to USD 19.97 billion in 2026 and is forecast to reach USD 32.60 billion by 2031 at 10.3% CAGR over 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, Micro-LED), Semiconductor Material (GaN/InGaN, Algainp, Other Semiconductor Materials), Application (General Lighting, Automotive, and More), and Geography (China, Japan, India, South Korea, Southeast Asia, Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific LED Chips Market Trends and Insights

Government-Led "Make In India" Incentives For LED Chip Fabrication

India's Production Linked Incentive scheme grants 4-6% rewards on incremental sales of qualified LED components, spurring brownfield expansions and new fabs that target a steep jump in domestic value addition from below 20% toward 80%. Approved applicants have already pledged more than USD 1 billion, unlocking a pathway for global chip producers to diversify sourcing and cut reliance on any single country.Success depends on parallel investment in GaN epitaxy reactors, trained talent, and supportive infrastructure, areas now moving up the policy priority list.

Electrification Of Two-Wheeler Mobility In Southeast Asia

Electric scooters and motorcycles dominate urban transport in Vietnam, Thailand, and Indonesia, creating a surge in demand for power-efficient LED headlamps, taillights, and instrument clusters. Adaptive beams and daytime running lights raise the chip content per vehicle, while the tropical climate sets strict thermal performance requirements. Vehicle makers favor modular LED assemblies that lower assembly complexity and warranty costs, positioning chip vendors with robust thermal engineering capabilities for outsized gains.

Supply-Demand Mismatch Of 6-Inch GaN Epitaxial Wafers

LED, power, and RF device makers are competing for finite 6-inch GaN wafer capacity, a tension aggravated by the slow migration to 8-inch lines. Price volatility and allocation risk squeeze margins for chip producers lacking captive epitaxy or strategic supply agreements. The dynamic fuels vertical integration moves across China, Taiwan, and South Korea, but raises entry barriers for fabless design houses that depend on merchant wafer supply.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Targets Accelerating Industrial LED Retrofits

- Expanding Mini-LED Backlighting Adoption In High-End TVs

- Persistent Yield Challenges In Micro-LED Mass Transfer

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The conventional LED segment retained 80.36% share in 2025, anchoring the Asia Pacific LED chips market size with dependable cost-per-lumen economics at sub-USD 0.10 per chip. Mini-LED arrays have carved out a premium middle ground, supporting thousands of local dimming zones in televisions and monitors while avoiding the full mass-transfer burden of micro-LEDs. Premium TV makers are scaling screen sizes from 43-inch to 100-inch, raising chip counts per panel and creating fertile ground for value-added binning and thermal management services. Micro-LED chips, although still below 5% volume, are advancing at a 14.34% CAGR on the back of direct-emissive display pilots for ultra-large TVs and augmented-reality wearables. Suppliers that master six-sigma transfer yields and parallel laser tools stand to translate early technical wins into outsized revenue as micro-LED throughput improves.

Price pressure in commodity conventional LEDs continues to compress gross margins, prompting large fabs to automate wafer handling and adopt larger-format reactors to dilute fixed costs. Mini-LED's sweet spot in television backlighting is widening as blue-chip brands pair quantum dots with denser LED matrices to deliver OLED-like contrast, extending the segment's runway beyond the forecast horizon. Micro-LED architectures command pricing power that is two to three times higher than mini-LEDs on a per-lumen basis, but the Asia Pacific LED chips market still values predictable delivery schedules over bleeding-edge claims, explaining the cautious but steady pace of micro-LED capacity additions. Technology roadmaps across China, South Korea, and Taiwan now sequence incremental yield milestones, aiming for 99.9999% transfer performance by 2028, which will be a decisive inflection for volume adoption.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, an SGH Company

- Epistar Corporation

- EVERLIGHT Electronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lumileds Holding B.V.

- NationStar Optoelectronics Co., Ltd.

- Lite-On Technology Corporation

- TYNTEK Corporation

- Lextar Electronics Corporation

- Bridgelux, Inc.

- Ams-OSRAM AG

- Rohinni, LLC

- PlayNitride Inc.

- HC SemiTek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Mini-LED Backlighting Adoption in High-End TVs

- 4.2.2 Government-Led "Make in India" Incentives for LED Chip Fabrication

- 4.2.3 Growing Demand for UV-C LED Chips in Sterilization Systems

- 4.2.4 Electrification of Two-Wheeler Mobility in Southeast Asia

- 4.2.5 Phosphor-Free Micro-LED Architectures Reducing Cost per Lumen

- 4.2.6 Corporate Net-Zero Targets Accelerating Industrial LED Retrofits

- 4.3 Market Restraints

- 4.3.1 Persistent Yield Challenges in Micro-LED Mass Transfer

- 4.3.2 Supply-Demand Mismatch of 6-Inch GaN Epitaxial Wafers

- 4.3.3 Intellectual-Property Cross-Licensing Barriers for Start-Ups

- 4.3.4 Volatile Rare-Earth Phosphor Prices Affecting Chip Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Southeast Asia

- 5.4.6 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Cree LED, an SGH Company

- 6.4.5 Epistar Corporation

- 6.4.6 EVERLIGHT Electronics Co., Ltd.

- 6.4.7 San'an Optoelectronics Co., Ltd.

- 6.4.8 OSRAM Opto Semiconductors GmbH

- 6.4.9 LG Innotek Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Lumileds Holding B.V.

- 6.4.12 NationStar Optoelectronics Co., Ltd.

- 6.4.13 Lite-On Technology Corporation

- 6.4.14 TYNTEK Corporation

- 6.4.15 Lextar Electronics Corporation

- 6.4.16 Bridgelux, Inc.

- 6.4.17 Ams-OSRAM AG

- 6.4.18 Rohinni, LLC

- 6.4.19 PlayNitride Inc.

- 6.4.20 HC SemiTek Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類

LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類 LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年

LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年