|

市場調查報告書

商品編碼

2063933

中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

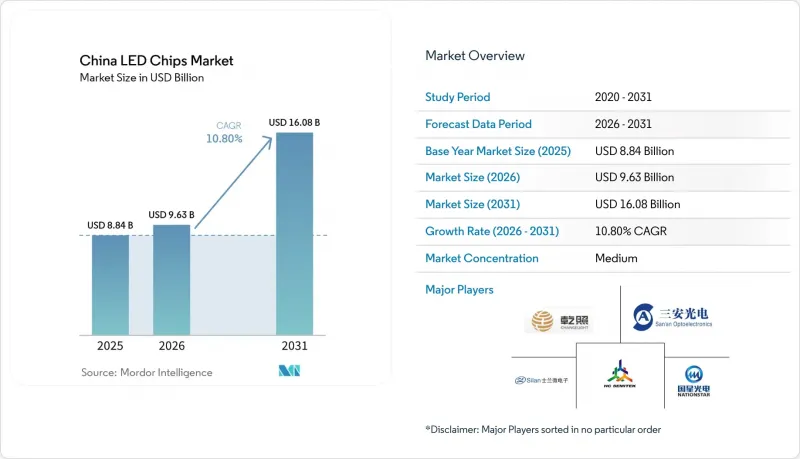

根據 Mordor Intelligence 預測,中國 LED 晶片市場規模預計到 2025 年將達到 88.4 億美元,到 2026 年將達到 96.3 億美元,到 2031 年將達到 160.8 億美元,2026 年至 2031 年的複合年成長率為 10.8%。

本報告按LED晶片技術(傳統LED、Mini-LED、Micro-LED)、半導體材料(GaN/InGaN、AlGaInP及其他半導體材料)和應用領域(通用照明、汽車照明、背光/顯示器、家用電子電器、工業/特殊照明)進行細分。市場預測以美元計價。

中國LED晶片市場趨勢與洞察

政府對國內半導體製造的補貼

國家積體電路基金第三期將於2024年投入470億美元,其中18%將用於化合物半導體,使認證LED晶圓廠的MOCVD反應器成本降低高達50%。此外,省級聯合投資還將追加85億美元,將促進產能快速擴張並確保短期資金籌措。然而,獲得補貼的企業必須在2027年前達到90%的設備國產化率,並達到15%的年生產力。這些要求有利於已經形成規模的大型企業。三安電子報告稱,2024年獲得的政府補貼相當於其淨利潤的22%,凸顯了其對政府補貼的持續依賴。雖然財政支持將加速產能擴張,但績效評估標準將透過強化領導企業企業的競爭優勢並淘汰競爭力較弱的新進入者,從而塑造中國LED晶片市場的中期格局。

向高效GaN-on-Si外延過渡

三安半導體和HC SemiTek被8吋晶圓特有的基板成本降低30-40%以及更高的晶片密度所吸引,在2025年第一季至2026年第一季期間,將其GaN-on-Si元件的總合能從31台擴充至47台。 2025年宣布的緩衝層技術突破使良率提升至91%,大幅縮小了與藍寶石平台的差距。儘管出於散熱的考慮,藍寶石仍然是高亮度LED領域的首選,但GaN-on-Si技術能夠實現低成本的LED燈和中功率背光,從而擴大了目標市場需求。能夠克服晶圓翹曲管理和熱失配問題的製造商,不僅可以提高利潤率,還能延長現有生產線的壽命,從而保持中國LED晶片市場的成長勢頭。

用於微型LED大規模生產的大量資本投資

最先進的雷射或靜電轉印設備單價在1,200萬美元至1,800萬美元之間,但其產能僅為滿足消費者經濟需求的20%至40%,這使得一條微型LED生產線的資本投資超過5,000萬美元。除非設備速度翻倍且缺陷率減半,否則穿戴式裝置和電視等產品難以大規模普及。對於大多數國內晶片製造商而言,早期階段的負盈利阻礙了其積極擴大規模,並削弱了中國LED晶片市場短期內的成長動力。

細分市場分析

2025年,傳統LED仍將佔中國LED晶片市場83%的佔有率,即使價格下降8-12%,也能支撐中國LED晶片市場的規模。成熟的4吋和6吋生產線仍在產生正現金流,為Mini-LED和Micro-LED的研發投入提供資金。 Mini-LED背光燈的出貨量已達420萬台電視,帶動了晶片(半導體晶片)出貨量的顯著成長。如果到2027年65吋OLED面板的價格降至300美元以下,Mini-LED的應用市場可能會萎縮至戶外標示牌和商用顯示器領域。然而,目前市場對局部調光和更高亮度的需求,正推動Mini-LED保持成長勢頭,進而支撐中國LED晶片市場的整體銷售成長。

儘管預計到2025年,microLED的銷售額佔比將不足2%,但其複合年成長率預計將達到約15.64%,到2031年將位居所有晶片類型之首。穿戴式顯示器和汽車抬頭顯示器需要無機發光元件所提供的高亮度和長壽命。 2025年發表在《自然·光子學》上的一項研究表明,間距小於10µm的microLED的效率可超過250lm/W,這不僅證明了其物理可行性,也凸顯了製造方面的挑戰。隨著矩陣轉移技術的進步,microLED最終可能會改變市場收入結構,但在未來三年內,傳統LED仍將繼續支撐中國LED晶片市場的整體技術轉型。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高階電視對Mini-LED背光的需求日益成長

- 政府對國內半導體製造的補貼

- 向高效GaN-on-Si外延過渡

- 新能源汽車頭燈的快速普及

- 在整個消費性電子產品供應鏈中推動在地化。

- 將微型LED整合到下一代穿戴式裝置中

- 市場限制因素

- 傳統LED晶片生產線產能過剩

- 微型LED的大規模生產需要大量資金投入。

- 與海外智慧財產權擁有者之間的專利訴訟風險

- 藍寶石和碳化矽基板的價格波動

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型分類的LED晶片技術

- 傳統LED

- Mini-LED

- Micro-LED

- 透過半導體材料

- GaN/InGaN

- AlGaInP

- 其他半導體材料

- 透過使用

- 一般照明

- 車

- 背光/顯示器

- 家用電子產品

- 工業/特殊照明

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sanan Optoelectronics Co., Ltd.

- HC SemiTek Corporation

- Xiamen Changelight Co., Ltd.

- Hangzhou Silan Microelectronics Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Jiangsu Azure Lighting Technologies Co., Ltd.

- Focus Lightings Tech Co., Ltd.

- Zhejiang Keguang Electronics Co., Ltd.(KINGLIGHT)

- Advanced Optoelectronic Technology, Inc.

- Epistar Corporation

- Nichia Corporation

- Cree LED, an SGH Company

- Lumileds Holding BV

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Genesis Photonics Inc.

- Shenzhen Refond Optoelectronics Co., Ltd.

- Shenzhen MTC Co., Ltd.

- Unistars Corporation

- Tianjin Zhonghuan Semiconductor Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china lED chips market size is projected to be USD 8.84 billion in 2025, USD 9.63 billion in 2026, and reach USD 16.08 billion by 2031, growing at a CAGR of 10.8% from 2026 to 2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, Micro-LED), Semiconductor Material (GaN/InGaN, Algainp, Other Semiconductor Materials), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, Industrial/Specialty Lighting). The Market Forecasts are Provided in Terms of Value (USD).

China LED Chips Market Trends and Insights

Government Subsidies for Domestic Semiconductor Manufacturing

Phase III of the National IC Fund earmarked USD 47 billion in 2024, with 18% directed to compound semiconductors, lowering MOCVD reactor costs by up to 50% for qualified LED fabs.Provincial co-funding adds a further USD 8.5 billion, translating into rapid capacity gains and safeguarding near-term capital access. Subsidy recipients, however, must hit 90% domestic equipment usage and 15% annual productivity metrics by 2027, requirements that favor entrenched scale players. Sanan reported government grants equal to 22% of 2024 net income, underscoring continuing dependence. While the cash support accelerates volume, the performance thresholds strengthen the competitive moat around leaders and cull weaker entrants, shaping the medium-term structure of the China LED chips market.

Transition Toward High-Efficacy GaN-on-Si Epitaxy

Sanan and HC SemiTek expanded their combined GaN-on-Si fleet from 31 to 47 reactors between Q1 2025 and Q1 2026, attracted by 30-40% lower substrate cost and the die density gains inherent to 8-inch wafers.Buffer-layer engineering breakthroughs published in 2025 pushed yields to 91%, closing much of the gap with sapphire platforms. Although high-brightness segments still prefer sapphire for thermal reasons, GaN-on-Si enables low-cost lamps and mid-power backlighting, broadening addressable demand. Producers that master wafer bow management and thermal mismatch will unlock margin relief while extending the lifespan of conventional lines, thereby sustaining the growth momentum of the China LED chips market.

High Capital Expenditure for Micro-LED Mass Transfer

State-of-the-art laser or electrostatic transfer tools cost USD 12-18 million each yet deliver only 20-40% of the throughput that consumer economics require, pushing a single micro-LED line's capex above USD 50 million. Until tool speeds double and defect rates halve, mass-market wearables and TVs remain out of reach. For most domestic chipmakers, negative early-stage returns deter aggressive scaling, tempering the near-term uplift to the China LED chips market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of New-Energy Vehicle Headlamp Adoption

- Rising Demand for Mini-LED Backlighting in High-End TVs

- Overcapacity in Conventional LED Chip Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs generated 83% of 2025 revenue, anchoring the China LED chips market size despite 8-12% price compression. Mature 4-inch and 6-inch lines still deliver positive cash flow, subsidizing R&D into mini-LED and micro-LED. Mini-LED backlighting shipments reached 4.2 million TV units, translating into a significant uplift in die volumes. Should OLED panels fall below USD 300 for a 65-inch size by 2027, mini-LED could retrench to outdoor signage and professional monitors. Yet today's local dimming requirements and brightness advantages keep mini-LED on an expansion path that supports total unit growth in the China LED chips market.

Micro-LED, though contributing less than 2% of 2025 sales, is projected to grow at about 15.64% CAGR through 2031, the fastest among chip types. Wearable displays and automotive head-up units require the high brightness and extended lifetime that inorganic emitters provide. A 2025 Nature Photonics study validated efficiencies above 250 lm/W at sub-10 µm pitches, proving the physics while highlighting manufacturing hurdles. As mass-transfer improves, micro-LED could eventually shift revenue mix, but for the next three years, conventional LEDs will continue to bankroll technological migration across the China LED chips market.

List of Companies Covered in this Report:

- Sanan Optoelectronics Co., Ltd.

- HC SemiTek Corporation

- Xiamen Changelight Co., Ltd.

- Hangzhou Silan Microelectronics Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Jiangsu Azure Lighting Technologies Co., Ltd.

- Focus Lightings Tech Co., Ltd.

- Zhejiang Keguang Electronics Co., Ltd. (KINGLIGHT)

- Advanced Optoelectronic Technology, Inc.

- Epistar Corporation

- Nichia Corporation

- Cree LED, an SGH Company

- Lumileds Holding B.V.

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Genesis Photonics Inc.

- Shenzhen Refond Optoelectronics Co., Ltd.

- Shenzhen MTC Co., Ltd.

- Unistars Corporation

- Tianjin Zhonghuan Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Mini-LED Backlighting in High-End TVs

- 4.2.2 Government Subsidies for Domestic Semiconductor Manufacturing

- 4.2.3 Transition Toward High-Efficacy GaN-on-Si Epitaxy

- 4.2.4 Rapid Expansion of New-Energy Vehicle Headlamp Adoption

- 4.2.5 Localization Push Across Consumer Electronics Supply Chains

- 4.2.6 Integration of Micro-LED in Next-Gen Wearables

- 4.3 Market Restraints

- 4.3.1 Overcapacity in Conventional LED Chip Lines

- 4.3.2 High Capital Expenditure for Micro-LED Mass Transfer

- 4.3.3 Patent Litigation Risks with Foreign IP Holders

- 4.3.4 Volatility in Sapphire and Silicon Carbide Substrate Prices

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sanan Optoelectronics Co., Ltd.

- 6.4.2 HC SemiTek Corporation

- 6.4.3 Xiamen Changelight Co., Ltd.

- 6.4.4 Hangzhou Silan Microelectronics Co., Ltd.

- 6.4.5 NationStar Optoelectronics Co., Ltd.

- 6.4.6 Jiangsu Azure Lighting Technologies Co., Ltd.

- 6.4.7 Focus Lightings Tech Co., Ltd.

- 6.4.8 Zhejiang Keguang Electronics Co., Ltd. (KINGLIGHT)

- 6.4.9 Advanced Optoelectronic Technology, Inc.

- 6.4.10 Epistar Corporation

- 6.4.11 Nichia Corporation

- 6.4.12 Cree LED, an SGH Company

- 6.4.13 Lumileds Holding B.V.

- 6.4.14 OSRAM Opto Semiconductors GmbH

- 6.4.15 Seoul Semiconductor Co., Ltd.

- 6.4.16 Genesis Photonics Inc.

- 6.4.17 Shenzhen Refond Optoelectronics Co., Ltd.

- 6.4.18 Shenzhen MTC Co., Ltd.

- 6.4.19 Unistars Corporation

- 6.4.20 Tianjin Zhonghuan Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類

LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類 LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年

LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年