|

市場調查報告書

商品編碼

2065498

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Japan LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

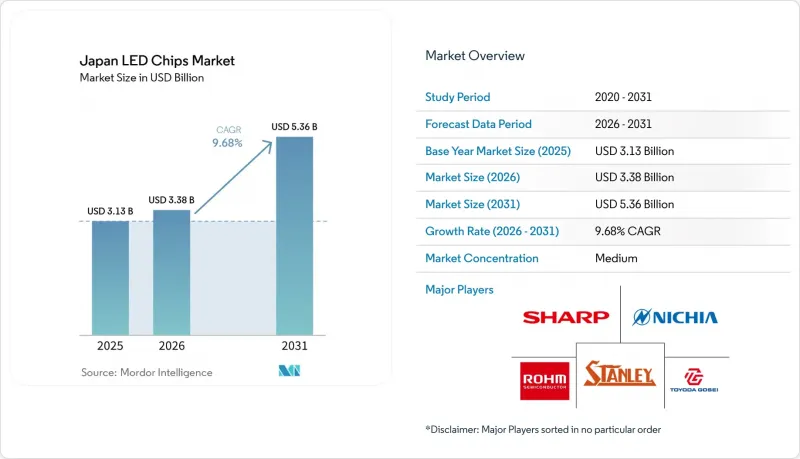

根據 Mordor Intelligence 預測,日本 LED 晶片市場預計將從 2025 年的 31.3 億美元成長到 2026 年的 33.8 億美元,到 2031 年達到 53.6 億美元,2026 年至 2031 年的複合年成長率預計為 9.68%。

本報告按LED晶片技術(傳統LED、Mini-LED、Micro-LED)、半導體材料(GaN/InGaN、AlGaInP及其他半導體材料)和應用領域(通用照明、汽車照明、背光/顯示器、家用電子電器、工業/特殊照明)進行細分。市場預測以美元計價。

日本LED晶片市場趨勢與洞察

政府對國內半導體生產的支持措施

2023年,日本向生產邏輯、記憶體和光電元件的晶圓廠提供了1.85兆日圓(約126億美元)的補貼。對台積電熊本第二工廠和Rapidus 2奈米中試生產線的支持,確保了潔淨室基礎設施建設的資金到位,這些設施目前已在包括LED外延在內的化合物半導體項目中共用。九州和北海道的人力資源發展計畫進一步增強了區域人才儲備,並緩解了LED晶圓廠的招募難題。

電動汽車頭燈的整合程度正在迅速提高。

小糸馬達報告稱,LED燈已佔其頭燈產量的82%,並計劃在2030年實現100%使用LED燈。自我調整遠光燈模組需要多達16,000個可獨立控制的發送器,與鹵素燈相比,每個單元的晶片數量增加了兩個數量級。日亞化學工業株式會社和英飛凌公司聯合推出了一款包含16,384個發光元件的微矩陣光引擎。與傳統方案相比,該技術可將功耗降低約18%,這對延長電池式電動車的續航里程至關重要。

用於微型LED大規模生產的大量資本投入

能夠達到接近99.99%組裝良率的工具組價格仍然昂貴。濱松光子學計畫在2025年投資370億日圓(約2.5億美元)運作一條8吋晶圓加工生產線,但如果下游轉移工具的效能達不到預期,這條生產線的獲利能力可能會受到影響。中小企業通常選擇購買晶片結構的授權,而不是投資整個微型LED後端製程。

細分市場分析

到2025年,傳統LED將佔據日本LED晶片市場約82.5%的佔有率(基於折舊免稅額的老舊生產線),但在市政照明昇級項目中,其每美元流明效率仍具有競爭力。 Mini-LED兼具性能和成本優勢,使高階電視品牌能夠在無需OLED成本的情況下實現高局部調光比。隨著汽車自我調整遠光燈和新興的擴增實境(AR)顯示技術對像素密度的要求越來越高,傳統晶片無法滿足這一需求,預計日本微型LED晶片市場規模將以約14%的複合年成長率成長。

日亞化學於2026年推出的DominoPLS模組,透過將微陣列整合到通用陶瓷基板上,降低了矩陣燈的成本,簡化了小型車的組裝。提高小於3µm的紅色發送器的效率仍然是一項挑戰,但供應商正與材料實驗室合作,力求將外部量子效率提升到超過5%的閾值,以滿足全彩穿戴式設備的要求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- Mini-LED背光電視的廣泛應用

- 政府對國內半導體生產的激勵措施

- 電動車頭燈整合度的激增

- 節能法規鼓勵用LED燈取代舊燈具。

- 植物工廠對園藝照明的需求日益成長

- 物聯網建築中智慧照明的發展

- 市場限制因素

- 鎵和銦供應鏈中斷

- 微型LED的大規模生產需要大量資金投入。

- 來自中國供應商的價格壓力日益增大

- LED晶片設計的專利訴訟風險

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- LED晶片技術

- 傳統LED

- Mini-LED

- Micro-LED

- 透過半導體材料

- GaN/InGaN

- AlGaInP

- 其他半導體材料

- 透過使用

- 一般照明

- 車

- 背光/顯示器

- 家用電子產品

- 工業/特殊照明

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Toyoda Gosei Co., Ltd.

- Rohm Co., Ltd.

- Stanley Electric Co., Ltd.

- Sharp Corporation

- Sony Semiconductor Solutions Corporation

- Seoul Semiconductor Co., Ltd.

- Osram Opto Semiconductors GmbH

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lumileds Holding BV

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Kingbright Electronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan lED chips market size is expected to increase from USD 3.13 billion in 2025 to USD 3.38 billion in 2026 and reach USD 5.36 billion by 2031, growing at a CAGR of 9.68% over 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, Algainp, and Other Semiconductor Materials), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting). The Market Forecasts are Provided in Terms of Value (USD).

Japan LED Chips Market Trends and Insights

Government Incentives for Domestic Semiconductor Production

Japan allocated JPY 1.85 trillion (USD 12.6 billion) in 2023 subsidies for fabs that cover logic, memory, and photonics devices. Support for TSMC's second Kumamoto plant and Rapidus's 2-nanometer pilot line finances clean-room infrastructure now shared by compound-semiconductor projects, including LED epitaxy. Workforce training programs in Kyushu and Hokkaido further reinforce the local talent pool, easing recruitment challenges for LED foundries.

Surge in Electric-Vehicle Headlamp Integration

Koito reported that LEDs already represent 82% of its headlamp output and targets 100% by 2030.Adaptive driving beam modules need as many as 16,000 individually addressed emitters, lifting per-vehicle chip counts by two orders of magnitude versus halogen. Nichia and Infineon unveiled a micro-matrix light engine featuring 16,384 emitters that lowers power draw by about 18% compared with preceding solutions, a critical benefit for battery-electric range preservation.

High Capital Expenditure for Micro-LED Mass Transfer

Tool sets that approach 99.99% placement yield remain expensive. Hamamatsu Photonics invested JPY 37 billion (USD 250 million) in 2025 to bring 8-inch wafer processing online, yet the line can still lose profitability if downstream transfer tools underperform.Smaller firms often opt to license chip architectures rather than bankroll full Micro-LED back-ends.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations Favoring LED Retrofits

- Rising Adoption of Mini-LED Backlit TVs

- Supply Chain Disruptions for Gallium and Indium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs represented about 82.5% of the Japanese LED chips market share in 2025, anchored by depreciated legacy lines that still deliver competitive lumens-per-dollar for municipal retrofits. Mini-LED bridges performance and cost, giving premium TV brands high local-dimming ratios without OLED expense. The Japan LED chips market size tied to Micro-LED is forecast to expand at a near 14% CAGR because automotive adaptive driving beams and emerging augmented-reality displays require pixel densities that legacy chips cannot achieve.

Nichia's DominoPLS modules introduced in 2026 cut matrix-lamp cost by integrating micro-arrays onto a common ceramic substrate, simplifying assembly for compact vehicles. Red emitter efficiency below 3 µm remains difficult, but suppliers collaborate with material labs to boost external quantum efficiency beyond 5%, a threshold needed for full-color wearables.

List of Companies Covered in this Report:

- Nichia Corporation

- Toyoda Gosei Co., Ltd.

- Rohm Co., Ltd.

- Stanley Electric Co., Ltd.

- Sharp Corporation

- Sony Semiconductor Solutions Corporation

- Seoul Semiconductor Co., Ltd.

- Osram Opto Semiconductors GmbH

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lumileds Holding B.V.

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Kingbright Electronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Mini-LED Backlit TVs

- 4.2.2 Government Incentives for Domestic Semiconductor Production

- 4.2.3 Surge in Electric Vehicle Headlamp Integration

- 4.2.4 Energy-Efficiency Regulations Favoring LED Retrofits

- 4.2.5 Increasing Demand for Plant-Factory Horticulture Lighting

- 4.2.6 Growth of Smart Lighting in IoT-Enabled Buildings

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions for Gallium and Indium

- 4.3.2 High Capital Expenditure for Micro-LED Mass Transfer

- 4.3.3 Intensifying Price Pressure from Chinese Suppliers

- 4.3.4 Patent Litigation Risks in LED Chip Designs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Toyoda Gosei Co., Ltd.

- 6.4.3 Rohm Co., Ltd.

- 6.4.4 Stanley Electric Co., Ltd.

- 6.4.5 Sharp Corporation

- 6.4.6 Sony Semiconductor Solutions Corporation

- 6.4.7 Seoul Semiconductor Co., Ltd.

- 6.4.8 Osram Opto Semiconductors GmbH

- 6.4.9 Cree LED, Inc.

- 6.4.10 Samsung Electronics Co., Ltd.

- 6.4.11 LG Innotek Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Lumileds Holding B.V.

- 6.4.14 Bridgelux, Inc.

- 6.4.15 Everlight Electronics Co., Ltd.

- 6.4.16 Citizen Electronics Co., Ltd.

- 6.4.17 Kingbright Electronic Co., Ltd.

- 6.4.18 Dominant Opto Technologies Sdn. Bhd.

- 6.4.19 Lextar Electronics Corporation

- 6.4.20 NationStar Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類

LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類 LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年

LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年