|

市場調查報告書

商品編碼

2065500

歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Europe LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

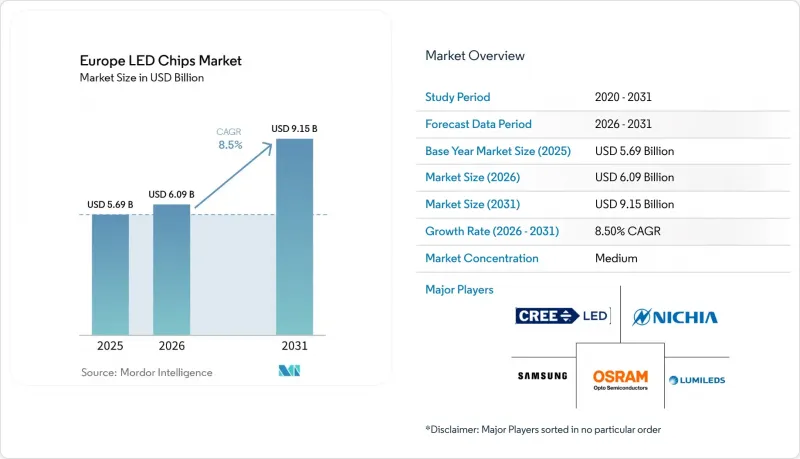

據 Mordor Intelligence 稱,歐洲 LED 晶片市場預計將從 2025 年的 56.9 億美元成長到 2026 年的 60.9 億美元,到 2031 年達到 91.5 億美元,預計 2026 年至 2031 年的複合年成長率為 8.5%。

本報告按LED晶片技術(傳統LED、Mini-LED、Micro-LED)、半導體材料(GaN/InGaN及其他半導體材料)、應用領域(通用照明、汽車照明、背光/顯示器、家用電子電器、工業/特殊照明)以及地區(英國、法國及其他歐洲國家)進行細分。市場預測以美元計價。

歐洲LED晶片市場的趨勢與洞察

智慧城市向路燈過渡

各市政當局正在維修公共照明系統,以降低高達75%的電力成本。 2024年,巴黎市政府簽署了一份價值7億歐元(約7.63億美元)的契約,計劃用配備遠距離診斷功能的LED燈具替換7萬盞舊燈具。米盧斯市政府投資2,400萬歐元(約2,616萬美元)改造1.4萬盞燈具,目標在2026年夏季前完成。法國的「Lum'ACTEE+」計畫已撥款1,500萬歐元(約1,635萬美元),計畫在2028年前在全國範圍內更換多達400萬盞燈具。智慧控制技術透過增加驅動積體電路和連接模組,並提高單顆LED晶片的半導體用量,正在擴大整個歐洲LED晶片市場。

電動汽車頭燈整合範圍的擴大

歐洲汽車製造商正採用高密度LED矩陣來遵守修訂後的ECE 123號法規,該法規強制要求2027年1月後推出的新車必須配備自我調整頭燈。歐司朗的「EVIYOS HD25」微型LED陣列擁有25,600個可尋址像素,目前已量產應用於奧迪Q6 e-tron和蔚來ET9車型。大眾2026款途銳和途觀將配備19,200像素的IQ.Light智慧頭燈,可在維持最大照明效果的同時,避免對向來車造成眩光。德國汽車製造商的集中度支撐了當地對晶片的需求,而日亞化學工業株式會社於2024年在亞琛成立的研發中心正在加強與汽車製造商的合作。

微型LED大規模生產需要高額的資本投資成本。

根據一家研究公司估計,到2025年,86.2%的材料成本將來自基板和轉移設備。 Springer在2024年的報告中指出,要達到OLED面板的經濟可行性,成品率需要超過99.9999%,但目前一代設備很少能達到大基板的這一標準。儘管應用材料公司及其競爭對手正努力將產量提高十倍,但預計在2028年甚至2030年之前,都不太可能實現與OLED的成本持平。歐洲顯示器組裝缺乏韓國大型企業數十億美元的資本投資能力,在經濟可行性提高之前,他們可能被迫專注於汽車抬頭顯示器(HUD)和穿戴式裝置面板等細分市場。

細分市場分析

2025年,傳統LED佔據了歐洲LED晶片市場80.26%的佔有率,這得益於成熟的供應鏈以及適用於通用照明和汽車外飾燈的中功率價格低於0.10美元。由於效率的逐步提升,例如日亞化學的757系列在65毫安培電流下實現了220流明/瓦的效率,該細分市場在價格敏感型應用領域仍然保持著競爭力。 Mini-LED則佔據了中間位置,並正在成為高階電視和車載資訊娛樂螢幕的標準升級方案,因為它們可以實現數千個局部調光區域,而無需像micro-LED那樣面臨品質傳輸方面的挑戰。

微型LED正以12.34%的複合年成長率穩步發展,其試點應用已應用於超大尺寸電視、像素尺寸小於10微米的智慧型手錶顯示器以及亮度高達10000尼特的汽車抬頭顯示器。 PlayNitride和Plessey正在推動尺寸小於5微米的單片式矽基微型LED陣列的研發,並將這種架構定位為下一代AR頭顯中OLED的繼任者。儘管隨著生態設計法規縮短改造週期,傳統LED的銷售量預計將趨於平穩,但其龐大的應用規模將確保長期的市場需求。預計到2028年,Mini-LED電視的出貨量將超過1500萬台,並有望保持成長勢頭,直到微型LED實現成本效益並成為主流產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 採用Mini-LED背光技術的顯示器迅速普及

- 電動汽車頭燈整合擴展

- 向智慧城市路燈過渡

- 歐盟綠色交易能源效率目標

- 擴大該廠晶圓層次電子構裝產能。

- UV-C LED 消毒系統的普及

- 市場限制因素

- 鎵和銦供應量的變化

- 微型LED大規模生產需要高額的資本投資成本

- 關於智慧財產權分割和版稅的爭議

- 在高階顯示器領域與OLED展開競爭

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- LED晶片技術

- 傳統LED

- Mini-LED

- Micro-LED

- 透過半導體材料

- GaN/InGaN

- AlGaInP

- 其他半導體材料

- 透過使用

- 一般照明

- 車

- 背光/顯示器

- 家用電子產品

- 工業/特殊照明

- 按地區

- 英國

- 德國

- 法國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Lumileds Holding BV

- Cree LED

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- II-VI Incorporated

- Epistar Corp.

- ams-OSRAM AG

- Rohinni LLC

- PlayNitride Inc.

- Plessey Semiconductors Ltd.

- Lextar Electronics Corp.

- OptoGaN Ltd.

- Everlight Electronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn Bhd

- Brightek Optoelectronic Co., Ltd.

- Crystal IS, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe lED chip market size is expected to increase from USD 5.69 billion in 2025 to USD 6.09 billion in 2026 and reach USD 9.15 billion by 2031, growing at a CAGR of 8.5% over 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, and Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting), and Geography (United Kingdom, France, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe LED Chips Market Trends and Insights

Shift Toward Smart City Streetlighting

Municipalities are retrofitting public lighting to shrink electricity bills by up to 75%. Paris awarded a EUR 700 million (USD 763 million) contract in 2024 to replace 70,000 fixtures with LED luminaires equipped with remote diagnostics. Mulhouse committed EUR 24 million (USD 26.16 million) to modernize 14,000 lamps, targeting completion by summer 2026. France's Lum'ACTEE+ program earmarked EUR 15 million (USD 16.35 million) for a nationwide upgrade of up to 4 million luminaires by 2028. Smart controls boost per-pole semiconductor content by adding driver ICs and connectivity modules, elevating the overall Europe LED chip market value.

Expanding EV Headlamp Integration

Europe's vehicle makers are embedding increasingly dense LED matrices to comply with amendments to ECE Regulation 123, which mandate adaptive front lighting on new models after January 2027. ams OSRAM's EVIYOS HD25 micro-LED array offers 25,600 addressable pixels and is already in volume production for the Audi Q6 e-tron and the NIO ET9. Volkswagen's 2026 Touareg and Tiguan carry 19,200-pixel IQ. Light headlamps that maintain maximum illumination while avoiding glare for oncoming traffic. German OEM concentration anchors chip demand locally, and Nichia's 2024 Aachen innovation center strengthens vendor collaboration with automakers.

High Capital Cost for Micro-LED Mass Transfer

The research company estimated that, in 2025, 86.2% of the materials stemmed from substrates and transfer tools. Springer's 2024 review concluded that yields above 99.9999% are necessary to match OLED panel economics, but current equipment generations rarely meet this benchmark on large substrates. Applied Materials and peers are striving to lift throughput tenfold, yet cost parity with OLED appears unlikely before 2028-2030. European display assemblers, lacking the multibillion-dollar capex muscle of Korean giants, may be forced to focus on niche automotive HUD and wearable panels until the economics improve.

Other drivers and restraints analyzed in the detailed report include:

- EU Green Deal Energy-Efficiency Targets

- Rapid Adoption of Mini-LED Backlit Displays

- Supply Volatility of Gallium and Indium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs dominated the European LED chip market share at 80.26% in 2025, buoyed by mature supply chains and sub-USD 0.10 pricing for mid-power die suited to general lighting and exterior automotive lamps. Incremental efficiency gains, such as Nichia's 757 series reaching 220 lumens per watt at 65 milliamps, keep the segment competitive for price-sensitive use cases. Mini-LED occupies the middle ground, enabling thousands of local dimming zones without the mass-transfer hurdles that restrain micro-LED, and is becoming the default upgrade path for premium televisions and in-vehicle infotainment screens.

Micro-LED is advancing at a 12.34% CAGR through pilot deployments in ultra-large televisions, smartwatch faces with sub-10-micrometer pixels, and automotive heads-up displays requiring 10,000-nit brightness. PlayNitride and Plessey are pushing monolithic micro-LED-on-silicon arrays below 5 micrometers, positioning the architecture as a successor to OLED in next-generation AR headsets. Conventional LED revenue will plateau as Ecodesign rules compress retrofit windows, yet its vast installed base secures a lengthy tail. Mini-LED is expected to exceed 15 million television shipments by 2028, maintaining momentum until micro-LED hits mainstream cost thresholds.

List of Companies Covered in this Report:

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Cree LED

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- II-VI Incorporated

- Epistar Corp.

- ams-OSRAM AG

- Rohinni LLC

- PlayNitride Inc.

- Plessey Semiconductors Ltd.

- Lextar Electronics Corp.

- OptoGaN Ltd.

- Everlight Electronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn Bhd

- Brightek Optoelectronic Co., Ltd.

- Crystal IS, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Mini-LED Backlit Displays

- 4.2.2 Expanding EV Headlamp Integration

- 4.2.3 Shift Toward Smart City Streetlighting

- 4.2.4 EU Green Deal Energy-Efficiency Targets

- 4.2.5 Increased Local Wafer-Level Packaging Capacity

- 4.2.6 Proliferation of UV-C LED Disinfection Systems

- 4.3 Market Restraints

- 4.3.1 Supply Volatility of Gallium and Indium

- 4.3.2 High Capital Cost for Micro-LED Mass Transfer

- 4.3.3 IP Fragmentation and Royalty Disputes

- 4.3.4 Competition From OLED in Premium Displays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 OSRAM Opto Semiconductors GmbH

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Cree LED

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 II-VI Incorporated

- 6.4.9 Epistar Corp.

- 6.4.10 ams-OSRAM AG

- 6.4.11 Rohinni LLC

- 6.4.12 PlayNitride Inc.

- 6.4.13 Plessey Semiconductors Ltd.

- 6.4.14 Lextar Electronics Corp.

- 6.4.15 OptoGaN Ltd.

- 6.4.16 Everlight Electronics Co., Ltd.

- 6.4.17 San'an Optoelectronics Co., Ltd.

- 6.4.18 Dominant Opto Technologies Sdn Bhd

- 6.4.19 Brightek Optoelectronic Co., Ltd.

- 6.4.20 Crystal IS, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類

LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類 LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年

LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年