|

市場調查報告書

商品編碼

2063671

美國LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)United States LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

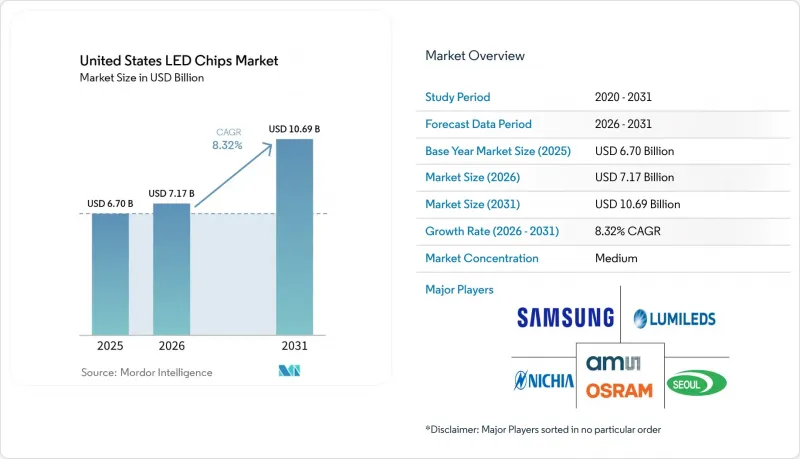

據 Mordor Intelligence 稱,2025 年美國 LED 晶片市值為 67 億美元,預計到 2031 年將達到 106.9 億美元,而 2026 年為 71.7 億美元,預測期(2026-2031 年)的複合年成長率為 8.32%。

本報告按LED晶片技術(傳統LED、Mini-LED等)、半導體材料(GaN/InGaN、AlGaInP等)和應用(通用照明、汽車、背光/顯示器、家用電子電器等)進行細分。市場預測以美元計價。

美國LED晶片市場趨勢與洞察

高階電視機中Mini-LED背光技術的廣泛應用

在2026年國際消費電子展(CES)上,採用數千顆紅、綠、藍三色mini-LED而非帶有彩色濾光片的白色LED的55英寸至130英寸電視被展示為主流產品後,銷售勢頭迅速增強。預計到2026年,mini-LED電視的出貨量將超過2,000萬台,而對晶片密度日益成長的需求迫使國內供應商將波長窗口縮小到2奈米以下。 2025年20-30%的成本降低使得這項技術得以從旗艦機型擴展到中階機型,從而擴大了正向電壓差小於0.1伏的氮化鎵(GaN)發光二極體的潛在市場。在美國LED晶片市場,這種累積效應已導致市場需求連續數年成長,這主要得益於電視、顯示器和遊戲機製造商對高密度晶片的強勁需求。 RGB mini-LED配置在某些設計中無需量子點層,使得晶片組件成本在系統整體價值中佔比更大。因此,能夠保證整批晶圓光束均勻性高的國內晶圓廠在贏得新的顯示器訂單方面更具優勢。

聯邦和州政府為固體照明產品提供節能獎勵

到2026年,補貼計畫將涵蓋美國商業占地面積的很大一部分,戶外照明類別的平均獎勵也將有所提高。第179D條稅額扣抵允許每平方英尺最高抵扣5.36美元,有效縮短了倉庫和冷藏設施高效照明維修的投資回收期,使其不到兩年。電力公司正從固定金額的單位補貼轉向節能模式,優先考慮能夠使照明燈具光效超過130流明/瓦並符合DesignLights聯盟優質產品標準的LED晶片。奧勒岡州將於2025年禁止使用螢光,夏威夷州將於2026年效仿,這將進一步減少對傳統燈具的獎勵,並將資金轉向具備網路控制功能的LED升級計畫。這些措施預計將確保未來 24 個月內美國 LED 晶片市場在獎盃、戶外和高棚照明燈具方面持續保持高需求。

碳化矽基板供應鏈瓶頸

碳化矽晶體生長仍是高能耗工藝,而向200毫米晶圓的轉變導致良率下降,進而削弱了有效產能。與功率元件製造商的競爭正在蠶食晶圓配額,因為電動車逆變器的利潤率高於LED外延。特種氣體和籽晶的進口限制,加上區域產業政策的摩擦,導致AEC-Q101認證元件的前置作業時間出現波動。美國半導體製造商正透過多年晶圓採購協議和旨在提高晶體品質的共同開發項目來規避風險,但小規模的參與企業缺乏議價能力,並面臨配額限制。由此導致的供應緊張將削弱美國LED晶片市場中高可靠性汽車和工業LED的成長潛力。

細分市場分析

到2025年,傳統發光元件將佔據美國LED晶片市場83.45%的佔有率,這反映了它們在獎盃、路燈和改裝燈具領域的主導地位。同時,mini-LED和micro-LED架構正以11.28%的複合年成長率快速成長,引領電視背光、主動式轉向頭燈和近眼AR微顯示器等高階產品市場。垂直氮化鎵(GaN)技術正逐漸成為一項過渡技術,它使單晶片的電流處理能力翻倍,從而實現照明設備的微型化,並提升高功率模組的散熱性能。

RGB mini-LED背光技術的普及使得一台電視機中整合了多達3萬顆晶片。雖然每流明的價格有所下降,但晶片的美元市佔率卻顯著上升,有效抵銷了通用照明領域的構成比。對micro-LED而言,大規模生產仍面臨許多挑戰,但國防航空電子設備和高階穿戴式裝置領域的試驗計畫正在驗證其可靠性。國內供應商將晶圓級分選技術與專有的無量子點色彩轉換技術結合,可望率先獲得市場認可。總而言之,大規模生產的傳統LED與快速發展的micro-LED節點的共存,使收入來源多元化,並保護了美國LED晶片市場免受單一細分市場波動的影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高階電視機中Mini-LED背光技術的廣泛應用

- 聯邦和州政府為固體照明產品提供節能獎勵

- 高功率氮化鎵晶片的每流明成本正在迅速下降。

- 汽車製造商專注於將LED像素照明應用於外部照明。

- 消毒系統中對UV-C LED晶片的需求不斷成長

- 智慧農業的興起需要園藝LED陣列

- 市場限制因素

- 碳化矽基板供應鏈瓶頸

- 用於大規模生產微型LED的設備需要大量資本投入

- 半導體製造商面臨的智慧財產權訴訟風險

- 溫度控管挑戰阻礙晶片小型化

- 產業供應鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型分類的LED晶片技術

- 傳統LED

- Mini-LED

- Micro-LED

- 透過半導體材料

- GaN/InGaN

- AlGaInP

- 其他半導體材料

- 透過使用

- 一般照明

- 車

- 背光/顯示器

- 家用電子產品

- 工業/特殊照明

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ams-OSRAM AG

- Lumileds Holding BV

- Nichia Corporation

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Coherent Corp.

- San'an Optoelectronics Co., Ltd.

- ON Semiconductor Corporation

- Everlight Electronics Co., Ltd.

- Ennostar Inc.

- Brightek Optoelectronic Co., Ltd.

- Genesis Photonics Inc.

- Cree LED, an SGH Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states lED chips market size was valued at USD 6.70 billion in 2025 and estimated to grow from USD 7.17 billion in 2026 to reach USD 10.69 billion by 2031, at a CAGR of 8.32% during the forecast period (2026-2031).

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and More), Semiconductor Material (GaN/InGaN, Algainp, and More), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States LED Chips Market Trends and Insights

Escalating Adoption of Mini-LED Backlighting in High-End TVs

Sales momentum accelerated after the 2026 Consumer Electronics Show showcased mainstream 55-inch to 130-inch televisions equipped with thousands of red, green, and blue mini-LED emitters rather than white LEDs with color filters. Unit shipments for mini-LED TVs surpassed 20 million in 2026, lifting chip density requirements and pressuring domestic suppliers to tighten binning to sub-2-nanometer wavelength windows. Cost reductions of 20-30% logged during 2025 moved the technology from flagship to mid-tier models, widening the total addressable market for GaN emitters with forward-voltage spreads below 0.1 volts. In the United States LED chip market, the cumulative effect is a multi-year uplift, as television, monitor, and gaming hardware brands require higher volumes of tight-pitch chips. RGB mini-LED configurations eliminate quantum-dot layers in several designs, thereby capturing more of the system's value into the chip bill of materials. Domestic fabs that can guarantee high luminous-flux uniformity across wafer lots are therefore well positioned to win new display contracts.

Federal and State Energy Efficiency Incentives for Solid-State Lighting

Rebate programs covered a significant share of the United States' commercial floor space in 2026, and average prescriptive incentives rose across outdoor categories. Section 179D deductions deliver up to USD 5.36 per square foot, effectively shaving payback periods to below two years for high-efficacy luminaire retrofits in warehouses and cold-storage facilities. Utilities are migrating from flat-per-unit rebates to energy-savings performance models, favoring LED chips that help fixtures exceed 130 lumens per watt and qualify for DesignLights Consortium Premium listings. Oregon's 2025 fluorescent-lamp ban, followed by Hawaii's 2026 ban, further compresses legacy-lamp incentives and channels funding toward LED-to-LED upgrades with networked controls. These measures ensure that the United States LED chip market continues to absorb high volumes for troffer, outdoor, and high-bay fixtures over the next 24 months.

Supply Chain Bottlenecks in Silicon Carbide Substrates

Silicon-carbide crystal growth remains energy intensive, and the move to 200 mm wafers confronts yield losses that erode effective capacity. Competition from power-device makers siphons wafer allocations, as electric-vehicle inverters command higher margins than LED epitaxy. Import restrictions on specialty gases and seed crystals, together with regional industrial-policy frictions, add volatility to lead times for AEC-Q101-qualified parts. U.S. chipmakers hedge risk through multi-year wafer offtake agreements and co-development projects aimed at improving crystalline quality, yet smaller entrants lack negotiating leverage and face allocation rationing. Resulting supply tension trims growth potential for high-reliability automotive and industrial LEDs within the United States LED chips market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Decline in Per-Lumen Cost of High-Power GaN Chips

- Automotive OEM Pivot Toward Exterior LED Pixel Lighting

- High Capital Expenditure for Micro-LED Mass Transfer Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional emitters retained 83.45% of the United States LED chip market share in 2025, reflecting dominance in troffers, streetlights, and retrofit lamps. In parallel, mini-LED and micro-LED architectures expanded at an 11.28% CAGR, unlocking premium price points in television backlighting, adaptive headlights, and near-eye AR microdisplays. Vertical GaN is emerging as a bridge technology, doubling current handling per die, enabling fixture downsizing, and enhancing thermal performance in high-power modules.

The influx of RGB mini-LED backlights, each television integrating up to 30,000 dies, markedly boosts chip dollar-content even as per-lumen prices fall, effectively counterbalancing commoditization in general lighting. For micro-LEDs, mass-transfer hurdles remain, but pilot programs in defense avionics and premium wearables are validating reliability metrics. Domestic suppliers that combine wafer-level binning with proprietary quantum-dot-free color conversion are positioned to capture early design wins. Collectively, the coexistence of high-volume conventional LEDs and fast-growing micro-LED nodes diversifies revenue streams and insulates the United States LED chips market against single-segment cyclicality.

List of Companies Covered in this Report:

- ams-OSRAM AG

- Lumileds Holding B.V.

- Nichia Corporation

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Coherent Corp.

- San'an Optoelectronics Co., Ltd.

- ON Semiconductor Corporation

- Everlight Electronics Co., Ltd.

- Ennostar Inc.

- Brightek Optoelectronic Co., Ltd.

- Genesis Photonics Inc.

- Cree LED, an SGH Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Adoption of Mini-LED Backlighting in High-End TVs

- 4.2.2 Federal and State Energy Efficiency Incentives for Solid-State Lighting

- 4.2.3 Rapid Decline in Per-Lumen Cost of High-Power GaN Chips

- 4.2.4 Automotive OEM Pivot Toward Exterior LED Pixel Lighting

- 4.2.5 Growing Demand for UV-C LED Chips in Disinfection Systems

- 4.2.6 Emergence of Smart Farming Requiring Horticultural LED Arrays

- 4.3 Market Restraints

- 4.3.1 Supply Chain Bottlenecks in Silicon Carbide Substrates

- 4.3.2 High Capital Expenditure for Micro-LED Mass Transfer Equipment

- 4.3.3 Intellectual Property Litigation Risk Among Chipmakers

- 4.3.4 Thermal Management Challenges Limiting Chip Miniaturization

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams-OSRAM AG

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Nichia Corporation

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Epistar Corporation

- 6.4.8 Coherent Corp.

- 6.4.9 San'an Optoelectronics Co., Ltd.

- 6.4.10 ON Semiconductor Corporation

- 6.4.11 Everlight Electronics Co., Ltd.

- 6.4.12 Ennostar Inc.

- 6.4.13 Brightek Optoelectronic Co., Ltd.

- 6.4.14 Genesis Photonics Inc.

- 6.4.15 Cree LED, an SGH Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

日本LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)中國LED晶片市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區LED晶片:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)迷你LED晶片:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)LED晶片:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)北美LED晶片市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年

LED晶片市場規模、佔有率、趨勢和預測:按產品、應用和地區分類,2026-2034年 LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類

LED晶片市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、組件、最終用戶、設備、安裝類型分類 LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年

LED晶片市場-全球產業規模、佔有率、趨勢、機會、預測:按應用、類型、最終用戶、地區和競爭格局分類,2021-2031年