|

市場調查報告書

商品編碼

2072648

西班牙綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Spain Integrated Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

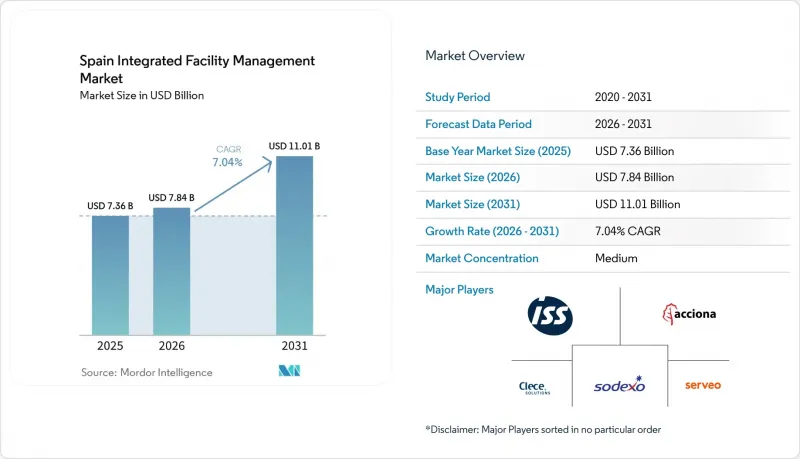

根據 Mordor Intelligence 預測,西班牙綜合設施管理市場規模預計將從 2025 年的 73.6 億美元成長到 2026 年的 78.4 億美元,並將從 2026 年到 2031 年以 7.04% 的複合年成長率成長,到 2031 年達到 10.1 億美元。

本報告按服務類型(硬性設施管理[資產管理、機電和暖通空調服務等]、軟性設施管理[辦公室支援和保全、清潔服務、餐飲服務等])和最終用戶(商業、旅館、機構/公共基礎設施、醫療保健等)進行細分。市場預測以美元計價。

西班牙整合性機構管理市場的趨勢與洞察

擴大非核心業務營運的外包

在西班牙的整合性機構管理市場,策略性外包已成為結構性營運模式。這是因為買家越來越要求將清潔、安保、餐飲、技術維護和職場支援等服務納入單一契約,並採用更簡化的管治結構。這種轉變不再只是為了降低成本。大規模租戶也希望減少與供應商的聯繫點,明確報告流程,並加強對分散地點服務品質的控制。中型企業也正在擺脫單一服務契約,這使得綜合服務提供者能夠獲得比以往外包週期更廣泛、更長的合約期限。公共部門也在推動這一趨勢,因為大規模合約越來越要求更強大的數位化工作流程、更清晰的績效證明以及公共設施服務交付的一致性。西班牙的「公共採購BIM計畫」提高了大規模公共專案供應商的資格要求,強制規定自2025年10月起,金額超過550萬歐元(620萬美元)的公共合約必須採用BIM技術。因此,在西班牙的綜合設施管理市場,那些兼具營運規模、合規能力和協調多項服務能力的公司,比那些僅以價格競爭的公司更受青睞。

節能建築的需求日益成長

能源效率正成為西班牙綜合設施管理市場的核心成長引擎。這是因為相關法規已將能源監控和最佳化作為標準合約要求,而不再只是可選附加服務。歐盟指令 (EU) 2024/1275 於 2024 年 5 月生效,西班牙必須在 2026 年 5 月前將其納入國內法。這為建築維修、控制系統和技術維護創造了合規主導的需求週期。西班牙國家建築維修計畫正是基於這項修訂後的指令制定,其政策框架包括到 2030 年和 2033 年維修能源效率最低的非住宅占地面積的里程碑,以及到 2050 年將非住宅建築的初級能源消耗降低 65% 的目標。西班牙也是歐盟智慧就緒指標試點成員國之一,進一步提升了建築自動化、資料檢驗和第三方效能認證在技術服務合約中的重要性。 2025年3月,ACCIONA Energia贏得了一份為期五年、價值560萬歐元(約630萬美元)的契約,負責馬德里市政府400多棟建築的能源管理。這表明,市政當局已經開始大規模地將這項工作外包。因此,隨著西班牙綜合設施管理市場進一步向能源主導採購模式轉變,能夠整合合規、測量、分析和營運交付的供應商更有可能贏得更多合約續約。

人事費用上升

人事費用壓力是西班牙綜合設施管理市場最明顯的短期阻礙因素,因為其最大的服務業仍嚴重依賴勞力密集的交付模式。軟性設施管理尤其脆弱,因為清潔、安保、餐飲和前台運營等服務通常以固定價格簽訂契約,即使在合約期間內工資成本上漲。西班牙的設施管理產業直接或間接支持超過60萬名員工,這意味著產業範圍內的工資協議和社會安全繳款會直接影響供應商的利潤率和競標策略。這種壓力也在改變投資重點,因為供應商正在加快清潔和監控等任務的自動化,以抵消多年合約中包含的薪資成長。西班牙的《殘障人士法》規定,員工人數超過50人的公司必須至少有2%的員工是殘障員工,這給大規模雇主增加了另一個合規負擔。因此,儘管西班牙的綜合設施管理市場持續成長,但定價、人員配置模式和合約條款正受到比以往外包週期更嚴格的審查。

細分市場分析

2025年,軟性設施管理(FM)在西班牙綜合設施管理(IFM)市場中佔62.53%。這反映了清潔、保全、餐飲和前台服務在公共、商業和醫療機構中的廣泛性和持續性。該細分市場之所以保持主導地位,是因為這些服務是西班牙租戶和公共機構最早外包的建築管理職能之一,並因此引起了經營團隊的關注。同時,安保服務正透過集中式警報接收模式和遠端監控不斷發展,為大型設施管理營運商提供了充足的空間來擴展員工隊伍並建立全國性的服務網路。這一歷史過程在2026年仍然至關重要,因為大規模買家仍然傾向於選擇以員工為基礎的捆綁式服務,這些服務可以快速部署到多個地點,而無需改變現有資產基礎。西班牙的《殘障人士法》也影響部分市場的採購行為,因為買家傾向於選擇擁有成熟員工體系和廣泛合規能力的成熟供應商。隨著經營團隊越來越重視職場品質和員工福祉,餐飲的重要性也日益突出。同時,保全服務正透過集中式警報接收模式和遠端監控不斷發展,從而減少了對純粹現場回應的需求。

預計到2031年,硬體維修)將以7.91%的複合年成長率成長,成為西班牙綜合設施管理(IFM)市場規模成長最快的細分領域。該細分領域具有結構性優勢,因為技術合規性、建築自動化和能源性能正日益成為一個統一的整體,而非各自獨立的支出項目。修訂後的《能源性能指令》(EPBD)和西班牙的維修計劃正在推動非住宅建築對資產管理、機電服務、消防和生命安全措施以及能源最佳化方面的需求不斷成長。受住宅、商業和工業應用中空氣和地熱能日益普及的推動,西班牙暖通空調(HVAC)產業在2025年實現了11.4%的成長。隨著裝機量的增加,未來對維護、診斷和效能檢驗的需求也將隨之成長。這種轉變強化了西班牙綜合設施管理(IFM)產業的技術層面,因為合規性、日益複雜的設備以及生命週期規劃正逐漸成為日常服務的一部分,而非偶爾的專案工作。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大非核心業務外包

- 節能建築的需求日益成長

- 智慧建築技術的普及

- 職場健康日益受到重視

- 歐盟分類法對ESG報告的壓力

- 引入人工智慧驅動的預測性維護

- 市場限制因素

- 人事費用上升導致通貨膨脹

- 供應商基礎在專業領域的細分

- 物聯網監控中的資料隱私問題

- 合格的暖通空調技術人員短缺

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按服務類型

- 硬設施管理

- 資產管理

- 機電及暖通空調服務

- 消防系統和安全措施

- 其他硬設施管理服務

- 軟設施管理

- 辦公室支援和安全

- 清潔服務

- 餐飲服務

- 其他設施管理服務

- 硬設施管理

- 按最終用戶行業分類

- 商業

- 飯店業

- 機構和公共基礎設施

- 衛生保健

- 工業和流程部門

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Acciona Facility Services SA

- ISS Facility Services Espana SA

- Sodexo Espana SA

- Clece SA

- Serveo Servicios Integrales SA

- Grupo Eulen SA

- Sacyr Facilities SLU

- Vinci Facilities Iberia SAU

- CBRE Group Inc.(Spain)

- JLL Spain

- Atalian Servest Iberia SAU

- Grupo Norte Agrupacion Empresarial de Servicios SA

- ENGIE Cofely Espana SLU

- OHL Servicios Ingesan SA

- Grupo SIFU

- Mitie Facilities Management Espana SL

- Johnson Controls Spain

- Ferrovial Servicios(Legacy Contracts)

- Altrad Rodisola SAU

- Seralia Facility Services SL

- Ilunion Facility Services SA

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain integrated facility management market size is expected to grow from USD 7.36 billion in 2025 to USD 7.84 billion in 2026 and is forecast to reach USD 11.01 billion by 2031 at 7.04% CAGR over 2026-2031.

This report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, and More], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and More]), and End User (Commercial, Hospitality, Institutional and Public Infrastructure, Healthcare, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Integrated Facility Management Market Trends and Insights

Growing Outsourcing of Non-Core Activities

Strategic outsourcing has become a structural operating model in the Spain integrated facility management market because buyers now want simpler governance across cleaning, security, catering, technical maintenance, and workplace support under one contract. The shift is no longer framed only around cost reduction, because large occupiers also want fewer vendor interfaces, tighter reporting lines, and stronger control over service quality across dispersed sites. Mid-sized companies are also moving beyond single-service contracts, which is helping integrated providers win broader scopes and longer terms than they did in earlier outsourcing cycles. Public administration is reinforcing this direction because larger contracts increasingly require stronger digital workflows, clearer performance evidence, and better delivery consistency across public estates. Spain's Plan BIM for Public Procurement made BIM compulsory for public contracts above EUR 5.5 million (USD 6.2 million) from October 2025, which raised the qualification threshold for suppliers seeking larger public assignments. As a result, the Spain integrated facility management market is rewarding operators that can combine operational scale, compliance capacity, and multi-service coordination rather than those that compete only on unit pricing.

Rising Demand for Energy-Efficient Buildings

Energy efficiency is becoming a core growth engine for the Spain integrated facility management market because regulation is turning energy monitoring and optimization into standard contract requirements rather than optional add-ons. Directive (EU) 2024/1275 entered into force in May 2024, and Spain must transpose it into national law by May 2026, which is creating a compliance-led demand cycle for building upgrades, control systems, and technical maintenance. Spain's National Building Renovation Plan is being developed under the recast directive, and the policy framework includes milestones to renovate the weakest-performing non-residential floor area by 2030 and 2033 while targeting a 65% reduction in primary energy use in non-residential buildings by 2050. Spain is also among the EU countries testing the Smart Readiness Indicator, which increases the relevance of building automation, data verification, and third-party performance evidence in technical service contracts. The March 2025 award to ACCIONA Energia for a 5-year EUR 5.6 million (USD 6.3 million) contract covering energy management across more than 400 Madrid City Council buildings shows that municipalities are already outsourcing this work at scale. Providers that can connect compliance, metering, analytics, and operational delivery are therefore likely to capture more renewals as the Spain integrated facility management market moves deeper into energy-led procurement.

High Labor Cost Inflation

Labor cost pressure is the clearest near-term constraint on the Spain integrated facility management market because its largest service areas still depend heavily on labour-intensive delivery models. Soft FM remains especially exposed, since cleaning, security, catering, and front-of-house services are often contracted at fixed prices even when wage obligations rise during the contract term. Spain's FM sector supports more than 600,000 workers directly and indirectly, which means sector-wide wage agreements and social contribution costs have an immediate effect on provider margins and bid discipline. This pressure is also changing investment priorities, because providers are accelerating automation in tasks such as cleaning and monitoring in order to offset the wage path built into multi-year contracts. Spain's General Disability Law adds another compliance layer for larger employers by requiring companies with 50 or more workers to maintain a 2% workforce quota for employees with disabilities. The result is that the Spain integrated facility management market is still growing, but price resets, staffing models, and contract terms are under much closer review than they were in earlier outsourcing cycles.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Smart Building Technologies

- EU Taxonomy Pressure on ESG Reporting

- Fragmented Supplier Base in Specific Trades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Soft Facility Management (FM) held 62.53% of the Spain integrated facility management (IFM) market share in 2025, reflecting the scale and recurrence of cleaning, security, catering, and front-of-house services across public, commercial, and healthcare estates. The segment remains dominant because these activities were among the first building functions that Spanish occupiers and public entities moved outside the organization, which drew greater management attention, while security services are evolving through centralized alarm reception models and remote supervision, giving large FM operators a long runway to build workforce depth and national coverage. That historical path still matters in 2026, because large buyers continue to prefer bundled labor-based services that can be rolled out quickly across many sites without changing the underlying asset base. Spain's General Disability Law also shapes procurement behavior in parts of the market, since buyers often favor established providers with mature workforce programs and broader compliance capacity. Catering is gaining added relevance as workplace quality and employee wellness receive more management attention, while security services are changing through centralized alarm reception models and remote supervision that reduce the need for purely site-bound coverage.

Hard FM is projected to expand at 7.91% CAGR, making it the fastest-growing part of the Spain IFM market size outlook through 2031. The segment is structurally advantaged because technical compliance, building automation, and energy performance are now rising together instead of as separate spending lines. The recast EPBD and Spain's renovation agenda are widening the need for asset management, mechanical and electrical services, fire and life safety work, and energy optimization across non-residential buildings. Spain's HVAC sector grew 11.4% in 2025, driven by aerothermal and geothermal adoption across residential, commercial, and industrial uses, and that larger installed base will need maintenance, diagnostics, and performance verification over time. This shift strengthens the technical side of the Spain integrated facility management industry because compliance, equipment complexity, and lifecycle planning are becoming part of everyday service delivery rather than occasional project work.

Complete Report Scope:

- By Service Type

- Hard Facility Management

- Asset Management

- MEP and HVAC Services

- Fire Systems and Safety

- Other Hard Facility Management Services

- Soft Facility Management

- Office Support and Security

- Cleaning Services

- Catering Services

- Other Facility Management Services

- Hard Facility Management

- By End User Industry

- Commercial

- Hospitality

- Institutional and Public Infrastructure

- Healthcare

- Industrial and Process Sector

- Other End-user Industries

List of Companies Covered in this Report:

- Acciona Facility Services S.A.

- ISS Facility Services Espana S.A.

- Sodexo Espana S.A.

- Clece S.A.

- Serveo Servicios Integrales S.A.

- Grupo Eulen S.A.

- Sacyr Facilities S.L.U.

- Vinci Facilities Iberia S.A.U.

- CBRE Group Inc. (Spain)

- JLL Spain

- Atalian Servest Iberia S.A.U.

- Grupo Norte Agrupacion Empresarial de Servicios S.A.

- ENGIE Cofely Espana S.L.U.

- OHL Servicios Ingesan S.A.

- Grupo SIFU

- Mitie Facilities Management Espana S.L.

- Johnson Controls Spain

- Ferrovial Servicios (Legacy Contracts)

- Altrad Rodisola S.A.U.

- Seralia Facility Services S.L.

- Ilunion Facility Services S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Outsourcing of Non-Core Activities

- 4.2.2 Rising Demand for Energy-Efficient Buildings

- 4.2.3 Expansion of Smart Building Technologies

- 4.2.4 Increasing Workplace Wellness Focus

- 4.2.5 EU Taxonomy Pressure on ESG Reporting

- 4.2.6 Deployment of AI-Enabled Predictive Maintenance

- 4.3 Market Restraints

- 4.3.1 High Labor Cost Inflation

- 4.3.2 Fragmented Supplier Base in Specialized Trades

- 4.3.3 Data-Privacy Concerns in IoT Monitoring

- 4.3.4 Shortage of Certified HVAC Technicians

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Hard Facility Management

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC Services

- 5.1.1.3 Fire Systems and Safety

- 5.1.1.4 Other Hard Facility Management Services

- 5.1.2 Soft Facility Management

- 5.1.2.1 Office Support and Security

- 5.1.2.2 Cleaning Services

- 5.1.2.3 Catering Services

- 5.1.2.4 Other Facility Management Services

- 5.1.1 Hard Facility Management

- 5.2 By End User Industry

- 5.2.1 Commercial

- 5.2.2 Hospitality

- 5.2.3 Institutional and Public Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Industrial and Process Sector

- 5.2.6 Other End-user Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Acciona Facility Services S.A.

- 6.4.2 ISS Facility Services Espana S.A.

- 6.4.3 Sodexo Espana S.A.

- 6.4.4 Clece S.A.

- 6.4.5 Serveo Servicios Integrales S.A.

- 6.4.6 Grupo Eulen S.A.

- 6.4.7 Sacyr Facilities S.L.U.

- 6.4.8 Vinci Facilities Iberia S.A.U.

- 6.4.9 CBRE Group Inc. (Spain)

- 6.4.10 JLL Spain

- 6.4.11 Atalian Servest Iberia S.A.U.

- 6.4.12 Grupo Norte Agrupacion Empresarial de Servicios S.A.

- 6.4.13 ENGIE Cofely Espana S.L.U.

- 6.4.14 OHL Servicios Ingesan S.A.

- 6.4.15 Grupo SIFU

- 6.4.16 Mitie Facilities Management Espana S.L.

- 6.4.17 Johnson Controls Spain

- 6.4.18 Ferrovial Servicios (Legacy Contracts)

- 6.4.19 Altrad Rodisola S.A.U.

- 6.4.20 Seralia Facility Services S.L.

- 6.4.21 Ilunion Facility Services S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球共消化設施市場報告全球設施管理服務市場:機會與策略展望(至2035年)

2026年全球共消化設施市場報告全球設施管理服務市場:機會與策略展望(至2035年) 日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)義大利綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)菲律賓綜合設施管理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)馬來西亞綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)印度綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國綜合設施管理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)