|

市場調查報告書

商品編碼

2072560

NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United Kingdom NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

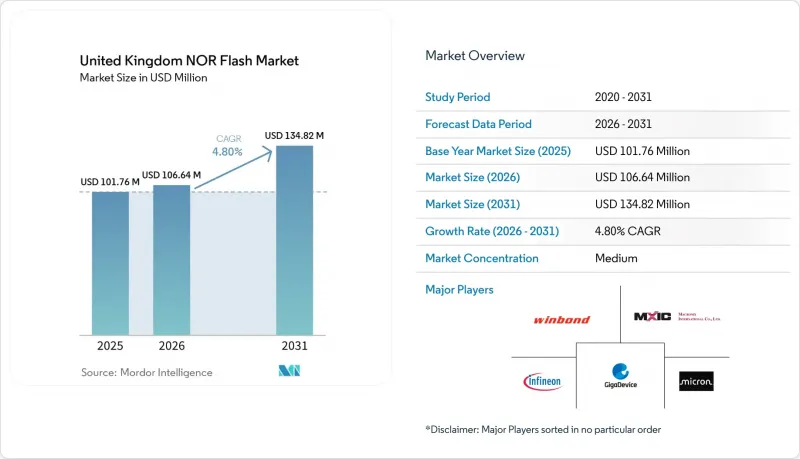

根據 Mordor Intelligence 預測,英國NOR 快閃記憶體市場將從 2026 年的 1.0664 億美元成長到 2031 年的 1.3482 億美元,2026 年至 2031 年的複合年成長率為 4.8%。

本報告按類型(串行NOR快閃記憶體、其他)、介面(四路SPI、其他)、容量(小於2兆位元、其他)、電壓(3V級、寬電壓、其他)、最終用戶應用(通訊、其他)、製程節點(45奈米、65奈米、其他)和封裝類型(QFN/SOIC、其他)進行細分。市場預測以價值(美元)和數量(單位)表示。

英國NOR快閃記憶體市場的趨勢與洞察

英國汽車製造商擴大採用ADAS和EV平台,這就需要即時啟動功能。

目前的汽車設計採用ADAS協議棧,從區域控制器、數位叢集和原地記憶體運行安全關鍵程式碼。英飛凌的ASIL-D認證SEMPER系列和華邦電子的W35T八進位系列是經過認證的裝置的典型例子,它們在-40 度C至+125 度C的溫度範圍內實現了400 MB/s的讀取頻寬。捷豹路虎因快閃記憶體組件短缺而在2026年中期停產,凸顯了供應的脆弱性,促使OEM廠商實施雙供應商採購並增加緩衝庫存。基於區域的電動車平台可以容納10到15個NOR插槽,是傳統數量的三倍多。這使得汽車產業成為英國NOR快閃記憶體市場最大的成長要素。

5G基礎設施的部署正在加速對通訊設備高可靠性程式碼儲存的需求。

Virgin Media O2 與愛立信和諾基亞合作的 7 億英鎊(8.89 億美元)升級預算,以及 Vodafone Three 承諾在南非地區實現 99% 的網路覆蓋,正在影響未來幾年的基地台擴建計劃。每個無線電單元都整合了 64 至 256 MB 的 NOR 閃存,用於儲存啟動代碼和補丁程序,旨在承受惡劣戶外環境下的運作循環。儘管由於監管方面的延誤,大約有 6200 份塔架建設許可證申請被擱置,導致安裝工作有所延遲,但採購計劃透明度的提高對於服務於英國NOR 閃存市場的代碼存儲供應商來說無疑是一大利好。

國內晶圓製造產能不足導致供應鏈出現脆弱性。

在英國,約有25家晶圓廠仍在採用180奈米以上的製程技術,迫使買家依賴進口來獲取所有先進的NOR快閃組件。國內先進NOR快閃記憶體組件產能的不足顯著增加了對外部供應商的依賴。海外的瓶頸進一步加劇了這種情況,預計到2026年,汽車級零件的前置作業時間將達到24週。因此,原始設備製造商(OEM)被迫維持相當於四個月的安全庫存,以應對供應鏈中斷。同時,紐波特正在進行的耗資2.5億英鎊(3.2億美元)的升級項目專注於碳化矽功率半導體,而非記憶體生產。因此,英國NOR快閃記憶體市場在結構上仍容易受到外部衝擊的影響。

細分市場分析

到2025年,串列裝置將佔據英國NOR快閃記憶體市場71.8%的主導地位。這一主導地位源於四路和八路總線的高效性,它們在保持首字節延遲的同時顯著縮小了PCB面積。並行NOR快閃記憶體由於其小於10奈秒的確定性存取時間,在航空電子和國防應用中繼續發揮至關重要的作用。然而,隨著串行頻寬達到400MB/s並成為具有競爭力的替代方案,其市佔率預計將會下降。此外,封裝技術的進步,特別是向WLCSP的轉變,正在推動串行NOR快閃記憶體進一步滲透到新興應用中。這些應用包括穿戴式裝置和物聯網節點,在這些應用中,緊湊高效的設計變得越來越重要。

這些趨勢也受到其他因素的進一步推動,這些因素放大了串列技術的優勢。汽車設計師透過將單端串行線路佈線到緊湊的線束中,減少了基板面積,簡化了設計並降低了成本。同時,工業OEM廠商也傾向使用串列NOR快閃記憶體,因為其元件數量較少,這有利於EMC合規性測試。這些趨勢正在推動各行各業在新設計中採用串列技術。因此,英國NOR快閃記憶體市場正日益向高速SPI生態系統轉型。這種轉變表明,串行NOR閃光存在滿足現代應用需求的重要性日益凸顯。

預計到 2025 年,四路 SPI 介面將佔總銷售額的 43.2%,而八路和 xSPI 介面預計到 2031 年將以 9.7% 的年均成長率成長。這一成長主要受 ADAS 網域控制器需求的不斷成長所驅動,這些控制器需要超過 200 MB/s 的讀取流才能高效運作。八路裝置具有顯著優勢,例如與四路裝置相比,隨機存取延遲降低了 40%,使其成為進階應用的首選。此外,這些裝置支援同時進行儲存體操作,這是實現無縫空中升級的關鍵特性。儘管具有這些優勢,但由於八路和 xSPI 介面依賴於微控制器的更新周期,它們的普及速度一直較為緩慢。然而,一級汽車零件供應商已經在檢驗xSPI 記憶體協定棧,並計劃將其整合到一項於 2027 年啟動的專案中。

傳統的單雙路SPI組件在消費性電子產品和公用事業收費計量表等對成本敏感的領域仍然發揮作用,因為價格是關鍵考慮因素。雖然這些組件有助於市場成長,但其過時的技術限制了其增值潛力。能夠抽象化匯流排寬度差異的軟體工具鏈正在加速向八進位介面的過渡,簡化製造商的轉型過程。因此,八進位介面有望成為下一代設計的標準選擇,尤其是在英國的NOR快閃記憶體市場。這種轉變反映了現代應用對更高效能和更高可靠性的日益成長的需求,而傳統的SPI組件無法充分滿足這些需求。八進制技術的應用有望重塑市場格局,並確保與不斷變化的設計要求相容。

到2025年,16兆位元(8Mb)頻寬將佔總支出的21.1%,這主要得益於工業和智慧型能源電錶領域對嵌入式控制器日益成長的需求。這些控制器對於這些應用的高效運作和能源管理至關重要。然而,成長動能正轉向1,28兆位元(64Mb)頻寬,預計同期成長率將達到7.3%。這一成長主要歸功於電動車閘道器的日益普及,這些閘道器需要高容量韌體和AI等待快取來支援高級功能。宏碁的ArmorBoot元件(512Mb至2GB)在為受網路安全法規約束的資產提供安全啟動解決方案方面發揮關鍵作用。這一趨勢正推動NOR快閃記憶體進入先前由NAND技術主導的應用領域。

低階2Mb及更小容量的快閃記憶體晶片因其尺寸小巧、效率高,在電源管理IC領域仍佔有一席之地。然而,晶片尺寸不斷縮小帶來的經濟挑戰正逐步降低供應商生產此類精細晶片的獲利能力,導致產量下降。同時,高階領域的技術進步正在開闢新的機會。堆疊式3D NOR技術的引進使得4Gb單晶片元件的開發成為可能。這些裝置非常適合對性能和可靠性要求極高的資訊娛樂系統和邊緣AI工作負載。這項技術進步顯著提升了英國NOR快閃記憶體市場的成長潛力,滿足了不斷成長的先進應用需求。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G基礎設施的部署正在加速對通訊設備高可靠性程式碼儲存的需求。

- 英國汽車製造商擴大採用 ADAS 和 EV 平台,這催生了對即時啟動功能的需求。

- 英國強制性的淨零能耗電費政策正在推動智慧電錶和物聯網技術的普及應用。

- 透過國防現代化計畫(TEMPEST、SkyNet 6)擴大安全 NOR 快閃記憶體的應用。

- 英國半導體設計稅收優惠政策(2023 年英國半導體策略)旨在促進本地原型設計。

- 英國製造的邊緣人工智慧模組向八進制/xSPI架構過渡

- 市場限制因素

- 國內晶圓製造能力不足導致供應鏈出現脆弱性。

- 低成本eMMC和高密度NAND解決方案之間的競爭日益激烈

- 28nm節點微影術設備高成本

- 英國脫歐使跨境半導體貿易的監管變得更加複雜。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 價格分析

第5章 市場規模與成長預測

- 按類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- 透過介面

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按密度

- 2兆位元或更少

- 4兆位元(2兆位元)

- 8兆位元(4兆位元)

- 16兆位元(8兆位元)

- 32兆位元(16兆位元)

- 64兆位元(32兆位元組)

- 128兆位元(64兆位元)

- 256兆位元(128兆位元)

- 超過 256 兆比特

- 透過電壓

- 3V級

- 1.8V 類

- 寬電壓範圍(1.65至3.6V)

- 1.8V 或更低電壓等級(1.2V、2.5V、5V)

- 透過最終用戶應用程式

- 家用電器

- 溝通

- 車

- 工業能源

- 其他

- 依製程技術節點

- 90奈米或以上

- 65nm

- 55nm

- 45nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 供應商定位分析

- 公司簡介

- Infineon Technologies AG

- Micron Technology Inc.

- Winbond Electronics Corp.

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corp.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan Xinxin Semiconductor Manufacturing Co. Ltd.

- Puya Semiconductor(Shanghai)Co. Ltd.

- Semiconductor Manufacturing International Corp.

- Adesto Technologies Corp.(a Dialog/Renesas Company)

- SMIC-Fabless UK Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom NOR flash market size is expected to increase from USD 106.64 million in 2026 to USD 134.82 million by 2031, growing at a CAGR of 4.8% over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (Quad SPI, and More), Density (2 Megabit and Less, and More), Voltage (3 V Class, Wide-Voltage, and More), End-User Application (Communication, and More), Process Technology Node (45 Nm, 65nm, and More), and Packaging Type (QFN/SOIC, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

United Kingdom NOR Flash Market Trends and Insights

Growing Adoption of ADAS and EV Platforms by UK OEMs Requiring Instant-Boot

Automotive designs now embrace zonal controllers, digital clusters, and ADAS stacks that run safety-critical code from execute-in-place memory. Infineon's ASIL-D qualified SEMPER line and Winbond's W35T octal family headline the approved device roster, enabling 400 MB/s read bandwidth within -40 °C to +125 °C envelopes. Jaguar Land Rover's mid-2026 production halt over missing flash parts underlined supply fragility, prompting OEMs to dual-source and raise buffer stock. Zone-based EV platforms can host 10-15 discrete NOR sockets, more than triple legacy counts, making automotive the single largest growth lever for the United Kingdom NOR Flash market.

5G Infrastructure Roll-Out Accelerating Demand for High-Reliability Code Storage in Telecom Gear

Virgin Media O2's GBP 700 million (USD 889 million) upgrade budget with Ericsson and Nokia, and Vodafone-Three's 99% SA coverage pledge create a multi-year base-station build-out pipeline. Each radio unit embeds 64-256 Mb NOR for boot code and patch storage that survives harsh outdoor duty cycles. Regulatory backlogs around 6,200 pending tower approvals delay installations but extend procurement visibility, benefiting code-storage suppliers serving the United Kingdom NOR Flash market.

Limited Domestic Wafer-Fab Capacity Leading to Supply-Chain Vulnerability

About 25 fabs in the UK continue to operate with geometries exceeding 180 nm, leading buyers to rely on imports for every advanced NOR part. The lack of domestic production capacity for advanced NOR Flash components has created a significant dependency on external suppliers. Offshore bottlenecks have further exacerbated the situation, with lead times for automotive-grade parts extending to 24 weeks in 2026. This has forced OEMs to maintain a safety stock for four months to mitigate supply chain disruptions. Meanwhile, an upgrade in Newport, costing GBP 250 million (USD 320 million), is focusing on SiC power instead of memory production. Consequently, the NOR Flash market in the UK remains structurally exposed to external shocks.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Smart Metering and IoT Deployments Under UK Net-Zero Mandate

- Shift Toward Octal/xSPI Architectures in Edge-AI Modules Manufactured in the UK

- Rising Competitiveness of Low-Cost eMMC and High-Density NAND Solutions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, serial devices claimed a dominant 71.8% share of the United Kingdom's NOR Flash market. This dominance is attributed to the efficiency of quad and octal buses, which have significantly reduced PCB area while maintaining first-byte latency. Parallel NOR continues to play a critical role in avionics and defense applications due to its deterministic sub-10 ns access. However, its market share is projected to decline as serial bandwidth reaches 400 MB/s, offering a competitive alternative. Additionally, advancements in packaging, particularly the transition to WLCSP, are further embedding serial NOR in emerging applications. These include wearables and IoT nodes, where compact and efficient designs are increasingly prioritized.

These trends are further bolstered by secondary effects that amplify the advantages of serial technology. Automotive designers are leveraging board savings by routing single-ended serial lines through compact harnesses, which simplifies design and reduces costs. At the same time, industrial OEMs are favoring serial NOR due to its lower component count, which proves advantageous during EMC compliance testing. These preferences are driving the adoption of serial technology in new designs across multiple industries. As a result, the United Kingdom's NOR Flash market is increasingly leaning towards high-speed SPI ecosystems. This shift underscores the growing importance of serial NOR in meeting the demands of modern applications.

In 2025, Quad SPI accounted for 43.2% of the revenue, while octal and xSPI interfaces are projected to grow at a rate of 9.7% through 2031. This growth is primarily driven by the increasing demand from ADAS domain controllers, which require read streams exceeding 200 MB/s to function efficiently. Octal devices offer significant advantages, including a 40% reduction in random-access latency compared to quad counterparts, making them a preferred choice for advanced applications. Additionally, these devices support simultaneous bank operations, a critical feature for enabling seamless over-the-air updates. Despite these benefits, the adoption of octal and xSPI interfaces has been slower due to their dependence on microcontroller refresh cycles. However, Tier-1 automotive suppliers are already validating xSPI memory stacks, targeting their integration into 2027 launch programs.

Legacy single and dual SPI components continue to play a role in cost-sensitive sectors, such as consumer electronics and utility meters, where affordability is a key consideration. These components contribute to market volume but offer limited potential for value growth due to their outdated technology. The transition to octal interfaces is being accelerated by software toolchains that abstract differences in bus width, simplifying the migration process for manufacturers. As a result, octal interfaces are expected to become the default boot path in next-generation designs, particularly in the UK NOR Flash market. This shift reflects the growing need for higher performance and reliability in modern applications, which legacy SPI components cannot adequately address. The adoption of octal technology is poised to redefine the market landscape, ensuring compatibility with evolving design requirements.

In 2025, the 16-Megabit-and-Less (More than 8 Mb) band accounted for 21.1% of spending, driven by the increasing demand for embedded controllers in industrial and smart-energy meters. These controllers are critical for enabling efficient operations and energy management in these applications. However, the growth trajectory is shifting towards the 128 Megabit and Less (More than 64 Mb) tier, which is projected to grow at a rate of 7.3% during the same period. This growth is primarily attributed to the rising adoption of EV gateways, which require larger firmware and AI weight caches to support advanced functionalities. Macronix's ArmorBoot components, ranging from 512 Mb to 2 GB, are playing a pivotal role by providing secure-boot solutions for cybersecurity-regulated assets. This development is pushing NOR Flash into application spaces that were previously dominated by NAND technology.

Low-end 2 Mb and smaller densities continue to find applications in power-management ICs, where their compact size and efficiency are advantageous. However, the economics of shrinking die sizes are gradually making these smaller geometries less viable for suppliers, leading to a reduction in their production. On the other hand, advancements at the higher end of the spectrum are opening new opportunities. The introduction of stacked 3D NOR technology is enabling the development of single-chip 4 Gb devices. These devices are well-suited for infotainment systems and edge-AI workloads, which demand high performance and reliability. This technological progress is significantly expanding the growth potential of the NOR Flash market in the United Kingdom, positioning it to meet the evolving demands of advanced applications.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less (More than 2 Mb)

- 8 Megabit and Less (More than 4 Mb)

- 16 Megabit and Less (More than 8 Mb)

- 32 Megabit and Less (More than 16 Mb)

- 64 Megabit and Less (More than 32 Mb)

- 128 Megabit and Less (More than 64 Mb)

- 256 Megabit and Less (More than 128 Mb)

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Sub-1.8 V Class (1.2 V, 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial and Energy

- Other Applications

- By Process Technology Node (Value)

- 90 nm and Above

- 65 nm

- 55 nm

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

List of Companies Covered in this Report:

- Infineon Technologies AG

- Micron Technology Inc.

- Winbond Electronics Corp.

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corp.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan Xinxin Semiconductor Manufacturing Co. Ltd.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Semiconductor Manufacturing International Corp.

- Adesto Technologies Corp. (a Dialog/Renesas Company)

- SMIC-Fabless UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G Infrastructure Roll-out Accelerating Demand for High-Reliability Code Storage in Telecom Gear

- 4.2.2 Growing Adoption of ADAS and EV Platforms by UK OEMs Requiring Instant-Boot

- 4.2.3 Expansion of Smart Metering and IoT Deployments Under UK Net-Zero Mandate

- 4.2.4 Defense Modernisation Programmes (Tempest, Skynet 6) Increasing Secure NOR Flash Uptake

- 4.2.5 Semiconductor Design Tax Incentives (UK Semiconductor Strategy 2023) Boosting Local Prototyping

- 4.2.6 Shift Toward Octal/xSPI Architectures in Edge AI Modules Manufactured in the UK

- 4.3 Market Restraints

- 4.3.1 Limited Domestic Wafer-Fab Capacity Leading to Supply-Chain Vulnerability

- 4.3.2 Rising Competitiveness of Low-Cost eMMC and High-Density NAND Solutions

- 4.3.3 High Photolithography Tooling Costs at 28 nm Nodes

- 4.3.4 Brexit-Induced Regulatory Complexity for Cross-Border Semiconductor Trade

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less NOR

- 5.3.2 4 Megabit and Less (More than 2 Mb)

- 5.3.3 8 Megabit and Less (More than 4 Mb)

- 5.3.4 16 Megabit and Less (More than 8 Mb)

- 5.3.5 32 Megabit and Less (More than 16 Mb)

- 5.3.6 64 Megabit and Less (More than 32 Mb)

- 5.3.7 128 Megabit and Less (More than 64 Mb)

- 5.3.8 256 Megabit and Less (More than 128 Mb)

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V-3.6 V)

- 5.4.4 Sub-1.8 V Class (1.2 V, 2.5 V, 5 V)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial and Energy

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Above

- 5.6.2 65 nm

- 5.6.3 55 nm

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Micron Technology Inc.

- 6.4.3 Winbond Electronics Corp.

- 6.4.4 Macronix International Co. Ltd.

- 6.4.5 GigaDevice Semiconductor Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corp.

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Wuhan Xinxin Semiconductor Manufacturing Co. Ltd.

- 6.4.11 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.12 Semiconductor Manufacturing International Corp.

- 6.4.13 Adesto Technologies Corp. (a Dialog/Renesas Company)

- 6.4.14 SMIC-Fabless UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)