|

市場調查報告書

商品編碼

2072556

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Germany NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

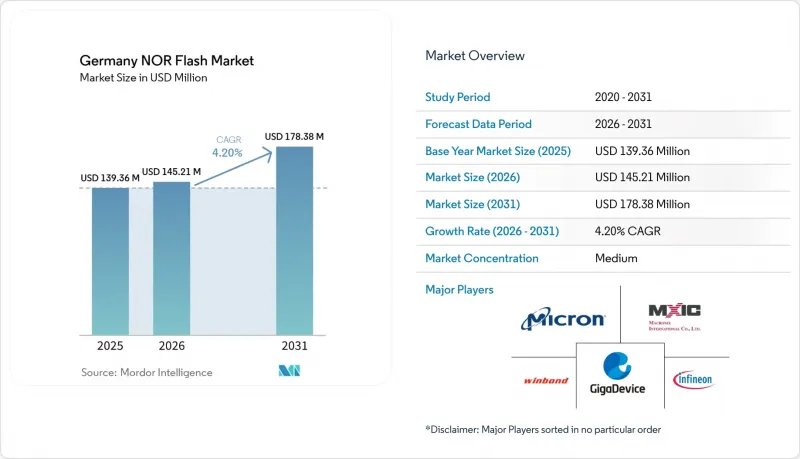

根據 Mordor Intelligence 預測,德國 NOR 閃光底片市場將從 2025 年的 1.3936 億美元成長到 2026 年的 1.4521 億美元,到 2031 年達到 1.7838 億美元,2026 年至 2031 年的複合年成長率為 4.20%。

本報告依NOR快閃記憶體類型(串列、平行)、介面(SPI單/雙等)、容量(2兆位元或以下等)、電壓(3V級等)、最終用戶應用(家用電子電器、通訊、其他)、製程節點(65奈米、45奈米、55奈米等)及封裝類型(WLCSP/CSP、其他)進行分類。市場預測以價值(美元)和銷售量(單位)表示。

德國NOR快閃記憶體市場的趨勢與洞察

韌體密集型 ADAS 和網域控制站正在加速對汽車 NOR 快閃記憶體的需求。

德國原始設備製造商 (OEM) 和一級供應商正從分散式電控系統 ( DECU) 轉向域和區域架構,這一轉變提高了每個汽車平臺所使用的外部代碼儲存容量。德國 NOR 快閃記憶體市場正受益於這一轉變,因為快速啟動、原地執行和可靠的韌體儲存仍然在安全至關重要的汽車系統中發揮核心作用。英飛凌將其汽車記憶體產品組合直接應用於進階駕駛輔助系統 (ADAS) 和自動駕駛的網域控制器設計。這些設計需要在系統級初始化之前實現快速啟動和可靠的韌體存取。這種設計模式限制了認證供應商的數量,使得認證供應商即使在整體記憶體價格走軟的情況下也能更容易維持價格。隨著運算功能在德國車輛架構中整合度的提高,每個控制器內的韌體密度持續成長,從根本上增強了對汽車級 NOR 組件的需求基礎。

德國製造地採用四路和八路 SPI 介面實現高速啟動物聯網邊緣設備

在德國工廠自動化領域,由於啟動延遲會直接導致生產中斷,感測器網路、閘道器和可程式控制器等設備正逐步採用更快的串列介面。德國NOR快閃記憶體市場也受惠於此轉變,工業邊緣設備中標準的SPI和雙I/O設備正被更高頻寬的四路SPI和八路解決方案所取代。華邦電子的W35T八路NOR閃存在200MHz DDR頻率下支援400MB/s的順序讀取吞吐量,專為需要即時啟動的工業工廠自動化和物聯網系統而設計。技嘉電子的GD25NX xSPI系列也推動了這一轉變,該系列採用1.8V核心和1.2V I/O設計,並降低了資源受限的邊緣節點對外部電源電路的需求。隨著德國機械製造商推動冗餘啟動代碼儲存和降低停機風險,八路和xSPI的應用正從小眾升級轉變為實際系統需求。

超過 256 Mb 的 NAND 快閃記憶體的成本差異限制了其在高密度消費產品中的應用。

細分市場分析

預計到2025年,串列NOR快閃記憶體將佔總銷售額的61.1%,顯示德國OEM廠商在緊湊型控制單元和工業邊緣設計上對低腳數記憶體有著強烈的偏好。在德國NOR快閃記憶體市場,串列NOR快閃記憶體預計到2031年將以5.2%的複合年成長率成長,超過整體市場成長率。其強勁的成長勢頭源於其與小型基板佈局的兼容性、低功耗以及易於整合到汽車和工業控制模組中。並行NOR閃存在基於平行總線MCU架構建構的舊式通訊和工業系統中繼續發揮至關重要的作用,這些系統在較長的運作內很少進行重新設計。

德國NOR快閃記憶體產業仍受到現有設備更新換代週期的影響,這導致即使新項目轉移到其他地方,傳統設備對平行方法的需求仍然存在。華邦電子和兆易半導體透過八進位和xSPI等變體推動了串列快閃記憶體的發展,這些變體在不改變基本串列架構配置的情況下提高了讀取頻寬。這種從標準串列介面轉向更快串列介面的內部轉變,使串行NOR快閃存在其現有部署基礎之外獲得了更大的發展動力。此外,由於同樣的成熟製程節點擴大應用於其他汽車和功率半導體產品,供應商必須謹慎管理該節點的產能。

到2025年,四路SPI介面將佔介面銷售額的50.4%,這反映了其與德國一級供應商廣泛使用的MCU和SoC系列產品的良好相容性。八路和xSPI介面是成長最快的介面,預計到2031年將以5.6%的複合年成長率成長,因為控制器頻寬需求持續成長。在德國NOR快閃記憶體市場,這種轉變與多域汽車控制器和工業邊緣設備密切相關,這些設備需要在不徹底改變記憶體架構的情況下實現更快的程式碼載入。此外,符合JEDEC xSPI標準將有助於供應商和OEM廠商使用熟悉的開發路徑遷移到八線裝置,從而降低遷移風險。

因此,德國NOR快閃記憶體產業並沒有放棄串行介面,而是在該框架內進行轉型。英飛凌的「SEMPER X1 LPDDR快閃記憶體」展示了這條轉型路徑的延伸,其頻寬專為下一代軟體定義車輛架構而設計,滿足高速資料存取和最大限度減少停機時間的需求。宏碁也透過其專注於xSPI的記憶體系列及其在汽車安全領域的定位,緊跟著這個發展方向,顯示廠商在介面藍圖上已達成廣泛共識。因此,儘管四路SPI仍然是目前的量產標準,但八路和xSPI正在日益塑造未來新設計的發展方向。

到2025年,16-32兆位元容量範圍將佔德國NOR快閃記憶體市場29.5%的銷售額,成為該市場最大的容量範圍。這一地位反映了其在車身控制模組、動力傳動系統控制器和工業邊緣閘道器等應用領域的適用性,這些應用的韌體映像目前仍主要採用此容量範圍。預計到2031年,128兆位元容量範圍將以5.7%的複合年成長率成長,因為曾經分散在各個模組中的軟體負載將被整合到域控制器、數位駕駛座系統和高性能工廠閘道器中。這種密度轉變是由程式碼量的整體成長、安全性更新的需求以及功能豐富的嵌入式系統的普及所驅動的。

256兆位元及以上容量的閃存在那些優先考慮「就地執行」性能和認證標準而非純粹成本效益的系統中也越來越受歡迎。低容量快閃記憶體仍廣泛應用於長壽命工業儀器設備和相對簡單的物聯網終端,儘管成長速度較為緩慢,但仍保持著重要的商業性地位。在德國NOR快閃記憶體市場,32兆位元容量的快閃記憶體仍然佔據著舉足輕重的地位,因為它在當前的汽車和工業生產項目中佔據了很大的佔有率。同時,隨著連網裝置對安全韌體映像、更新暫存和更長軟體支援週期的需求不斷成長,高容量產品的實用性也日益凸顯。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- ADAS 和網域控制站中韌體的大量使用正在加速對汽車 NOR(非調節器作業系統)的需求。

- 德國製造地在高速物聯網邊緣設備中採用 4 位元和 8 位元 SPI 介面

- 衛星群級低地球軌道衛星需要抗輻射NOR快閃記憶體元件

- 德國聯邦政府對「微電子」的津貼正在推動國內 55 奈米和 40 奈米 NOR(自然軌道)晶片的生產,目標是實現該技術的自給自足。

- 工業4.0工廠中的強制安全啟動和OTA更新

- 適用於穿戴式和即時醫療用電子設備的低功耗 1.8V 串行 NOR 閘

- 市場限制因素

- 容量超過 256 Mb 的 NAND 快閃記憶體成本溢價阻礙了高密度產品在消費者中的廣泛普及。

- 45奈米以下微型化的極限:引導德國OEM廠商制定MRAM與ReRAM替代技術藍圖

- 台灣代工廠的集中為德國一級供應商帶來了供應鏈中斷風險。

- 由於中國產能增加,平均售價(ASP)下降,影響了歐洲供應商的利潤率。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監管和技術展望

- 波特五力分析

- 價格分析

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- By Interface

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按密度

- 2兆位元或更少

- 2-4兆位元及以上

- 4 到 8 兆位元以上

- 8 至 16 兆位元及以上

- 16-32兆位元及以上

- 32-64兆位元及以上

- 64兆位元及以上至128兆比特

- 超過 128 兆比特到 256 兆比特

- 超過 256 兆比特

- 透過電壓

- 3 V級

- 1.8 V級

- 寬電壓範圍(1.65V 至 3.6V)

- 其他低於 1.8 V 的類別(1.2 V、2.5 V、5 V)

- 透過最終用戶應用程式

- 家用電子產品

- 溝通

- 車

- 產業

- 其他用途

- 依製程技術節點

- 90奈米或以上

- 65 nm

- 55奈米(包括58奈米)

- 45 nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他套餐

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Samsung Electronics Co. Ltd.

- Alliance Memory Inc.

- Zbit Semiconductor Inc.

- Puya Semiconductor Co. Ltd.

- Etron Technology Inc.

- XTX Technology Limited

- Jiangsu Ruichip Electronic Co. Ltd.

- Pujing Memory Co. Ltd.

- AMIC Technology Corp.

- Tower Semiconductor Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany NOR flash market size is expected to increase from USD 139.36 million in 2025 to USD 145.21 million in 2026 and reach USD 178.38 million by 2031, growing at a CAGR of 4.20% over 2026-2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, and More), End-User Application (Consumer Electronics, Communication, and More), Process Technology Node (65 Nm, 45 Nm, 55 Nm, and More), Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Germany NOR Flash Market Trends and Insights

Firmware-Intensive ADAS And Domain Controllers Accelerating Automotive-Grade NOR Demand

Germany's OEM and Tier-1 base is moving from distributed electronic control units toward domain- and zonal-architecture approaches, and that shift increases the amount of external code storage used on each vehicle platform. The Germany NOR flash memory market benefits from this transition because fast boot, execute-in-place operation, and dependable firmware storage remain central to safety-critical automotive systems. Infineon positions its automotive memory portfolio directly into ADAS and autonomous domain controller designs, where rapid startup and dependable firmware access are required before wider system initialization. This design pattern narrows the pool of qualified suppliers, helping certified vendors defend pricing even when broader memory pricing softens. As German vehicle architectures consolidate compute functions, firmware density continues to rise within each controller, which supports a structurally firmer demand base for automotive-grade NOR parts.

Quad And Octal SPI Adoption For Fast-Boot IoT Edge Devices Across German Manufacturing Hubs

Germany's factory automation base is adopting faster serial interfaces because boot delays translate directly into production interruptions in sensor networks, gateways, and programmable controllers. The German NOR flash memory market is gaining from this shift as standard SPI and dual I/O devices give way to higher-bandwidth quad SPI and octal solutions in industrial edge equipment. Winbond's W35T octal NOR supports 400 MB/s continuous read throughput at 200 MHz DDR and is positioned for industrial factory automation and IoT systems that need instant-on behavior. GigaDevice also moved this transition forward with its GD25NX xSPI line, which combined a 1.8 V core and 1.2 V I/O design to reduce the external power circuitry requirements in constrained edge nodes. As German machine builders push for redundant boot-code storage and lower downtime risk, octal and xSPI adoption is moving from a niche upgrade to a practical system requirement.

Cost premium over NAND above 256 Mb limiting high-density consumer adoption

Other drivers and restraints analyzed in the detailed report include:

- Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- Bundesregierung Mikroelektronik Funding Driving 55 Nm And 40 Nm On-Shore Production For NOR Self-Sufficiency

- Scaling ceilings beyond 45 nm steering German OEM roadmaps toward MRAM/ReRAM substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR flash held 61.1% of revenue in 2025, and that lead shows how strongly German OEMs prefer low pin-count memory for compact control units and industrial edge designs. In the German NOR flash memory market, serial NOR flash is also expected to grow at a 5.2% CAGR through 2031, which keeps it ahead of overall market growth. This strength comes from compatibility with smaller board layouts, lower power draw, and easier integration into automotive and industrial control modules. Parallel NOR flash still matters in older telecommunications and industrial systems that were built around parallel-bus MCU architectures and are rarely redesigned during long operating lives.

The German NOR flash memory industry is still influenced by installed-base replacement cycles, and that helps sustain parallel demand in legacy equipment even as new programs move elsewhere. Winbond and GigaDevice have both pushed the serial category forward through octal and xSPI variants that raise read bandwidth without changing the basic serial architecture path. That internal migration from standard serial interfaces to faster serial interfaces gives serial NOR an extra layer of momentum beyond its installed base. It also means suppliers must manage node capacity carefully because the same mature process nodes are increasingly used across other automotive and power semiconductor products.

Quad SPI accounted for 50.4% of interface revenue in 2025, reflecting its broad compatibility with the MCU and SoC families widely used by German Tier-1 suppliers. The fastest interface growth comes from octal and xSPI, projected to grow at a 5.6% CAGR through 2031 as controller bandwidth needs continue to rise. In the German NOR flash memory market, this change is tied to multi-domain vehicle controllers and industrial edge devices that need faster code loading without a full memory architecture change. JEDEC xSPI compliance also reduces migration risk by helping suppliers and OEMs move toward 8-line devices with a familiar development path.

The German NOR flash memory industry is therefore shifting inside the serial category rather than abandoning it. Infineon's SEMPER X1 LPDDR flash shows how far that path can go, with bandwidth designed for next-generation software-defined vehicle architectures that require rapid data access and minimal downtime. Macronix has also aligned with this direction through its xSPI-oriented memory family and automotive safety positioning, indicating broad vendor agreement on the interface roadmap. The practical outcome is that quad SPI remains the current volume standard, while octal and xSPI increasingly define where new design wins are heading.

The 16-32 megabit tier accounted for 29.5% of revenue in 2025, making it the largest density bracket in the German NOR flash memory market. That position reflects its fit with body control modules, powertrain controllers, and industrial edge gateways, where firmware images still sit comfortably within that range. The 128 megabit tier is projected to grow at a 5.7% CAGR through 2031 as domain controllers, digital cockpit systems, and more capable factory gateways combine software loads that were once spread across separate modules. This density shift follows the broader rise in code volume, secure update staging, and feature-rich embedded systems.

The 256 megabit and above categories are also gaining traction in systems where execute-in-place performance and certification standards matter more than raw cost efficiency. Lower-density tiers continue to serve long-life industrial instrumentation and simpler IoT endpoints, making them commercially relevant even if growth is modest. The German NOR flash memory market for the 32 megabit tier remains important because it accounts for a large share of current automotive and industrial production programs. At the same time, larger densities are becoming more practical as connected devices require more room for secure firmware images, update staging, and longer software support windows.

Complete Report Scope:

- By Type (Value and Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Other Sub-1.8 V Classes (1.2 V, 2.5 V, 5 V)

- By End-User Application (Value and Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packages

List of Companies Covered in this Report:

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Samsung Electronics Co. Ltd.

- Alliance Memory Inc.

- Zbit Semiconductor Inc.

- Puya Semiconductor Co. Ltd.

- Etron Technology Inc.

- XTX Technology Limited

- Jiangsu Ruichip Electronic Co. Ltd.

- Pujing Memory Co. Ltd.

- AMIC Technology Corp.

- Tower Semiconductor Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Firmware-Intensive ADAS and Domain Controllers Accelerating Automotive-Grade NOR Demand

- 4.2.2 Quad and Octal SPI Adoption for Fast-Boot IoT Edge Devices across German Manufacturing Hubs

- 4.2.3 Constellation-Scale LEO Satellites Requiring Radiation-Hardened NOR Flash Devices

- 4.2.4 Bundesregierung "Mikroelektronik" Funding Driving 55 nm and 40 nm On-Shore Production for NOR Self-Sufficiency

- 4.2.5 Secure Boot and OTA-Update Mandates in Industrie 4.0 Factories

- 4.2.6 Low-Power 1.8 V Serial NOR Enabling Wearable and Point-of-Care Healthcare Electronics

- 4.3 Market Restraints

- 4.3.1 Cost Premium over NAND above 256 Mb Limiting High-Density Consumer Adoption

- 4.3.2 Scaling Ceilings beyond 45 nm Steering German OEM Roadmaps toward MRAM and ReRAM Substitutes

- 4.3.3 Foundry Concentration in Taiwan Exposing Supply-Chain Disruption Risk for German Tier-1s

- 4.3.4 ASP Compression from Expanding Chinese Capacity Impacting Vendor Margins in Europe

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type (Value and Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Other Sub-1.8 V Classes (1.2 V, 2.5 V, 5 V)

- 5.5 By End-User Application (Value and Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and More

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packages

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Micron Technology Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Samsung Electronics Co. Ltd.

- 6.4.11 Alliance Memory Inc.

- 6.4.12 Zbit Semiconductor Inc.

- 6.4.13 Puya Semiconductor Co. Ltd.

- 6.4.14 Etron Technology Inc.

- 6.4.15 XTX Technology Limited

- 6.4.16 Jiangsu Ruichip Electronic Co. Ltd.

- 6.4.17 Pujing Memory Co. Ltd.

- 6.4.18 AMIC Technology Corp.

- 6.4.19 Tower Semiconductor Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis

東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)