|

市場調查報告書

商品編碼

2072554

東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)South East Asia NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

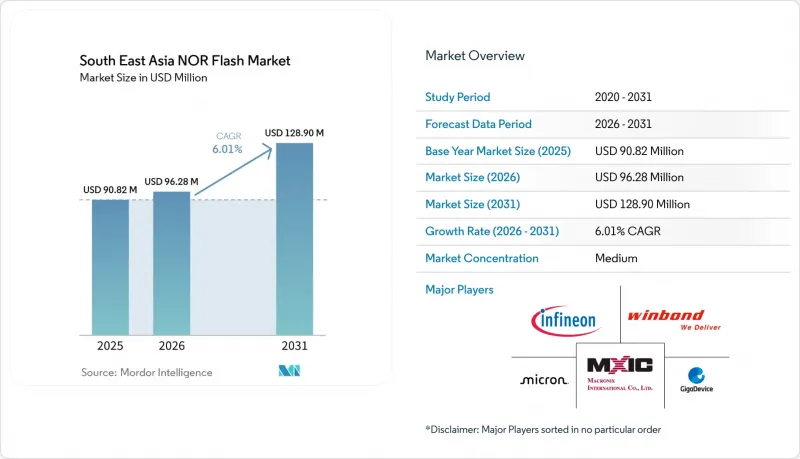

根據 Mordor Intelligence 預測,東南亞 NOR 閃光底片市場規模將從 2025 年的 9,082 萬美元成長到 2026 年的 9,628 萬美元,然後在 2031 年達到 1.289 億美元,2026 年至 2031 年的複合成長率為 6.01%。

本報告依NOR快閃記憶體類型(串列、平行)、介面(SPI單/雙介面、其他)、容量(2兆位元以下、其他)、電壓(3V級、1.8V、其他)、最終用戶應用(通訊、其他)、製程節點(65nm、45nm、其他)及封裝類型(WLCSP/CSP、其他)進行分類。市場預測以價值(美元)和數量(單位)表示。

東南亞NOR快閃記憶體市場趨勢與洞察

政府主導的獎勵正在推動電子製造業的擴張。

政府政策是推動東南亞NOR快閃記憶體市場短期需求的最顯著因素之一。這是因為獎勵政策正在吸引更多組裝、封裝和電子製造項目落腳該地區。越南第33/2025/TT-BKHCN號通知規定了電子製造商享有稅收優惠的四項資格標準,包括使用在越南設計或製造的半導體,以及供應鏈中國內採購率達到30%或以上,從而促進了晶片產品中在地採購組件比例的提高。柔佛-新加坡經濟特區於2025年1月啟動,為符合條件的電子和半導體企業提供長達15年的5%企業所得稅優惠,使其對希望在OEM設計和組裝工廠附近設立基地的供應商越來越有吸引力。泰國國家半導體藍圖旨在25年內培養超過23萬名高技能工人,顯示泰國將半導體能力視為長期產業發展重點,而非短期政策議題。馬來西亞的「新獎勵框架」於2026年3月1日生效,該框架重組了其製造業支援體系,重點關注電子、半導體封裝和精密工程。這擴大了使用代碼儲存和啟動記憶體的工廠的基礎設施。這些框架縮短了一級原始設備製造商(OEM)的位置決策時間,同時擴大了部署電子生產線的基礎設施,從而為NOR快閃記憶體創造直接且持續的需求。

該地區汽車電子產業叢集的形成與發展

隨著智慧駕駛座、ADAS(高級駕駛輔助系統)、電動車電源管理和OTA軟體的普及,可靠的韌體儲存需求日益成長,汽車電子產業叢集正在推動東南亞NOR快閃記憶體市場的擴張。 2025年9月,多碼電子(MCE)與惠州福友通用電子簽署了一項製造和開發協議,旨在推動東協地區駕駛座域控制器和聯網汽車技術的在地化。為此,MCE計劃在製造地附近投資1.5億至2億馬幣(約3400萬至4500萬美元)。 VinFast的目標是到2025年實現電動車在地化率超過60%,到2026年達到84%,這意味著需要採購更多用於ECU(電子控制單元)和電池管理系統的車規級記憶體。馬來西亞也擁有結構性優勢,其半導體出口基地和汽車研發工作在馬來西亞汽車與機器人物聯網實驗室(MARI)支持的國家計劃下匯聚。實際上,這意味著該地區許多汽車專案正在從基本的儲存需求轉向符合安全標準的裝置,這些裝置需要更高的可靠性和資料保持性能。這種轉變提高了市場進入門檻,減少了認證供應商的數量,並推動了東南亞NOR快閃記憶體市場高價值產品的成長。

過度依賴位於東南亞以外的鑄造廠

東南亞NOR快閃記憶體市場最大的結構性限制在於,儘管該地區NOR快閃記憶體消費量龐大,但卻無法掌控生產NOR快閃記憶體的晶圓製造地。東南亞仍面臨晶圓廠產能持續短缺的問題,儘管該地區努力建構更完善的半導體生態系統,但晶片製造仍集中在中國大陸和台灣地區。在中國,資源配置早期轉向成熟邏輯節點的擴張已經給NOR快閃生產帶來了壓力,導致越南和馬來西亞等國的組裝商面臨供應緊張的局面。 2026年1月宣布的美台貿易投資協定將把台灣2,500億美元的半導體投資轉移到美國,這進一步強化了人們的預期,即大規模向東南亞轉移上游工藝晶圓廠產能的可能性不大。由於獲得認證的NOR快閃供應商數量有限,在資源緊張的情況下,當地製造商難以實現供應鏈多元化。因此,在預測期的大部分時間裡,東南亞NOR快閃記憶體市場將極易受到地緣政治衝擊和供應商優先決策的影響。

細分市場分析

2025年,串列NOR快閃記憶體的銷售額佔比達到62.1%,同年在東南亞NOR快閃記憶體市佔率也達到62.1%。此外,預計從2026年到2031年,串行NOR快閃記憶體的複合年成長率(CAGR)將達到7.5%,在所有產品類型中位居榜首,顯示其主導地位不僅沒有減弱,反而更加穩固。該細分市場與區域製造地緊密相關,因為SPI連接、更少的引腳數量和緊湊的基板要求與消費性電子產品、通訊設備以及各種工業產品中使用的大量微控制器設計相契合。此外,原地執行能力減少了對影子RAM的需求,從而緩解了材料清單(BOM)成本壓力,而成本控制在產品架構中至關重要。 2026年,華邦電子將持續拓展藍圖,這些產品將採用高速介面和低功耗外形外形規格,以滿足此市場需求。

因此,在東南亞NOR快閃記憶體市場,串列NOR快閃記憶體無需進行重大設計變更,即可應用於大規模生產的消費級平台和新型邊緣裝置。穿戴式裝置、Wi-Fi模組、物聯網終端和智慧家庭設備均受益於該系列產品的空間效率和標準化的控制器相容性。因此,除非特定頻寬或舊有系統要求另有規定,否則東南亞NOR快閃記憶體產業仍將串行NOR快閃記憶體作為大多數新設計的預設選擇。平行NOR快閃記憶體仍然發揮作用,但其應用主要限於較舊的工業控制器、汽車顯示器以及需要頻繁啟動且寬匯流排仍然具有實際應用價值的系統。英飛凌和華邦電子提供的車規級平行產品在ECU和資訊娛樂平台領域保持著穩固的利基市場,即使到了2024年,這些平台仍然需要這種架構。東南亞NOR快閃記憶體市場的長期發展方向仍然明確地聚焦於串列產品。這是因為該地區的大多數新組裝項目都優先考慮緊湊的佈局、更少的引腳數和易於平台復用。

到2025年,四路SPI將佔據最大的介面銷售佔有率,達到44.8%,這反映出其在主流電子組裝領域的廣泛應用。預計從2026年到2031年,八路和xSPI將以7.7%的複合年成長率成長,顯示隨著處理器和汽車系統對更高讀取頻寬的需求不斷變化,性能要求也在穩步提升。這種市場格局清晰地反映了東南亞NOR快閃記憶體市場的現狀,即傳統的大規模生產和前瞻性的新設計項目以不同的速度推進。四路SPI仍然根基穩固,因為許多現有的微控制器平台已經支援它,並且在通訊模組和消費產品中擁有龐大的應用基礎。因此,即使工程團隊正在為更快的標準做準備,四路SPI仍保持著強勁的市場需求。

在東南亞NOR快閃記憶體市場,隨著即時程式碼執行在汽車處理器、AI控制器和高效能嵌入式系統中日益普及,八進位SPI和xSPI正逐漸佔據市場主導地位。英飛凌的SEMPER產品組合支援八進位SPI和HYPERBUS,其耐用性和資料保持特性針對工業和汽車應用進行了最佳化,這表明介面升級已能滿足嚴苛的應用需求。意法半導體在其最新的STM32N系列裝置中也支援8位元和16位元XSPI配置,這進一步印證了控制器生態系統在建置時已充分考慮了xSPI的支援。單通道和雙通道SPI在低成本藍牙模組、物聯網感測器和入門級穿戴式裝置中仍然至關重要,尤其是在越南和印尼等對成本高度敏感的市場。然而,平台設計的方向已經明確,在東南亞NOR快閃記憶體市場,能夠同時支援大規模四通道SPI平台和向八進制及xSPI遷移路徑的供應商將越來越受到重視。

到2025年,32-64兆位元容量的快閃記憶體將佔東南亞NOR快閃記憶體市場總銷量的27.7%,成為該地區最大的容量等級。這項頻寬與主流Wi-Fi晶片、藍牙SoC、智慧電錶以及眾多中低價位穿戴裝置的韌體需求高度契合,也解釋了其在主要組裝廠的銷售優勢。此外,此容量等級還具有產品線豐富、採購前置作業時間短的優勢,這對於庫存量極低的製造商至關重要。從這個意義上講,該容量等級佔據了東南亞NOR快閃記憶體市場部署基礎的大部分,並在消費和通訊領域的需求週期中保持了市場的穩定。與專業終端應用相比,此容量等級與日常電子設備的生產連結最為緊密。

容量超過 256 兆位元的高階快閃記憶體市場預計將在 2026 年至 2031 年間以 7.3% 的複合年成長率成長,成為成長最快的容量範圍。其主要驅動力是對人工智慧伺服器的需求。基於 GB200 的機架需要比傳統機架多得多的 NOR 快閃記憶體元件,這促使資源重新分配到更高容量的元件上。宏碁已宣布計劃在 2026 年下半年提供 3D NOR 快閃記憶體元件樣品,目標是在 2027 年開始量產。這代表了業界對傳統 2D NOR 結構容量限制的直接回應。 8 兆位元至 32 兆位元的中等容量範圍對於物聯網和攜帶式診斷設備仍然至關重要,而 128 兆位元至 256 兆位元的範圍則支援網路設備、安全存取設備和汽車子系統。這在東南亞NOR快閃記憶體市場形成了多層次的需求模式,單一容量系列無法滿足所有成長細分市場的需求。此外,鑑於消費者購買週期、基礎設施擴容和人工智慧主導的資源分配壓力等因素會導致需求波動,這意味著同時涵蓋主流和高容量節點的供應商在滿足市場需求方面具有優勢。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府主導的激勵措施,旨在促進電子製造業的擴張。

- 該地區汽車電子產業叢集的形成與發展

- 穿戴式裝置和照護現場設備製造外包趨勢日益明顯。

- 加速5G和FTTH網路基礎設施的部署

- 全球一級原始設備製造商的供應鏈回流計劃

- 邊緣人工智慧微控制器對 NOR 快閃記憶體的需求正在激增。

- 市場限制因素

- 過度依賴東南亞以外的鑄造廠

- 來自中國供應商的成本競爭力對利潤率造成了越來越大的壓力。

- 新興的非揮發性儲存技術的應用日益廣泛

- 20奈米及以下微影術熟練工人長期短缺

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監管和技術展望

- 波特五力分析

- 價格分析

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- 透過介面

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按產能

- 2兆位元或更少

- 2-4兆比特

- 4-8兆比特

- 8-16兆比特

- 16-32兆比特

- 32-64兆比特

- 64-128兆比特

- 128-256兆比特

- 超過 256 兆比特

- 透過電壓

- 3V級

- 1.8V 類

- 寬電壓範圍(1.65 至 3.6 V)

- 其他 - 1.2V 級及類似的 1.8V 或更低電壓(2.5V、5V 等)

- 透過最終用戶應用程式

- 家用電子產品

- 溝通

- 車

- 產業

- 其他終端用戶應用程式

- 依製程技術節點

- 90奈米或以上

- 65nm

- 55奈米(包括58奈米)

- 45nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他

- 按地區

- 越南

- 印尼

- 菲律賓

- 泰國

- 馬來西亞

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Puya Semiconductor(Shanghai)Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- AMIC Technology Corporation(NEW)

- AP Memory Technology Co. Ltd.(NEW)

- Yangtze Memory Technologies Co. Ltd.(YMTC)

第7章 市場機會與未來展望

According to Mordor Intelligence, the south east asia NOR flash market size is expected to grow from USD 90.82 million in 2025 to USD 96.28 million in 2026 and is forecast to reach USD 128.90 million by 2031 at 6.01% CAGR over 2026-2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, 1. 8V, and More), End-User Application (Communication, and More), Process Technology Node (65 Nm, 45 Nm, and More), and Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

South East Asia NOR Flash Market Trends and Insights

Government-Led Incentives Driving Expansion In Electronics Manufacturing

Government policy has become one of the clearest near-term demand supports for the Southeast Asia NOR Flash Memory market because incentive programs are drawing more assembly, packaging, and electronics manufacturing projects into the region. Vietnam's Circular 33/2025/TT-BKHCN set four eligibility criteria for tax relief for electronics manufacturers, including the use of Vietnam-designed or manufactured semiconductors and at least 30% domestic supply-chain participation, which encourages more localized component sourcing around chip-based products. The Johor-Singapore Special Economic Zone launched in January 2025 and offers a 5% corporate tax rate for qualifying electronics and semiconductor operations for up to 15 years, which improves the case for suppliers that want to stay close to OEM design and assembly centers. Thailand's national semiconductor roadmap targets more than 230,000 highly skilled personnel over a 25-year period, showing that the country is treating semiconductor capability as a long-cycle industrial priority rather than a short policy window. Malaysia's New Incentive Framework became operational on March 1, 2026, and reshaped manufacturing support around electronics, semiconductor packaging, and precision engineering, which broadens the base of plants that consume code storage and boot memory. As these frameworks shorten location decisions for Tier-1 OEMs, they increase the installed base of electronics production lines that generate direct and repeat NOR Flash demand.

Formation And Growth Of Automotive Electronics Clusters In The Region

Automotive electronics clusters are driving the Southeast Asia NOR Flash Memory market higher, as every move toward smart cockpits, ADAS, EV power management, and OTA software increases demand for reliable firmware storage. Multi-Code Electronics and Huizhou Foryou General Electronics signed a manufacturing and development agreement in September 2025 to localize cockpit domain controllers and connected-vehicle technology across ASEAN, with MCE investing RM150 million to RM200 million (USD 34 million to USD 45 million) near Perodua's manufacturing hub. VinFast reached more than 60% EV localization in 2025 and is targeting 84% by 2026, implying increased procurement of automotive-grade memory for ECUs and battery management systems. Malaysia also has a structural advantage because its semiconductor export base and automotive development agenda are converging under national policies supported by the Malaysia Automotive, Robotics and IoT Institute. In practice, this means more vehicle programs in the region are moving from basic memory needs toward safety-qualified devices with stronger reliability and retention requirements. That shift raises entry barriers, concentrates approved vendor lists, and supports higher-value content in the Southeast Asia NOR Flash Memory market.

Heavy Dependence On Foundries Located Outside South East Asia

The biggest structural constraint on the South East Asia NOR Flash Memory market is that the region consumes large volumes of NOR Flash but does not control the wafer fabrication base that produces it. South East Asia still faces a persistent fab gap, with chipmaking concentrated in China and Taiwan even as the region tries to build a deeper semiconductor ecosystem. Earlier allocation shifts in China toward mature logic node expansion have already put pressure on NOR Flash output, tightening supply for assemblers in countries such as Vietnam and Malaysia. U.S.-Taiwan trade and investment commitments announced in January 2026 directed USD 250 billion in Taiwanese semiconductor investment toward the United States, reinforcing the view that new upstream fab capacity is not moving to Southeast Asia at scale. Because the qualified supplier base in NOR Flash is narrow, local manufacturers cannot easily diversify when allocation is tight. This leaves the Southeast Asia NOR Flash Memory market exposed to geopolitical shocks and supplier prioritization decisions for most of the forecast period.

Other drivers and restraints analyzed in the detailed report include:

- Rising Trend Of Outsourcing In Wearable And Point-Of-Care Device Manufacturing

- Accelerated Deployment Of 5G And Fiber-To-The-Home Network Infrastructure

- Intensified Margin Pressures From Cost-Competitive Chinese Vendors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR Flash accounted for 62.1% of revenue in 2025, representing 62.1% of the South East Asia NOR Flash market share that year. It also posted the fastest projected CAGR among type segments at 7.5% for 2026-2031, showing that leadership is being reinforced rather than eroded. The segment aligns with the regional manufacturing base because SPI connectivity, lower pin counts, and compact board requirements match the microcontroller-heavy designs used in consumer electronics, communications equipment, and a broad range of industrial products. Execute-in-place capability also reduces the need for shadow RAM, which keeps bill-of-materials pressure under control in a region where cost discipline shapes product architecture. In 2026, Winbond continues to extend its higher-density serial NOR and automotive-grade product roadmap, with faster interfaces and low-power form factors that align with this demand pattern.

The practical outcome is that serial NOR serves both high-volume consumer platforms and newer edge devices without forcing major design changes across the Southeast Asia NOR Flash Memory market. Wearables, Wi-Fi modules, IoT endpoints, and smart appliances all benefit from the segment's space efficiency and standardized controller compatibility. That is why the Southeast Asia NOR Flash Memory industry continues to treat serial NOR as the default option for most new designs unless a specific bandwidth or legacy system condition points elsewhere. Parallel NOR Flash still has a role, but it is mostly tied to older industrial controllers, automotive displays, and boot-intensive systems where a wider bus remains operationally useful. Automotive-grade parallel offerings from Infineon and Winbond preserved a protected niche in 2024 for ECUs and infotainment platforms that still require that architecture. Even so, the long-term direction of the Southeast Asia NOR Flash Memory market remains clearly aligned with serial products, as most new regional assembly programs prioritize compact layouts, lower pin count, and easier platform reuse.

Quad SPI held the largest interface revenue share at 44.8% in 2025, reflecting its wide installation base across mainstream electronics assembly. Octal and xSPI are forecast to grow at the fastest CAGR of 7.7% from 2026 to 2031, indicating a steady shift in performance requirements as processors and vehicle systems demand higher read bandwidth. This split captures the current shape of the South East Asia NOR Flash market, where legacy volume and forward-looking design wins are moving at different speeds. Quad SPI remains deeply embedded because many existing microcontroller platforms already support it, and the installed base across communications modules and consumer products is large. That gives it continued volume strength even as engineering teams prepare for faster standards.

Octal and xSPI are gaining ground as real-time code execution becomes more common in automotive processors, AI-capable controllers, and higher-performance embedded systems in the Southeast Asia NOR Flash Memory market. Infineon's SEMPER portfolio supports Octal SPI and HYPERBUS with endurance and retention characteristics optimized for industrial and automotive use, demonstrating that interface upgrades are already aligned with demanding applications. STMicroelectronics also supports XSPI 8-bit and 16-bit configurations in its newer STM32N-series devices, confirming that controller ecosystems are now being built with xSPI readiness in mind. Single and dual SPI channels still matter in low-cost Bluetooth modules, IoT sensors, and entry wearables, especially in cost-sensitive markets such as Vietnam and Indonesia. Yet the direction of platform design is clear, and the South East Asia NOR Flash Memory market will increasingly reward suppliers that can support both the large Quad SPI base and the migration path toward Octal and xSPI.

The more than 32 to 64 megabit category held 27.7% of revenue in 2025, making it the largest density tier in the regional market. This band aligns closely with the firmware needs of mainstream Wi-Fi chips, Bluetooth SoCs, smart meters, and many low-to-mid-tier wearables, which explains its volume advantage in core assembly hubs. It also benefits from broad product catalogs and shorter procurement lead times, which matter for manufacturers running lean inventories. In that sense, the segment captures a large part of the installed base that has kept the Southeast Asia NOR Flash Memory market stable across consumer and communications demand cycles. It is the tier most closely tied to everyday electronics output rather than to specialized high-end applications.

At the top end, the greater than 256 megabit segment is projected to grow at a 7.3% CAGR from 2026 to 2031, which makes it the fastest-growing density range. AI-driven server demand is a major reason, because a GB200-based rack requires far more NOR Flash devices than a conventional rack and has begun to reallocate resources toward higher-capacity parts. Macronix stated that sampling of 3D NOR Flash devices is planned for the second half of 2026, with mass production targeted for 2027, which signals a direct industry response to density limits in traditional 2D NOR structures. Intermediate ranges from 8 megabit to 32 megabit remain important for IoT and portable diagnostics, while 128 megabit to 256 megabit supports network equipment, secure access devices, and vehicle subsystems. This produces a layered demand pattern in the South East Asia NOR Flash Memory market where no single density family can serve every growth pocket. It also means suppliers that span mainstream and high-capacity nodes are better placed to capture demand as purchasing shifts between consumer cycles, infrastructure build-outs, and AI-led allocation pressure.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2 V Class and Similar Sub-1.8 V (2.5 V, 5 V, etc.)

- By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-user Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography (Value, Volume)

- Vietnam

- Indonesia

- Philippines

- Thailand

- Malaysia

List of Companies Covered in this Report:

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- AMIC Technology Corporation (NEW)

- AP Memory Technology Co. Ltd. (NEW)

- Yangtze Memory Technologies Co. Ltd. (YMTC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government-Led Incentives Driving Expansion in Electronics Manufacturing

- 4.2.2 Formation and Growth of Automotive Electronics Clusters in the Region

- 4.2.3 Rising Trend of Outsourcing in Wearable and Point-of-Care Device Manufacturing

- 4.2.4 Accelerated Deployment of 5G and Fiber-to-the-Home Network Infrastructure

- 4.2.5 Supply-Chain Re-shoring Initiatives by Global Tier-1 OEMs

- 4.2.6 Surging Demand for NOR Flash in Edge AI Microcontrollers

- 4.3 Market Restraints

- 4.3.1 Heavy Dependence on Foundries Located Outside South East Asia

- 4.3.2 Intensified Margin Pressures from Cost-Competitive Chinese Vendors

- 4.3.3 Increased Adoption of Emerging Alternative Non-Volatile Memory Technologies

- 4.3.4 Chronic Skilled-Labour Gaps in Sub-20 nm Lithography

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory and Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Others - 1.2 V Class and Similar Sub-1.8 V (2.5 V, 5 V, etc.)

- 5.5 By End-user Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-user Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and More

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

- 5.8 By Geography (Value, Volume)

- 5.8.1 Vietnam

- 5.8.2 Indonesia

- 5.8.3 Philippines

- 5.8.4 Thailand

- 5.8.5 Malaysia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Micron Technology Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.11 Samsung Semiconductor

- 6.4.12 Alliance Memory

- 6.4.13 AMIC Technology Corporation (NEW)

- 6.4.14 AP Memory Technology Co. Ltd. (NEW)

- 6.4.15 Yangtze Memory Technologies Co. Ltd. (YMTC)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)