|

市場調查報告書

商品編碼

2072559

印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)India NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

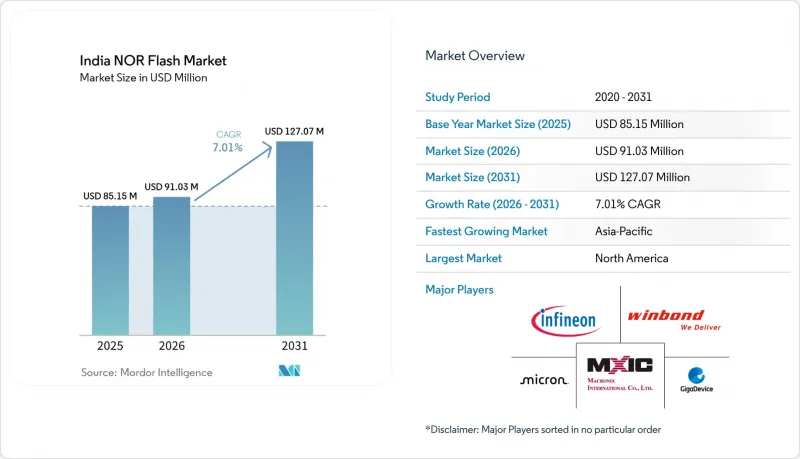

據 Mordor Intelligence 稱,印度 NOR 快閃記憶體市場預計將從 2025 年的 8,515 萬美元成長到 2026 年的 9,103 萬美元,到 2031 年達到 1.2707 億美元,預計 2026 年至 2031 年的複合年成長率為 6.9%。

本報告按類型(串行NOR快閃記憶體、其他)、介面(SPI單/雙介面、其他)、容量(小於2Mbit、其他)、電壓(3V級、其他)、最終用戶應用(消費性電子、汽車、其他)、製程節點(65nm、45nm、其他)和封裝類型(WLCSP/CSP、其他)進行細分。市場預測以價值(美元)和數量(單位)兩種形式呈現。

印度NOR快閃記憶體市場的趨勢與洞察

政府的生產關聯激勵計畫和半導體補貼降低了資本進入的門檻。

在「印度半導體2.0計畫」下,政府撥款100億印度盧比(約1.2億美元)用於新建組裝、檢測、標記和封裝(ATMP)於一體的工廠。此外,根據“電子元件製造計劃”,22個項目於2026年1月獲得批准,總價值達4186.3億印度盧比(約合50.2億美元),這些項目吸引了私營部門的共同投資,並降低了本地電子製造服務(EMS)企業的投資回收門檻。美光公司將在蘇南德投資27.5億美元建造一座ATMP工廠,體現了政府對外國直接投資的信心,並正在推動古吉拉突邦周邊產業生態系統的發展。

強制安全啟動正在加速對串列 NOR 記憶體的需求。

印度標準局 (BIS) 現已強制要求消費性物聯網韌體進行加密簽章檢查,迫使原始設備製造商 (OEM) 整合專用的、即時非揮發性代碼儲存。宏碁 (Macronix) 對此做出回應,發布了 ArmorBoot MX76 系列,該系列產品提供高達 1GB 的內存,並支援 3.0V 和 1.8V 雙路供電,適用於支援安全啟動的智慧電錶設計。預計智慧電錶和支付終端部署的早期合規性將確保該設計在 2027 年前持續應用。

國內先進製造工廠的短缺限制了供應的穩定性。

ISM各階段核准的十家半導體企業主要專注於28nm邏輯和化合物半導體,而非嵌入式非揮發性記憶體(NOR)。因此,目前所有55nm以下的NOR晶圓均來自台灣和中國大陸,導致對這些地區的依賴。這種依賴性構成風險,尤其是在供應鏈中斷或地緣政治緊張局勢發生時。此外,2026年第一季DRAM現貨價格飆升70%,凸顯了代工廠在市場供應緊張時頻繁調整生產重點。這種調整進一步加劇了NOR生產的挑戰,導致前置作業時間延長和供應鏈更加緊張。這一趨勢凸顯了目前半導體產業NOR供應鏈的脆弱性。

細分市場分析

預計到2025年,串列裝置將佔據印度62.7%的市場佔有率,超過NOR快閃記憶體市場的整體成長速度。與平行產品相比,串列裝置具有顯著優勢,例如佔用較少的基板面積和引腳數量。這種效率優勢在消費性物聯網、汽車控制單元和工業PLC等應用中尤其重要。串行產品的緊湊設計和更強大的功能使其成為現代應用的首選,並推動了各行各業的採用。

同時,並行NOR記憶體仍應用於需要16位元匯流排的傳統通訊設備和航空電子設備背板中。然而,廠商正日益將八進位串列產品定位為這些系統的即插即用升級方案。八進位串列產品在顯著縮小尺寸的同時,實現了與平行NOR記憶體相同的400 MB/s吞吐量。華邦電子、宏碁和兆易半導體等公司在2025-2026年擴展了其八進制產品線,為設計人員提供了一條無縫過渡到串行技術的途徑,而無需犧牲頻寬。

預計到2025年,四路SPI介面將佔介面銷售額的47.6%。然而,八路和xSPI介面的成長速度最快,這主要得益於JEDEC xSPI 2.0認證以及汽車應用中對300-400 MB/s高速讀取需求的不斷成長。這些進步使製造商能夠滿足對更快、更有效率的儲存解決方案日益成長的需求。此外,八路和xSPI介面能夠在提升效能的同時保持與現有系統的兼容性,這進一步促進了它們的普及。

英飛凌的「Semper」系列和兆易半導體的「GD25LX256E」等領先廠商正在將xSPI介面與功能安全和低功耗等特性結合。這些創新旨在滿足汽車和工業自動化等行業不斷變化的需求。同時,單雙SPI介面在穿戴式裝置和感測器等對成本高度敏感的應用中仍然發揮著至關重要的作用,因為在這些應用中,最小化韌體體積和提高成本效益至關重要。

2025年,中等容量(32-64 Mbit)的儲存設備仍將佔據市場主導地位,市佔率達28.7%。這些設備憑藉其優異的性價比和廣泛的應用範圍,依然是用戶的首選。然而,在技術進步和對高效資料儲存解決方案日益成長的需求推動下,對高容量儲存設備的需求正在穩步成長。像Mindgrove的V2600這樣的AI協處理器是這種趨勢的主要驅動力,因為它們需要更大的模型權重才能有效運作。

在國防領域,航空電子系統對容量為256 Mbit或以上的抗輻射加固組件的採購量正在持續成長。這些組件透過與印度巴拉特電子公司(Bharat Electronics)簽訂的合約採購,以滿足對高可靠性應用的特定需求。儘管該領域屬於小眾市場,產量較低,但由於專用組件價格高昂,盈利依然豐厚。隨著國防系統的發展和對更先進儲存解決方案需求的成長,預計對這些元件的需求將會擴大。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府主導的生產關聯激勵計畫和印度半導體補貼對資本投資的影響

- 印度標準局推出了安全啟動標準,以增強物聯網設備的安全性。

- 國內汽車ADAS ECU市場成長

- 透過「印度製造」舉措擴大智慧型手機生產

- 國內對航太和國防航空電子模組中八路 NOR 快閃記憶體的需求正在擴大。

- 採用需要在裝置上儲存程式碼的物聯網邊緣人工智慧晶片。

- 市場限制因素

- 印度面臨著用於先進的 55nm 及以下 NOR 快閃記憶體技術的國內晶圓製造能力不足的問題。

- 高額進口關稅對 NOR 快閃存貨接收成本的影響:與東南亞製造地的比較。

- OEM廠商轉向多晶片封裝導致對分立式NOR快閃記憶體組件的需求下降。

- 中國大陸和台灣之間的地緣政治風險導致供應不確定性,影響了印度買家對委託代工廠的分配。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

- 價格分析

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- 透過介面

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按密度

- 2Mbit 或更小的 NOR 閘

- 2~4Mbit

- 4~8Mbit

- 8~16Mbit

- 16~32Mbit

- 32~64Mbit

- 64~128Mbit

- 128~256Mbit

- 超過 256Mbit

- 透過電壓

- 3V級

- 1.8V 類

- 寬電壓範圍(1.65至3.6V)

- 其他 - 1.2V 級及類似產品

- 透過最終用戶應用程式

- 家用電器

- 溝通

- 車

- 產業

- 其他終端用戶應用程式

- 依製程技術節點

- 90奈米或以上

- 65nm

- 55奈米(包括58奈米)

- 45nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 供應商定位分析

- 公司簡介

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Wuhan XMC

- Puya Semiconductor(Shanghai)Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- Zbit Semiconductor

- XTX Technology(Shenzhen)Limited

- Shenzhen Longsys Electronics Co. Ltd.

- Cypress Semiconductor Corporation

- Eon Silicon Solution Inc.

- AMIC Technology Corporation

- Elite Semiconductor Memory Technology Inc.

- Jiangsu Fudan Microelectronics Group Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india NOR flash market size is expected to increase from USD 85.15 million in 2025 to USD 91.03 million in 2026 and reach USD 127.07 million by 2031, growing at a CAGR of 6.9% over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (SPI Single/Dual, and More), Density (2 Mbit and Less, and More), Voltage (3 V Class, and More), End-User Application (Consumer Electronics, Automotive and More), Process Technology Node (65 Nm, 45 Nm, and More), and Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Both Value (USD) and Volume (Units).

India NOR Flash Market Trends and Insights

Government PLI and Semiconductor Subsidies Lower Capital Barriers

India Semiconductor Mission 2.0 earmarked INR 1,000 crore (USD 120 million) for new assembly-test-mark-pack sites, while the Electronics Component Manufacturing Scheme approved 22 projects worth INR 41,863 crore (USD 5.02 billion) in January 2026, unlocking private coinvestment and reducing payback hurdles for local EMS companies. Micron's USD 2.75 billion ATMP plant in Sanand signals confidence in foreign direct investment and encourages the formation of an ecosystem around Gujarat.

Secure-Boot Mandates Accelerate Serial NOR Demand

The Bureau of Indian Standards now requires cryptographic signature checks for consumer IoT firmware, pushing OEMs to add dedicated non-volatile code storage that can execute in place.Macronix answered with its ArmorBoot MX76 family up to 1 GB that supports dual 3.0 V and 1.8 V rails for secure-boot smart-meter designs. Early compliance efforts in smart-meter and payment-terminal rollouts ensure sustained design-in activity through 2027.

Lack of Advanced Domestic Fabs Constrains Supply Security

Ten semiconductor ventures cleared under ISM phases are primarily focused on 28 nm logic or compound semiconductors, rather than embedded non-volatile memory. As a result, all sub-55 nm NOR wafers are currently sourced from Taiwan and China, creating a dependency on these regions. This reliance poses a risk, especially during periods of supply chain disruptions or geopolitical tensions. Additionally, a 70% spike in DRAM spot prices during the first quarter of 2026 highlighted how foundry lines often shift priorities during market crunches. Such shifts further exacerbate the challenges for NOR production, leading to extended lead times and constrained supply. This dynamic underscores the vulnerability of the NOR supply chain in the current semiconductor landscape.

Other drivers and restraints analyzed in the detailed report include:

- Automotive ADAS Electronics Need Functional-Safety NOR Flash

- Make in India Smartphone Output Sustains High-Volume Consumption

- Import Tariffs Inflate Memory Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial devices held 62.7% share in 2025 and are projected to outgrow the overall India NOR Flash market. These devices offer significant advantages by reducing board area and pin counts compared to parallel parts. This efficiency is particularly valued in applications such as consumer IoT, automotive control units, and industrial PLCs. The compact design and enhanced functionality of serial products make them a preferred choice for modern applications, driving their adoption across various industries.

Parallel NOR, on the other hand, continues to find use in legacy telecom and avionics backplanes that require 16-bit buses. However, vendors are increasingly positioning Octal serial parts as drop-in upgrades for these systems. Octal serial parts match the 400 MB/s throughput of parallel NOR while significantly reducing the footprint. Companies like Winbond, Macronix, and GigaDevice expanded their Octal portfolios during 2025-2026, providing designers with a seamless migration path to serial technology without compromising on bandwidth.

Quad SPI generated 47.6% of interface revenue in 2025. However, Octal and xSPI interfaces are witnessing the fastest growth, driven by JEDEC xSPI 2.0 certification and the increasing demand for high-speed reads of 300-400 MB/s in automotive applications. These advancements are enabling manufacturers to meet the growing need for faster and more efficient memory solutions. The adoption of Octal and xSPI is further supported by their ability to deliver enhanced performance while maintaining compatibility with existing systems.

Leading vendors, such as Infineon with its Semper series and GigaDevice with the GD25LX256E, are integrating xSPI interfaces with features like functional safety and low power consumption. These innovations cater to the evolving requirements of industries like automotive and industrial automation. Meanwhile, Single and Dual SPI interfaces continue to hold relevance in ultra-cost-sensitive applications, such as wearables and sensors, where firmware size remains minimal, and cost efficiency is a priority.

Mid-range 32-64 Mbit devices continued to dominate in 2025, accounting for 28.7% of the market share. These devices remain a preferred choice due to their balance of cost and performance, catering to a wide range of applications. However, the demand for higher-capacity devices is steadily increasing, driven by advancements in technology and the growing need for efficient data storage solutions. AI co-processors, such as Mindgrove's V2600, are a key driver of this trend as they require larger model weights to function effectively.

In the defense sector, avionics systems are increasingly procuring radiation-tolerant parts with capacities of 256 Mbit or more. These components are sourced through contracts with Bharat Electronics, addressing the specific needs of high-reliability applications. While this segment represents a low-volume niche, it remains highly profitable due to the premium pricing of specialized components. The demand for such devices is expected to grow as defense systems continue to evolve and require more advanced memory solutions.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Mbit and Less NOR

- More than 2-4 Mbit NOR

- More than 4-8 Mbit NOR

- More than 8-16 Mbit NOR

- More than16-32 Mbit NOR

- More than 32-64 Mbit NOR

- More than 64-128 Mbit NOR

- More than 128-256 Mbit NOR

- Greater than 256 Mbit NOR

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Others -1.2 V Class and Similar

- By End-user Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-user Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (incl. 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

List of Companies Covered in this Report:

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Infineon Technologies AG

- Micron Technology Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Renesas Electronics Corporation

- Wuhan XMC

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Semiconductor

- Alliance Memory

- Zbit Semiconductor

- XTX Technology (Shenzhen) Limited

- Shenzhen Longsys Electronics Co. Ltd.

- Cypress Semiconductor Corporation

- Eon Silicon Solution Inc.

- AMIC Technology Corporation

- Elite Semiconductor Memory Technology Inc.

- Jiangsu Fudan Microelectronics Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Impact of Government-Led PLI and Semiconductor India Subsidies on Capital Expenditures

- 4.2.2 Implementation of Secure-Boot Standards by the Bureau of Indian Standards to Strengthen IoT Device Security

- 4.2.3 Growth in Domestic Automotive ADAS ECU Market

- 4.2.4 Expansion of Smartphone Production under the Make in India Initiative

- 4.2.5 Rising Demand for Octal NOR Flash in Domestic Aerospace and Defense Avionics Modules

- 4.2.6 Adoption of IoT Edge AI Chips Requiring On-Device Code Storage

- 4.3 Market Restraints

- 4.3.1 Limited Indigenous Wafer Fabrication Capabilities for Advanced Sub-55 nm NOR Flash Technology in India

- 4.3.2 Impact of High Import Duties on Landed Costs of NOR Flash versus Southeast Asian Manufacturing Hubs

- 4.3.3 Declining Demand for Discrete NOR Flash Components Due to OEMs' Transition to Multi-Chip Packages

- 4.3.4 Supply Uncertainty from China-Taiwan Geopolitical Risks Affecting Contract Foundry Allocation for Indian Buyers

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Mbit and Less NOR

- 5.3.2 More than 2-4 Mbit NOR

- 5.3.3 More than 4-8 Mbit NOR

- 5.3.4 More than 8-16 Mbit NOR

- 5.3.5 More than16-32 Mbit NOR

- 5.3.6 More than 32-64 Mbit NOR

- 5.3.7 More than 64-128 Mbit NOR

- 5.3.8 More than 128-256 Mbit NOR

- 5.3.9 Greater than 256 Mbit NOR

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V-3.6 V)

- 5.4.4 Others -1.2 V Class and Similar

- 5.5 By End-user Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-user Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and More

- 5.6.2 65 nm

- 5.6.3 55 nm (incl. 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Micron Technology Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Wuhan XMC

- 6.4.10 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.11 Samsung Semiconductor

- 6.4.12 Alliance Memory

- 6.4.13 Zbit Semiconductor

- 6.4.14 XTX Technology (Shenzhen) Limited

- 6.4.15 Shenzhen Longsys Electronics Co. Ltd.

- 6.4.16 Cypress Semiconductor Corporation

- 6.4.17 Eon Silicon Solution Inc.

- 6.4.18 AMIC Technology Corporation

- 6.4.19 Elite Semiconductor Memory Technology Inc.

- 6.4.20 Jiangsu Fudan Microelectronics Group Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)