|

市場調查報告書

商品編碼

2072557

亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Asia-Pacific NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

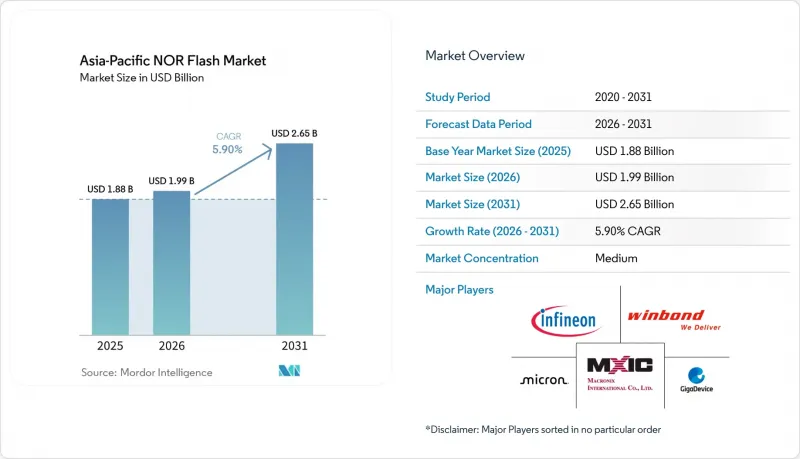

根據 Mordor Intelligence 預測,亞太地區 NOR 快閃記憶體市場規模預計將從 2025 年的 18.8 億美元成長到 2026 年的 19.9 億美元,到 2031 年將達到 26.5 億美元,2026 年至 2031 年的複合年成長率為 5.9%。

本報告按類型(例如,串行NOR快閃記憶體)、介面(例如,四路SPI)、容量(例如,小於2兆位元)、電壓(例如,3V級)、最終用戶應用(例如,家用電子電器)、製程節點(例如,45奈米、55奈米)、封裝類型(例如,WLCSP/CSP)和地區進行細分。市場預測以價值(美元)和數量(單位)表示。

亞太地區NOR快閃記憶體市場趨勢及洞察。

中國和日本汽車電子領域ADAS和資訊娛樂系統的記憶體需求快速成長。

在中國和日本的汽車系統中,對冗餘NOR陣列的安全啟動和故障運行功能的依賴性日益增強,預計到2028年,每輛車的平均負載將達到128兆位元,高於2024年的32兆位元。日本一級供應商正在採用雙通道NOR晶片以符合ISO 26262 ASIL-D標準。英飛凌的SEMPER元件預計將於2025年獲得瑞薩電子R-CAR Gen4認證,以支持該市場典型的2-3年設計更新周期。僅ADAS(高級駕駛輔助系統)就已佔據該地區汽車NOR晶片銷售額的一半以上。預計到2025年,中國汽車出貨量將達到2,700萬輛,且電氣化進程不斷推進,這一領域將構成長期需求的基礎。

亞太地區設計公司向八進制和HyperBus NOR架構的過渡

儘管八進位和xSPI介面在2025年的出貨量佔比僅為15-18%,但它們正迅速成長,這主要得益於邊緣AI和汽車閘道控制器對超過400MB/s頻寬的需求。 2026年3月,英飛凌發布了與LPDDR相容的NOR內存,將讀取吞吐量提升至800MB/s,並簡化了佈線。技嘉科技的1.2V八進位產品支援電池供電的物聯網節點,並將工作電流降低高達40%。隨著台灣和韓國的設計公司將其邊緣AI加速器遷移到xSPI,供應商正在獲得多年期高利潤契約,這有助於抵消家用電子電器的價格壓力。

對中國當地的EUV和DUV設備出口限制

2024年10月實施的擴大版《外國直接產品規則》禁止向中國記憶體工廠出口先進微影術設備,實際上將中國當地的製造流程限制在40奈米及更早的製程水平,這種情況在可預見的未來將持續。由於28奈米NOR記憶體預計可節省30-40%的功耗,這項限制將阻礙中國當地供應商獲得汽車設計訂單。日本與美國政策的趨同進一步擴大了技術差距,導致東京電子無法取得蝕刻系統。儘管台灣和韓國正朝22奈米製程邁進,但中國仍停留在成熟的製程節點。

細分市場分析

到2025年,串列NOR快閃存在亞太地區的NOR快閃記憶體市場將維持71.8%的市佔率。這是因為SPI和四路SPI介面將滿足消費性電子和物聯網應用的大部分啟動程式碼需求。並行NOR快閃記憶體的銷售額將僅佔28.2%,但其複合年成長率將達到7.3%,這主要得益於工業控制和汽車模組等對安全性要求極高的應用中對確定性延遲的迫切需求。並行元件將繼續應用於安全氣囊和ABS等對存取時間要求極高的應用領域,這些應用需要低於50奈秒的存取速度。

為了應對這項挑戰,串行架構供應商正透過增加基於硬體的信任根和冗餘機制,向現有的平行架構製造商發起挑戰,預計在下一輪平台更新中,競爭將進一步加劇。串行架構在密度和可靠性方面也在穩步提升。宏碁的 ArmorBoot MX76 晶片實現了 1Gigabit安全啟動功能,這表明曾經僅限於並行 NOR 記憶體的「原地執行」和安全功能,如今也可以應用於串行設計。無法提供這些增強功能的供應商,將面臨被限制在以成本為導向的消費性電子設備市場的風險,而來自中國新參與企業的價格競爭將進一步擠壓其利潤空間。

單/雙路 SPI 介面佔據市場主導地位,預計到 2025 年將佔據 47.6% 的市場佔有率。然而,頻寬限制在約 80 MB/s,這限制了其在資料密集型系統中的應用。儘管有此限制,對於對成本敏感且高速性能要求不高的應用而言,它仍然是首選。四路 SPI 介面約佔 35% 的市場佔有率,目前正經歷重大變革,為需要更快韌體更新的中階智慧型手機和工業閘道提供支援。同時,八路和 xSPI 介面雖然出貨量佔不到 20%,但正經歷顯著成長。這些先進介面的複合年成長率 (CAGR) 為 9.6%,主要得益於對汽車乙太網路閘道器和邊緣 AI 加速器日益成長的需求,這些設備需要高達 800 MB/s 的讀取性能。

介面多樣化在供應商的發展藍圖中扮演著至關重要的角色。台灣設計公司正迅速採用xSPI介面,從汽車行業客戶那裡獲得了多年契約,並穩定了其收入來源。傳統的消費性電子和白色家電製造商仍然依賴SPI單/雙介面。這種選擇主要是出於減少控制器引腳數量和確保成本效益的需要。因此,像SPI單/雙介面這樣的成熟介面能夠維持長期的收入基礎,這得益於效用。

預計到2025年,亞太地區NOR快閃記憶體市場中,容量為64兆位元及以下的裝置將佔據27.2%的佔有率。這主要歸功於低成本微控制器在各種應用中的廣泛使用。這些裝置因其價格實惠且相容於舊有系統而保持著較高的市場需求。然而,容量超過256兆位元的裝置正以10.9%的複合年成長率快速成長,這主要得益於OLED智慧型手機、ADAS控制器和邊緣AI模組對更大韌體儲存的需求不斷成長。宏碁的1Gigabit「ArmorBoot」技術支援用於空中下載(OTA)更新的隔離安全分區,正在推動旗艦智慧型手機採用0.5Gigabit級NOR快閃記憶體。這一趨勢凸顯了高階應用對高容量NOR快閃記憶體日益成長的需求。

容量在 128 至 256 兆位元之間的中等密度產品在成本和容量之間取得了良好的平衡,使其成為汽車資訊娛樂系統和工業人機介面 (HMI) 的理想選擇。這些容量能夠滿足對儲存容量要求適中的應用,且不會顯著增加成本。容量在 2 至 8 兆位元之間的產品仍然用於超低成本感測器,因為這些感測器對儲存容量的要求很低。然而,這些低容量產品的市場佔有率正逐年被整合到系統晶片(SoC) 中的嵌入式快閃記憶體解決方案所取代,後者在現代應用中提供了更優異的效能和效率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國和日本汽車電子市場對ADAS和資訊娛樂系統的記憶體需求快速成長。

- 在中國和韓國,基於OLED的智慧型手機設計正在推動對高密度串列NOR記憶體的需求。

- 半導體自給自足的獎勵(例如中國和印度的PLI)正在加速該地區NOR型晶圓廠的建設。

- 東協物聯網製造群需要低功耗程式碼儲存。

- 台灣和韓國向工業4.0升級:工業自動化

- 亞太地區設計公司向 Octal/Hyperbus NOR 架構的過渡

- 市場限制因素

- 深圳設計採用案例中低成本NAND和ReRAM的蠶食現象

- 台灣12吋晶片代工廠供應緊張,導致價格波動。

- 28nm 與 22nm NOR 晶片研發拓展;資本支出與主流邏輯產品線對比

- 對中國當地出口EUV/DUV設備的限制

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

- 價格分析

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- By Interface

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按密度

- 2兆位元或以下的NOR閘

- 位元深度為 4 兆位元或更低(超過 2 MB)的 NOR 記憶體

- 位元深度為 8 兆位元或更低(超過 4 MB)的 NOR 記憶體

- 16兆位元或更小的NOR記憶體(超過8MB)

- 位元深度為 32 兆位元或更低(超過 16 MB)的 NOR 記憶體

- 位元深度為 64 兆位元或更低(超過 32 MB)的 NOR 記憶體

- 位元深度為 128 兆位元或更低(超過 64 MB)的 NOR 記憶體

- 位元深度為 256 兆位元或更低(超過 128 MB)的 NOR 記憶體

- 超過 256 兆比特

- 透過電壓

- 3 V級

- 1.8 V級

- 寬電壓範圍(1.65V 至 3.6V)

- 其他 - 1.2 V 級(以及低於 1.8 V 的類似產品:2.5 V、5 V)

- 透過最終用戶應用程式

- 家用電子產品

- 溝通

- 車

- 產業

- 其他終端用戶應用程式

- 依製程技術節點

- 90奈米及更早

- 65 nm

- 55奈米(包括58奈米)

- 45 nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他包裝類型

- 按地區

- 中國

- 日本

- 韓國

- 台灣

- 印度

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Winbond Electronics Corp.

- GigaDevice Semiconductor Inc.

- Macronix International Co., Ltd.

- Micron Technology Inc.

- Infineon Technologies AG

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Elite Semiconductor Memory Tech(ESMT)

- Puya Semiconductor(Shanghai)Co.

- Wuhan XMC

- Integrated Silicon Solution Inc.(ISSI)

- Samsung Electronics Co. Ltd.

- STMicroelectronics NV

- Alliance Memory, Inc.

- SK hynix Inc.

- AMIC Technology Corp.

- NXP Semiconductors NV

- Powerchip Semiconductor Manufacturing Corp.

- Adesto Technologies(renesas)

- BOYA Microelectronics Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific NOR flash market size is expected to grow from USD 1.88 billion in 2025 to USD 1.99 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at a 5.9% CAGR over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (Quad SPI, and More), Density (2 Megabit and Less, and More), Voltage (3 V Class, and More), End-User Application (Consumer Electronics, and More), Process Technology Node (45 Nm, 55 Nm, and More), Packaging Type (WLCSP/CSP, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific NOR Flash Market Trends and Insights

Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics

Automotive systems in China and Japan increasingly rely on redundant NOR arrays for safe-boot and fail-operational functions, pushing average vehicle content from 32 megabits in 2024 to a projected 128 Megabits by 2028. Japanese Tier-1 suppliers embed dual-channel NOR to achieve ISO 26262 ASIL-D compliance. Infineon's SEMPER devices qualified with Renesas R-CAR Gen4 in 2025, evidencing the two-to-three-year design-win horizon common in this market. ADAS alone already represents more than half of automotive NOR revenue in the region. With China delivering 27 million vehicles in 2025 and electrification rising, the segment anchors long-term demand.

Shift To Octal and HyperBus NOR Architectures Across Asia-Pacific Design Houses

Octal and xSPI interfaces delivered only 15-18% of 2025 volumes yet are scaling fast on the back of bandwidth needs above 400 MB/s in edge-AI and automotive gateway controllers. Infineon introduced an LPDDR-compatible NOR in March 2026, doubling read throughput to 800 MB/s and simplifying routing. GigaDevice's 1.2 V Octal parts serve battery-powered IoT nodes, cutting active current by up to 40%. As Taiwanese and Korean design houses migrate edge-AI accelerators to xSPI, suppliers secure multi-year, higher-margin contracts that offset consumer-electronic price pressure.

Export-Control Curbs on EUV and DUV Tools Into Mainland China

Expanded Foreign Direct Product Rule measures implemented in October 2024 bar advanced lithography shipments to Chinese memory fabs, limiting mainland processes to 40-nanometer and older for the foreseeable future. Automotive-grade NOR at 28 nanometers promises 30-40% power savings, so the restriction hampers mainland suppliers seeking vehicle design wins. Japan's alignment with U.S. policy cut access to Tokyo Electron etch systems, reinforcing the technology split: Taiwan and South Korea advance to 22 nanometers while China remains at mature nodes.

Other drivers and restraints analyzed in the detailed report include:

- Chip-Self-Sufficiency Incentives in China and India

- OLED-Centric Smartphone Designs Pushing High-Density Serial NOR

- 12-Inch Foundry Tightness in Taiwan Driving Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR retained 71.8% of the Asia-Pacific NOR Flash market share in 2025, as SPI and Quad SPI interfaces satisfy most consumer and IoT boot-code needs. Parallel NOR, although only 28.2% of revenue, benefits from a 7.3% CAGR driven by deterministic-latency requirements in industrial control and safety-critical automotive modules. Parallel devices remain embedded in airbags and ABS, where sub-50 ns access cannot be compromised.

In response, serial suppliers add hardware root-of-trust and redundancy to challenge parallel incumbents, foreshadowing tighter competition in the next platform refresh. Serial architectures are also creeping upward in density and reliability. Macronix's ArmorBoot MX76 brings 1 Gigabit secure-boot capability, showing that execute-in-place and security, once exclusive to parallel NOR, can migrate to serial designs. Suppliers that fail to offer these enhancements risk confinement to cost-sensitive consumer devices, where price wars with Chinese entrants squeeze margins.

SPI Single/Dual dominated the market with a 47.6% share in 2025. However, its bandwidth ceilings, capped at approximately 80 MB/s, restrict its application in data-intensive systems. Despite this limitation, it remains a preferred choice for cost-sensitive applications where high-speed performance is not critical. Quad SPI, holding around 35% of the market share, is at a pivotal stage, catering to mid-range smartphones and industrial gateways that require faster firmware updates. Meanwhile, Octal and xSPI interfaces, though accounting for less than 20% of total units, are experiencing significant growth. These advanced interfaces are growing at a 9.6% CAGR, driven by increasing demand for automotive Ethernet gateways and edge-AI accelerators that require read performance of up to 800 MB/s.

Interface fragmentation is playing a critical role in shaping supplier roadmaps. Taiwanese design houses are quickly adopting xSPI interfaces and securing multiyear commitments from automotive clients, helping stabilize their revenue streams. Manufacturers of legacy appliances and white goods continue to rely on SPI Single/Dual interfaces. This choice is primarily driven by the need to minimize controller pin counts and ensure cost efficiency. As a result, mature interfaces like SPI Single/Dual maintain a long revenue tail, supported by their relevance in applications where advanced performance is not a priority.

Devices at 64 megabits or below accounted for 27.2% of the Asia-Pacific NOR Flash market in 2025, driven by the widespread use of low-cost microcontrollers across various applications. These devices remain popular due to their affordability and compatibility with legacy systems. However, densities above 256 megabits are growing rapidly, with a CAGR of 10.9%, as OLED smartphones, ADAS controllers, and edge-AI modules increasingly require larger firmware storage. Macronix's 1 Gigabit ArmorBoot technology supports isolated secure partitions for over-the-air updates, encouraging flagship smartphones to adopt half-gigabit NOR footprints. This trend highlights the growing demand for higher-density NOR Flash in advanced applications.

Mid-tier densities, ranging from 128 to 256 megabits, strike a balance between cost and capacity, making them ideal for automotive infotainment systems and industrial human-machine interfaces (HMIs). These densities cater to applications that require moderate storage without significantly increasing costs. 2-8 Megabit parts continue to find use in ultra-low-cost sensors, where minimal storage is sufficient. However, these lower-density parts are gradually losing market share each year to embedded flash solutions integrated within system-on-chips, which offer better performance and efficiency for modern applications.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less (greater than 2 MB) NOR

- 8 Megabit and Less (greater than 4 MB) NOR

- 16 Megabit and Less (greater than 8 MB) NOR

- 32 Megabit and Less (greater than 16 MB) NOR

- 64 Megabit and Less (greater than 32 MB) NOR

- 128 Megabit and Less (greater than 64 MB) NOR

- 256 Megabit and Less (greater than 128 MB) NOR

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2 V Class (and similar sub-1.8 V: 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography

- China

- Japan

- South Korea

- Taiwan

- India

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Winbond Electronics Corp.

- GigaDevice Semiconductor Inc.

- Macronix International Co., Ltd.

- Micron Technology Inc.

- Infineon Technologies AG

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Elite Semiconductor Memory Tech (ESMT)

- Puya Semiconductor (Shanghai) Co.

- Wuhan XMC

- Integrated Silicon Solution Inc. (ISSI)

- Samsung Electronics Co. Ltd.

- STMicroelectronics NV

- Alliance Memory, Inc.

- SK hynix Inc.

- AMIC Technology Corp.

- NXP Semiconductors N.V.

- Powerchip Semiconductor Manufacturing Corp.

- Adesto Technologies (renesas)

- BOYA Microelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics

- 4.2.2 OLED-Centric Smartphone Designs Pushing High-Density Serial NOR in China and Korea

- 4.2.3 Chip-Self-Sufficiency Incentives (China, India PLI) Accelerate Regional NOR Fabs

- 4.2.4 IoT Manufacturing Clusters in ASEAN Requiring Low-Power Code Storage

- 4.2.5 Industry 4.0 Upgrades in Taiwan and South Korea Industrial Automation

- 4.2.6 Shift to Octal/HyperBus NOR Architectures Across Asia-Pacific Design Houses

- 4.3 Market Restraints

- 4.3.1 Low-Cost NAND and ReRAM Cannibalization in Shenzhen Design Wins

- 4.3.2 12-Inch Foundry Tightness in Taiwan Driving Price Volatility

- 4.3.3 Escalating 28 nm and 22 nm NOR R&D Capex vs. Mainstream Logic Lines

- 4.3.4 Export-Control Curbs on EUV / DUV Tools into Mainland China

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less NOR

- 5.3.2 4 Megabit and Less (greater than 2 MB) NOR

- 5.3.3 8 Megabit and Less (greater than 4 MB) NOR

- 5.3.4 16 Megabit and Less (greater than 8 MB) NOR

- 5.3.5 32 Megabit and Less (greater than 16 MB) NOR

- 5.3.6 64 Megabit and Less (greater than 32 MB) NOR

- 5.3.7 128 Megabit and Less (greater than 64 MB) NOR

- 5.3.8 256 Megabit and Less (greater than 128 MB) NOR

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Others - 1.2 V Class (and similar sub-1.8 V: 2.5 V, 5 V)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-User Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

- 5.8 By Geography

- 5.8.1 China

- 5.8.2 Japan

- 5.8.3 South Korea

- 5.8.4 Taiwan

- 5.8.5 India

- 5.8.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corp.

- 6.4.2 GigaDevice Semiconductor Inc.

- 6.4.3 Macronix International Co., Ltd.

- 6.4.4 Micron Technology Inc.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Renesas Electronics Corp.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Elite Semiconductor Memory Tech (ESMT)

- 6.4.9 Puya Semiconductor (Shanghai) Co.

- 6.4.10 Wuhan XMC

- 6.4.11 Integrated Silicon Solution Inc. (ISSI)

- 6.4.12 Samsung Electronics Co. Ltd.

- 6.4.13 STMicroelectronics NV

- 6.4.14 Alliance Memory, Inc.

- 6.4.15 SK hynix Inc.

- 6.4.16 AMIC Technology Corp.

- 6.4.17 NXP Semiconductors N.V.

- 6.4.18 Powerchip Semiconductor Manufacturing Corp.

- 6.4.19 Adesto Technologies (renesas)

- 6.4.20 BOYA Microelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)