|

市場調查報告書

商品編碼

2072555

歐洲NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Europe NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

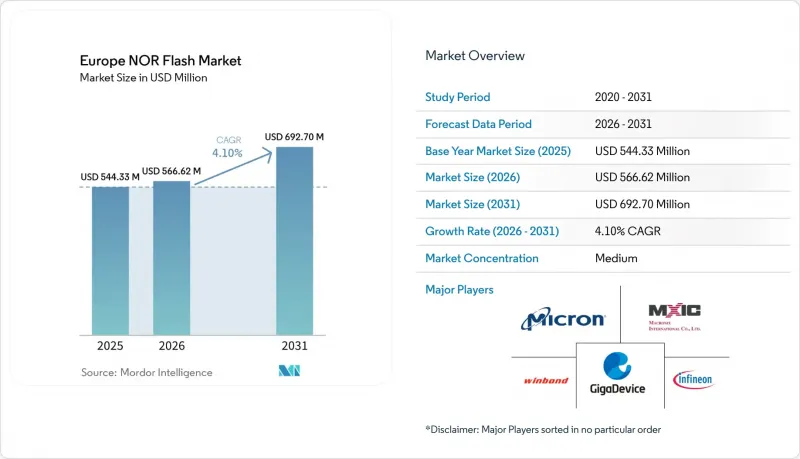

根據 Mordor Intelligence 預測,歐洲 NOR 閃光膠片市場規模預計將從 2025 年的 5.4433 億美元和 2026 年的 5.6662 億美元成長到 2031 年的 6.927 億美元,2026 年至 2031 年的年複合成長率(CAGR)。

本報告依NOR快閃記憶體類型(串列、平行)、介面(SPI、四路SPI等)、容量(2兆位元以下、2兆位元以上)、電壓(3V級、3V以上)、終端用戶應用(家用電子電器等)、製程節點(55/58奈米、65奈米、45奈米等)及封裝類型(WLCSP/CSP等)進行細分。市場預測以價值(美元)和數量(單位)表示。

歐洲NOR快閃記憶體市場的趨勢與洞察

歐洲電動車向OTA韌體更新的轉變正在推動對高密度SPI NOR的需求。

聯合國第156號法規規定,自2024年7月起,在歐盟銷售的所有新車都必須配備軟體更新管理系統,這迫使一級供應商過渡到雙存儲體NOR快閃記憶體設計,以便在更新另一個存儲體的同時,保持一個存儲體中的運作中代碼。這項要求需要持續提供回滾鏡像,從而增加了每個ECU所需的最小快閃記憶體容量,並直接推動了歐洲NOR快閃記憶體市場對高密度產品的需求。此外,支援OTA更新且整合安全功能的NOR快閃記憶體售價將高於標準代碼儲存設備,從而使汽車級組件的價格更具優勢。英飛凌推出的「SEMPER X1」是一款LPDDR快閃記憶體產品,面向對高速存取和即時執行要求極高的下一代汽車電子電氣架構。隨著歐洲高階OEM廠商持續推進軟體定義汽車平臺的標準化,此轉變將確保在高密度SPI NOR快閃存在預測期內保持有利地位。

汽車製造商強制性的快閃記憶體品質目標正在推動閃存在德國和北歐國家的普及。

德國一級供應商和北歐汽車電子製造商持續將ASIL-D功能安全標準作為新型ADAS和閘道器ECU專案的實際准入要求,從而提高了歐洲NOR快閃記憶體市場的認證標準。 GigaDevice的汽車級SPI NOR快閃記憶體系列「GD25/55」於2024年12月獲得ISO 26262 ASIL-D認證,使先前僅限於成熟供應商的認證活動也得以開展。 Macronix也於2025年1月將其MXSMIO系列的OctaFlash和Quad SPI版本擴展至ASIL-D合規範圍,進一步豐富了汽車級產品選擇。隨著新供應商準備獲得ASIL-D認證,即使現有供應商維持設計訂單,採購團隊在插槽定價方面也擁有了更大的議價能力。 AEC-Q100 1級熱性能和可靠性篩檢提供了額外的保障,有助於保護高性能汽車插槽免受能力較弱的新進入者的衝擊。

28 奈米浮閘節點的晶圓廠級良率下降,導致平均銷售價格 (ASP) 的波動性增加。

先進的28奈米浮閘整合技術在電荷損耗和單元耦合方面仍面臨挑戰,這會導致高密度NOR產品的擦除閾值升高並降低有效輸出。隨著良率的降低,供應商通常會優先選擇高階車規級產品,這使得工業和通訊客戶在採購和定價方面的柔軟性降低。這一趨勢對歐洲NOR快閃記憶體市場影響顯著,因為德國和法國的汽車買家已經受到嚴格的認證規則約束,難以進行簡單的替換。此外,由於AEC-Q100和JEDEC可靠性篩檢增加了額外的篩選流程,基準晶圓生產無法直接轉換為可直接銷售的車規晶片。因此,需要採用先進特殊節點認證NOR晶片的買家往往會面臨價格波動和更長的規劃週期。

細分市場分析

到2025年,串行NOR快閃記憶體將佔據歐洲NOR快閃記憶體市場66.1%的佔有率,這反映了市場長期以來對並行設備所採用的寬總線架構的摒棄。串行產品之所以能夠保持其主導地位,是因為它們可以減少引腳數量、降低PCB佈線複雜性,並便於整合到緊湊型汽車ECU和工業控制器中。這些系統級優勢與組件成本同等重要,因為在許多新計畫中,基板面積、電源佈線和封裝整合正日益成為嚴格的設計優先順序。因此,串列組件在歐洲NOR快閃記憶體市場備受青睞,不僅用於主流的基於MCU的系統,也用於需要更高頻寬但又不希望佔用過多物理空間的新型控制器設計。華邦電子的八路NOR產品系列展示了串行架構的進步,該公司重點介紹了其支援xSPI的產品高達400 MB/s的順序讀取吞吐量。

在某些航空電子設備、國防通訊和長壽命工業PLC專案中,並行NOR快閃記憶體仍然具有重要價值,因為在這些專案中,傳統的時序特性和重新設計風險比引腳效率更為重要。儘管這些應用範圍有限,但它們仍然佔據著重要的商業性地位,因為這些專案中的客戶通常優先考慮平台的連續性而非架構變更。諸如ISO 26262之類的功能安全標準適用於這兩種產品類型,但串行NOR快閃記憶體受益於近期認證方面的投入以及活躍供應商更廣泛的產品發布。這種廣泛的生態系統至關重要,因為汽車和工業系統採購團隊越來越傾向於選擇具有更強大的工具支援、更廣泛的介面相容性和長期發展藍圖的組件。因此,歐洲NOR快閃記憶體市場正在圍繞新設計中的串行解決方案進行整合,而並行NOR快閃存在專業部署環境中的維護和連續性方面發揮著越來越重要的作用。

到 2025 年,Quad SPI 將佔據歐洲 NOR 快閃記憶體市場 49.7% 的佔有率,鞏固其在當前 MCU 和 SoC 生態系統中的深厚地位。其主導地位源於成熟的驅動程式支援、廣泛的晶片組相容性以及在汽車和工業系統中長期累積的認證經驗。由於許多 OEM 廠商在重新設計成本高昂且程式碼遷移預算有限的情況下優先考慮介面的連續性,因此這個市場基礎仍然至關重要。英飛凌的 SEMPER NOR 產品系列將繼續支援汽車和工業平台的主流嵌入式需求,在這些平台中,經過檢驗的運作比介面的突然變更更為重要。對於歐洲 NOR 快閃記憶體市場的大部分用戶而言,只要頻寬需求保持在當前就地執行限制之內,Quad SPI 仍然是首選。

然而,隨著網域控制器、人工智慧邊緣節點和先進通訊硬體的吞吐量不斷超越傳統四路SPI的極限,市場重心正向高效能系統轉移。因此,八路和xSPI已成為成長最快的介面類型,市場預測到2031年將以5.9%的複合年成長率成長。宏碁在2025年3月宣布其OctaFlash產品將被意法半導體的STM32N6平台採用,支援200MHz DDR模式下400MB/s的吞吐量,這印證了上述趨勢。此外,JEDEC對xSPI的標準化也緩解了廠商鎖定帶來的擔憂,使計畫開發下一代電路板的OEM廠商更容易過渡到八路介面。因此,歐洲NOR快閃記憶體市場格局呈現為四路SPI保持廣泛的應用基礎,而八路和xSPI則在高頻寬應用中不斷擴大市場佔有率。

到2025年,32-64兆位元以上的NOR快閃記憶體將佔歐洲NOR快閃記憶體市場25.6%的佔有率,成為銷售量最大的容量等級。這反映了單ECU汽車電子產品、工業感測器融合節點以及通訊用戶端設備對韌體儲存的需求,這些應用無需承擔更高容量帶來的額外成本。由於許多嵌入式程式仍採用此容量範圍,因此該細分市場仍保持強勁成長動能。受系統複雜性不斷提高的驅動,預計到2031年,256兆位元及以下(超過128MB)的NOR快閃記憶體市場將以6.1%的複合年成長率成長。在歐洲,這種轉變與區域控制器和網域控制器設計的普及密切相關,這些設計整合了先前分散在各個小型ECU中的程式碼庫。

4-8兆位元及以上、2-4兆位元及以上以及低容量NOR閃存在傳統工業控制器和簡易感測器平台中保持著穩定的部署基礎。由於客戶優先考慮設計的延續性而非性能提升,市場需求依然強勁。供應商的路線圖正在擴展,以適應新的低功耗應用,例如,GigaDevice計劃於2026年3月將其超低功耗SPI NOR系列「GD25UF」的容量從8兆位元擴展至256兆位元。這將支援藍圖運算平台、醫療穿戴式裝置和邊緣人工智慧系統等需要更高容量、低功耗存儲,同時又能維持NOR快閃記憶體特性的應用。歐洲NOR快閃記憶體市場仍以中等容量產品為主,但由於軟體複雜性的增加,中高容量產品的成長正在加速。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車OEM廠商設定的快閃記憶體品質目標正在推動德國和北歐國家對快閃記憶體技術的採用。

- 歐盟對以資料為中心的邊緣人工智慧的日益普及,正在推動工業PLC中串行NOR的應用。

- 歐洲電動車向OTA韌體更新的轉變正在推動對高密度SPI NOR的需求。

- 英國和法國的電信開放式無線存取網部署:需要低延遲啟動代碼儲存。

- 有關醫療穿戴式裝置 (MDR) 的法規正在加速安全 NOR 的整合。

- 歐盟晶片法為 28 奈米和 45 奈米 NOR 生產線(例如德勒斯登)提供資金

- 市場限制因素

- 在消費性物聯網設備中,容量低於 256 Mb 的產品擴大採用 1.8V NAND 作為替代方案。

- 28 奈米浮閘節點的晶圓廠級良率下降,導致平均銷售價格 (ASP) 的波動性增加。

- 歐洲專用光掩模供應緊張,阻礙了並行 NOR 技術的推廣。

- 英國脫歐後海關延誤對英國一級汽車供應商前置作業時間的影響

- 產業價值鏈分析

- 監理展望

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 價格分析

- 投資分析

第5章 市場規模與成長預測

- 按類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- By Interface

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按密度

- 2兆位元或更少

- 2 到 4 兆位元以上

- 4 到 8 兆位元以上

- 8 至 16 兆位元及以上

- 16-32兆位元及以上

- 32-64兆位元及以上

- 64兆位元及以上至128兆比特

- 超過 128 兆比特到 256 兆比特

- 超過 256 兆比特

- 透過電壓

- 3 V級

- 1.8 V級

- 寬電壓範圍(1.65V 至 3.6V)

- 其他 - 1.2V 級(小於 1.8V、2.5V、5V)

- 透過最終用戶應用程式

- 家用電子產品

- 溝通

- 車

- 產業

- 其他終端用戶應用程式

- 依製程技術節點

- 90奈米或以上

- 65 nm

- 55奈米(包括58奈米)

- 45 nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他包裝類型

- 國家

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Vendor Positioning Analysis

- 公司簡介

- Infineon Technologies AG

- Micron Technology Inc.

- Winbond Electronics Corp.

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Elite Semiconductor Microelectronics Tech. Inc.

- Samsung Electronics Co. Ltd.

- SK hynix Inc.

- SMIC NOR Foundry Services

- Tower Semiconductor

- ISSI Automotive Grade NOR(China)

- Macron Flash Ltd.

- Cypress Semiconductor Corp.

- Alliance Memory Inc.

- Puya Semiconductor(Shanghai)Co. Ltd.

- Hua Hong Semiconductor Ltd.

- EON Silicon Solution Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe NOR flash market size is projected to expand from USD 544.33 million in 2025 and USD 566.62 million in 2026 to USD 692.70 million by 2031, registering a CAGR of 4.10% between 2026 to 2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Interface (SPI, Quad SPI, and More), Density (2 Megabit and Less, and More), Voltage (3V Class, and More), End-User Application (Consumer Electronics, and More), Process Technology Node (55/58 Nm, 65 Nm, 45 Nm, and More), and Packaging Type (WLCSP/CSP, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Europe NOR Flash Market Trends and Insights

Shift To OTA Firmware Updates In European EVs Boosting High-Density SPI NOR Demand

UN Regulation No. 156 made a software update management system mandatory for all new vehicles sold in the European Union from July 2024, pushing Tier-1 suppliers toward dual-bank NOR designs that can update one bank while the other keeps the live code running. That requirement increases the minimum flash allocation per ECU because rollback images must remain available, thereby directly increasing density demand in the European NOR Flash Memory market. It also supports better pricing for automotive-grade parts because OTA-ready NOR with integrated security features sells at a premium to standard code-storage devices. Infineon's SEMPER X1 was introduced as an LPDDR Flash product aimed at next-generation automotive electronic and electrical architectures where fast access and real-time execution matter. As European premium OEMs continue to standardize software-defined vehicle platforms, this shift keeps high-density SPI NOR in a favorable position across the forecast period.

Automotive OEM-Mandated Flash Quality Targets Driving Design-Ins In Germany And Nordics

German Tier-1 suppliers and Nordic automotive electronics manufacturers continue to treat ASIL-D functional safety as a practical entry requirement for new ADAS and gateway ECU programs, which raises the qualification bar in the Europe NOR Flash Memory market. GigaDevice's GD25/55 automotive-grade SPI NOR family received ISO 26262 ASIL D certification in December 2024, opening access to qualification activities previously reserved for more established suppliers. Macronix also expanded its automotive-grade options in January 2025 by extending ASIL D compliance across both OctaFlash and Quad SPI variants in its MXSMIO family. Once an additional supplier reaches ASIL-D readiness, procurement teams gain greater negotiating power over socket pricing, even when incumbent vendors retain the design win. AEC-Q100 Grade 1 thermal and reliability screening adds another barrier, helping protect premium automotive sockets from low-capability entrants.

Fab-Level Yield Losses On 28 Nm Floating-Gate Nodes Elevating ASP Volatility

Advanced floating-gate integration at 28 nm continues to face charge-loss and cell-coupling challenges, which can widen erase thresholds and reduce effective output in higher-density NOR products. When yield tightens, suppliers usually prioritize premium automotive grades first, leaving industrial and communications customers with less procurement and pricing flexibility. In the Europe NOR Flash Memory market, that pattern matters because automotive buyers in Germany and France already operate under strict qualification rules that limit easy substitution. AEC-Q100 and JEDEC reliability screening add additional filtering steps, meaning baseline wafer volumes do not directly translate into saleable automotive die. The practical result is more volatile pricing and longer planning cycles for buyers who need qualified NOR at advanced specialty nodes.

Other drivers and restraints analyzed in the detailed report include:

- EU Data-Centric Edge-AI Roll-Outs Elevating Serial NOR Adoption In Industrial PLCs

- EU Chips Act Funding For 28 Nm And 45 Nm NOR Lines In Dresden

- Rising 1.8 V NAND Substitutes Below 256 Mb In Consumer IoT Nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR Flash held 66.1% of the Europe NOR Flash market share in 2025, which reflected a long-running shift away from the wider bus structure used in parallel devices. The segment kept that lead because serial parts reduce pin count, lower PCB routing complexity, and fit more easily into compact automotive ECUs and industrial controllers. In many new programs, those system-level benefits matter as much as component cost because board area, power routing, and package integration are becoming stricter design priorities. The European NOR Flash market has therefore favored serial parts not only for mainstream MCU-based systems, but also for newer controller designs that need better bandwidth without a large physical footprint. Winbond's Octal NOR portfolio shows how far serial architectures have advanced, with the company highlighting continuous read throughput up to 400 MB/s on xSPI-enabled products.

Parallel NOR Flash still has value in selected avionics, defense communications, and long-life industrial PLC programs, where legacy timing behavior and redesign risk are more important than pin efficiency. Those uses are narrower, but they remain commercially relevant because customers in such programs often prefer platform continuity over architectural change. Functional safety rules such as ISO 26262 apply across both product types, yet serial NOR has benefited from a wider flow of recent certification investments and product launches from active suppliers. That wider ecosystem matters because procurement teams in automotive and industrial systems increasingly favor parts with stronger tool support, broader interface compatibility, and longer forward roadmaps. As a result, the European NOR Flash Memory market continues to consolidate around serial solutions for new designs, while parallel NOR serves more of a maintenance and continuity role in specialized deployments.

Quad SPI accounted for 49.7% of the Europe NOR Flash market in 2025, underscoring its deep embeddedness in current MCU and SoC ecosystems. Its lead comes from mature driver support, broad chipset compatibility, and a long history of qualification across automotive and industrial systems. That installed base still matters because many OEMs prefer interface continuity when redesign costs are high, and code migration budgets are tight. Infineon's SEMPER NOR product range continues to support these mainstream embedded requirements across automotive and industrial platforms that prioritize validated operation over aggressive interface change. For much of the European NOR Flash market, Quad SPI remains the default choice when bandwidth demands stay within current execute-in-place limits.

The balance is shifting toward higher-performance systems because domain controllers, AI-enabled edge nodes, and advanced communications hardware are pushing beyond traditional Quad SPI throughput ceilings. Octal and xSPI therefore represent the fastest-growing interface class, with the market forecast indicating 5.9% CAGR through 2031. Macronix demonstrated this direction in March 2025, when it said its OctaFlash products were selected for STMicroelectronics' STM32N6 platform and could support 200 MHz DDR mode for 400 MB/s throughput. JEDEC xSPI standardization also reduces supplier lock-in concerns, making Octal migration easier for OEMs planning the next board generation. The result is a market mix where Quad SPI maintains its broad installed base, while Octal and xSPI capture a rising share of higher-bandwidth applications in the European NOR Flash Memory market.

The more than 32 to 64 megabit NOR segment accounted for 25.6% of the Europe NOR Flash Memory market in 2025, making it the largest density tier by revenue. It reflects the needs of single-ECU automotive electronics, industrial sensor-fusion nodes, and telecom customer-premises equipment that require firmware storage without the higher cost of density bands. This segment remains durable as many embedded programs still fit within this range. The 256 Megabit and Less (greater than 128MB) NOR tier is forecast to grow at a 6.1% CAGR through 2031, driven by rising system complexity. In Europe, this shift aligns with zonal and domain-controller designs, consolidating code bases previously spread across smaller ECUs.

Smaller-density segments, more than 4 to 8 megabit, more than 2 to 4 megabit, and 2 megabit and less NOR, retain a stable installed base in legacy industrial controllers and simple sensor platforms. Demand remains steady as customers prioritize design continuity over performance upgrades. Supplier roadmaps are extending upward for new low-power applications, as seen in GigaDevice's March 2026 expansion of its GD25UF ultra-low-power SPI NOR series from 8 Mb to 256 Mb. This supports AI computing platforms, medical wearables, and edge-AI systems needing larger low-power storage while retaining NOR flash characteristics. The European NOR Flash Memory market remains anchored in mid-range densities, with growth accelerating in upper-middle tiers due to increasing software complexity.

Complete Report Scope:

- By Type (Value and Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less

- More than 2 to 4 Megabit

- More than 4 to 8 Megabit

- More than 8 to 16 Megabit

- More than 16 to 32 Megabit

- More than 32 to 64 Megabit

- More than 64 to 128 Megabit

- More than 128 to 256 Megabit

- More than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V-3.6 V)

- Others - 1.2 V Class (Sub-1.8 V, 2.5 V, 5 V)

- By End-User Application (Value and Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and More

- 65 nm

- 55 nm (Including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Country

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

List of Companies Covered in this Report:

- Infineon Technologies AG

- Micron Technology Inc.

- Winbond Electronics Corp.

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Elite Semiconductor Microelectronics Tech. Inc.

- Samsung Electronics Co. Ltd.

- SK hynix Inc.

- SMIC NOR Foundry Services

- Tower Semiconductor

- ISSI Automotive Grade NOR (China)

- Macron Flash Ltd.

- Cypress Semiconductor Corp.

- Alliance Memory Inc.

- Puya Semiconductor (Shanghai) Co. Ltd.

- Hua Hong Semiconductor Ltd.

- EON Silicon Solution Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automotive OEM-Mandated Flash Quality Targets Driving Design-Ins in Germany and Nordics

- 4.2.2 EU Data-Centric Edge-AI Roll-Outs Elevating Serial NOR Adoption in Industrial PLCs

- 4.2.3 Shift to OTA Firmware Updates in European EVs Boosting High-Density SPI NOR Demand

- 4.2.4 Telecom Open-RAN Deployments in UK and France Requiring Low-Latency Boot Code Storage

- 4.2.5 Medical-Grade Wearables Regulation (MDR) Accelerating Secure NOR Integration

- 4.2.6 EU Chips Act Funding for 28 nm and 45 nm NOR Lines (e.g., Dresden)

- 4.3 Market Restraints

- 4.3.1 Rising 1.8 V NAND Substitutes Below 256 Mb in Consumer IoT Nodes

- 4.3.2 Fab-Level Yield Losses on 28 nm Floating-Gate Nodes Elevating ASP Volatility

- 4.3.3 Tight Allocation of Specialty Photomasks in Europe Hindering Parallel NOR Expansion

- 4.3.4 Post-Brexit Customs Delays Impacting Lead-Times for UK Automotive Tier-1s

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type (Value and Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V-3.6 V)

- 5.4.4 Others - 1.2 V Class (Sub-1.8 V, 2.5 V, 5 V)

- 5.5 By End-User Application (Value and Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-User Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and More

- 5.6.2 65 nm

- 5.6.3 55 nm (Including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

- 5.8 By Country

- 5.8.1 Germany

- 5.8.2 United Kingdom

- 5.8.3 France

- 5.8.4 Italy

- 5.8.5 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Infineon Technologies AG

- 6.4.2 Micron Technology Inc.

- 6.4.3 Winbond Electronics Corp.

- 6.4.4 Macronix International Co. Ltd.

- 6.4.5 GigaDevice Semiconductor Inc.

- 6.4.6 Integrated Silicon Solution Inc.

- 6.4.7 Renesas Electronics Corp.

- 6.4.8 Microchip Technology Inc.

- 6.4.9 Elite Semiconductor Microelectronics Tech. Inc.

- 6.4.10 Samsung Electronics Co. Ltd.

- 6.4.11 SK hynix Inc.

- 6.4.12 SMIC NOR Foundry Services

- 6.4.13 Tower Semiconductor

- 6.4.14 ISSI Automotive Grade NOR (China)

- 6.4.15 Macron Flash Ltd.

- 6.4.16 Cypress Semiconductor Corp.

- 6.4.17 Alliance Memory Inc.

- 6.4.18 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.19 Hua Hong Semiconductor Ltd.

- 6.4.20 EON Silicon Solution Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

德國 NOR Flush:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)東南亞NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)NOR Flush(英國):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)亞太地區NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告印度NOR沖洗液:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)美國NOR快閃記憶體:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031年)NOR閃存在家用電子電器)。工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)