|

市場調查報告書

商品編碼

2066694

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

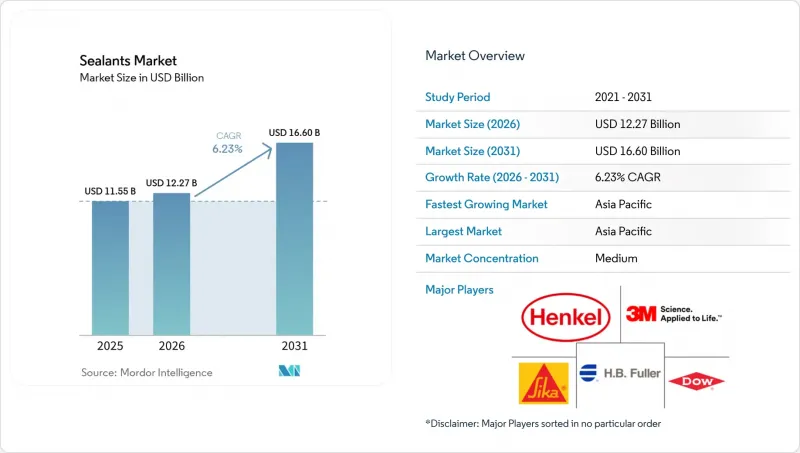

據 Mordor Intelligence 稱,2025 年密封劑市值為 115.5 億美元,預計到 2031 年將達到 166 億美元,而 2026 年為 122.7 億美元,預測期(2026-2031 年)的複合年成長率為 6.23%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂及其他樹脂)、終端用戶行業(航太、汽車、建築、醫療及其他終端用戶行業)和地區(亞太地區、北美、歐洲、南美以及中東和非洲)進行細分。市場預測以美元計價。

全球密封劑市場趨勢及洞察

全球基礎建設投資擴張

各國政府和多邊金融機構正著力製定2025年的基礎建設規劃,與2024年相比,這趨勢愈發明顯。橋面伸縮縫、隧道密封墊和管道密封劑均採用聚硫化物或聚氨酯材料,這些材料能夠承受±50%的位移而不發生內聚破壞。印度的國家基礎設施規劃將資源用於公路、地鐵和港口的現代化改造,所有這些都需要符合ASTM C920 25級標準的堅固連接材料。

中國的「一帶一路」舉措持續為鐵路走廊和深水碼頭建設提供資金,這些項目均指定使用雙組分矽酮密封系統,即使在高濕度環境下也能實現不粘手固化。官民合作關係(PPP)模式縮短了競標週期,使那些能夠儘早獲得基於ISO 11600標準的設計認證的供應商獲得了策略優勢。總體而言,公共部門資本支出的增加擴大了需要初始密封和定期翻新的接縫的安裝基礎,從而擴大了密封劑市場。

電動車的輕量化和多材料黏合

預計到2025年,電池式電動車)的產量將顯著成長。汽車製造商正在用鋁和碳纖維複合材料取代鋼製外殼,但這會帶來電流腐蝕的風險,而機械緊固件無法解決這個問題。結構密封劑能夠黏合不同的基材,吸收振動,並在電池組內部提供介電絕緣,以應對-40 度C至+85 度C之間的反覆溫度波動。諸如SikaPower Flexible Epoxy之類的配方中添加了阻燃填料,可將熱失控逃生時間延長至超過聯合國ECE R100.03標準規定的5分鐘閾值。由於磷酸鋰鐵鋰電池的能量密度較低,設計人員正在透過加長模組和增加密封長度來增加每輛車使用的密封劑用量(以克為單位)。因此,汽車行業為減輕重量、提高靜音和增強安全性所做的努力正在推動密封劑市場收入的穩定成長。

更嚴格的VOC和REACH法規正在推高配方變更的成本。

REACH法規附件十七對室內密封膠的VOC含量設定了限制,而加州1168號法規則規定了更嚴格的限制。重新配製產品以符合這些標準需要大量的投資和時間。這個過程包括加速老化試驗和第三方機構的GREENGUARD評估。以丙酮或叔丁基乙酸酯取代芳香族溶劑會縮短可操作時間。因此,承包商必須調整密封膠的施工速度以防止空隙形成。此外,水性丙烯酸密封膠需要添加殺菌劑和凍融穩定劑,這會使包裝更加複雜並增加原料成本。該地區的製造商缺乏聚合物合成能力,迫使他們以高價購買預先配製的低VOC樹脂。因此,儘管合規產品有望獲得市場佔有率,但密封膠市場的短期盈利仍面臨挑戰。

細分市場分析

到2025年,矽酮產品將佔總銷售量的44.11%,這主要得益於其在高位移接縫、高溫密封墊以及紫外線照射下的外牆等領域作為耐久性標竿的地位。丙烯酸類產品在水性載體(符合50克/公升VOC限值)的推動下,預計到2031年將以6.21%的複合年成長率成長,並正在蠶食矽酮在多孔基材應用領域的市場佔有率。聚氨酯憑藉其耐磨性和可塗漆性的均衡組合,佔據了中端市場,尤其適用於停車場和廣場的接縫。環氧樹脂由於其脆性以及無法承受動態位移,目前仍主要應用於化學和污水處理領域。聚硫化物、丁基樹脂和乳膠丙烯酸樹脂完善了市場,其中聚硫化物樹脂因其低於3克/平方米·天的水蒸氣透過率,在雙層玻璃窗領域佔據了一席之地。 ISO 11600 標準加強了資訊揭露要求,強制樹脂供應商公佈一定溫度範圍內的彈性模量和伸長率曲線,以便規範制定者選擇與計算出的接縫位移相符的產品。為了應對丙烯酸樹脂的崛起,矽酮樹脂製造商正在開發無需等離子處理即可與聚乙烯和聚丙烯黏合的中性固化、免底塗型產品。同時,兼具抗紫外線性能和可塗漆性的混合型矽烷封端聚醚樹脂正在開拓新的細分市場。這些樹脂技術的創新共同造就了蓬勃發展的密封劑市場,有利於那些能夠擴大特殊單體供應的製造商。

區域分析

預計到2025年,亞太地區將佔全球需求的36.13%,並將以7.32%的複合年成長率持續成長至2031年。由於住宅高層建築的建設,中國仍然是消費中心,但由於「綠色建築評估標準」下的新規將密封劑的排放限制在0.05 mg/m³·h*以內,溶劑型密封劑向水性密封劑的轉變正在加速。預計到2025年,印度的汽車產量將創歷史新高,其中電動二輪車和三輪車將佔據大部分佔有率,從而帶動了對電池組密封劑的本地需求,而Pidilight與一家日本矽膠供應商的合資企業正在處理這部分需求。隨著供應鏈多元化,越南和印尼等東南亞國家正在吸引電子和汽車組裝產業,從而推動了對無塵室和導熱等級密封劑需求的成長。即使在日本和韓國等相對成熟的市場,半導體和燃料電池密封劑產業仍保持成長,這些產業依賴超高純度的矽酮。

儘管亞太地區成長領先,但北美和歐洲(預計到2025年將佔總產量的大部分)卻落後於亞太地區。在美國,受《基礎設施投資與就業法案》的推動,需求正穩定成長。該法案為橋樑維修和交通基礎設施維修提供資金,並明確規定使用能夠承受±50%位移的聚氨酯和聚硫黏合劑系統。同時,歐洲旨在2030年提高數百萬棟建築能源效率的「改造浪潮」正在推動對低模量矽酮周邊密封膠的需求,以增強氣密性。此外,REACH法規附件十七要求對配方進行在地化修改,這提高了市場進入門檻,使擁有大型研發規模的成熟企業更具優勢。

剩餘的市場佔有率由南美、中東和非洲佔據。在沙烏地阿拉伯,公共投資基金(PIF)正向NEOM新城和其他大型企劃投入大量資金。這些項目要求使用低模量聚氨酯外牆接縫材料,以應對沙漠地區溫度的劇烈波動。同時,在巴西,海上油氣開發的蓬勃發展推動了對聚硫化物和環氧樹脂類密封劑的需求,尤其是那些耐海水浸泡的密封劑。在南非,對可再生能源的重新關注推動了對用於密封太陽能組件的紫外線穩定矽酮的需求。雖然這些地區的市場規模可能不大,但它們為經驗豐富的複合材料生產商提供了成長機會。那些願意克服惡劣氣候和嚴格技術規範挑戰的公司,可以顯著擴大其在密封劑市場的佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球基礎建設投資成長

- 電動車的輕量化和多材料連接

- 智慧建築對高性能耐候材料的需求

- 亞太地區終端市場的快速擴張

- 引入自動化和機器人點膠生產線

- 市場限制因素

- 更嚴格的VOC和REACH法規正在推高配方變更的成本。

- 矽酮單體價格波動

- 適當應用中熟練勞動力短缺

- 價值鏈分析

- 波特五力模型

- 分銷通路分析

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 馬來西亞

- 泰國

- 印尼

- 新加坡

- 澳洲

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- Avery Dennison

- BASF SE

- Carlisle Companies

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- MAPEI SpA

- Momentive

- Pidilite Industries Ltd

- RPM International

- Saint-Gobain

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding NV

- THE YOKOHAMA RUBBER CO., LTD.

- ThreeBond Holdings Co., Ltd.

- Tremco

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the sealants market size was valued at USD 11.55 billion in 2025 and is estimated to grow from USD 12.27 billion in 2026 to reach USD 16.60 billion by 2031, at a CAGR of 6.23% during the forecast period (2026-2031).

This report is Segmented by Resin (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins), End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (USD).

Global Sealants Market Trends and Insights

Growth in Global Infrastructure Spending

Governments and multilateral lenders committed to infrastructure programs in 2025, showing an increase over 2024. Bridge-deck expansion joints, tunnel gaskets, and pipeline seals all rely on polysulfide or polyurethane grades that tolerate +-50% movement without cohesive failure. India's National Infrastructure Pipeline earmarks resources for highways, metro rail, and port modernization, each requiring robust jointing materials that comply with ASTM C920 Class 25.

China's Belt and Road Initiative continues to fund rail corridors and deep-water terminals that specify two-component silicone systems capable of tack-free cure in high-humidity climates. Public-private partnerships are compressing bid schedules, so suppliers that secure early design approvals under ISO 11600 gain a strategic advantage. Overall, higher public capital outlays enlarge the sealants market by widening the installed base of joints that need initial sealing and periodic renewal.

Lightweighting and Multi-Material Bonding in Electric Vehicles

Battery-electric vehicle production increased significantly in 2025. Automakers are replacing steel closures with aluminum and carbon-fiber composites, creating galvanic-corrosion risks that mechanical fasteners cannot manage. Structural sealants bridge dissimilar substrates, damp vibration, and supply dielectric insulation inside battery packs that cycle between -40 °C and +85 °C. Formulations such as SikaPower flexible epoxies incorporate flame-retardant fillers, extending thermal-runaway escape time beyond the 5-minute threshold set by UN ECE R100.03. As lithium-iron-phosphate chemistries have lower energy density, designers lengthen modules and increase linear seal length, boosting grams-per-vehicle consumption. The automotive drive toward lighter, quieter, and safer platforms, therefore, channels steady incremental revenue to the sealants market.

VOC and REACH Tightening Driving Reformulation Costs

REACH Annex XVII has set a VOC content limit for interior sealants, while California's Rule 1168 imposes an even stricter ceiling. Reformulating products to meet these thresholds requires significant investment and time. This process includes accelerated weathering tests and third-party GREENGUARD evaluations. When aromatic solvents are replaced with acetone or tertiary butyl acetate, the open time decreases. As a result, applicators need to adjust their bead-laying speed to prevent voids. Additionally, water-based acrylics necessitate biocides and freeze-thaw stabilizers, complicating packaging and increasing raw material costs. Producers in the region, lacking polymer synthesis capabilities, are forced to pay a premium for pre-formulated low-VOC resins. Consequently, while compliant products are poised to capture a larger market share, the immediate profitability of the sealants market faces challenges.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Performance Weatherproofing in Smart Buildings

- Rapid Expansion of Asia-Pacific End-Markets

- Silicone Monomer Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone products controlled 44.11% of 2025 volume, confirming their role as the durability benchmark for high-movement joints, high-temperature gaskets, and ultraviolet-exposed facades. Acrylic chemistries, propelled by water-based carriers that meet 50 g/L VOC limits, are advancing at a 6.21% CAGR through 2031, eroding silicone share in porous-substrate applications. Polyurethanes occupy a mid-market niche, balancing abrasion resistance and paintability, which suits parking deck and plaza joints. Epoxies remain confined to chemical-processing and wastewater environments because brittleness restricts dynamic movement. Polysulfides, butyls, and latex acrylics round out the mix, with polysulfides holding a foothold in insulated-glass units thanks to moisture-vapor-transmission rates under 3 g/m2*day. Intensifying disclosure under ISO 11600 forces resin suppliers to publish modulus and elongation profiles across temperatures, enabling specifiers to match products to calculated joint movement. Silicone makers counter the acrylic advance with neutral-cure, primerless grades that adhere to polyethylene and polypropylene without plasma treatment, while hybrid silyl-terminated polyether systems blend UV endurance and paintability to open new niches. Collectively, resin innovation keeps the sealants market dynamic and favors producers able to scale specialty monomer supply.

Geography Analysis

Asia-Pacific accounted for 36.13% of global demand in 2025 and is on track for a 7.32% CAGR to 2031. China continues to headline consumption through residential tower construction, yet new rules from the Green Building Evaluation Standard cap sealant emissions at 0.05 mg/m3*h, accelerating the switch from solvent to water-based systems. India's automotive output hit record vehicles in 2025, with electric two- and three-wheelers comprising a significant portion of the mix, creating local demand for battery-pack sealants serviced by joint ventures between Pidilite and Japanese silicone suppliers. Southeast Asian nations such as Vietnam and Indonesia are attracting electronics and vehicle assembly as supply chains diversify, lifting call-offs for clean-room and thermally conductive grades. Japan and South Korea, relatively mature markets, still see growth in semiconductor and fuel-cell sealing that depends on ultra-pure silicones.

Asia-Pacific leads in growth, while North America and Europe, together accounting for a significant portion of the 2025 volume, lag. The United States, buoyed by the Infrastructure Investment and Jobs Act, is witnessing a steady demand surge. This act funds bridge repairs and transit upgrades, specifically calling for polyurethane and polysulfide joint systems rated for +-50% movement. Meanwhile, Europe's Renovation Wave, aiming for energy upgrades on millions of buildings by 2030, is driving up demand for low-modulus silicone perimeter seals that enhance airtightness. Additionally, REACH Annex XVII is compelling local reformulations, thereby raising entry barriers and bolstering incumbents with their research and development scale.

South America and the Middle East-Africa account for the remaining market share. In Saudi Arabia, the Public Investment Fund has allocated significant resources for NEOM and other mega-projects. These projects mandate low-modulus polyurethane facade joints, designed to withstand desert temperature fluctuations. Over in Brazil, the offshore build-out is pushing the need for polysulfide and epoxy grades, specifically those resistant to seawater immersion. South Africa, on the other hand, is driving demand for UV-stable silicones in photovoltaic module sealing, thanks to its renewed focus on renewable energy. While these regions may be smaller in absolute terms, they present growth opportunities for seasoned formulators. Those willing to navigate the challenges of extreme climates and stringent technical specifications stand to significantly boost their stake in the sealants market.

- 3M

- Arkema

- Avery Dennison

- BASF SE

- Carlisle Companies

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- MAPEI S.p.A.

- Momentive

- Pidilite Industries Ltd

- RPM International

- Saint-Gobain

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Holding N.V.

- THE YOKOHAMA RUBBER CO., LTD.

- ThreeBond Holdings Co., Ltd.

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in global infrastructure spending

- 4.2.2 Lightweighting and multi-material bonding in Electricle Vehicles

- 4.2.3 Demand for high-performance weather-proofing in smart buildings

- 4.2.4 Rapid expansion of Asia-Pacific end-markets

- 4.2.5 Adoption of automated/robotic dispensing lines

- 4.3 Market Restraints

- 4.3.1 VOC and REACH tightening driving reformulation costs

- 4.3.2 Silicone monomer price volatility

- 4.3.3 Skilled-labour gap for correct application

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Distribution Channel Analysis

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-User Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Singapore

- 5.3.1.9 Australia

- 5.3.1.10 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Russia

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison

- 6.4.4 BASF SE

- 6.4.5 Carlisle Companies

- 6.4.6 Dow

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Illinois Tool Works

- 6.4.10 MAPEI S.p.A.

- 6.4.11 Momentive

- 6.4.12 Pidilite Industries Ltd

- 6.4.13 RPM International

- 6.4.14 Saint-Gobain

- 6.4.15 Shin-Etsu Chemical Co., Ltd.

- 6.4.16 Sika AG

- 6.4.17 Soudal Holding N.V.

- 6.4.18 THE YOKOHAMA RUBBER CO., LTD.

- 6.4.19 ThreeBond Holdings Co., Ltd.

- 6.4.20 Tremco

- 6.4.21 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)