|

市場調查報告書

商品編碼

2066686

日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Japan Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

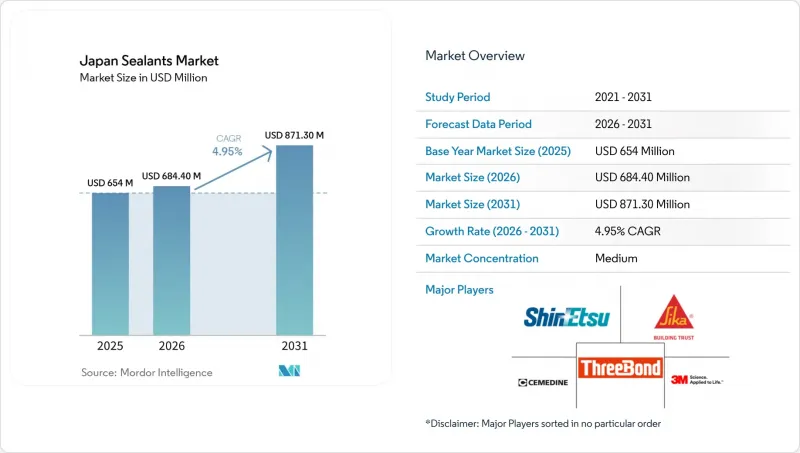

根據 Mordor Intelligence 預測,日本密封膠市場規模將從 2025 年的 6.54 億美元成長到 2026 年的 6.844 億美元,然後在 2031 年達到 8.713 億美元,2026 年至 2031 年的複合年成長率為 4.95%。

本報告按樹脂類型(矽樹脂、聚氨酯樹脂、丙烯酸樹脂、環氧樹脂、聚硫化物樹脂及其他樹脂)和終端用戶產業(航太、汽車、建築、醫療、電子半導體及其他終端用戶產業)進行細分。市場預測以美元計價。

日本密封膠市場趨勢與洞察

住宅抗震維修費用飆漲。

日本國土交通省已累計1,125億日圓(約7.55億美元)用於2025會計年度基於GX ZEH計畫的門窗及隔熱材料維修津貼。鑑於2024年能登半島地震中剛性接縫放大了剪切力,抗震維修隔震系統與高流動性密封劑結合的趨勢日益明顯。 CemedyneCEMEDINE CO., LTD.於2024年推出的「扇貝密封」聚氨酯產品,以煅燒扇貝殼為填充材,實現了水產養殖廢棄物的再利用,同時保持了30-35的邵氏A硬度,並可適應±25%的接縫位移。單組分濕固化聚氨酯可將雙組分環氧樹脂的混合誤差降低40%,目前已成為維修工程的主流選擇。隨著 GX ZEH 的獲批,2024 年第三季國內建築密封膠出貨量比上年同期成長 6%。

促進日本電動車和混合動力汽車產業的減重

2025年,名古屋大學證明,奈米纖維素增強環氧樹脂的衝擊強度是傳統黏合劑的22倍,使得開發鋁製輪圈蓋成為可能,每輛車可減重8-12公斤。豐田計劃在其下一代電池式電動車平台上將黏合劑的黏合面積增加30%。豐田將優先使用聚氨酯和改性矽酮,以防止在-40 度C至+120 度C的溫度範圍內電流腐蝕。積水富勒的「EV Protect 4006 SFR」符合UL 94 V-0標準,同時僅增加60千瓦時電池組不到2公斤的重量。 2024年,汽車密封劑的需求推動日本黏合劑產量增加2.7%,但由於轉向無溶劑反應型熱熔膠,乳液型產品的產量下降了6%。

石化原料價格波動

2025年8月,日本石腦油價格較去年同期下跌12.8%,至每噸85,800日圓(約每噸575美元),但在2026年3月霍爾木茲海峽封鎖後,價格飆升66%。由於聚氨酯密封劑的價格與苯和丙烯的價格走勢密切相關,原油價格每桶30美元的變動會導致成本變化15%至20%,這使得小規模生產商難以有效對沖風險。 2026年3月,積水富勒公司將原料前置作業時間延長至14至16週,並限制了電池製造商的供貨。跨國企業正轉向使用蓖麻油衍生的生物基多元醇,而日本國內的中小型企業則轉向使用本地採購的矽砂生產的矽酮。

細分市場分析

矽酮密封膠憑藉其卓越的抗紫外線性能和對玻璃、金屬及不同基材的優異黏合性,預計到2025年將佔據日本密封膠市場38.5%的佔有率。聚氨酯密封膠,尤其是獲得UL 94 V-0認證的電動車電池組的雙組分產品,預計到2031年將以每年6.02%的速度成長。丙烯酸密封膠仍是室內細木工的首選,但由於其±7.5%的位移容差不符合抗震標準,其市佔率很少超過個位數。環氧樹脂和聚硫化物密封膠在化學品密封領域佔有一定的市場佔有率,但目前二者總合市佔率仍低於5%。

矽酮在高階應用領域,例如磁浮列車的隧道接縫、半導體封裝以及太陽能組件的邊緣密封,仍然佔據主導地位。聚氨酯領域的創新技術,例如積水富勒的“EV Protect 4006 SFR”,正在滿足矽酮無法經濟有效地滿足的汽車輕量化需求。矽烷封端聚合物的興起,憑藉其與聚硫化物相當的耐化學性以及更複雜的混合工藝,正在蠶食聚硫化物的市場佔有率。總而言之,樹脂的多樣化並未削弱矽酮的主導地位;相反,它透過開拓新的性能領域,擴大了日本密封劑市場的整體規模。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 終端用戶趨勢

- 市場促進因素

- 用於住宅抗震改造的支出正在激增。

- 日本電動車和混合動力汽車產業的輕量化努力

- 由於先進醫療設備的出口,對醫用密封劑的需求增加。

- 低揮發性有機化合物(VOC)獎勵適用於淨零能耗住宅

- 新幹線和磁浮列車對矽酮防水材料的需求

- 市場限制因素

- 石化原料價格波動

- 嚴格的PRTR和VOC排放標準

- 由於熟練安裝人員人手不足,安裝成本不斷上漲。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 矽酮

- 聚氨酯

- 丙烯酸纖維

- 環氧樹脂

- 多硫化物

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 電子和半導體

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介(包括全球概覽、市場概覽、主要業務板塊、財務資訊、策略資訊、產品和服務以及近期發展動態)

- 3M

- Arkema

- CEMEDINE Co.,Ltd.

- Dow

- HB Fuller

- Henkel AG & Co. KGaA

- Konishi Co., Ltd.

- Momentive

- Nichiban Co., Ltd.

- Sekisui Fuller

- Sharp Chemical Ind. Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Sumitomo Bakelite Co., Ltd.

- Taisei Polytech Co., Ltd.

- The Yokohama Rubber Co., Ltd.

- ThreeBond Holdings Co., Ltd.

- Tokuyama Corporation

- Wacker Chemie AG

- Yokohama Industrial Products

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan sealants market size is expected to grow from USD 654 million in 2025 to USD 684.40 million in 2026 and is forecast to reach USD 871.30 million by 2031 at 4.95% CAGR over 2026-2031.

This report is Segmented by Resin Type (Silicone, Polyurethane, Acrylic, Epoxy, Polysulfide, and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, Electronics and Semiconductor, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Japan Sealants Market Trends and Insights

Surging Renovation Spend on Earthquake-Resilient Housing

Japan's Ministry of Land, Infrastructure, Transport and Tourism allocated JPY 112.5 billion (USD 755 million) in FY 2025 to subsidize window and insulation retrofits under the GX ZEH scheme. Seismic upgrades increasingly pair base-isolation systems with high-movement-capacity sealants because rigid joints amplified shear forces during the 2024 Noto Peninsula quake. Cemedine's Scallop Seal polyurethane, launched in 2024 with calcined scallop-shell filler, diverts aquaculture waste and delivers Shore A 30-35 while meeting +-25% joint movement. One-component moisture-cure polyurethanes now dominate retrofit jobs since they eliminate 40% of the mixing errors seen with two-part epoxies. GX ZEH approvals boosted domestic building-sealant shipments 6% year-on-year in Q3 2024.

Light-Weighting Push in Japan's EV and Hybrid Auto Sector

Nagoya University proved in 2025 that nanocellulose-reinforced epoxy delivers 22 times the impact strength of legacy adhesives, enabling aluminum closures that remove 8-12 kg per vehicle. Toyota will raise adhesive-bonded surface area by 30% on its next battery-electric platform, favoring polyurethanes and modified silicones that prevent galvanic corrosion across -40 °C to +120 °C. Sekisui Fuller's EV Protect 4006 SFR adds under 2 kg to a 60 kWh pack while meeting UL 94 V-0. Automotive sealant consumption helped lift Japan's adhesive output 2.7% in 2024, even as emulsion systems fell 6% with the switch to solvent-free reactive hot melts.

Petrochemical Feedstock Price Volatility

Japan's naphtha fell 12.8% year-on-year to JPY 85,800/ton (USD 575/ton) in Aug 2025 but spiked 66% after the March 2026 Strait of Hormuz disruption. Polyurethane sealants track benzene and propylene, so a USD 30 bbl crude move swings costs 15-20%, and smaller producers cannot hedge effectively. Sekisui Fuller lengthened raw-material lead times to 14-16 weeks and rationed shipments to battery customers in Mar 2026. Multinationals are shifting toward bio-based polyols from castor oil, while domestic SMEs pivot to silicones that depend on local silica-sand feedstock.

Other drivers and restraints analyzed in the detailed report include:

- Medical-Grade Sealants Demand from Advanced Device Exports

- Low-VOC Incentives for Net-Zero Energy Houses

- Skilled Applicator Labor Shortage Elevating Installation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicones captured 38.5% of the Japan sealants market in 2025, reflecting unmatched UV stability and adhesion to glass, metal, and dissimilar substrates. Polyurethanes are expanding at 6.02% annually through 2031, aided by UL 94 V-0 two-component grades for EV battery packs. Acrylics remain favored in interior joinery but rarely exceed a mid-single-digit share because +-7.5% movement capacity fails seismic codes. Epoxies and polysulfides fill chemical-containment niches yet now represent below 5% combined volume.

Silicones keep commanding premium applications such as maglev tunnel joints, semiconductor encapsulation, and photovoltaic module edge-sealing. Polyurethane innovation, typified by Sekisui Fuller EV Protect 4006 SFR, captures lightweighting demand in automobiles that silicones cannot meet economically. The rise of silane-terminated polymers is eroding polysulfide presence by delivering similar chemical resistance without mixing complexity. Overall, resin diversification has not dented silicone leadership; instead, it is expanding total Japan sealants market size by opening new performance windows.

List of Companies Covered in this Report:

- 3M

- Arkema

- CEMEDINE Co.,Ltd.

- Dow

- H.B. Fuller

- Henkel AG & Co. KGaA

- Konishi Co., Ltd.

- Momentive

- Nichiban Co., Ltd.

- Sekisui Fuller

- Sharp Chemical Ind. Co., Ltd.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Sumitomo Bakelite Co., Ltd.

- Taisei Polytech Co., Ltd.

- The Yokohama Rubber Co., Ltd.

- ThreeBond Holdings Co., Ltd.

- Tokuyama Corporation

- Wacker Chemie AG

- Yokohama Industrial Products

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 End-user Trends

- 4.3 Market Drivers

- 4.3.1 Surging renovation spend on earthquake-resilient housing

- 4.3.2 Light-weighting push in Japan's EV and hybrid auto sector

- 4.3.3 Medical-grade sealants demand from advanced device exports

- 4.3.4 Low-VOC incentives for Net-Zero Energy Houses

- 4.3.5 Silicone demand for Shinkansen and maglev tunnel waterproofing

- 4.4 Market Restraints

- 4.4.1 Petrochemical feedstock price volatility

- 4.4.2 Stringent PRTR and VOC emission norms

- 4.4.3 Skilled applicator labour shortage elevating installation costs

- 4.5 Value Chain Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Silicone

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Epoxy

- 5.1.5 Polysulfide

- 5.1.6 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Electronics and Semiconductor

- 5.2.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 CEMEDINE Co.,Ltd.

- 6.4.4 Dow

- 6.4.5 H.B. Fuller

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Konishi Co., Ltd.

- 6.4.8 Momentive

- 6.4.9 Nichiban Co., Ltd.

- 6.4.10 Sekisui Fuller

- 6.4.11 Sharp Chemical Ind. Co., Ltd.

- 6.4.12 Shin-Etsu Chemical Co., Ltd.

- 6.4.13 Sika AG

- 6.4.14 Sumitomo Bakelite Co., Ltd.

- 6.4.15 Taisei Polytech Co., Ltd.

- 6.4.16 The Yokohama Rubber Co., Ltd.

- 6.4.17 ThreeBond Holdings Co., Ltd.

- 6.4.18 Tokuyama Corporation

- 6.4.19 Wacker Chemie AG

- 6.4.20 Yokohama Industrial Products

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)