|

市場調查報告書

商品編碼

2066687

泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Thailand Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

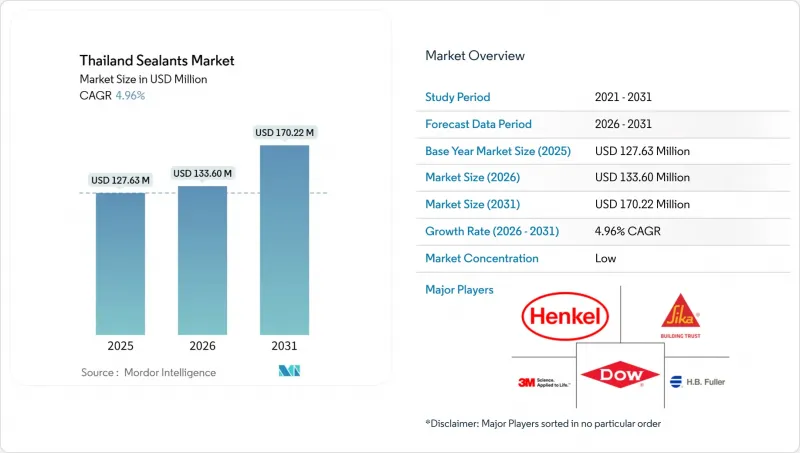

根據 Mordor Intelligence 預測,泰國密封膠市場規模將從 2025 年的 1.2763 億美元成長到 2026 年的 1.336 億美元,到 2031 年達到 1.7022 億美元,2026 年至 2031 年的複合年成長率為 4.96%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂、混合樹脂及其他樹脂)和終端用戶行業(航太、汽車、建築施工、電子電氣、醫療保健及其他終端用戶行業)進行細分。市場預測以美元計價。

泰國密封膠市場趨勢與洞察

泰國東部經濟走廊(EEC)基礎建設蓬勃發展

2025年,東部經濟走廊(EEC)已吸引總額達602.3億美元的投資申請,引導資金流向諸如WHA ESIE 5等智慧園區。資料中心外殼結構接縫處需要使用耐火密封膠,電纜穿牆處需要使用防火/防水密封膠,而電池潔淨室則需要使用離子控制矽酮配方。泰國的「快速通行證」(FastPass)系統可將許可證核准時間縮短高達50%,並優先考慮擁有本地庫存且能提供現場技術服務的供應商。框架合約目前是主要的採購方式,透過儘早確定性能規範,減少了專案進行過程中使用替代品的情況。

汽車和電動車生產廠商擴大生產規模

比亞迪和廣汽集團於2024年7月在泰國開設了一條組裝線,以支持泰國政府的「30@30」目標,該目標將獎勵與國內採購比例掛鉤。電池組密封需要使用矽酮和聚氨酯材料,這些材料必須在-40 度C至+90 度C的溫度範圍內保持黏合力,並符合UL 94 V-0標準。科思創計畫收購位於羅勇府的Vencorex HDI工廠,這將確保雙組分聚氨酯系統所需的脂肪族異氰酸酯的供應。電動車生產線中使用的六軸機器人對黏度控制有嚴格的要求,這提高了本地混煉廠商的品管標準。

石油化工原料價格波動對利潤率帶來壓力。

2024年石腦油均價為每噸674美元,但2025年上半年跌至每噸607美元。同時,丙烯和聚氯乙烯(PVC)價格居高不下,導致加工商毛利率下降200-300個基點。像TOA Paint將庫存週期延長至120天,體現了對沖供應風險的策略。再生高密度聚乙烯(HDPE)使用量的增加,以及ISCC Plus認證成本的上升,都加劇了市場波動。

細分市場分析

到2025年,矽酮將佔據泰國密封膠市場40.50%的佔有率。這個市場主要受電子產業群聚和城市外牆的主導,電子產業叢集需要將離子污染控制在10 ppm以下,而都市區外牆則需要紫外線穩定性。混合樹脂和其他樹脂的市場佔有率將以6.76%的複合年成長率成長,直至2031年,因為承包商優先考慮±25%的拉伸性和麵漆適用性。西卡(Sika)的「Hybriflex SMP」正是這一轉變的體現,它將聚氨酯的韌性與矽酮的耐候性相結合。聚氨酯系統在電動車電池組領域仍佔據主導地位。在該領域,來自科思創(Covestro)羅勇工廠(即將關閉)的脂肪族異氰酸酯正在減少固化時間的波動。丙烯酸類產品在DIY通路佔據主導地位,但家庭債務限制了自由裁量權裝修支出。環氧樹脂在瑪塔普(Map Ta Phut)化工廠仍然是小眾產品,因為該工廠對耐化學性要求很高。

法規和產能趨勢進一步強化了這些趨勢。瓦克位於張家港的新型特種矽酮混煉廠及其位於金川的生產線提高了純度標準,迫使當地混煉企業達到類似的水平。波士特公司獲得EC1 PLUS和M1認證的混合型產品,其生物基含量高達46%,標誌著產業正朝著永續性正在改變高級產品的競標。泰國工業標準協會(TIS)的TIS 1321-2566標準將於2024年3月生效,該標準新增了黏合力測試要求,迫使小規模的混煉企業將這項測試外包,從而延長了產品上市週期。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 泰國的東部經濟走廊(EEC)計畫正在推動基礎建設熱潮。

- 汽車製造商擴大電動車生產

- 都市區高層建築和公寓的翻新需要高品質的防水措施。

- 電子產品出口叢集正在推動對高純度矽酮密封劑的需求。

- DIY零售市場透過電子商務平台快速成長,帶動了小批量壓克力產品的銷售。

- 市場限制因素

- 石油化工原料價格波動對利潤率帶來壓力。

- 對揮發性有機化合物和化學品的更嚴格監管增加了配方變更的成本。

- 合格承包商短缺

- 價值鏈分析

- 分銷通路分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 混合樹脂和其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 電子電器設備

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- BASF SE

- Covestro AG

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- ITW Polymers Sealants

- MAPEI SpA

- Meridian Adhesives Group(PAS Bangkok Co.)

- Momentive Performance Materials Inc.

- Pidilite Industries Ltd.

- Plic Firston(Thailand)Co., Ltd.

- SCG Chemicals PCL

- Selic Corp PCL

- Shin-Etsu Chemical Co., Ltd.

- Siam Polyurethane Co., Ltd.

- Sika AG

- Soudal Group

- The Yokohama Rubber Co., Ltd.(Hamatite)

- TOA Paint(Thailand)PCL

- Uniseal Co., Ltd.

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the thailand sealants market size is projected to grow from USD 127.63 million in 2025 to USD 133.60 million in 2026, and reach USD 170.22 million by 2031, growing at a CAGR of 4.96% from 2026 to 2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Hybrid and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Electronics and Electrical, Healthcare, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Thailand Sealants Market Trends and Insights

Infrastructure Boom Under Thailand's Eastern Economic Corridor

The EEC attracted USD 60.23 billion of investment applications in 2025, channeling capital into smart estates such as WHA ESIE 5. Data-center shells specify fire-rated joint sealants and cable-penetration firestops, while battery cleanrooms call for ionic-controlled silicone formulations. Thailand FastPass cuts permit times by up to 50%, favoring suppliers that hold local inventory and offer on-site technical service. Framework agreements now dominate procurement, locking in performance specifications early and reducing mid-project substitutions.

Automotive-EV Production Expansion by OEMs

BYD and GAC Aion inaugurated Thai assembly in July 2024, underpinning a national 30@30 target that ties incentives to domestic content. Battery-pack sealing requires silicone and polyurethane chemistries that retain adhesion from -40 °C to +90 °C and meet UL 94 V-0. Covestro's planned acquisition of the Vencorex HDI site in Rayong secures aliphatic isocyanate supply for two-component polyurethane systems. Automated six-axis robots on EV lines demand tight viscosity control, raising quality-system thresholds for local compounders.

Petrochemical Feedstock Volatility Compressing Margins

Naphtha averaged USD 674 per ton in 2024, dipping to USD 607 in H1 2025, yet propylene and PVC remained high, trimming converter gross margins by 200-300 bps. Extended inventories to 120 days, as practiced by TOA Paint, reflect supply-risk hedging. Increased recycled-HDPE use introduces certification costs under ISCC Plus, adding further variability.

Other drivers and restraints analyzed in the detailed report include:

- Urban High-Rise and Condominium Renovations

- Electronics Export Clusters Fueling High-Purity Silicone Demand

- Stricter VOC and Chemical Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone captured 40.50% of the Thailand sealants market in 2025, ruled by electronics clusters that require less than 10 ppm ionic contamination and urban facades that demand UV stability. Hybrid and other resins are advancing at a 6.76% CAGR through 2031 as contractors value +-25% movement and over-paintability. Sika's Hybriflex SMP demonstrates this shift by blending polyurethane toughness with silicone weatherability. Polyurethane systems remain entrenched in EV battery packs, where aliphatic isocyanates sourced from Covestro's soon-to-close Rayong site reduce cure-time variability. Acrylic dominates DIY channels, though household debt curbs discretionary renovations. Epoxies stay niche for Map Ta Phut chemical plants that need strong chemical resistance.

Regulatory and capacity moves reinforce these patterns. Wacker's new specialty-silicones complex in Zhangjiagang and Jincheon lines ratchet purity benchmarks, pressing local mixers to match. Bostik's 46% bio-based hybrid with EC1 PLUS and M1 certification signals the sustainability pivot transforming premium bids. The Thailand Industrial Standards Institute's TIS 1321-2566 enforcement from March 2024 adds adhesion-test hurdles that smaller compounders must outsource, lengthening product-launch cycles.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF SE

- Covestro AG

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- ITW Polymers Sealants

- MAPEI S.p.A.

- Meridian Adhesives Group (PAS Bangkok Co.)

- Momentive Performance Materials Inc.

- Pidilite Industries Ltd.

- Plic Firston (Thailand) Co., Ltd.

- SCG Chemicals PCL

- Selic Corp PCL

- Shin-Etsu Chemical Co., Ltd.

- Siam Polyurethane Co., Ltd.

- Sika AG

- Soudal Group

- The Yokohama Rubber Co., Ltd. (Hamatite)

- TOA Paint (Thailand) PCL

- Uniseal Co., Ltd.

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure boom under Thailand's Eastern Economic Corridor (EEC) programme

- 4.2.2 Automotive-EV production expansion by OEMs

- 4.2.3 Urban high-rise and condominium renovations demanding premium weather-proofing

- 4.2.4 Electronics export clusters fuelling demand for high-purity silicone sealants

- 4.2.5 DIY-retail surge via e-commerce platforms boosting small-pack acrylic sales

- 4.3 Market Restraints

- 4.3.1 Petrochemical feed-stock price volatility compressing margins

- 4.3.2 Stricter VOC and chemical compliance raising reformulation costs

- 4.3.3 Shortage of certified applicators

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Hybrid and Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Electronics and Electrical

- 5.2.5 Healthcare

- 5.2.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Covestro AG

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 ITW Polymers Sealants

- 6.4.9 MAPEI S.p.A.

- 6.4.10 Meridian Adhesives Group (PAS Bangkok Co.)

- 6.4.11 Momentive Performance Materials Inc.

- 6.4.12 Pidilite Industries Ltd.

- 6.4.13 Plic Firston (Thailand) Co., Ltd.

- 6.4.14 SCG Chemicals PCL

- 6.4.15 Selic Corp PCL

- 6.4.16 Shin-Etsu Chemical Co., Ltd.

- 6.4.17 Siam Polyurethane Co., Ltd.

- 6.4.18 Sika AG

- 6.4.19 Soudal Group

- 6.4.20 The Yokohama Rubber Co., Ltd. (Hamatite)

- 6.4.21 TOA Paint (Thailand) PCL

- 6.4.22 Uniseal Co., Ltd.

- 6.4.23 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)