|

市場調查報告書

商品編碼

2066679

德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Germany Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

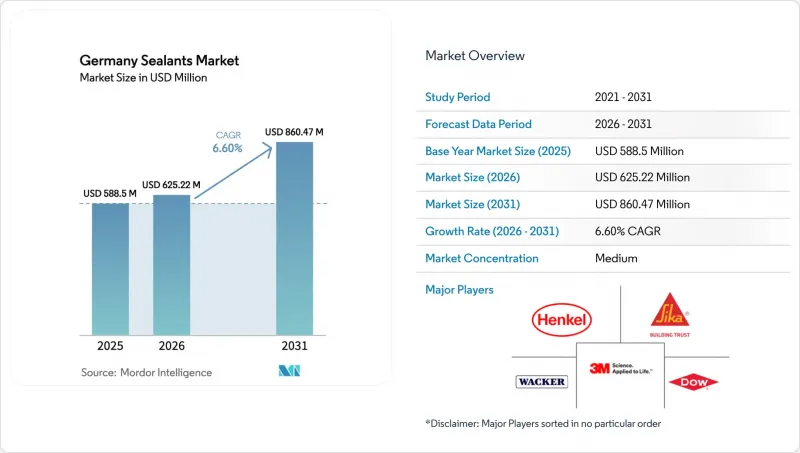

據 Mordor Intelligence 稱,2025 年德國密封劑市值為 5.885 億美元,預計到 2031 年將達到 8.6047 億美元,而 2026 年為 6.2522 億美元,預測期(2026-2031 年)的複合年成長率為 6.60%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂及其他樹脂)和終端用戶行業(航太、汽車、建築、醫療及其他終端用戶行業)進行細分。市場預測以美元計價。

德國密封劑市場的趨勢與洞察

節能維修工程蓬勃發展

德國的維修率缺口(到2025年僅0.67%,政策目標是2%)催生了對氣密性膜、窗框伸縮縫和外牆密封膠的潛在需求,這些產品需不含塑化劑遷移,並能承受-20 度C至+80 度C的溫度。一項5000億歐元的現代化計畫每年撥款20億歐元用於社會住宅維修,並額外撥款32.5億歐元用於橋樑和隧道維修,直至2029年,這為基礎設施密封膠市場提供了多年穩定的市場需求前景。德國的「建築工程補貼計畫」(BEG)已延長至2029年,目前涵蓋太陽能發電系統、熱泵管道和機械通風系統介面的穿孔,這些都需要專用密封墊。根據《德國聯邦產品法規》(CPR 2024/3110),數位產品護照將從2026年起逐步實施,要求供應商披露「隱含碳含量」和「可回收性」等信息,這些規定已對公開競標影響。西卡公司為慕尼黑馬里恩霍夫輕軌項目採用的低排放系統表明,生命週期報告如何將永續性數據轉化為競標中的決定性差異化因素。

汽車輕量化及電動車的墊片要求

電池外殼、電力電子外殼以及電芯到電池組的整體設計需要超過 20 kV/mm 的介電強度和 -40 度C至 +105 度C的耐冷卻液性能,這推動了對不含異氰酸酯的聚氨酯和 STP 化學品的轉向,以滿足即將訂定的 PFAS 法規。漢高杜塞爾多夫電池工程中心能夠快速為多材料外殼客製化熱界面材料和密封化合物。 Erling Klinger 的「MetaloBond」混合墊片在 200 度C下具有超過 15 N/mm 的剝離強度,適用於高速馬達外殼。德國一級供應商正擴大將這些解決方案出口到中國電動車製造商,隨著他們拓展中國市場(預計到 2030 年,中國市場將佔全球銷量的三分之一),其成長速度超過了國內汽車生產。那些率先採用阻燃和電壓絕緣平台的公司正在確保其設計在全球範圍內得到應用,這為德國密封劑市場的長期成長奠定了基礎。

高波動性異氰酸酯和矽酮原料價格

2026年第一季,矽酮DMC價格較去年同期上漲28%。這主要是由於太陽能級矽的需求量佔矽總產量的28%,以及陶氏化學位於威爾斯巴里工廠的關閉導致歐洲矽供應減少15萬噸。由於中國供應超過70%的金屬矽,德國複合材料生產商容易受到新疆和四川發行限制造成的供應中斷的影響。原油價格波動和環境檢查導致TDI和MDI價格飆升,對聚氨酯利潤率造成壓力。尚未後向整合的公司正在退出通用填縫材料市場,轉而專注於以規格主導的德國密封劑市場,而中型企業仍然面臨原料前置作業時間延長導致的營運資金短缺問題。

細分市場分析

到2031年,聚氨酯基產品將以7.24%的複合年成長率成長,這主要得益於STP混合型產品的推出,該產品無需處理異氰酸酯。矽酮密封膠憑藉其在帷幕牆玻璃和電池組墊片等應用中無與倫比的-60 度C至+250 度C的工作溫度範圍,在2025年仍將佔據德國密封膠市場37.5%的佔有率。瓦克化學位於努克里茨的全新STP-E生產線新增了15千噸產能,標誌著其生產重心正轉向兼具矽酮抗紫外線穩定性和聚氨酯韌性的混合型產品。環氧樹脂密封膠在工業地板接縫和航太複合材料燃料箱領域仍佔有一席之地,而丙烯酸密封膠因其成本低廉且易於塗漆,仍然是室內裝飾應用的首選。在供應商研發方面,環氧聚氨酯網路和矽烷改質聚醚等化學結構的整合正在取得進展,模糊了樹脂之間的明確界限,並擴大了德國密封劑市場的整體應用範圍。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 節能維修建設熱潮

- 輕型汽車和電動車對墊片的需求。

- 醫療一次性用品和藥品包裝的成長

- 由於建築法規更加嚴格,低揮發性有機化合物和生物基密封劑正在推廣。

- 離岸風力發電機葉片維修用密封劑的需求

- 市場限制因素

- 高波動性異氰酸酯和矽酮原料價格

- 高效能感壓膠帶的可用性作為一種替代方案

- 歐盟關於反應性樹脂的微塑膠法規提案

- 技術純熟勞工短缺,無法正確塗抹密封劑

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- Dow

- EGO Dichtstoffwerke GmbH & Co. KG

- HB Fuller Company

- Henkel AG & Co. KGaA

- MAPEI SpA

- Sika AG

- Soudal NV

- Wacker Chemie AG

- Tremco Illbruck GmbH

- Otto Chemie

- BASF SE(construction chemicals)

- PPG Industries(Sealants Europe)

- DAP Products

- Pecora Corporation

- Selena Group

- Kommerling Chemische Fabrik

- Dymax Europe GmbH

- Soudal(illbruck)

第7章 市場機會與未來展望

According to Mordor Intelligence, the germany sealants market size was valued at USD 588.5 million in 2025 and is estimated to grow from USD 625.22 million in 2026 to reach USD 860.47 million by 2031, at a CAGR of 6.60% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Germany Sealants Market Trends and Insights

Construction Boom in Energy-Efficient Renovations

Germany's renovation-rate gap, 0.67% in 2025 versus the 2% policy target, creates pent-up demand for airtight membranes, window-frame expansion joints and facade seals that survive -20 °C to +80 °C without plasticizer migration. The EUR 500 billion modernization plan earmarks EUR 2 billion a year to 2029 for social-housing upgrades plus EUR 3.25 billion for bridge and tunnel refurbishment, locking in multi-year visibility for infrastructure-grade sealants. BEG subsidies extend to 2029 and now cover photovoltaic penetrations, heat-pump ducts and mechanical-ventilation interfaces, each requiring specialized gaskets. Digital product passports under CPR 2024/3110 start phasing in from 2026, forcing vendors to disclose embodied-carbon and recyclability credentials that already influence public tenders. Sika's low-emission systems on Munich's Marienhof S-Bahn project illustrate how lifecycle reporting is turning sustainability data into a hard-bid differentiator.

Automotive Lightweighting and E-Mobility Gasketing Needs

Battery housings, power-electronics cases and cell-to-pack designs impose dielectric strength above 20 kV/mm and coolant resistance from -40 °C to +105 °C, prompting a switch to isocyanate-free polyurethane and STP chemistries that also meet upcoming PFAS restrictions. Henkel's Dusseldorf Battery Engineering Centre enables rapid prototyping of thermal-interface and sealing compounds customized for multi-material bodies. ElringKlinger's MetaloBond hybrid gasket delivers peel strength over 15 N/mm at 200 °C, supporting high-speed e-motor housings. Germany's Tier-1s increasingly export these solutions to Chinese EV makers, expected to hold one-third of global sales by 2030, amplifying growth beyond domestic vehicle production. Early movers with flame-retardant, voltage-isolation compliant platforms are locking in global design wins that underpin the Germany sealants market long term.

Volatile Isocyanate and Silicone Feedstock Prices

Silicone DMC climbed 28% year-on-year in Q1 2026 as solar-grade demand hit 28% of total silicone output while Dow's Barry, Wales shutdown removed 150 kt of European supply. China provides over 70% of silicon metal, leaving German formulators exposed to Xinjiang and Sichuan power rationing disruptions. Parallel spikes in TDI and MDI, driven by oil volatility and environmental inspections, squeeze polyurethane margins. Firms lacking backward integration are retreating from commodity caulks to focus on the specification-led Germany sealants market, but mid-tier players still face working-capital strain from longer raw-material lead times.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare Single-Use Devices and Pharma Packaging Growth

- Stricter Bauordnungen Pushing Low-VOC / Bio-Based Sealants

- Availability of High-Performance Pressure-Sensitive Tapes as Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane formulations are growing at 7.24% CAGR through 2031, anchored by STP hybrids that eliminate isocyanate handling. Silicone maintained a 37.5% Germany sealants market share in 2025 owing to unmatched -60 °C to +250 °C service windows in facade glazing and battery-pack gasketing. Wacker Chemie's new STP-E line at Nunchritz adds 15 kiloton incremental capacity and illustrates a capital pivot into hybrids that bridge silicone UV stability and polyurethane toughness. Epoxy sealants keep a niche in industrial-floor joints and aerospace composite fuel tanks, while acrylics remain preferred for interior trim owing to paintability at low cost. Supplier research and development increasingly merges chemistries, epoxy-polyurethane networks or silane-modified polyethers, blurring hard resin boundaries yet widening application coverage across the Germany sealants market.

List of Companies Covered in this Report:

- 3M

- Arkema

- Dow

- EGO Dichtstoffwerke GmbH & Co. KG

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- MAPEI S.p.A.

- Sika AG

- Soudal NV

- Wacker Chemie AG

- Tremco Illbruck GmbH

- Otto Chemie

- BASF SE (construction chemicals)

- PPG Industries (Sealants Europe)

- DAP Products

- Pecora Corporation

- Selena Group

- Kommerling Chemische Fabrik

- Dymax Europe GmbH

- Soudal (illbruck)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Construction boom in energy-efficient renovations

- 4.2.2 Automotive lightweighting and e-mobility gasketing needs

- 4.2.3 Healthcare single-use devices and pharma packaging growth

- 4.2.4 Stricter Bauordnungen pushing low-VOC / bio-based sealants

- 4.2.5 Offshore wind-turbine blade repair sealants demand

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate and silicone feedstock prices

- 4.3.2 Availability of high-performance pressure-sensitive tapes as substitutes

- 4.3.3 EU micro-plastic restriction proposals for reactive resins

- 4.3.4 Skilled-labour shortage for correct sealant installation

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Dow

- 6.4.4 EGO Dichtstoffwerke GmbH & Co. KG

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 MAPEI S.p.A.

- 6.4.8 Sika AG

- 6.4.9 Soudal NV

- 6.4.10 Wacker Chemie AG

- 6.4.11 Tremco Illbruck GmbH

- 6.4.12 Otto Chemie

- 6.4.13 BASF SE (construction chemicals)

- 6.4.14 PPG Industries (Sealants Europe)

- 6.4.15 DAP Products

- 6.4.16 Pecora Corporation

- 6.4.17 Selena Group

- 6.4.18 Kommerling Chemische Fabrik

- 6.4.19 Dymax Europe GmbH

- 6.4.20 Soudal (illbruck)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)