|

市場調查報告書

商品編碼

2066688

馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Malaysia Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

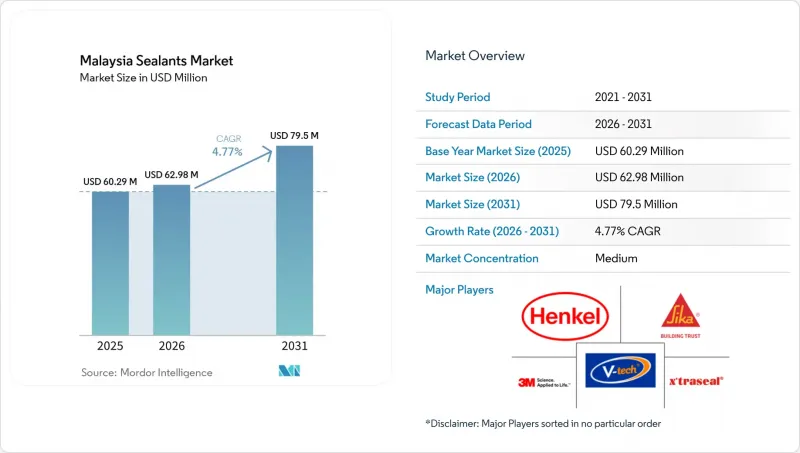

據 Mordor Intelligence 稱,馬來西亞密封劑市場在 2025 年的價值為 6,029 萬美元,預計到 2031 年將達到 7,950 萬美元,而 2026 年為 6,298 萬美元,預測期(2026-2031 年)的複合年成長率為 4.7%。

本報告按樹脂類型(矽酮、聚氨酯、丙烯酸酯、環氧樹脂及其他)和終端用戶產業(航太、汽車、建築、醫療、電子電氣及其他終端用戶產業)進行細分。市場預測以美元計價。

馬來西亞密封膠市場趨勢及洞察

公共部門大型企劃的激增推高了對建築密封劑的需求。

東海岸鐵路(ECRL)將於2026年初完成92.62%,其中高架橋、隧道和車站建築的外牆大量使用密封膠,投資額達502.7億馬幣(約113億美元)。雖然諸如捷運3號線(MRT-3)和新山-新加坡捷運系統連接線(JRT-SLC)等並行項目進一步推高了需求,但真正推動這一變化的動力是“70%工業化建築系統(IBS)要求”,該要求將接縫密封工作從戶外現場轉移到溫控工廠。可控的固化製程減少了返工,縮短了專案週期,並有利於那些精通自動化點膠的供應商。新加坡建築業發展局(CIDB)的「2025年能力標準」將建築資訊模型(BIM)技術能力納入承包商執照要求,使不良的接縫設計不再只是保固問題,而是合規風險。

醫療設備出口的蓬勃發展帶動了對可消毒矽膠的需求。

馬來西亞醫療設備出口額在2024年達到370億令吉,自2021年馬幣馬幣。這導致市場對符合FDA標準的矽酮密封劑的需求增加,此類密封劑即使在134 度C下反覆蒸氣滅菌後也不會產生萃取物。在連續流滅菌生產線中,快速乾燥是避免瓶頸的必要條件,因此對鉑基矽酮密封劑的需求也隨之成長。能夠通過ISO 10993生物相容性認證的本地化合物生產商正在獲得定價權,尤其是在檳城,無塵室建造商正在尋求密封和感測器解決方案以簡化驗證流程。

矽酮單體價格的波動對中小化合物生產商的利潤率帶來了壓力。

自2024年以來,由於中國工廠關閉和原物料價格飆升,成本出現了兩位數的波動,這給缺乏避險能力的中小型企業利潤率帶來了壓力。儘管瓦克正在逐步擴大在韓國和日本的產能,但這並未解決區域供應短缺的問題,當地複合材料生產商面臨難以預測的成本基礎。產業整合正在加速。一體化生產商正在收購利基品牌以確保分銷網路。一些中小企業正在轉向使用原料成本更穩定、應用範圍更窄的MS聚合物和丙烯酸體系。

細分市場分析

2025年,矽酮在馬來西亞密封膠市場佔據39.50%的佔有率。這主要歸功於航太燃料箱密封、醫療設備無塵室密封以及幕牆外牆密封等應用領域對耐紫外線和耐熱性能的嚴格要求。聚氨酯預計到2031年將以6.02%的複合年成長率成長,主要驅動力是電動車電池組模組將鋁製冷卻板黏合到複合材料材料外殼上。丙烯酸樹脂用於中高層住宅的室內裝修,在這些場所,可塗漆性比移動性更為重要;而環氧樹脂則在耐化學腐蝕地板材料領域佔據了一席之地。

在馬來西亞密封膠市場,MS聚合物混合產品的市場規模目前較小,但由於越來越多的加工商需要不含異氰酸酯的可塗漆體系,因此該市場正在不斷擴張。 VITAL TECHNICAL公司在MS聚合物領域佔據了超過50%的區域市場佔有率,並正致力於獲得生產線認證,以充分利用其8分鐘無黏性的優勢。該公司樹脂產品線豐富,涵蓋了特殊等級、可膨脹密封膠、水下固化型和防火體系,而這一趨勢也得益於SIRIM認證的低VOC配方數量的不斷成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大型公共部門專案的激增推高了對建築密封劑的需求。

- 醫療設備出口的蓬勃發展帶動了對可消毒矽膠的需求。

- 向模組化、工業化建築系統 (IBS) 的轉變正在加速工廠預塗接縫密封劑的使用。

- 丹絨馬林和克林電動車組裝的擴張,帶動了對高溫電池組密封劑需求的成長。

- 雪蘭莪州航太維修產業叢集的擴張正在推動對燃料箱和結構密封劑的需求。

- 市場限制因素

- 矽酮單體價格的波動對中小化合物生產商的利潤率帶來了壓力。

- 由於技術純熟勞工短缺,導致工藝粗糙和接頭過早失效。

- 馬來西亞遲遲未能推出自己的低VOC標準,造成了監管上的不確定性。

- 價值鏈分析

- 分銷通路分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 矽酮

- 聚氨酯

- 丙烯酸纖維

- 環氧樹脂

- 其他

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 電子設備和電氣裝置

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- BASF SE

- Chemibond Enterprise Sdn Bhd

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- Mapei SpA

- Mohm Chemical Sdn. Bhd.

- Momentive Performance Materials

- Pidilite Industries Ltd.

- RPM International Inc.

- Selic Corp.

- Sika AG

- Soudal Group

- VITAL TECHNICAL Sdn Bhd

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the malaysia sealants market size was valued at USD 60.29 million in 2025 and is estimated to grow from USD 62.98 million in 2026 to reach USD 79.5 million by 2031, at a CAGR of 4.77% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Silicone, Polyurethane, Acrylic, Epoxy, and Others) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, Electronics and Electricals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Sealants Market Trends and Insights

Surge in Public-Sector Megaproject Pipeline Boosts Construction Sealant Demand

The East Coast Rail Link reached 92.62% completion in early 2026, injecting RM 50.27 billion (USD 11.3 billion) into sealant-intensive viaducts, tunnels, and station envelopes. Parallel programs such as MRT-3 and the Johor Bahru-Singapore Rapid Transit System Link deepen volume, but the real shift stems from the 70% IBS requirement that relocates joint sealing from outdoor sites to climate-controlled factories. Controlled curing cuts rework, shortens project cycles, and favors suppliers skilled in automated dispensing. The Construction Industry Development Board's (CIDB) 2025 Competency Standard adds Building Information Modeling proficiency to contractor licensing, pushing improper joint design from a warranty concern to a compliance risk.

Medical-Device Export Boom Driving Need for Sterilizable Silicone Grades

Malaysia's medical-device exports climbed to RM 37 billion in 2024 after RM 20 billion of cumulative investment since 2021, prompting demand for FDA-compliant silicone sealants that tolerate repeated 134 °C steam sterilization without extractables. Continuous-flow sterilization lines require faster tack-free times to avert bottlenecks, shifting preference toward platinum-catalyzed grades. Local formulators that can certify ISO 10993 biocompatibility gain pricing power, particularly as Penang's cleanroom builders look for seal-and-sensor solutions that streamline validation.

Volatile Silicone-Monomer Prices Squeezing SME Formulators' Margins

Double-digit cost swings since 2024, sparked by Chinese plant outages and feedstock spikes, are eroding margins at SMEs without hedging capacity. Wacker's incremental builds in South Korea and Japan have not neutralized regional tightness, so local formulators face unpredictable cost baselines. Consolidation is accelerating: integrated producers are acquiring niche brands to lock in distribution. Some SMEs are pivoting to MS-polymer or acrylic systems with steadier input costs but narrower application windows.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Modular Building Systems Accelerates Factory-Applied Sealant Usage

- Growing EV Assembly Stimulates High-Temperature Battery-Pack Sealant Uptake

- Labor-Skill Shortages Causing Premature Joint Failures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone held a 39.50% Malaysia sealants market share in 2025 because aerospace fuel-tank sealing, medical-device cleanrooms, and curtain-wall facades cannot compromise on UV stability and temperature resistance. Polyurethane is forecast to grow at a 6.02% CAGR through 2031, pushed by EV battery-pack modules that bond aluminum cooling plates to composite casings. Acrylic serves mid-rise residential interiors where paintability trumps movement capability, while epoxy fills chemical-resistant flooring niches.

The Malaysia sealants market size for MS-polymer hybrids is small today, but expanding as fabricators seek isocyanate-free systems that still accept paint. VITAL TECHNICAL claims over 50% regional share in MS-polymer sales and is leveraging eight-minute tack-free times to win factory-line approvals. Specialty grades, intumescent, underwater curing, and fire-rated systems, round out the resin palette and are shaped by rising SIRIM certification of low-VOC formulations.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF SE

- Chemibond Enterprise Sdn Bhd

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- Mapei S.p.A.

- Mohm Chemical Sdn. Bhd.

- Momentive Performance Materials

- Pidilite Industries Ltd.

- RPM International Inc.

- Selic Corp.

- Sika AG

- Soudal Group

- VITAL TECHNICAL Sdn Bhd

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in public-sector megaproject pipeline boosts construction sealant demand

- 4.2.2 Medical-device export boom driving need for sterilizable silicone grades

- 4.2.3 Shift to modular/industrialised building systems (IBS) accelerates factory-applied joint-sealant usage

- 4.2.4 Growing EV assembly in Tanjung Malim and Kulim stimulating high-temperature battery-pack sealant uptake

- 4.2.5 Aerospace MRO cluster expansion in Selangor fuels demand for fuel-tank and structural sealants

- 4.3 Market Restraints

- 4.3.1 Volatile silicone monomer prices squeezing SME formulators' margins

- 4.3.2 Labour-skill shortages causing improper application and premature joint failures

- 4.3.3 Delayed adoption of Malaysia-specific low-VOC standards creating regulatory uncertainty

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Existing Competitors

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Silicone

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Epoxy

- 5.1.5 Others

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Electronics and Electricals

- 5.2.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Chemibond Enterprise Sdn Bhd

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Illinois Tool Works Inc.

- 6.4.9 Mapei S.p.A.

- 6.4.10 Mohm Chemical Sdn. Bhd.

- 6.4.11 Momentive Performance Materials

- 6.4.12 Pidilite Industries Ltd.

- 6.4.13 RPM International Inc.

- 6.4.14 Selic Corp.

- 6.4.15 Sika AG

- 6.4.16 Soudal Group

- 6.4.17 VITAL TECHNICAL Sdn Bhd

- 6.4.18 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)