|

市場調查報告書

商品編碼

2066690

新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Singapore Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

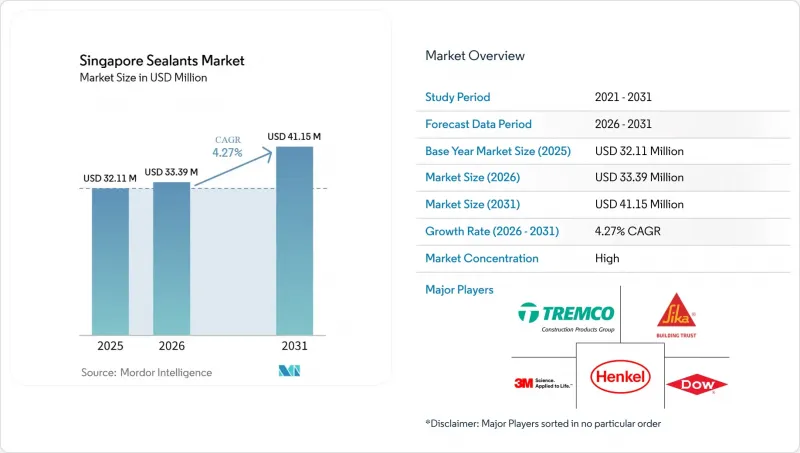

根據 Mordor Intelligence 預測,新加坡密封膠市場規模將從 2025 年的 3,211 萬美元成長到 2026 年的 3,339 萬美元,然後在 2031 年達到 4,115 萬美元,2026 年至 2031 年的複合年成長率為 4.27%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂及其他樹脂)和終端用戶行業(航太、汽車、建築、醫療及其他終端用戶行業)進行細分。市場預測以美元計價。

新加坡密封劑市場趨勢及洞察

加速公共部門基礎設施發展計劃

目前有五項鐵路工程正在並行:裕廊區域線、跨島線一期、環線六期、湯申-東海岸線五期以及市區線三期東段。這些工程預計將啟用數十個車站。這些車站需要防火隧道、月台和大廳接縫,從而對快速固化、低收縮的矽酮、聚氨酯和聚硫密封膠產生持續的年度需求。市區重建局(URA)的總體規劃承諾提供超過8萬套新住宅,根據住宅發展局(HDB)的數據,截至2026年初,將有127個項目開工,這將確保密封膠在未來幾年內都有需求。 CONQUAS 2025現已將功能測試結果與臨時使用許可證的發放掛鉤,並且越來越重視那些能夠在一次施工中實現無滲漏玻璃安裝並符合滲漏標準的產品。因此,承包商往往更傾向於選擇無需底塗即可黏合、柔韌性好且修補週期短的配方。提供現場培訓和快速固化樣品的經銷商可以提高產品採用率並鼓勵客戶重複訂購。

向綠色認證建築圍護結構過渡

新加坡綠建築標誌(Green Mark)指南強調在整個生命週期中減少碳足跡,並建議使用低排放密封劑。這些密封劑必須獲得GEV EMICODE EC1 PLUS、新加坡綠色標籤或同等認證。西卡(Sika)的產品,如Sikaflex Purform和SikaTop-540 Seal,符合多項室內空氣品質標準,並幫助開發商獲得LEED能源與環境設計認證積分。此外,這些產品還有助於開發人員獲得綠建築標誌獎勵,包括占地面積的優先待遇。漢高(Henkel)新成立的吉尼奧科學園區(Gineo Science Park)實驗室正在加速推進無全氟烷基化合物的研發,以應對新加坡國家環境局即將訂定的溶劑法規,並已做好提前合規的準備。隨著職場接觸標準的日益嚴格,濕固化聚氨酯和異氰酸酯及芳香族化合物排放量極低的混合矽烷封端聚合物的市場佔有率正在不斷擴大。開發商擴大指定使用雙組分環氧-聚氨酯混合材料進行地下防水工程。這是因為它們沒有收縮,可以防止在地下水位高的地區(例如掩埋的沿海地區)發生分層。

矽聚合物的進口價格受中國供應情況波動的影響。

中國對金屬矽冶煉廠的環境法規推高了碳酸二甲酯的現貨溢價,顯著延長了亞洲和歐洲之間的前置作業時間。在完全依賴進口的新加坡,固定價格的公開競標阻礙了成本轉嫁,迫使經銷商承擔了成本的急劇上漲。有些公司轉而使用丙烯酸或混合聚合物,但改用替代品會帶來違反保固的風險,尤其是在高變形或對紫外線耐受性要求較高的情況下。跨國公司透過從多個地區採購來分散原料風險,但中小企業被迫依賴不斷增加的庫存,這給它們的營運資金帶來了壓力。

細分市場分析

2025年,矽酮在新加坡密封膠市場仍佔據38.50%的佔有率,其特點是具有卓越的抗紫外線性能和-40 度C至100 度C的工作溫度範圍。然而,聚氨酯預計將超越新加坡密封膠市場的整體成長率,在2026年至2031年間實現6.21%的複合年成長率。這是因為建築師在玻璃帷幕牆和預製混凝土接縫處指定使用低彈性模量和高位移吸收能力的產品。 「SikaHyflex 250 Facade」專為適應大位移而設計,使承包商無需使用隔離膠帶即可加寬接縫。雖然純矽酮產品在潮濕環境中經常面臨挑戰,但像PENOSIL Facade Joint Hybrid 25LM這樣的混合型MS聚合物卻非常有效。這些聚合物與潮濕基材的黏合性良好,並符合嚴格的排放標準。另一方面,丙烯酸和丁基密封膠仍然是室內裝潢和防潮應用的首選,尤其是在成本是主要考慮因素且位移有限的情況下。

在南海岸空氣品質管理區 (AQMD) 第 1124 號規則的推動下,溶劑型聚硫化物轉變為濕固化化學品的轉變正在加速。該規則禁止在 2028 年前在航太密封劑中使用對氯苯並三氟化物,預示著全球供應鏈的精簡,並將波及新加坡的規範。製造商提供的符合產品加權最大增量反應性 (PWMIR) 標準的催化劑,凸顯了監管趨勢,即聚氨酯和混合平台在結構上優於傳統聚硫化物。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速公共部門基礎設施發展計劃

- 過渡到具有綠色認證的建築圍護結構

- 半導體潔淨室擴建

- 加強在實裡達機場和樟宜機場作為飛機維修、修理和大修中心的地位。

- 政府對低揮發性有機化合物材料的獎勵措施

- 市場限制因素

- 矽聚合物的進口價格受中國供應情況波動的影響。

- 2025 年建屋發展局移交高峰過後,未開工的公共住宅計畫數量將減少。

- 接收外籍勞工的配額日益嚴格,導致企業招募成本上升。

- 價值鏈分析

- 分銷通路分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Alteco Chemical Pte Ltd.

- Dow

- Fosroc, Inc.

- HB Fuller Company

- Henkel AG & Co. KGaA

- MAPEI SpA

- PFE Technologies Pte Ltd

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco Incorporated

第7章 市場機會與未來展望

According to Mordor Intelligence, the singapore sealants market size is expected to grow from USD 32.11 million in 2025 to USD 33.39 million in 2026 and is forecast to reach USD 41.15 million by 2031 at 4.27% CAGR over 2026-2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins ) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

Singapore Sealants Market Trends and Insights

Accelerated Public-Sector Infrastructure Pipeline

Five concurrent rail packages, the Jurong Region Line, Cross Island Line Stage 1, Circle Line Stage 6, Thomson-East Coast Line Stage 5, and Downtown Line Stage 3 East, will introduce dozens of stations that require fire-rated tunnel, platform, and concourse joints, sustaining annual demand for fast-cure, low-shrink silicone, polyurethane, and polysulfide grades. The Urban Redevelopment Authority's Master Plan pledges more than 80,000 new residential units, while Housing and Development Board data lists 127 active projects in early 2026, collectively locking in multi-year sealant volumes. CONQUAS 2025 now ties functional-test results to Temporary Occupation Permit issuance, elevating the premium on products that achieve leak-free glazing and ponding compliance in a single pass. Contractors, therefore, favor formulations with primer-less adhesion and extended movement capability that shorten remediation cycles. Distributors that supply site training and accelerated-cure mock-ups strengthen specification pull-through and repeat orders.

Transition to Green-Certified Building Envelopes

Singapore's Green Mark guidelines emphasize reducing life-cycle carbon footprints and encourage the use of low-emission sealants. These sealants must hold certifications such as GEV EMICODE EC1 PLUS, the Singapore Green Label, or equivalent. Sika's products, Sikaflex Purform and SikaTop-540 Seal, comply with various indoor-air-quality standards, supporting developers in obtaining Leadership in Energy and Environmental Design (LEED) credits. Additionally, these products help developers qualify for Green Mark incentives, including gross floor area benefits. Henkel's new Geneo Science Park lab accelerates perfluoroalkyl-substance-free research and development ahead of anticipated National Environment Agency solvent limits, keeping the firm positioned for early compliance bids. Moisture-cure polyurethanes and hybrid silyl-terminated polymers, which emit negligible isocyanates or aromatics, gain share as workplace exposure limits tighten. Developers increasingly specify two-component epoxy-polyurethane hybrids for below-grade waterproofing because they deliver zero shrinkage and prevent delamination in high water-table sites along reclaimed coasts.

Volatile Silicone Polymer Import Prices Tied to China Supply

Spot premiums for dimethyl carbonate increased, and lead times between Asia and Europe lengthened significantly, driven by China's environmental restrictions on silicon-metal smelters. Singapore, fully import-dependent, saw distributors absorb cost spikes because fixed-price public tenders prevented pass-through. Some shifted to acrylic or hybrid polymers, but substitution risks warranty breaches where high movement or ultraviolet (UV) durability is mandatory. Multinationals with multi-regional sourcing diversified feedstock exposure, while smaller players relied on higher inventory holdings, straining working capital.

Other drivers and restraints analyzed in the detailed report include:

- Semiconductor Clean-Room Expansion

- Growing aircraft Maintenance, Repair, and Overhaul (MRO) hub status

- Shrinking Public-Housing Backlog Post-Handover Peak

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone retained 38.50% of the Singapore sealants market share in 2025, owing to superior UV resistance and -40 °C to 100 °C service capability. However, polyurethane's 6.21% CAGR from 2026 to 2031 outpaces the overall Singapore sealants market size as architects specify low-modulus, high-movement products for glass facades and precast concrete joints. SikaHyflex 250 Facade is designed to accommodate significant movement, allowing contractors to widen joints without requiring bond-breaker tape. In humid conditions, where pure silicones often face challenges, hybrid MS-polymers like PENOSIL Facade Joint Hybrid 25LM are highly effective. These polymers adhere well to damp substrates and achieve high emissions standards. Meanwhile, acrylic and butyl mastics continue to be preferred for interior trim and vapor-barrier details, particularly in applications where cost sensitivity is critical, and movement is limited.

The transition from solvent-borne polysulfides to moisture-cure chemistries accelerates under South Coast Air Quality Management District (AQMD) Rule 1124, which bans para-chlorobenzotrifluoride in aerospace sealants by 2028, signaling global supply rationalization that will ripple into Singapore specifications. Producers responding with Product-Weighted Maximum Incremental Reactivity-compliant catalysts highlight a regulatory trend that structurally favors polyurethane and hybrid platforms over legacy polysulfides.

List of Companies Covered in this Report:

- 3M

- Alteco Chemical Pte Ltd.

- Dow

- Fosroc, Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- MAPEI S.p.A.

- PFE Technologies Pte Ltd

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated public-sector infrastructure pipeline

- 4.2.2 Transition to green-certified building envelopes

- 4.2.3 Semiconductor clean-room expansion

- 4.2.4 Growing aircraft MRO hub status at Seletar and Changi

- 4.2.5 Government incentives for low-VOC materials

- 4.3 Market Restraints

- 4.3.1 Volatile silicone polymer import prices tied to China supply

- 4.3.2 Shrinking public-housing backlog post-HDB 2025 handover peak

- 4.3.3 Tight migrant-labour quotas raising on-site application costs

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Alteco Chemical Pte Ltd.

- 6.4.3 Dow

- 6.4.4 Fosroc, Inc.

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 MAPEI S.p.A.

- 6.4.8 PFE Technologies Pte Ltd

- 6.4.9 Shin-Etsu Chemical Co., Ltd.

- 6.4.10 Sika AG

- 6.4.11 Soudal Group

- 6.4.12 Tremco Incorporated

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)