|

市場調查報告書

商品編碼

2066680

法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)France Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

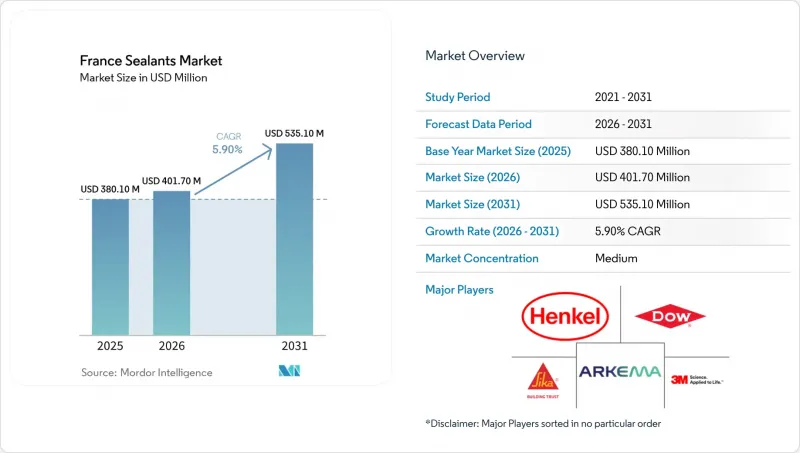

根據 Mordor Intelligence 預測,法國密封劑市場規模將從 2025 年的 3.801 億美元成長到 2026 年的 4.017 億美元,到 2031 年將達到 5.351 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 5.90%。

本報告按樹脂類型(矽樹脂、聚氨酯樹脂、丙烯酸樹脂、環氧樹脂及其他樹脂)及終端用戶產業(航太、汽車及運輸、建築施工、醫療及其他終端用戶產業)進行細分。市場預測以美元計價。

法國密封膠市場趨勢與洞察

需求激增正在推動節能建築外圍護結構的維修。

MaPrimeRenov已將其面向極低收入家庭的預付現金計劃延長至2025年12月,提供高達50%的預付款,方便他們即時購買用於熱橋、屋頂接縫和管道穿孔的矽酮和聚氨酯密封膠。液態矽酮氣密防水材料,例如Momentive Elemax 2600,可透過抑制不受控制的氣流,將暖通空調能耗降低高達35%,使其成為難以實施片材防水的維修工程中極具吸引力的投資選擇。中等收入家庭的補貼上限提高至80%,擴大了他們獲得法國FDES認證的高品質、低VOC產品的管道,確保符合基於HQE Cible 8目標的氣密性標準。強制性的ISO 11600 25級流動性要求和EN 15651-2認證確保了玻璃和幕牆接縫的耐久性。這些政策和標準框架結合起來,鞏固了高性能建築密封劑的多年需求週期。

法國汽車生產中電動車的輕量化要求

在車身本體中,鋁和碳纖維增強聚合物、鋼和複合材料等多種材料的黏合正在取代機械緊固件,導致抗剪切環氧樹脂和聚氨酯黏合劑的消耗量增加,這些黏合劑也可用作減震器和電池外殼密封劑。漢高公司於2025年4月宣布推出的AI生成的虛擬黏合劑和可剝離化學組合物,旨在滿足歐盟電池護照法規的要求,該法規強制要求電池在報廢後進行可追溯性和分解。經等離子預處理的丙烯酸-環氧樹脂混合樹脂可在紫外線照射下數分鐘內固化,從而縮短生產線週期時間並提高與低能耗塑膠的黏合力,進而提高Stellantis和雷諾工廠的產能。 MS聚合物在LEED v4和SCAQMD 1168法規提高VOC(揮發性有機化合物)濃度低於250 g/L的要求下,展現出顯著優勢。這些聚合物在不使用異氰酸酯的閾值下,可達到±25%至±50%的置換率。監管和生產相關因素的共同作用,推動汽車密封劑保持強勁的成長勢頭。

石化原料價格波動

由於原料成本約佔銷售額的50%,法國複合材料生產商難以透過季度建築合約將不斷上漲的價格轉嫁給消費者,這給其息稅折舊攤銷前利潤(EBITDA)帶來了壓力。儘管BASF在蓋斯馬工廠擴建MDI產能預計在2027年前緩解供應緊張局面,但地緣政治風險持續推高苯和石腦油價格,使密封劑生產商的利潤率面臨劇烈波動的風險。尤其是在亞洲低價進口產品持續湧入的情況下,沒有採取對沖措施的公司將被迫在銷售量下降和利潤縮水之間做出選擇。

細分市場分析

2025年,矽酮密封膠在法國密封膠市場佔有38.5%的佔有率。這主要得益於結構玻璃、雙層玻璃和耐候幕牆領域不可取代的需求。 「Sikasil IG-25 HM Plus」符合EN 1279-4和ASTM C1184標準,確保真空絕熱玻璃的氣體密封性能,而真空絕熱玻璃對單位成本的要求較高。聚氨酯預計將推動法國密封膠市場的擴張,預計2026年至2031年複合年成長率將達到7.24%。這主要是由於電動車製造商為了減輕重量和延長電池續航里程,傾向於以黏接而非焊接的方式連接鋁、碳纖維增強複合材料(CFRP)和鋼製模組。

丙烯酸密封膠由於其在可塗漆性和近乎零VOC含量方面的裝飾優勢,目前仍主要應用於室內靜態接縫,但其對位移的適應性較差,限制了其在戶外的應用。環氧樹脂密封膠在工業地板材料和航太特定應用領域佔據主導地位,其抗張強度和耐化學性彌補了固化速度慢的不足。 Baxxodur EC 151可在5°C下實現功能性固化,從而延長了冬季施工窗口期。聚硫化物和MS聚合物分別在燃料箱密封和無異氰酸酯接縫密封等領域發揮特殊作用,但它們面臨著被新型生物基產品在中期內替代的風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 正在進行的維修引發了對節能建築外圍護結構維修的需求激增。

- 法國汽車生產中電動車的輕量化要求

- 空中巴士及區域航太叢集複合材料黏合技術的發展

- 「可修復性指數法」正在促進家用電器和家電維護用密封劑的銷售。

- 法國離岸風力發電建設帶動了對船用密封膠的需求。

- 市場限制因素

- 石化原料價格波動

- 歐盟 REACH 法規提高了對二異氰酸酯的限制,從而增加了合規成本。

- 生物基黏合劑替代品的興起正在侵蝕傳統密封劑的市場佔有率。

- 價值鏈分析

- 分銷通路分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 矽酮

- 聚氨酯

- 丙烯酸纖維

- 環氧樹脂

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 汽車和運輸業

- 建築/施工

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- BASF SE

- BASFIKA Produits Chimiques

- Bolton Group

- CERMIX

- Den Braven France

- DL Chemicals NV

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- ISPO Group

- MAPEI SpA

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soprema Group

- Soudal NV

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the france sealants market size is projected to grow from USD 380.10 million in 2025 to USD 401.70 million in 2026, and reach USD 535.10 million by 2031, growing at a CAGR of 5.90% from 2026 to 2031.

This report is Segmented by Resin Type (Silicone, Polyurethane, Acrylic, Epoxy, and Other Resins) and End-User Industry (Aerospace, Automotive and Transportation, Building and Construction, Healthcare, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

France Sealants Market Trends and Insights

Renovation-Led Demand Surge in Energy-Efficient Building Envelope Upgrades

MaPrimeRenov' extended cash advances up to 50% for very modest households through December 2025, stimulating immediate purchases of silicone and polyurethane sealants for thermal bridges, roof junctions, and duct penetrations. Fluid-applied silicone air-and-water barriers such as Momentive Elemax 2600 can reduce HVAC energy use by as much as 35% by limiting uncontrolled airflow, an attractive payback lever in retrofit settings where sheet membranes are difficult to place. The subsidy's raised cost ceiling to 80% for middle-income households broadens access to premium low-VOC products carrying French FDES declarations, ensuring airtightness compliance under HQE Cible 8 targets. Mandatory ISO 11600 Class 25 movement and EN 15651-2 designations safeguard joint durability in glazing and facade works. These policy and standard frameworks collectively lock in a multi-year demand cycle for high-performance building sealants.

EV Lightweighting Requirements in French Automotive Production

Multi-material bonding, aluminum to carbon-fiber-reinforced polymer and steel to composites, is displacing mechanical fasteners in EV body-in-white architecture, pushing consumption of shear-resistant epoxy and polyurethane adhesives that double as vibration dampers and battery-case sealants. Henkel's April 2025 reveal of AI-generated virtual adhesives and debondable chemistries anticipates EU battery-passport rules that will require traceability and end-of-life disassembly. Acrylic-epoxy hybrids activated by UV in minutes are improving line takt times and adhesion to low-energy plastics when pre-treated with plasma, enabling higher throughput at Stellantis and Renault plants. Evolving LEED v4 and SCAQMD Rule 1168 thresholds below 250 g/L VOC are giving MS polymers an advantage, delivering +-25% to +-50% movement without isocyanate exposure. The combined regulatory and production drivers keep automotive grade sealants on a robust growth path.

Petrochemical Feedstock Price Volatility

With raw materials representing roughly 50% of revenue, French formulators struggle to pass spikes through quarterly construction contracts, compressing EBITDA. BASF's MDI expansion in Geismar may ease tightness by 2027, yet geopolitical risk continues to swing benzene and naphtha costs, exposing sealant makers to margin whiplash. Those without hedging must choose between volume attrition and profit erosion, especially given the persistence of lower-priced Asian imports.

Other drivers and restraints analyzed in the detailed report include:

- Composite Bonding Growth in Airbus and Regional Aerospace Clusters

- Repairability-Index Law Boosting DIY and Appliance Maintenance Sealant Sales

- Stricter EU REACH Limits on Di-Isocyanates Raising Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone captured 38.5% of the France sealants market share in 2025, powered by irreplaceable demand in structural glazing, insulating glass units, and weatherproof facades. Sikasil IG-25 HM Plus meets EN 1279-4 and ASTM C1184, securing gas-retention in vacuum-insulated glazing which commands premium unit prices. Polyurethane is set to pace the France sealants market size expansion, growing 7.24% CAGR during 2026-2031 as EV assemblers bond aluminum, CFRP, and steel modules, substituting welds to cut weight and extend battery range.

Acrylics remain relegated to interior static joints where paintability and near-zero VOC confer decorative advantages, but low movement capability limits outdoor use. Epoxies command niche industrial flooring and aerospace applications where tensile strength and chemical resistance justify slow cure; Baxxodur EC 151 allows functional cure at 5 °C, expanding winter construction windows. Polysulfides and MS polymers fill specialized roles, fuel-tank sealing and isocyanate-free construction joints, respectively, but face medium-term substitution risk from bio-based entrants.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF SE

- BASFIKA Produits Chimiques

- Bolton Group

- CERMIX

- Den Braven France

- DL Chemicals NV

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works

- ISPO Group

- MAPEI S.p.A.

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soprema Group

- Soudal NV

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation-led demand surge in energy-efficient building envelope upgrades

- 4.2.2 EV lightweighting requirements in French automotive production

- 4.2.3 Composite bonding growth in Airbus and regional aerospace clusters

- 4.2.4 Repairability-index law boosting DIY and appliance maintenance sealant sales

- 4.2.5 Marine-grade sealants demand from French offshore-wind build-out

- 4.3 Market Restraints

- 4.3.1 Petrochemical feedstock price volatility

- 4.3.2 Stricter EU REACH limits on di-isocyanates raising compliance costs

- 4.3.3 Emerging bio-based adhesive substitutes eroding conventional sealant share

- 4.4 Value Chain Analysis

- 4.5 Distribution Channel Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Silicone

- 5.1.2 Polyurethane

- 5.1.3 Acrylic

- 5.1.4 Epoxy

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive and Transportation

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 BASFIKA Produits Chimiques

- 6.4.5 Bolton Group

- 6.4.6 CERMIX

- 6.4.7 Den Braven France

- 6.4.8 DL Chemicals NV

- 6.4.9 Dow

- 6.4.10 H.B. Fuller Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Illinois Tool Works

- 6.4.13 ISPO Group

- 6.4.14 MAPEI S.p.A.

- 6.4.15 RPM International Inc.

- 6.4.16 Saint-Gobain Weber

- 6.4.17 Sika AG

- 6.4.18 Soprema Group

- 6.4.19 Soudal NV

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)