|

市場調查報告書

商品編碼

2066684

中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

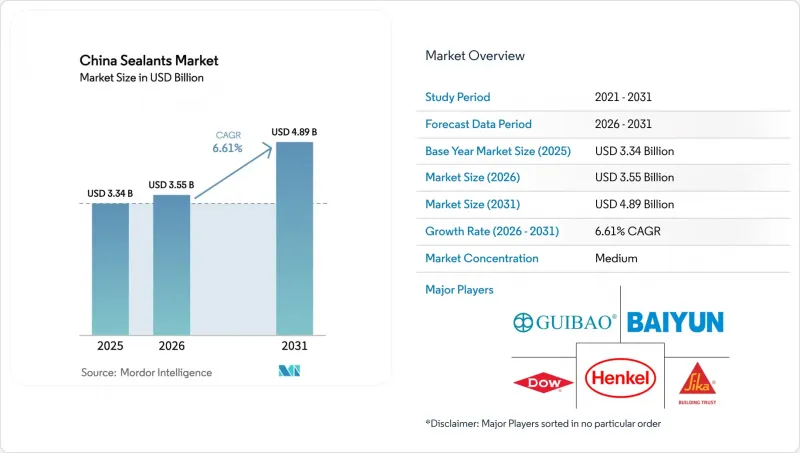

根據 Mordor Intelligence 預測,中國密封膠市場規模將從 2025 年的 33.4 億美元成長到 2026 年的 35.5 億美元,然後在 2031 年達到 48.9 億美元,2026 年至 2031 年的複合年成長率為 6.61%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂及其他樹脂)及終端用戶產業(航太、汽車及交通運輸、電子及半導體、建築及施工、醫療保健及其他終端用戶產業)進行細分。市場規模和預測均以美元計價。

中國密封膠市場趨勢與洞察

綠建築標準的實施正在加速對高品質、低VOC密封劑的需求。

將於2026年6月生效的強制性國家標準GB 30981.1-2025將收緊建築塗料及相關材料中揮發性有機化合物(VOCs)、半揮發性化合物、除生物劑和重金屬的限制,迫使生產商修改配方。不遵守該標準將導致更高的環保稅和省級審計。集團標準T/CBMF 297-2024中的生命週期評估(LCA)要求將加強公共部門專案的採購審查,促進幕牆和預製建築接縫中使用醇基固化矽酮和水性丙烯酸密封膠。 GB/T 35609-2025等配套框架將環境指標納入綠色產品標籤,加速住宅市場的兩極化,屆時傳統肟基固化矽酮將主要依靠價格競爭。一線城市已強制要求透過即時監測對揮發性有機化合物(VOC)排放進行數位化報告,這使得已投資建造低排放試點生產線的企業獲得了先發優勢。隨著合規成本的上升,中國密封膠市場越來越重視能夠快速調整配方並實現「從生產到出貨」全程可追溯的垂直整合供應商。

汽車輕量化正在加速向多材料黏合的過渡。

在中國電動車領域,車身結構正從機械緊固件轉向高度依賴黏合劑的鋁合金和複合材料車身,以滿足嚴格的續航里程和效率目標。 2024年,汽車鋁合金車身黏接製程市場規模約860億元人民幣(120億美元),預計2030年將達到2,300億元人民幣(320億美元),屆時鋁合金車身的採用率將接近40%。結構聚氨酯黏合劑具有優異的室溫固化性能和減振能力,有助於縮短機器人生產線的生產週期。蔚來ET7等領先的電動車平台所採用的結構性黏著劑,可將車輛的碰撞強度提升120公尺以上,是第一代車型用量的三倍。國內一級供應商與汽車製造商共同開發專有的黏合劑配方,透過減少設計迭代和將智慧財產權保留在國內,正在加強中國密封劑市場的技術基礎。

矽酮單體價格的波動給利潤率帶來了壓力。

由於單體生產商協調減產30%,二甲基環矽氧烷(DMC)現貨價格在2025年11月飆升20%,達到每噸13,200元人民幣(1,892.88美元)。受中國西南地區水電供應限制及工業矽成本上漲的影響,2026年1月,價格進一步上漲,達到每噸13,775元人民幣(1,975.33美元)。沒有長期合約或金融對沖的中小型化合物生產商的毛利率下降了多達450個基點。像瓦克這樣的大型綜合企業利用自身的矽氧烷產能來緩解成本飆升的影響,進一步擴大了中國密封劑市場的競爭差距。

細分市場分析

矽酮產品憑藉其在帷幕牆玻璃、外牆板和太陽能組件等領域久經考驗的耐久性,預計到2025年將佔據中國密封膠市場41.55%的佔有率。聚氨酯產品預計到2031年將以7.56%的複合年成長率成長,這主要得益於新能源汽車(NEV)的直接嵌裝玻璃以及需要在零下溫度下保持柔軟性的製冷保溫板。環氧樹脂、丙烯酸樹脂和MS混合體系仍是具有成長潛力的細分市場,其中MS混合體係由於其不含異氰酸酯的安全性以及快速的初始強度,每年市場佔有率成長80個基點。

儘管D4中間體價格的急劇上漲加劇了矽酮的成本劣勢,但複合技術、中性固化催化劑、黏合促進劑和紫外線穩定包裝等技術的進步不斷提升了矽酮的性能。瓦克張家港特種矽酮工廠供應高純度矽酮液(最初從德國進口),縮短了電子封裝級矽酮的前置作業時間。廣州聯達等國內企業正在推廣MS Hybrid矽酮,該產品邵氏A硬度可在20至50之間調節,且無需底塗即可粘合鍍鋅鋼板。這在模組化建築工廠中極具提案,因為這類工廠每班次需要多次更換基材。在預測期內,中國密封膠市場將從單一化學成分主導的格局轉變為多種樹脂產品組合的局面。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 綠建築標準的實施正在加速對高品質、低VOC密封劑的需求。

- 對更輕型汽車的需求正在推動多基板黏合技術的轉變。

- 電子商務倉庫的激增導致對地板接縫密封劑和冷庫密封劑的需求增加。

- 中國民用航太MRO生態系的快速擴張

- 智慧工廠的引入正在推動對單組分紫外線固化密封劑的需求。

- 市場限制因素

- 矽酮單體價格的波動給利潤率帶來了壓力。

- 加強地方政府對溶劑排放的環境審計

- 低等級建築矽酮產能過剩

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 建築/施工

- 汽車和運輸業

- 航太

- 電子和半導體

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- ACC Silicones(Shenzhen)

- Anabond Limited

- Arkema

- Beijing Oriental Yuhong Waterproof Technology

- Bondchem

- Chengdu Guibao Science and Technology Co., Ltd.

- CHT Germany GmbH

- Dow

- Guangzhou Baiyun Technology Co, Ltd.

- Guangzhou Jointas Chemical Co.

- HB Fuller Company

- Hangzhou Zhijiang Advanced Material Co.

- Henkel AG & Co. KGaA

- Huitian Adhesive Co.

- Momentive Performance Materials

- Shin-Etsu Chemical Co.

- Sika AG

- Tonsan Adhesive

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the china sealants market size is expected to grow from USD 3.34 billion in 2025 to USD 3.55 billion in 2026 and is forecast to reach USD 4.89 billion by 2031 at 6.61% CAGR over 2026-2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins) and End-User Industry (Aerospace, Automotive and Transportation, Electronics and Semiconductors, Building and Construction, Healthcare, and Other End-User Industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

China Sealants Market Trends and Insights

Green-Building Code Enforcement Accelerates Premium, Low-VOC Sealant Demand

Mandatory national standard GB 30981.1-2025, effective June 2026, tightens limits on VOCs, semi-volatile compounds, biocides, and heavy metals in architectural coatings and accessory materials, forcing producers to reformulate or face higher environmental-protection taxes and provincial audits. Life-cycle assessment requirements in group standard T/CBMF 297-2024 heighten procurement scrutiny for public-sector projects, propelling alcohol-cure silicones and water-based acrylics in curtain-wall and prefabricated-building joints. Complementary frameworks such as GB/T 35609-2025 embed environmental metrics into green-product labeling, accelerating market bifurcation where legacy oxime-cure silicones compete mainly on price in residential retrofit channels. Tier-1 cities are already mandating digital VOC-emission reporting via real-time monitoring, giving an early-mover advantage to companies that invested in low-emission pilot lines. As compliance costs rise, the China Sealants market increasingly rewards vertically integrated suppliers capable of rapid formulation pivots and cradle-to-gate traceability.

Automotive Light-Weighting Drives Multi-Substrate Bonding Shift

China's electric-vehicle segment is migrating from mechanical fasteners to adhesive-intensive aluminum and mixed-material bodies to meet stringent range and efficiency targets. The automotive aluminum-alloy body connection-process market was roughly RMB 86 billion (USD 12 billion) in 2024 and is expected to climb to RMB 230 billion (USD 32 billion) by 2030 as aluminum-body penetration rises toward 40%. Structural polyurethane adhesives are favored for ambient-temperature cure and vibration damping, supporting higher takt times on robotized lines. Flagship EV platforms such as the NIO ET7 feature more than 120 meters of crash-toughened structural adhesive per vehicle, a threefold increase from first-generation models. Domestic Tier-1s co-developing proprietary bonding recipes with automakers shorten design iterations and retain intellectual property in-country, strengthening the technology spine of the China Sealants market.

Volatile Silicone Monomer Pricing Squeezes Margins

Spot prices for dimethyl-cyclosiloxane (DMC) jumped 20% in November 2025 to RMB 13,200 (USD 1,892.88) per ton after monomer producers coordinated 30% output cuts. Hydropower curtailments in Southwest China and higher industrial-silicon costs pushed quotes further to RMB 13,775 (USD 1,975.33) per ton by January 2026. Smaller formulators, lacking long-term contracts or financial hedges, saw gross margins compress by up to 450 basis points. Large integrated players such as Wacker leveraged captive siloxane capacity to buffer cost spikes, widening competitive gaps within the China Sealants market.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce Warehousing Boom Raises Floor-Joint and Cold-Storage Sealant Use

- Rapid Expansion of China's Commercial Aerospace MRO Ecosystem

- Intensifying Provincial Environmental Audits on Solvent Emissions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone products commanded 41.55% of the China Sealants market share in 2025, supported by proven durability in curtain-wall glazing, facade panels, and photovoltaic modules. Polyurethane's 7.56% forecast CAGR through 2031 is propelled by direct-glazing in new-energy vehicles and by cold-storage insulation panels that demand flexibility at sub-zero temperatures. Epoxy, acrylic, and MS-hybrid chemistries remain growth niches, yet MS-hybrids are adding 80 basis points of share per year thanks to isocyanate-free safety and faster green strength.

Silicone's cost disadvantage widens when D4 intermediates surge, but formulation science, neutral-cure catalysts, adhesion promoters, and UV-stability packages continue to raise performance ceilings. Wacker's Zhangjiagang specialty silicones hub supplies high-purity fluids initially imported from Germany, shortening lead times for electronics encapsulation grades. Domestic challengers, such as Guangzhou Jointas, are promoting MS-hybrids with Shore-A hardness tunable from 20 to 50 and primer-less adhesion to galvanized steel, a compelling proposal in modular-construction factories that switch substrates several times per shift. Over the forecast window, the China sealants market will tilt toward diversified resin portfolios rather than single-chemistry dominance.

List of Companies Covered in this Report:

- 3M

- ACC Silicones (Shenzhen)

- Anabond Limited

- Arkema

- Beijing Oriental Yuhong Waterproof Technology

- Bondchem

- Chengdu Guibao Science and Technology Co., Ltd.

- CHT Germany GmbH

- Dow

- Guangzhou Baiyun Technology Co, Ltd.

- Guangzhou Jointas Chemical Co.

- H.B. Fuller Company

- Hangzhou Zhijiang Advanced Material Co.

- Henkel AG & Co. KGaA

- Huitian Adhesive Co.

- Momentive Performance Materials

- Shin-Etsu Chemical Co.

- Sika AG

- Tonsan Adhesive

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Green-building code enforcement accelerates premium, low-VOC sealant demand

- 4.2.2 Automotive light-weighting drives multi-substrate bonding shift

- 4.2.3 E-commerce warehousing boom raises floor-joint and cold-storage sealant use

- 4.2.4 Rapid expansion of China's commercial aerospace MRO ecosystem

- 4.2.5 Smart-factory adoption spurs demand for one-component UV-curable sealants

- 4.3 Market Restraints

- 4.3.1 Volatile silicone monomer pricing squeezes margins

- 4.3.2 Intensifying provincial environmental audits on solvent emissions

- 4.3.3 Over-capacity in low-grade construction silicones

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive and Transportation

- 5.2.3 Aerospace

- 5.2.4 Electronics and Semiconductors

- 5.2.5 Healthcare

- 5.2.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACC Silicones (Shenzhen)

- 6.4.3 Anabond Limited

- 6.4.4 Arkema

- 6.4.5 Beijing Oriental Yuhong Waterproof Technology

- 6.4.6 Bondchem

- 6.4.7 Chengdu Guibao Science and Technology Co., Ltd.

- 6.4.8 CHT Germany GmbH

- 6.4.9 Dow

- 6.4.10 Guangzhou Baiyun Technology Co, Ltd.

- 6.4.11 Guangzhou Jointas Chemical Co.

- 6.4.12 H.B. Fuller Company

- 6.4.13 Hangzhou Zhijiang Advanced Material Co.

- 6.4.14 Henkel AG & Co. KGaA

- 6.4.15 Huitian Adhesive Co.

- 6.4.16 Momentive Performance Materials

- 6.4.17 Shin-Etsu Chemical Co.

- 6.4.18 Sika AG

- 6.4.19 Tonsan Adhesive

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)德國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)