|

市場調查報告書

商品編碼

2066683

西班牙密封劑市場:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Spain Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

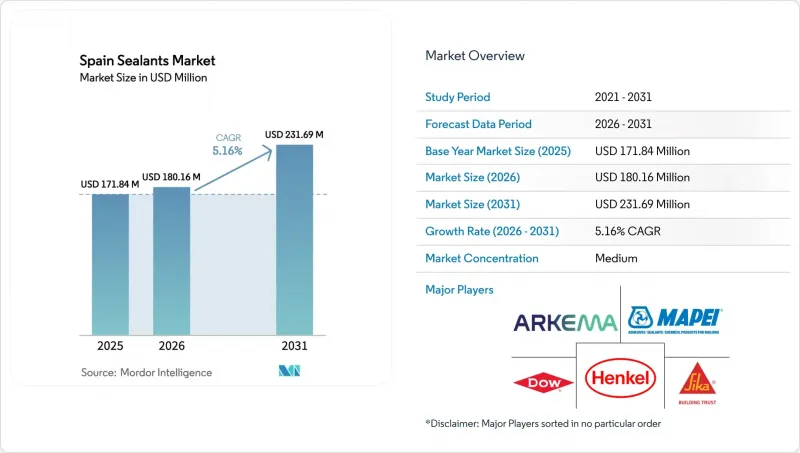

根據 Mordor Intelligence 預測,西班牙密封劑市場規模預計將在 2025 年達到 1.7184 億美元,2026 年達到 1.8016 億美元,到 2031 年達到 2.3169 億美元,2026 年至 2031 年的複合年成長率為 5.16%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂及其他樹脂)和終端用戶行業(航太、汽車、建築、醫療及其他終端用戶行業)進行細分。市場規模和預測均以美元計價。

西班牙密封劑市場的趨勢與洞察

西班牙老舊住宅存量主導需求激增。

預計到2025年,西班牙將完成185萬套住宅維修,大型維修的許可數量將年增12.9%。由於約80%的住宅能源效率等級較低,政府提供的高達100%的維修成本稅收優惠政策,正穩步推動窗框密封膠、伸縮縫和氣密密封材料的需求成長。根據PNRE 2026的最低能源效率標準,非住宅建築的能源效率必須在2030年前超過2020年能效最低的16%,從而形成可預測的多年訂單儲備。雖然馬德里、巴塞隆納和塞維利亞是補貼的主要受益城市,但西班牙建設產業正面臨70萬勞動力短缺,這促使建築商轉向使用與預製外牆相容的工廠生產的密封系統。由此帶來的需求成長,鞏固了西班牙密封膠市場的強勁成長動能。

為減輕車輛重量而製定的法規正在推動結構密封劑的使用。

歐洲關於報廢車輛的法規迫使汽車製造商採用依賴結構性黏著劑的複合材料車身以減輕重量。西班牙向電動車轉型的重點是位於阿拉貢的價值41億歐元的寧德時代-Stellantis合資電池工廠,該工廠預計到2026年底每年將供應50吉瓦時電池。該計畫推動了當地對符合UL 94 V-0和IEC 62368-1標準的阻燃聚氨酯和矽酮化學品的需求。可根據需要剝離以便回收的高延展性密封劑正成為理想的解決方案,技術領導者預計將在西班牙密封劑市場獲得高利潤。

異氰酸酯價格的波動給聚氨酯密封劑的利潤率帶來了壓力。

歐洲乙烯價格平均為每噸800美元,是美國的兩倍,中東的四倍,這使得該地區高達40%的產能面臨停產風險。由於西班牙全部依賴進口MDI(二苯基甲烷二異氰酸酯)和TDI(甲苯二異氰酸酯),每季20-30%的價格波動擠壓了以30天結算週期運營的小規模混煉企業的利潤空間。由於缺乏國內裂解裝置,原料價格波動仍是西班牙密封劑市場聚氨酯銷售的結構性阻力。

細分市場分析

到2025年,矽酮密封膠將佔據西班牙密封膠市場38.15%的佔有率,主要用於外牆和衛生潔具等需要卓越紫外線穩定性和防黴性能的應用領域。瓦克公司採用生質能衍生成分配製而成並獲得EC1+認證的「ELASTOSIL eco 7770 P」是此類別中的高級產品。雖然聚氨酯的銷售量目前小規模,但預計將以6.96%的複合年成長率成長,這主要得益於阿拉貢新超級工廠電動汽車電池密封和風力渦輪機葉片維修領域對高拉伸接縫的需求。西卡公司的「Purform」系列產品已符合REACH法規,並具有低單體含量的特點,有望抓住這一成長機會。

環氧樹脂產品在航太和工業地板材料等小眾市場仍佔有一席之地,而丙烯酸產品則面臨價格壓力,並部分被機械緊固件取代。新興的生物基混合物,例如混合矽烷改質聚合物 (SMP) 和 Bostic 的 46% 生物碳配方,正在為優先考慮基於 CPR 2024 環境等級的公共計畫開闢新的機會。總體而言,通用矽酮和丙烯酸產品的表現預計將與西班牙密封劑市場持平或低於該水平,而特種聚氨酯和經認證的混合系統預計將高於市場平均水平。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 西班牙老舊住宅存量維修需求激增。

- 為減輕車輛重量而製定的法規正在推動結構密封劑的使用。

- 歐盟的「Fit-for-55」能源效率法規正在推動對低VOC密封劑的需求增加。

- 陸上風力渦輪機葉片維修業務迅速擴張。

- 西班牙電動車超級工廠的利基需求

- 加泰隆尼亞的自修復聚合物研發叢集正在吸引投資者。

- 市場限制因素

- 異氰酸酯價格的波動給聚氨酯密封劑的利潤率帶來了壓力。

- 低層建築中機械緊固件的使用增加

- REACH法規對錫催化劑矽油有嚴格的規定

- 國內原料供應基地短缺

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Adhesivas Centro

- Adhesivos del Segura

- Arkema

- Comercial Quimica Masso

- Dow

- Fischer Iberica

- Grupa Selena

- HB Fuller Company

- Henkel AG & Co. KGaA

- Industrias Quimicas del Adhesivo

- MAPEI SpA

- Novasil SL

- Orbafoam

- QS Adhesives & Sealants SL

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soudal Group

- Tremco Illbruck

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the spain sealants market size is projected to be USD 171.84 million in 2025, USD 180.16 million in 2026, and reach USD 231.69 million by 2031, growing at a CAGR of 5.16% from 2026 to 2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Spain Sealants Market Trends and Insights

Renovation-Driven Demand Surge in Spain's Aged Housing Stock

Spain completed 1.85 million home renovations in 2025, and licenses for deep rehabilitation climbed 12.9% year on year. Roughly 80% of dwellings carry poor energy ratings, so fiscal incentives covering up to 100% of retrofit costs are channeling steady volumes toward window-perimeter, expansion-joint, and airtightness sealants. Minimum Energy Performance Standards under the PNRE 2026 require non-residential buildings to outperform the worst 16% of 2020 stock by 2030, creating a predictable multi-year order pipeline. Madrid, Barcelona, and Seville concentrate most subsidy beneficiaries, while a 700,000-worker shortfall in Spanish construction is steering contractors toward factory-applied sealant systems compatible with prefabricated facades. The resulting uplift cements a strong base trajectory for the Spain Sealants market.

Automotive Lightweighting Mandates Boosting Structural Sealant Usage

European End-of-Life Vehicle rules push automakers toward mixed-material bodies that depend on structural adhesives for weight savings. Spain's EV transition is centered on the EUR 4.1 billion CATL-Stellantis battery plant in Aragon, due to supply 50 GWh annually by end-2026. The project elevates local demand for flame-retardant polyurethane and silicone chemistries meeting UL 94 V-0 and IEC 62368-1. High-elongation sealants that debond on command to enable recycling are emerging as preferred solutions, positioning technology leaders to capture premium margins in the Spain Sealants market.

Volatile Isocyanate Prices Squeezing Polyurethane Sealant Margins

European ethylene costs average USD 800 per tons, double United States and quadruple Middle-East benchmarks, exposing up to 40% of regional capacity to closure risk. Spain imports all MDI (methylene diphenyl diisocyanate) and TDI (toluene diisocyanate), so 20-30% quarterly price swings erode margins for small formulators on 30-day terms. Absent domestic crackers, raw-material volatility remains a structural drag on polyurethane sales inside the Spain Sealants market.

Other drivers and restraints analyzed in the detailed report include:

- EU Fit-for-55 Energy-Efficiency Rules Raising Demand for Low-VOC Sealants

- Rapid Growth of On-Shore Wind-Blade Refurbishments

- Rising Substitution by Mechanical Fasteners in Low-Rise Construction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone sealants held 38.15% of Spain Sealants market share in 2025, anchored by facade and sanitary applications that benefit from UV stability and mildew resistance. Wacker's ELASTOSIL eco 7770 P adds biomass-offset content and EC1 plus certification, illustrating the premium end of this category. Polyurethane volumes are smaller today yet forecast to climb at 6.96% CAGR, propelled by EV battery sealing at the new Aragon gigafactory and high-elongation joints in wind-blade repairs. Sika's Purform series, already REACH-compliant and low-monomer, positions the firm to capture this uplift.

Epoxy chemistries remain niche, serving aerospace and industrial flooring, while acrylics face price pressure and partial substitution from mechanical fasteners. Hybrid silyl-modified polymers (SMP) and emerging bio-based blends, such as Bostik's 46% bio-carbon formulation, are carving out opportunities in public projects that weigh environmental classes under CPR 2024. Overall, commodity silicones and acrylics will track or trail the Spain Sealants market, whereas specialty polyurethane and certified hybrid systems are primed for above-trend gains.

List of Companies Covered in this Report:

- 3M

- Adhesivas Centro

- Adhesivos del Segura

- Arkema

- Comercial Quimica Masso

- Dow

- Fischer Iberica

- Grupa Selena

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Industrias Quimicas del Adhesivo

- MAPEI S.p.A.

- Novasil SL

- Orbafoam

- QS Adhesives & Sealants SL

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soudal Group

- Tremco Illbruck

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renovation-driven demand surge in Spain's aged housing stock

- 4.2.2 Automotive lightweighting mandates boosting structural sealant usage

- 4.2.3 EU "Fit-for-55" energy-efficiency rules raising demand for low-VOC sealants

- 4.2.4 Rapid growth of on-shore wind-blade refurbishments

- 4.2.5 Niche demand from Spanish EV gigafactories

- 4.2.6 Self-healing polymer RandD clusters in Catalonia attracting investors

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate prices squeezing polyurethane sealant margins

- 4.3.2 Rising substitution by mechanical fasteners in low-rise construction

- 4.3.3 Strict REACH restrictions on tin-catalyzed silicones

- 4.3.4 Limited domestic feedstock base

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Adhesivas Centro

- 6.4.3 Adhesivos del Segura

- 6.4.4 Arkema

- 6.4.5 Comercial Quimica Masso

- 6.4.6 Dow

- 6.4.7 Fischer Iberica

- 6.4.8 Grupa Selena

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Industrias Quimicas del Adhesivo

- 6.4.12 MAPEI S.p.A.

- 6.4.13 Novasil SL

- 6.4.14 Orbafoam

- 6.4.15 QS Adhesives & Sealants SL

- 6.4.16 RPM International Inc.

- 6.4.17 Saint-Gobain Weber

- 6.4.18 Sika AG

- 6.4.19 Soudal Group

- 6.4.20 Tremco Illbruck

- 6.4.21 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)