|

市場調查報告書

商品編碼

2066682

英國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United Kingdom Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

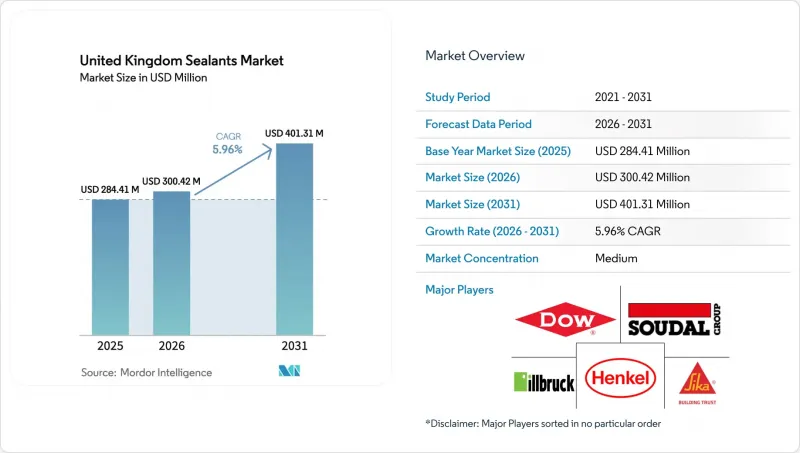

根據 Mordor Intelligence 預測,英國密封劑市場規模將從 2025 年的 2.8441 億美元和 2026 年的 3.0042 億美元成長到 2031 年的 4.0131 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.96%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂、聚硫化物樹脂、混合矽烷改性聚合物(SMP) 及其他樹脂)和終端用戶產業(航太、汽車、建築、醫療及其他終端用戶產業)進行細分。市場規模和預測均以美元計價。

英國密封劑市場趨勢及洞察

英國高層住宅維修對防火密封膠的需求不斷成長

《建築安全法》已將防火密封膠從可選升級項目轉變為英格蘭約12,500棟高層住宅的強制性產品。如今,可膨脹丙烯酸和矽酮密封膠必須通過EN 13501-1標準認證,並證明其與空腔密封系統的兼容性,這導致越來越多的企業傾向於選擇能夠提供第三方測試結果的品牌。格倫費爾大廈火災後的調查顯示,煙霧擴散是由於接縫缺陷造成的,這促使客戶對未經驗證的化學成分進行更嚴格的審查,並延長了核准週期。鐵路樞紐和機場的基礎設施維修也需要防火和隔音性能,這縮小了供應商的選擇範圍,並推高了價格。沒有EN認證產品線的中小型複合材料製造商正在被能夠投資持續測試的跨國供應商所取代,但需求仍然集中在倫敦和曼徹斯特,而這些地區的人事費用和物流成本已經推高了專案預算。

更嚴格的VOC法規正在推動混合矽烷封端聚合物的轉變。

SI 2012/1715 將建築密封劑中的揮發性有機化合物 (VOC) 含量限制在 5–10 克/公升。隨著 2024 年起現場檢查力度加大,遵守這些法規對承包商而言變得日益重要。混合型 SMP 等級產品在滿足此限制的同時,排放極低,可在環境濕度下固化,且無需異氰酸酯標籤,因此成為許多框架合約中的首選。歐洲佔全球 SMP 產能的 44%,而英國是該地區採用速度最快的國家。這主要歸功於公共部門採購負責人要求在競標文件中提交環境產品聲明 (EPD)。瓦克化學和 KCC 公司等供應商正在擴充其英國技術團隊,並對承包商進行濕度敏感型處理方法的培訓。雖然與溶劑型聚氨酯相比,這種轉變將使每公升成本增加 15–25%,但它將使承包商能夠遵守即將推出的生命週期碳排放法規,這可能會加速傳統溶劑型系統的淘汰。

金屬矽和MDI原料價格的波動

截至2026年3月,由於中國供應過剩,金屬矽價格較去年同期下跌14.98%;而歐洲MDI價格在2026年2月上漲7.9%,苯胺價格在2024年第四季上漲18%。因此,由於住宅不願完全接受價格上漲,聚氨酯生產商的利潤率面臨壓力。隨著原物料價格走勢分化,高階應用領域的市佔率正向矽轉移,同時,聚氨酯供應商也在試用TDI混合物,增加了職業暴露的風險。紅海海運中斷導致交貨前置作業時間延長10至14天,迫使經銷商持有更多庫存,從而佔用營運資金。

細分市場分析

至2025年,矽酮樹脂的需求量將佔總需求的33.50%,主要受醫療領域和防火外牆等符合EN 15651認證的應用需求所驅動。混合矽烷改性聚合物(SMP)產品預計在預測期(2026-2031年)內將以7.12%的複合年成長率成長,是所有樹脂中成長率最高的。這一成長與承包商對符合日益嚴格的VOC法規的單組分、無標籤檢視系統的偏好相符。聚氨酯因其耐化學性和對不同基材的黏合性,在電動車電池組和工業地板材料仍發揮重要作用。丙烯酸酯和聚硫化物繼續用於易澇地區的室內建築和土木工程。 ISO 11600和ASTM C920相關法規的協調統一提高了性能標準,加速了矽酮、SMP和聚氨酯的研發投入,而一些細分化學品領域則停滯不前。

這些競爭影響已初見端倪。瓦克化學計劃於2025年擴大其在英國的技術支持,而西卡則推出用於鐵路車輛的“Sikaflex-268 PowerCure”,旨在利用形狀記憶聚合物(SMP)的快速固化特性來取代聚硫化物。目前,專注於聚硫化物的中小型化合物製造商將其產品範圍限制在海洋和潮汐應用領域,因為在這些領域,浸水耐久性至關重要。隨著建築監管機構對環境產品聲明(EPD)的要求日益提高,那些無力承擔生命週期評估費用的供應商正在失去被納入規範的機會,這進一步鞏固了垂直整合的矽酮和SMP製造商的主導地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 英國高層建築維修工程對防火密封膠的需求不斷增加。

- 更嚴格的VOC法規正在推動混合矽烷封端聚合物的轉變。

- 英國脫歐後的基礎設施獎勵策略正在加速建築密封劑的消耗。

- 電動車電池組對密封件的需求日益成長。

- 英國國民醫療服務系統(NHS)設施維護的延誤導致醫療設施需要維修。

- 市場限制因素

- 金屬矽和MDI原料價格的波動

- 由於熟練工人短缺,項目延期

- 與現成墊片解決方案的競爭

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 多硫化物

- 混合矽烷改質聚合物(SMPs)

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 住宅

- 商業的

- 基礎設施

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Adshead Ratcliffe & Co Ltd.

- Arkema

- Bond It Group

- DAP Products

- Dow

- Sika Limited

- Fischer UK

- The Sherwin-Williams Company

- Gorilla Glue Company

- Henkel AG & Co. KGaA

- Hodgson Sealants

- illbruck(Tremco CPG)

- MAPEI SpA

- RPM International Inc.

- Sika AG

- Soudal Group

- Tremco Incorporated

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom sealants market size is projected to expand from USD 284.41 million in 2025 and USD 300.42 million in 2026 to USD 401.31 million by 2031, registering a CAGR of 5.96% between 2026 and 2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, Polysulfide, Hybrid Silane-Modified Polymer (SMP), and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

United Kingdom Sealants Market Trends and Insights

Growing Demand for Fire-Resistant Sealants in UK High-Rise Refurbishments

The Building Safety Act is transforming fire-rated sealants from optional upgrades to compulsory products across roughly 12,500 high-rise dwellings in England. Intumescent acrylics and silicones must now achieve EN 13501-1 classification and prove compatibility with cavity-barrier systems, shifting procurement toward brands that can present third-party test evidence. Post-Grenfell inquiries traced smoke spread to joint failures, raising client scrutiny and lengthening approval cycles for unproven chemistries. Infrastructure upgrades in rail hubs and airports also require dual fire and acoustic ratings, which narrows the supplier pool and supports premium pricing. Smaller formulators lacking EN-certified lines are ceding share to multinational suppliers that can finance continuous testing, while demand remains concentrated in London and Manchester, where labor and logistics costs already elevate project budgets.

Stricter VOC Regulations Pushing Shift to Hybrid Silane-Terminated Polymers

SI 2012/1715 caps VOC content in construction sealants at 5-10 g/L, and intensified site inspections since 2024 have made compliance visible to contractors. Hybrid SMP grades meet the limit with negligible emissions, cure through ambient moisture, and avoid isocyanate labeling, which makes them the default choice in many framework contracts. Europe holds 44% of global SMP capacity, and the United Kingdom is the region's fastest adopter because public-sector buyers mandate Environmental Product Declarations in tender documents. Suppliers such as Wacker Chemie and KCC Corporation have expanded UK technical teams to train applicators on moisture-sensitive handling. The transition raises costs by 15-25% per liter compared with solvent-borne polyurethane but positions contractors for forthcoming lifecycle-carbon rules that could expedite the exit of legacy solvent systems.

Volatility in Silicon-Metal and MDI Raw-Material Prices

Silicon metal declined 14.98% year-on-year to March 2026 on Chinese oversupply, while European MDI rose 7.9% in February 2026, and aniline rose 18% in Q4 2024. Polyurethane producers, therefore, face margin compression because residential contractors resist full pass-through price increases. Divergent raw-material trends are shifting share toward silicone in premium applications, while polyurethane suppliers are experimenting with TDI blends that raise occupational-exposure risks. Freight disruptions through the Red Sea add 10-14 days to lead times, compelling distributors to carry higher inventories that tie up working capital.

Other drivers and restraints analyzed in the detailed report include:

- Post-Brexit Infrastructure Stimulus Accelerating Construction Sealant Consumption

- NHS Estate Maintenance Backlog Driving Healthcare-Facility Refurbishment

- Skilled Applicator Shortage Causing Project Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone grades accounted for 33.50% of 2025 demand, anchored by EN 15651-certified applications in healthcare and fire-rated facades. Hybrid Silane-Modified Polymer (SMP) products are forecast to grow at a CAGR of 7.12% annually during the forecast period (2026-2031), the fastest among all resins. That rise aligns with contractor preference for one-component, label-free systems that comply with tightening VOC caps. Polyurethane retains relevance in EV battery packs and industrial flooring because of its chemical resistance and adhesion to dissimilar substrates. Acrylic and polysulfide persist in interior decoration and immersion-zone civil works. Regulatory convergence around ISO 11600 and ASTM C920 is elevating performance thresholds, which is accelerating research and development spend on silicone, SMP, and polyurethane while niche chemistries stagnate.

The competitive effects are already visible. Wacker Chemie expanded UK technical support in 2025, and Sika AG introduced Sikaflex-268 PowerCure for rail carriages, aiming to displace polysulfide with faster SMP curing. Smaller formulators focusing on polysulfide now confine their offers to marine and tidal applications where immersion durability still commands a premium. As building-control officers increasingly request EPDs, suppliers that cannot finance lifecycle assessments are losing specification visibility, reinforcing the leadership of vertically integrated silicone and SMP producers.

List of Companies Covered in this Report:

- 3M

- Adshead Ratcliffe & Co Ltd.

- Arkema

- Bond It Group

- DAP Products

- Dow

- Sika Limited

- Fischer UK

- The Sherwin-Williams Company

- Gorilla Glue Company

- Henkel AG & Co. KGaA

- Hodgson Sealants

- illbruck (Tremco CPG)

- MAPEI S.p.A.

- RPM International Inc.

- Sika AG

- Soudal Group

- Tremco Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for fire-resistant sealants in UK high-rise refurbishments

- 4.2.2 Stricter VOC regulations pushing shift to hybrid silane-terminated polymers

- 4.2.3 Post-Brexit infrastructure stimulus accelerating construction sealant consumption

- 4.2.4 Rising electric-vehicle battery-pack sealing needs

- 4.2.5 NHS estate maintenance backlog driving healthcare-facility refurbishment

- 4.3 Market Restraints

- 4.3.1 Volatility in silicon-metal and MDI raw-material prices

- 4.3.2 Skilled applicator shortage causing project delays

- 4.3.3 Competition from prefabricated gasket solutions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Polysulfide

- 5.1.6 Hybrid Silane-Modified Polymer (SMP)

- 5.1.7 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.3.1 Residential

- 5.2.3.2 Commercial

- 5.2.3.3 Infrastructure

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Adshead Ratcliffe & Co Ltd.

- 6.4.3 Arkema

- 6.4.4 Bond It Group

- 6.4.5 DAP Products

- 6.4.6 Dow

- 6.4.7 Sika Limited

- 6.4.8 Fischer UK

- 6.4.9 The Sherwin-Williams Company

- 6.4.10 Gorilla Glue Company

- 6.4.11 Henkel AG & Co. KGaA

- 6.4.12 Hodgson Sealants

- 6.4.13 illbruck (Tremco CPG)

- 6.4.14 MAPEI S.p.A.

- 6.4.15 RPM International Inc.

- 6.4.16 Sika AG

- 6.4.17 Soudal Group

- 6.4.18 Tremco Incorporated

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)