|

市場調查報告書

商品編碼

2066681

義大利密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Italy Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

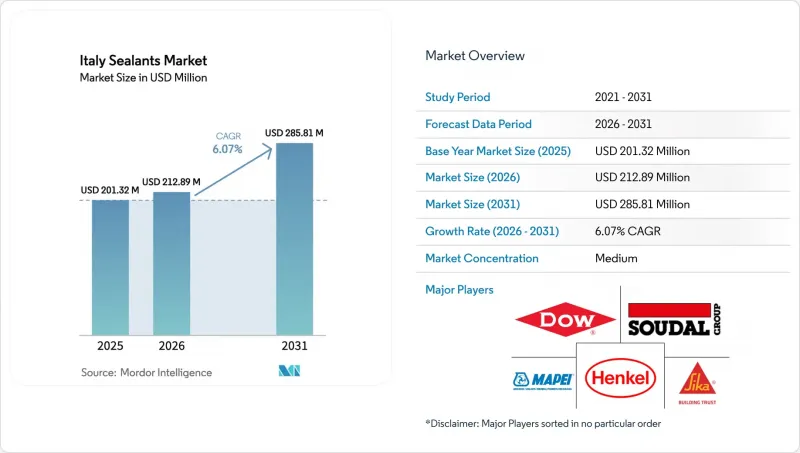

據 Mordor Intelligence 稱,義大利密封劑市場預計將從 2025 年的 2.0132 億美元成長到 2026 年的 2.1289 億美元,到 2031 年達到 2.8581 億美元,2026 年至 2031 年的複合年成長率為 6.07%。

本報告按樹脂類型(丙烯酸樹脂、環氧樹脂、聚氨酯樹脂、矽樹脂及其他樹脂)和終端用戶行業(航太、汽車、建築、醫療及其他終端用戶行業)進行細分。市場規模和預測均以美元計價。

義大利密封膠市場趨勢與洞察

歐盟的「翻新浪潮」正在推動維修的需求。

義大利「復甦與韌性計畫」計畫投入139.5億歐元,用於維修超過10萬棟建築和3,600萬平方公尺的房屋,這將有力支撐義大利密封膠市場的維修熱潮。 2026年預算將繼續對主要住宅維修提供50%的稅額扣抵,確保丙烯酸和低VOC聚氨酯系統的需求穩定成長。 EN 16516和CDPH v1.2基準值(截至28日,總VOC含量低於300µg/m³,甲醛含量低於10µg/m³)提高了配方要求,有利於水性產品,因為水性產品在胺固化過程中也能減少氣味。Lombardia、Lazio和Campania三個大區的房屋存量合計佔目標建築存量的近一半,這為擁有高度集中的區域樞紐的經銷商創造了集中的物流優勢。市場需求正從傳統的矽酮外牆接縫材料轉向混合密封劑,這種密封劑無需底漆即可粘合到各種現有基材上,從而減少了技術純熟勞工的工作時間,而該市場目前已經面臨 265,000 名工人的短缺。

由於電動車電池重量減輕,對密封劑的需求增加。

Stellantis的目標是到2030年將電池重量減輕50%,並已在都靈的電池技術中心投資4,000萬美元。這導致當地對導熱和介電密封劑的需求增加。目前電動車大約使用8磅黏合劑和密封劑,而新的電池單體封裝設計預計到2030年將使這一用量增加到約12磅,從而支撐義大利密封劑市場的長期銷售量成長。 Corano的雙組分聚脲體係可在30秒內固化,因此無需在目前大規模生產的模組中使用機械緊固件。陶氏化學的「VORATRON」系列聚氨酯產品導熱係數為0.3–3.1 W/mK,可實現被動散熱,並顯著降低電池組的重量和體積。這些規格要求動作溫度範圍為-40 度C至85 度C ,介電強度為20 kV/mm或更高,促使化合物設計人員轉向使用矽酮和特殊的聚氨酯基化學物質。

矽酮單體價格波動

由於鉑催化劑價格較去年同期翻番,且受中東原料供應中斷的影響,二甲基二氯矽烷供應減少,瓦克化學在2026年兩次上調了矽酮價格。這令依賴進口85%中間體的義大利化合物生產商陷入困境。鉑金佔矽酮密封劑銷售成本的20%之多,其現貨價格已從2025年的每盎司900美元上漲至2026年3月的每盎司1850美元。陶氏化學宣布將於2026年年中關閉其位於英國巴里的矽氧烷製造地,導致歐洲產能損失,進一步加劇了成本波動,並給法薩·博托洛(Fassa Bortolo)和凱拉科爾(Keracole)等區域性公司的利潤率帶來壓力。

細分市場分析

矽酮密封膠在-60 度C至200 度C的溫度範圍內具有無與倫比的抗紫外線性能,預計在2025年佔據義大利密封膠市場40.50%的佔有率。在義大利密封膠市場中,丙烯酸類產品市場預計到2031年將以7.12%的複合年成長率成長。這主要得益於BASF的水性產品“Acronal 5036”,該產品採用無味胺固化,彈性恢復率超過40%。雖然混合型MS聚合物和聚硫化物的總佔有率仍低於10%,但它們在機場路面和水下結構等特殊接縫領域仍佔據重要地位。

丙烯酸產品的過濾率不斷提高與「超級獎勵」CAM標準直接相關,該標準將VOC(揮發性有機化合物)含量限制在50 g/L以內。溶劑型聚氨酯很難在不犧牲底漆性能的前提下達到此閾值。聚氨酯在結構玻璃製造領域仍佔據主導地位,其抗張強度超過2 MPa,邵氏A硬度為40-60。這些特性對於工業地板材料和外牆錨固連接至關重要。環氧樹脂憑藉其複雜的混合物和化學不滲透性,已在製藥地板和無塵室等細分市場中佔據了一席之地。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 終端用戶趨勢

- 市場促進因素

- 歐盟的「翻新浪潮」提振了維修需求。

- 由於電動車電池重量減輕,對密封劑的需求增加。

- 更嚴格的VOC法規正在加速水基化學品的普及。

- 光伏一體化幕牆需要耐用的邊緣密封條。

- 用於機器人和3D列印結構的混合密封劑

- 市場限制因素

- 矽酮單體價格波動

- 中小企業因CE標誌/CPR合規性而承擔的成本負擔

- 由於熟練技術人員短缺,市場需求正轉向使用密封墊的系統。

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 環氧樹脂

- 聚氨酯

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 衛生保健

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Arkema

- BASF SE

- Dow

- Fassa Bortolo

- General Sealants Inc.

- HB Fuller Company

- Henkel AG & Co. KGaA

- Index SpA

- Kerakoll SpA

- MAPEI SpA

- NPT Srl

- Pidilite Industries Ltd.

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soudal Holding NV

- Torggler Srl

- Tremco CPG Italia

- Wacker Chemie AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the italy sealants market size is expected to increase from USD 201.32 million in 2025 to USD 212.89 million in 2026 and reach USD 285.81 million by 2031, growing at a CAGR of 6.07% over 2026-2031.

This report is Segmented by Resin Type (Acrylic, Epoxy, Polyurethane, Silicone, and Other Resins) and End-User Industry (Aerospace, Automotive, Building and Construction, Healthcare, and Other End-User Industries). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Italy Sealants Market Trends and Insights

EU Renovation Wave-Fuelled Retrofit Demand

Planned spending of EUR 13.95 billion under Italy's Recovery and Resilience Plan covers more than 100,000 buildings and 36 million m2 of upgrades, sustaining retrofit momentum for the Italy Sealants market. The 2026 budget continues a 50% tax bonus on primary-residence renovations, guaranteeing steady pull-through for acrylic and low-VOC polyurethane systems. EN 16516 and CDPH v1.2 thresholds (less than or equal to 300 µg/m3 total VOC and less than or equal to 10 µg/m3 formaldehyde at 28 days) tighten qualifying formulations, favoring waterborne products that also mitigate amine-cure odor. Lombardy, Lazio, and Campania together host nearly half of the eligible building stock, concentrating logistics advantages for distributors with dense regional hubs. Demand shifts away from conventional silicone facade joints toward hybrid sealants able to bond mixed legacy substrates without primers, reducing skilled labor hours in a market already short 265,000 workers.

EV-Battery Lightweighting Sealant Needs

Stellantis targets a 50% battery-weight cut by 2030 and has invested USD 40 million in a Turin Battery Technology Center that boosts local demand for thermally conductive and dielectric sealants. Current electric vehicles carry roughly 8 lb of adhesives and sealants; new cell-to-pack designs may lift content toward 12 lb by 2030, supporting long-run volume upside for the Italy Sealants market. Two-component polyurea systems from Collano deliver 30-s fixture times, eliminating mechanical fasteners in modules now entering series production. Dow's VORATRON polyurethane grades add 0.3-3.1 W/mK thermal conductivity, allowing passive cooling that slashes pack weight and volume. These specifications demand service from -40°C to 85°C and dielectric strength more than or equal to 20 kV/mm, steering formulators toward silicone and specialty polyurethane chemistries.

Silicone-Monomer Price Volatility

Wacker Chemie raised silicone prices twice in 2026 after platinum catalysts doubled YoY and Middle-East feedstock disruptions reduced dimethyldichlorosilane supply, squeezing Italian formulators who import 85% of intermediates. Platinum represents up to 20% of silicone sealant COGS, and spot prices climbed from USD 900/oz in 2025 to USD 1,850/oz by March 2026. Dow's announced closure of its Barry, UK, siloxanes unit in mid-2026 removes European capacity, amplifying cost swings that depress margins for regional firms such as Fassa Bortolo and Kerakoll.

Other drivers and restraints analyzed in the detailed report include:

- Stricter VOC Limits Accelerating Water-Based Chemistries

- BIPV Facades Requiring Edge-Seal Longevity

- CE-Mark/CPR Compliance Cost Burden for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone commanded a 40.50% hold on the Italy Sealants market share in 2025, supported by unrivaled UV stability across -60°C to 200°C service windows. The Italy Sealants market size for acrylic formulations is projected to climb at a 7.12% CAGR through 2031, buoyed by BASF's waterborne Acronal 5036 that delivers more than or equal to 40% elastic recovery without amine-cure odor. Hybrid MS polymers and polysulfides together remain below 10% of volume, yet retain footholds in specialty joints such as airport pavements and submerged structures.

Acrylic's rising penetration links directly to Superbonus CAM criteria that cap VOC at 50 g/L, a threshold that solvent-borne polyurethane struggles to meet without primer sacrifices. Polyurethane continues to dominate structural glazing with tensile strengths of more than 2 MPa and Shore A 40-60, crucial to industrial flooring and facade anchor joints. Epoxy holds a niche in pharmaceutical floors and cleanrooms, leveraging chemical impermeability despite mixing complexity.

List of Companies Covered in this Report:

- 3M

- Arkema

- BASF SE

- Dow

- Fassa Bortolo

- General Sealants Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Index S.p.A.

- Kerakoll S.p.A.

- MAPEI S.p.A.

- NPT Srl

- Pidilite Industries Ltd.

- RPM International Inc.

- Saint-Gobain Weber

- Sika AG

- Soudal Holding N.V.

- Torggler S.r.l.

- Tremco CPG Italia

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 End-User Trends

- 4.3 Market Drivers

- 4.3.1 EU "Renovation Wave"-fuelled retrofit demand

- 4.3.2 EV-battery lightweighting sealant needs

- 4.3.3 Stricter VOC limits accelerating water-based chemistries

- 4.3.4 BIPV facades requiring edge-seal longevity

- 4.3.5 Robotic/3-D printed construction compatible hybrid sealants

- 4.4 Market Restraints

- 4.4.1 Silicone-monomer price volatility

- 4.4.2 CE-mark/CPR compliance cost burden for SMEs

- 4.4.3 Trade-skills shortage shifting demand to pre-gasketed systems

- 4.5 Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Resins

- 5.2 By End-user Industry

- 5.2.1 Aerospace

- 5.2.2 Automotive

- 5.2.3 Building and Construction

- 5.2.4 Healthcare

- 5.2.5 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 BASF SE

- 6.4.4 Dow

- 6.4.5 Fassa Bortolo

- 6.4.6 General Sealants Inc.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Index S.p.A.

- 6.4.10 Kerakoll S.p.A.

- 6.4.11 MAPEI S.p.A.

- 6.4.12 NPT Srl

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 RPM International Inc.

- 6.4.15 Saint-Gobain Weber

- 6.4.16 Sika AG

- 6.4.17 Soudal Holding N.V.

- 6.4.18 Torggler S.r.l.

- 6.4.19 Tremco CPG Italia

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測

建築和施工密封膠市場規模、佔有率和成長分析:按類型、應用、固化類型、最終用戶、分銷管道、功能和地區分類—2026-2033年產業預測 密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)日本密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)法國密封膠:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)馬來西亞密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

2026-2034年全球建築和施工密封劑市場規模、佔有率、趨勢和成長分析報告新加坡密封劑:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

耐燃料密封劑市場:2026-2032年全球市場預測(依樹脂類型、形態、固化機制、包裝、應用分類)泰國密封劑市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)中國密封膠市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)