|

市場調查報告書

商品編碼

2065501

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)North America Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

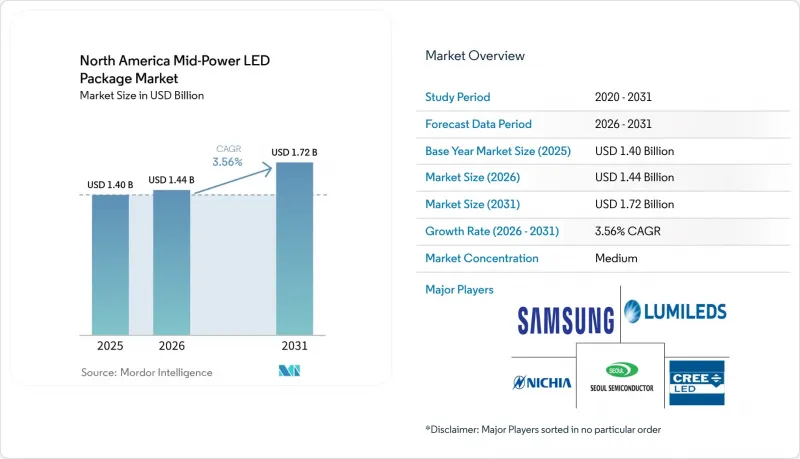

根據 Mordor Intelligence 預測,北美中中功率LED構裝市場規模將從 2025 年的 14 億美元和 2026 年的 14.4 億美元成長到 2031 年的 17.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 3.56%。

本報告按輸出功率範圍(0.2–0.5 W 和 0.5–小於 1 W)、封裝結構(SMD 和 CSP,包括 2835、3014、3030 等)、應用領域(通用照明、汽車照明、顯示和背光、特殊和利基應用)以及國家/地區(美國、加拿大、墨西哥)進行細分。市場預測以美元 (USD) 為單位。

北美中功率LED構裝市場趨勢與洞察

汽車LED要求標準化

加拿大運輸部第8版TSD 108標準於2025年10月強制實施,使其發光強度和耐久性法規與美國FMVSS 108標準保持一致。一級供應商目前正在為北美地區設計單一模組平台,主要採用功率範圍在0.5瓦至0.8瓦之間的中功率封裝陣列。與密度較低的高功率叢集相比,這些陣列的散熱更加均勻。美國國家公路交通安全管理局(NHTSA)在2024年拒絕放寬自我調整光束的眩光閾值,進一步凸顯了高密度陣列在複雜光學系統中保持均勻亮度的必要性。 SAE J1889標準於2025年4月新增了加速熱循環測試,有利於結溫較低的中功率封裝。墨西哥於2026年2月公佈的汽車戰略表明,未來將批准矩陣式和連續式功能,預計這將進一步增加每輛車上的裝置數量。這些統一的要求加在一起,正在推動號誌、日行燈和自我調整系統對中功率LED 的需求增加。

節能建築標準的快速提高

加州「Title 24-2025」規定,自2026年1月起,照明功率密度最多降低15%;而IECC 2024則要求在2026年採用該標準的城市中,照明設備需持續調光至10%的功能,並需具備更廣泛的人員佔用檢測功能。奧勒岡州的「2026年住宅專用建築特殊標準」和紐約市的「2025年能源效率標準」也增加了類似的規定,將高人流量場所的維修投資回收期縮短至12-18個月。中功率燈具可與傳統的恆定電流驅動器無縫整合,使承包商能夠重複利用現有線路並最大限度地減少運作,從而加快專案批准。中西部和東南部的電力公司繼續為每個獲得DLC認證的燈具提供30至80美元的補貼,其中大多數燈具使用2835或3030中功率LED。儘管第一波改造浪潮趨於平緩,但由於更嚴格的法規和退稅帶來的經濟效益,總體而言,維修工程的數量仍然很高。

磷光體材料供應鏈中的脆弱性

中國在2025年4月和10月實施的稀土元素出口限制,使得銪、鋱和釔的出口受到許可證限制,導致中國以外現貨市場的價格飆升。美國釔進口量在八個月內從333噸驟降至17噸,臨時庫存僅能滿足一到兩季的LED磷光體需求。經談判,限制措施暫停一年,全面實施延後至2026年11月。然而,這種情況凸顯了單一供應來源的風險,促使原始設備製造商(OEM)要求雙軌供應認證,並制定不含稀土元素的磷光體藍圖。

細分市場分析

受商業維修和汽車訊號燈需求的推動,預計到2025年,功率在0.5瓦至1瓦以下的LED封裝產品將佔據北美中中功率LED構裝市場61.88%的佔有率,成為該細分市場中最大的市場佔有率。如此高的市場佔有率反映了發光效率的穩定提升,使設計人員能夠以更少的二極體實現流明目標,並減少貼片工藝和驅動通道的數量。展望下一個預測期,該功率範圍預計將以3.96%的複合年成長率成長,超越低功率和接近1瓦的功率範圍,因為OEM廠商從熱可靠性的角度出發,將目光聚焦於這一「最佳功率區間」。

隨著加州能源法規第24條和國際電工委員會(IECC)法規的日益嚴格,照明設備製造商已將產品功率從0.2瓦至0.5瓦的裝置轉向中階。這是因為更高功率的封裝可以採用更薄的基板,並簡化控制。汽車產業的一級供應商在SAE修訂了熱循環測試標準,確認其在振動條件下的可靠性後,已開始在其日間行車燈(DRL)和矩陣陣列應用中使用0.6瓦至0.8瓦的發送器。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 汽車LED要求標準化

- 節能建築標準的快速提高

- 降低中功率LED晶片的成本

- 垂直農場中園藝照明的快速發展

- 將可調光白光LED整合到以人為本的照明系統中

- 擴大電力公司對中功率LED照明燈具的補貼計劃

- 市場限制因素

- 來自亞洲低成本進口商品的價格壓力

- 當超過 1W 的上限時,溫度控管將面臨挑戰。

- 磷光體材料供應鏈中的脆弱性

- 商業地產維修週期延誤

- 產業價值鏈分析

- 技術展望

- 監理情勢

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 0.2~0.5 W

- 0.5 至小於 1 瓦

- 依封裝架構

- SMD(表面黏著型元件)

- 2835

- 3014

- 3030

- 其他(3528、3020、5050 等)

- CSP(晶片級封裝)

- SMD(表面黏著型元件)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 專業/小眾

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Lumileds Holding BV

- Cree LED Inc.

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- OSRAM Opto Semiconductors GmbH

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Lite-On Technology Corporation

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

- Epistar Corporation

- Bridgelux, Inc.

- MLS Co., Ltd.

- Bridgelux, Inc.

- Dominant Opto Technologies Sdn. Bhd.

- Toyoda Gosei Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america mid-power LED package market size is projected to expand from USD 1.40 billion in 2025 and USD 1.44 billion in 2026 to USD 1.72 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Mid-Power LED Package Market Trends and Insights

Standardization of Automotive LED Requirements

Transport Canada TSD 108 Revision 8 became mandatory in October 2025, aligning the photometric and durability rules with U.S. FMVSS 108. Tier-1 suppliers now engineer a single module platform for the continent, and that platform predominantly specifies arrays of 0.5 W to 0.8 W mid-power packages, which spread heat more evenly than sparse high-power clusters. NHTSA's refusal in 2024 to relax adaptive-beam glare thresholds reinforces the need for high-density arrays that maintain uniform luminance across complex optics. SAE J1889 added accelerated thermal-cycling tests in April 2025, favoring lower-junction-temperature mid-power packages. Mexico's February 2026 automotive strategy signals future approvals for matrix and sequential functions, further increasing device count per vehicle. Together, the harmonized requirements expand demand for mid-power LEDs in signal, DRL, and adaptive systems.

Surge In Energy-Efficient Building Codes

California Title 24-2025 lowered lighting power densities by up to 15%, effective January 2026, while IECC 2024 calls for continuous dimming to 10% and broader occupancy sensing in cities that adopted the code in 2026. Oregon's 2026 Residential Specialty Code and New York City's 2025 Energy Conservation Code add similar controls, shortening retrofit paybacks to as little as 12-18 months in high-use spaces. Because mid-power packages integrate seamlessly with legacy constant-current drivers, contractors can reuse wiring and minimize downtime, thereby accelerating project approvals. Utilities in the Midwest and Southeast continue to offer rebates of USD 30-80 per DLC-qualified luminaire, and most of those fixtures use 2835 or 3030 mid-power LEDs. Collectively, stricter codes and rebate economics sustain high retrofit volumes despite plateauing first-wave conversions.

Supply Chain Vulnerability for Phosphor Materials

China's rare-earth export curbs in April and October 2025 placed europium, terbium, and yttrium under license, driving multi-fold price spikes in non-Chinese spot markets. U.S. yttrium imports collapsed from 333 t to 17 t within eight months, and stopgap stockpiles can cover only one to two quarters of LED phosphor demand. A negotiated one-year suspension defers full enforcement to November 2026, yet the episode spotlighted single-source risk, prompting OEMs to request dual-supply certification or non-rare-earth phosphor roadmaps.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost of Mid-Power LED Chips

- Rapid Expansion of Horticulture Lighting in Vertical Farms

- Slow Retrofit Cycle in Commercial Real Estate Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Commercial retrofits and automotive signal lamps together propelled the 0.5 W-to-Less Than 1 W class to a 61.88% share in 2025, the highest in the North America mid-power LED package market. That weight reflects steady gains in efficacy that let designers hit lumen targets with fewer diodes, reducing pick-and-place steps and driver channel counts. Moving to the next forecast period, the same class is forecast to grow at a 3.96% CAGR, outperforming both lower-wattage and near-1 W classes as OEMs converge on this sweet spot for thermal reliability.

Fixture makers migrated from 0.2 W to 0.5 W devices toward the mid-range as Title 24 and IECC constraints tightened, as higher-wattage packages allow slimmer boards and simpler controls. Automotive Tier-1 suppliers enlarged DRL and matrix arrays with 0.6 W-to-0.8 W emitters after SAE revised thermal-cycling tests, confirming reliability under vibration.

List of Companies Covered in this Report:

- Nichia Corporation

- Lumileds Holding B.V.

- Cree LED Inc.

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- OSRAM Opto Semiconductors GmbH

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Lite-On Technology Corporation

- Lextar Electronics Corporation

- NationStar Optoelectronics Co., Ltd.

- Epistar Corporation

- Bridgelux, Inc.

- MLS Co., Ltd.

- Bridgelux, Inc.

- Dominant Opto Technologies Sdn. Bhd.

- Toyoda Gosei Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Standardization of Automotive LED Requirements

- 4.2.2 Surge in Energy-Efficient Building Codes

- 4.2.3 Declining Cost of Mid-Power LED Chips

- 4.2.4 Rapid Expansion of Horticulture Lighting in Vertical Farms

- 4.2.5 Integration of Tunable White LEDs in Human-Centric Lighting

- 4.2.6 Expansion of Utility Rebate Programs Targeting Mid-power LED Fixtures

- 4.3 Market Restraints

- 4.3.1 Price Pressure From Low-Cost Asian Imports

- 4.3.2 Thermal Management Challenges Above 1 W Ceiling

- 4.3.3 Supply Chain Vulnerability For Phosphor Materials

- 4.3.4 Slow Retrofit Cycle in Commercial Real Estate Segment

- 4.4 Industry Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Cree LED Inc.

- 6.4.4 Samsung Electronics Co., Ltd.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 OSRAM Opto Semiconductors GmbH

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Lite-On Technology Corporation

- 6.4.10 Lextar Electronics Corporation

- 6.4.11 NationStar Optoelectronics Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Bridgelux, Inc.

- 6.4.14 MLS Co., Ltd.

- 6.4.15 Bridgelux, Inc.

- 6.4.16 Dominant Opto Technologies Sdn. Bhd.

- 6.4.17 Toyoda Gosei Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)