|

市場調查報告書

商品編碼

2063979

中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)China Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

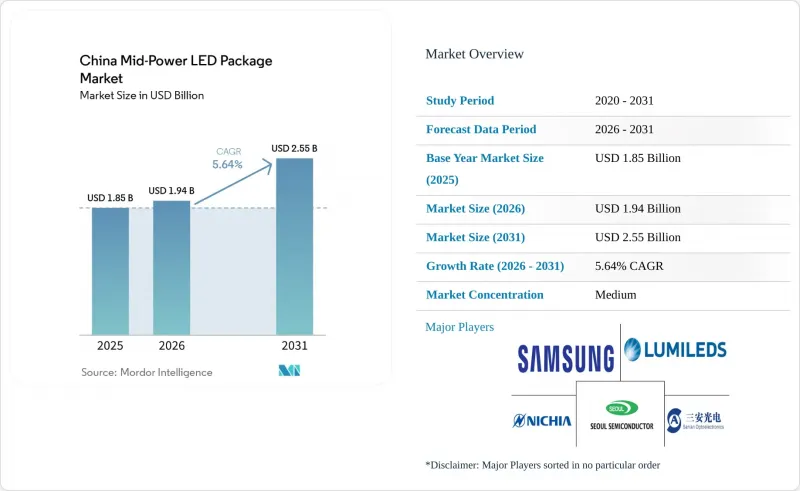

根據Mordor Intelligence預測,中國中功率LED構裝市場規模預計在2025年達到18.5億美元,2026年達到19.4億美元,2031年達到25.5億美元,2026年至2031年的複合年成長率為5.64%。

本報告按輸出功率範圍(0.2–0.5W 和 0.5–1W)、封裝結構(SMD 和 CSP,包括 2835、3014、3030 等)以及應用領域(通用照明、汽車照明、顯示器和背光以及特殊/小眾應用)進行細分。市場預測以美元 (USD) 為單位。

中國中功率LED構裝市場趨勢及洞察。

中國二線城市對節能照明的需求日益成長

在合肥、潛江、銅陵和增城等城市,透過能源績效合約資金籌措的市政照明維修專案正在不斷擴大,單燈物聯網控制技術可將維護回應時間縮短高達80%。檢驗的節能保證使私人投資者能夠在9-10年內收回專案成本,從而催生了對性能可預測的中功率LED構裝的需求。 GB 30255-2026標準將最低光通量效率提高到105 lm/W,並將待機功耗限制在0.5 W,因此,功率低於0.5 W(小於1 W)的高效LED封裝成為路燈維修的首選。隨著越來越多的二線城市設定在2030年實現碳排放達峰的目標,維修計畫儲備正在增加,這支撐了未來幾年的需求預測。這一趨勢正推動供應商專注於滿足新的光學性能和閃爍限制的長壽命陶瓷和覆晶SMD封裝技術。

政府補貼計畫促進LED製造業的進步

財政部已撥款936億元人民幣(約130億美元)用於碳減排項目,中國人民銀行也設立了8,000億元人民幣(約1,110億美元)的低成本再融資機制,以加速工廠升級改造。這些資金正推動垂直整合專案的發展,例如TCL華照光電收購福州華照光電,以及國星光電和利亞德光電的產能擴張。補貼標準傾向於生產Mini/Micro LED、汽車級和園藝級封裝且能源效率超過中國能源效率等級1級標準的生產線,這進一步推動了市場佔有率轉移到垂直整合型企業。省政府也增加了配套津貼,最高可達新設備成本的20%,加速了高速覆晶鍵合機和自動化磷光體噴塗生產線的引進。因此,缺乏資金和汽車級認證的中小型封裝製造商在補貼訂單中處於劣勢。

中國LED構裝線產能過剩導致價格下降

從2022年到2025年,由於新參與企業產能擴張速度超過市場需求,中功率產品的平均售價有所下降。儘管在2026年初,由於行業整體的努力,價格有所回升,但通用照明產品市場仍面臨供應過剩的問題。零售商行事謹慎,不願將成本上漲轉嫁給消費者,導致封裝產品製造商的營運資金週轉週期延長。 2025年,原物料價格波動導致黃金、白銀和銅價飆升,對毛利率造成壓力。到2025年第三季度,這一趨勢已十分明顯,市場主要參與者三安光電公佈的利潤率下降數據印證了這一點。雖然市場重組有望增強定價權,但缺乏專有技術的小型供應商面臨著在市場達到平衡之前被淘汰的迫切威脅。

細分市場分析

2025年,功率範圍在0.5W至1W以下的LED封裝產品將佔據中國中中功率LED構裝市場62.1%的佔有率,預計到2031年,其市場規模將以5.99%的複合年成長率成長。此功率範圍的產品在光通量、散熱和成本之間取得了良好的平衡,使其成為室內照明、路燈以及Mini LED局部調光區域的關鍵產品。結溫為125度C的陶瓷和覆晶3030封裝產品正逐漸取代塑膠封裝,應用於汽車側標誌燈和日間行車燈。

材料技術的進步,例如效率高達 5.05 µmol J⁻¹ 的深紅色 3535 型園藝 LED,正推動該領域向環境可控農業領域拓展。基於 GB 31831-2025 標準日益嚴格的發光效率目標,以及更嚴格的閃爍標準,進一步鞏固了 0.5 W 中電流發光裝置的應用。 0.2–0.5 W 低功率元件在裝飾燈條和攜帶式設備領域仍佔據一席之地,而 1 W 以下的封裝裝置則正向高棚照明和紫外線市場轉移。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國主要城市對節能照明的需求日益成長

- 政府補貼計畫促進LED製造業的進步

- 汽車LED大燈的迅速普及

- 電視和顯示器中Mini-LED背光技術的應用正在迅速成長。

- 增加對智慧城市基礎建設照明的投資

- 透過地緣政治技術自給自足實現LED供應鏈本地化

- 市場限制因素

- 中國LED構裝線產能過剩導致價格下降

- 高純度磷光體供應鏈中斷

- 針對藍光危害制定了嚴格的規定,限制驅動電流。

- 採用整合式COB和高功率封裝的競爭方案

- 產業價值鏈分析

- 技術展望

- 監理情勢

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 0.2~0.5 W

- 0.5 至小於 1 瓦

- 所以

- SMD(表面黏著型元件)

- 2835

- 3014

- 3030

- 其他(3528、3020、5050 等)

- CSP(晶片級封裝)

- SMD(表面黏著型元件)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 專業/小眾

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- Cree LED, Inc.

- ams Osram GmbH

- Shenzhen NationStar Optoelectronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- MLS Co., Ltd.(Forest Lighting)

- Lextar Electronics Corporation

- Bridgelux, Inc.

- Shenzhen Jufei Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Lite-On Technology Corporation

- Toyoda Gosei Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the china mid-power LED package market size is projected to be USD 1.85 billion in 2025, USD 1.94 billion in 2026, and reach USD 2.55 billion by 2031, growing at a CAGR of 5.64% from 2026 to 2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others, and CSP), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

China Mid-Power LED Package Market Trends and Insights

Growing Demand for Energy-Efficient Lighting in China's Tier-2 Cities

Municipal retrofits financed through energy-performance contracts are scaling across Hefei, Qianjiang, Tongling, and Zengcheng, where single-lamp IoT controls cut maintenance response times by as much as 80%. Verified energy-savings guarantees allow private investors to recover project costs over 9- to 10-year terms, creating a predictable mid-power LED package pull-through. The GB 30255-2026 standard boosts minimum efficacy to 105 lm/W and caps standby power at 0.5 W, thereby favoring high-efficacy 0.5 W- less than 1 W packages for streetlighting retrofits. As more Tier-2 cities commit to carbon-peaking goals before 2030, retrofit pipelines are lengthening, underpinning multi-year demand visibility. The dynamic is reinforcing supplier interest in long-lifetime ceramic and flip-chip SMD formats that meet the new optical and flicker limits.

Government Subsidy Programs for Industrial Upgrades in LED Manufacturing

The Ministry of Finance earmarked RMB 93.6 billion (USD 13 billion) for carbon-reduction projects, while the People's Bank of China opened RMB 800 billion (USD 111 billion) in low-cost refinancing to accelerate factory upgrades. These funds are underwriting vertical-integration deals such as TCL CSOT's purchase of Fuzhou Huazhao Optoelectronics and capacity expansions at NationStar and Leyard. Subsidy criteria favor lines producing Mini/Micro LED, automotive, and horticultural packages that exceed Level 1 China Energy Label thresholds, further tilting market share toward integrated players. Provincial governments add matching grants that offset up to 20% of new equipment costs, hastening adoption of high-speed flip-chip bonders and automated phosphor-spray lines. Smaller packagers lacking capital or automotive-grade qualifications are consequently losing bids for subsidy-linked orders.

Price Erosion Due To Overcapacity in Chinese LED Packaging Lines

Between 2022 and 2025, new entrants ramped up capacity faster than demand, leading to a drop in average selling prices for mid-power packages. While a concerted effort in early 2026 led to a price rebound, the market still grapples with an oversupply of commodity lighting. Retailers tread carefully, hesitant to transfer rising costs to consumers, which in turn elongates working-capital cycles for packagers. In 2025, fluctuations in raw-material prices led to surges in gold, silver, and copper prices, exerting pressure on gross margins. By Q3 2025, this was evident as San'an Optoelectronics, a key market player, reported a dip in its margins. While consolidation in the market promises to bolster pricing power, smaller vendors lacking unique technology face the looming threat of being edged out before market equilibrium is achieved.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Automotive LED Headlamp Adoption

- Surge In Mini-LED Backlight Adoption in TVs And Monitors

- Supply Chain Disruptions for High-Purity Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W- Less Than 1 W class accounted for 62.1% of the China mid-power LED package market share in 2025, with its market size forecast to expand at a 5.99% CAGR to 2031. This range balances luminous flux, heat dissipation, and cost, making it the workhorse for indoor lamps, streetlights, and Mini LED local-dimming zones. Ceramic and flip-chip 3030 formats rated to 125 °C junction temperature are increasingly displacing plastic packages in automotive side markers and daytime running lamps.

Material advances, such as deep-red 3535 horticultural LEDs with an efficiency of 5.05 µmol J-1, extend the segment into controlled-environment agriculture. Tightening efficacy targets under GB 31831-2025, plus stricter flicker metrics, further entrench the adoption of mid-current 0.5 W emitters. Lower-power 0.2-0.5 W devices keep a niche in decorative strips and portable gadgets, while less than or equal to 1 W packages migrate toward high-bay and UV markets.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- Cree LED, Inc.

- ams Osram GmbH

- Shenzhen NationStar Optoelectronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Lextar Electronics Corporation

- Bridgelux, Inc.

- Shenzhen Jufei Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Lite-On Technology Corporation

- Toyoda Gosei Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Energy-Efficient Lighting in China's Tier-2 Cities

- 4.2.2 Government Subsidy Programs for Industrial Upgrades in LED Manufacturing

- 4.2.3 Rapid Expansion of Automotive LED Headlamp Adoption

- 4.2.4 Surge in Mini-LED Backlight Adoption in TVs and Monitors

- 4.2.5 Rising Investments in Smart City Infrastructure Lighting

- 4.2.6 Localization of LED Supply Chain Due to Geopolitical Tech Self-Reliance

- 4.3 Market Restraints

- 4.3.1 Price Erosion Due to Overcapacity in Chinese LED Packaging Lines

- 4.3.2 Supply Chain Disruptions for High-Purity Phosphors

- 4.3.3 Stringent Blue-Light Hazard Regulations Limiting Drive Current

- 4.3.4 Competition from Integrated COB and High-Power Packages

- 4.4 Industry Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Cree LED, Inc.

- 6.4.6 ams Osram GmbH

- 6.4.7 Shenzhen NationStar Optoelectronics Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Hongli Zhihui Group Co., Ltd.

- 6.4.10 Refond Optoelectronics Co., Ltd.

- 6.4.11 San'an Optoelectronics Co., Ltd.

- 6.4.12 MLS Co., Ltd. (Forest Lighting)

- 6.4.13 Lextar Electronics Corporation

- 6.4.14 Bridgelux, Inc.

- 6.4.15 Shenzhen Jufei Optoelectronics Co., Ltd.

- 6.4.16 Dominant Opto Technologies Sdn. Bhd.

- 6.4.17 Lite-On Technology Corporation

- 6.4.18 Toyoda Gosei Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)