|

市場調查報告書

商品編碼

2064347

美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)United States Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

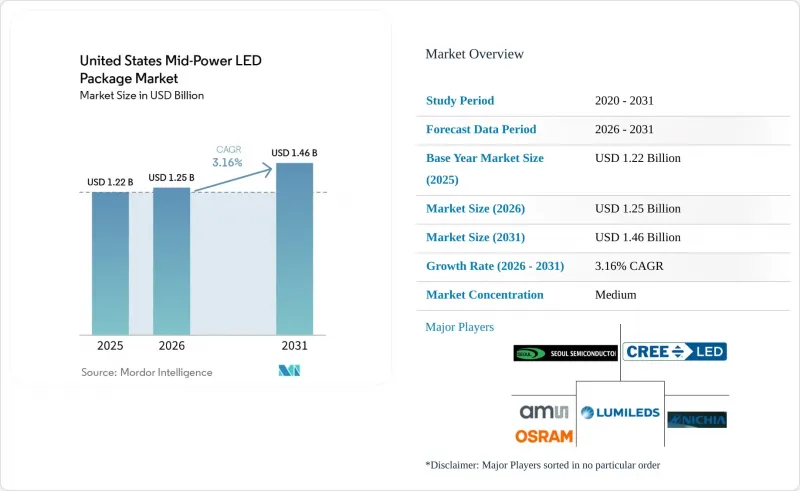

根據 Mordor Intelligence 預測,美國中中功率LED構裝市場規模預計到 2025 年將達到 12.2 億美元,到 2026 年將達到 12.5 億美元,到 2031 年將達到 14.6 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 3.16%。

本報告按輸出功率範圍(0.2W–0.5W、0.5W–1W)、封裝結構(SMD、CSP)和應用領域(通用照明、汽車照明、顯示器背光、特殊/小眾應用)進行分類。市場預測以美元(USD)計價。

美國中功率LED構裝市場趨勢與洞察

商業設施維修中節能照明的快速普及

目前,公用事業補貼計畫涵蓋了美國約四分之三的電力用戶。隨著2026年將連網照明目標產品納入補貼範圍,建築業主正逐步將照明設備從第二代LED升級到LED。通貨膨脹控制法案將節能超過25%的項目的第179D條攤銷補貼提高至每平方英尺5美元,有效縮短了高顯色指數(CRI)中功率LED陣列的投資回收期至三年以內。有些倉庫用150瓦LED高棚燈替換了400瓦金鹵燈,報告指出節能60%,垂直照明效果也提升。同時,運動感測器和自然光利用的普及增加了每個燈具的發光元件數量。儘管照明燈具總出貨量已趨於穩定,但發光元件密度的增加正在推動封裝需求的成長,即使在成熟的建築市場中,也支撐著美國中功率LED構裝市場的發展。加州和紐約州的區域性項目增加了對閃爍和色度的嚴格目標,這鼓勵採用優質產品,從而為國內供應商帶來更高的利潤率。

LED在汽車外部照明的廣泛應用。

隨著美國聯邦機動車輛安全標準 (FMVSS) 108 允許在全美範圍內自我調整遠光燈,福特、通用汽車和 Stellantis 計劃在其所有 2027 款輕型卡車上引入矩陣式頭燈。每個模組整合了 40 至 120 個可獨立控制的中功率LED(通常為 0.5W 聚光燈),可調暗特定區域以避免眩光。 LG Innotek 憑藉其 Nexlide Pixel 平台(已獲得 88 款車型共 146 份訂單)的目標是到 2030 年實現 7.31 億美元的汽車照明年銷售額。此外,尾燈也正轉向採用分段式 LED,用於動畫效果和車對車通訊,其封裝數量是傳統靜態陣列的兩倍。由於汽車製造商要求符合 AEC-Q102 標準並提供 15 年保修,因此平均售價 (ASP) 不受困擾通用照明等級的價格壓力的影響,從而支持了美國中功率LED構裝市場的成長。

亞洲激烈的競爭導致價格下降

中國廠商如國星科技和億光科技利用垂直整合的藍寶石和外延生產線,將0.5W元件的現金成本降至0.02美元以下,使得中功率封裝的平均售價在2025年之前的四年內下降了30%至40%。儘管2026年1月黃金和銅線現貨價格的飆升使得中國當地供應商得以將標價提高至多10%,暫時緩解了美國供應商的壓力,但結構性成本差距依然存在。因此,照明燈具OEM廠商正在採取雙通路採購策略:從海外採購通用SKU,同時為符合AEC-Q102和ISO 13485標準的專案尋找國內供應商,由於可追溯性和客製化分檔,這些項目的價格溢價為15%至20%。這種策略持續對維修市場的利潤率造成巨大壓力,儘管存在一些細分市場的利多因素,但仍抑制了美國中功率LED構裝市場的整體複合年成長率。

細分市場分析

2025年,功率在0.5W至1W以下的LED封裝產品將占美國中中功率LED構裝市場63.19%的佔有率,預計到2031年將以3.88%的複合年成長率成長。工業設施以150W LED高棚燈取代400W金鹵燈時,通常使用24至36個此類中功率封裝的LED,即可在160 lm/W的能源效率比下實現18,000至22,000流明的光通量,同時利用被動式鋁製散熱器將結溫保持在75 度C以下。此類LED也常用於園藝照明,因為它能將光子分散到更多發光元件上,從而最大限度地減少樹冠中的光斑,並且只需通過驅動器設置即可簡化頻譜調節,無需更換燈具。

雖然0.2-0.5瓦的裝置已應用於穿戴式裝置和側發光標牌,但隨著消費品小型化進程趨於平緩,以及汽車設計師傾向於將環境照明模組整合到幾顆中功率晶片中以簡化佈線,該領域的擴張速度正在放緩。由於消毒流程需要更快的劑量輸送,專用紫外線產品的耗電量也不斷增加。日亞化學工業株式會社的280奈米NCSU434D(輸出功率135毫瓦)就是一個典型的例子,它展現了曾經的低功率小眾市場如何向中功率方向發展,並鞏固了其在美國中中功率LED構裝行業的核心地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 商業設施維修中節能照明的快速普及

- LED在汽車外部照明的廣泛應用。

- 美國垂直農場中園藝照明應用的擴大

- 根據《晶片封裝法案》(CHIPS Act),聯邦政府對國內半導體封裝給予優惠待遇。

- MiniLED背光技術在高級電視和顯示器中的廣泛應用。

- WELL和LEED建築中可調光白光照明標準的出現。

- 市場限制因素

- 由於與亞洲國家的激烈競爭,價格下降

- 緊湊型照明燈具設計中的溫度控管挑戰

- 銦和鎵價格波動所帶來的供應鏈風險

- CSP可靠性測試協定標準化進程中的延誤

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 0.2 W~0.5 W

- 0.5 W~1 W

- 所以

- SMD(表面黏著型元件)

- 2835

- 3014

- 3030

- 其他(3528、3020、5050 等)

- CSP(晶片級封裝)

- SMD(表面黏著型元件)

- 透過使用

- 一般照明

- 汽車照明

- 顯示背光

- 特殊/小眾應用

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ams OSRAM AG

- Nichia Corporation

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- Cree LED, a business of Smart Global Holdings

- Samsung Electronics Co., Ltd.

- Lite-On Technology Corporation

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corporation

- LG Innotek Co., Ltd.

- Nationstar Optoelectronics Co., Ltd.

- Bridgelux, Inc.

- Dominant Opto Technologies Sdn. Bhd.

- Epistar Corporation

- Sanan Optoelectronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- Stanley Electric Co., Ltd.

- Osram Opto Semiconductors GmbH

- Refond Optoelectronics Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states mid-power LED package market size is projected to be USD 1.22 billion in 2025, USD 1.25 billion in 2026, and reach USD 1.46 billion by 2031, growing at a CAGR of 3.16% from 2026 to 2031.

This report is Segmented by Power Range (0. 2 W To 0. 5 W, and 0. 5 W To Less Than 1 W), Package Architecture (Surface Mount Device, and Chip Scale Package), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty and Niche). The Market Forecasts are Provided in Terms of Value (USD).

United States Mid-Power LED Package Market Trends and Insights

Rapid Adoption Of Energy-Efficient Lighting In Commercial Retrofits

Utility rebate programs now cover roughly three-quarters of U.S. electricity customers, and 2026 expansions added networked luminaires to eligible product lists, pushing building owners toward second-generation LED-to-LED upgrades. The Inflation Reduction Act raised the Section 179D write-off to USD 5.00 per square foot for projects that cut lighting energy by at least 25%, effectively lowering payback to under three years for high-CRI mid-power arrays. Warehouses replacing 400 W metal-halide fixtures with 150 W LED high bays report 60% energy savings and better vertical illumination, while the move to occupancy sensing and daylight harvesting increases emitter count per fitting. Higher emitter density boosts package demand even though total luminaire shipments have plateaued, sustaining the United States mid-power LED package market during a mature construction cycle. Regional programs in California and New York add stretch targets on flicker and chromaticity, driving uptake of premium bin grades that carry healthier margins for domestic suppliers.

Increasing LED Penetration In Automotive Exterior Lighting

Federal Motor Vehicle Safety Standard 108 now allows adaptive driving beams nationwide, prompting Ford, General Motors, and Stellantis to roadmap matrix headlamps across 2027 model-year light-trucks. Each module integrates 40-120 individually addressable mid-power LEDs, typically 0.5 W CSPs, that dim exact zones to avoid glare. LG Innotek targets USD 731 million in annual automotive-lighting sales by 2030 on the back of its Nexlide Pixel platform, which has already booked 146 orders spanning 88 vehicle models. Rear lamps are also migrating to segmented LEDs for animation and vehicle-to-vehicle signaling, doubling package counts versus static arrays. Because automakers require AEC-Q102 and 15-year warranties, ASPs remain insulated from the price compression hurting general-lighting grades, sustaining growth in the United States mid-power LED package market.

Price Erosion Owing To Intense Asian Competition

Average selling prices for mid-power packages fell 30-40% in the four years to 2025 as Chinese makers such as Nationstar and Everlight leveraged vertically integrated sapphire and epitaxy lines to push cash costs below USD 0.02 per 0.5 W part. A January 2026 spot hike for gold and copper wire prompted mainland suppliers to lift list prices by up to 10%, offering temporary relief to U.S. vendors, yet the structural cost gap persists. Luminaire OEMs therefore dual-source, procuring commodity SKUs offshore while reserving domestic suppliers for AEC-Q102 or ISO 13485 projects that carry 15-20% price premiums for traceability and custom binning. The tactic keeps margin pressure acute in retrofit channels, restraining the overall United States mid-power LED package market CAGR despite segment-specific tailwinds.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use Of Horticultural Lighting By U.S. Vertical Farms

- Federal Incentives For Domestic Semiconductor Packaging Under CHIPS Act

- Thermal Management Challenges In Compact Luminaire Designs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W to Less Than 1 W class accounted for 63.19% of 2025 revenue in the United States mid-power LED package market, and it is projected to expand at a 3.88% CAGR through 2031. Industrial facilities swapping 400 W metal-halide fittings for 150 W LED high bays typically use 24-36 of these mid-tier packages to achieve 18,000-22,000 lumens at 160 lm W-1 while maintaining junction temperatures below 75 °C with passive aluminum heat sinks. Horticultural arrays likewise favor this class because distributing photons across a larger emitter count minimizes canopy hotspots and simplifies spectral tuning via driver settings rather than fixture swaps.

Wearables and edge-lit signage rely on 0.2-0.5 W devices, but that slice is expanding more slowly as consumer miniaturization plateaus and automotive designers consolidate ambient modules into fewer mid-power chips to simplify harnessing. Specialty ultraviolet products are nudging power upward as disinfection protocols demand faster dose delivery. Nichia's 280 nm NCSU434D at 135 mW output exemplifies how once-low-power niches are converging toward mid-range wattages, reinforcing the core position of this class in the United States mid-power LED package industry.

List of Companies Covered in this Report:

- ams OSRAM AG

- Nichia Corporation

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Cree LED, a business of Smart Global Holdings

- Samsung Electronics Co., Ltd.

- Lite-On Technology Corporation

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corporation

- LG Innotek Co., Ltd.

- Nationstar Optoelectronics Co., Ltd.

- Bridgelux, Inc.

- Dominant Opto Technologies Sdn. Bhd.

- Epistar Corporation

- Sanan Optoelectronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Citizen Electronics Co., Ltd.

- Stanley Electric Co., Ltd.

- Osram Opto Semiconductors GmbH

- Refond Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Energy-Efficient Lighting in Commercial Retrofits

- 4.2.2 Increasing LED Penetration in Automotive Exterior Lighting

- 4.2.3 Growing Use of Horticultural Lighting by U.S. Vertical Farms

- 4.2.4 Federal Incentives for Domestic Semiconductor Packaging Under CHIPS Act

- 4.2.5 MiniLED Backlight Proliferation in High-End TVs and Monitors

- 4.2.6 Emergence of Tunable White Standards in WELL and LEED Buildings

- 4.3 Market Restraints

- 4.3.1 Price Erosion Owing to Intense Asian Competition

- 4.3.2 Thermal Management Challenges in Compact Luminaire Designs

- 4.3.3 Supply-Chain Risk From Indium and Gallium Price Volatility

- 4.3.4 Slow Standardization of CSP Reliability Testing Protocols

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2 W - 0.5 W

- 5.1.2 0.5 W - Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050 etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Nichia Corporation

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Cree LED, a business of Smart Global Holdings

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Lite-On Technology Corporation

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Lextar Electronics Corporation

- 6.4.10 LG Innotek Co., Ltd.

- 6.4.11 Nationstar Optoelectronics Co., Ltd.

- 6.4.12 Bridgelux, Inc.

- 6.4.13 Dominant Opto Technologies Sdn. Bhd.

- 6.4.14 Epistar Corporation

- 6.4.15 Sanan Optoelectronics Co., Ltd.

- 6.4.16 Toyoda Gosei Co., Ltd.

- 6.4.17 Citizen Electronics Co., Ltd.

- 6.4.18 Stanley Electric Co., Ltd.

- 6.4.19 Osram Opto Semiconductors GmbH

- 6.4.20 Refond Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)