|

市場調查報告書

商品編碼

2063977

亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

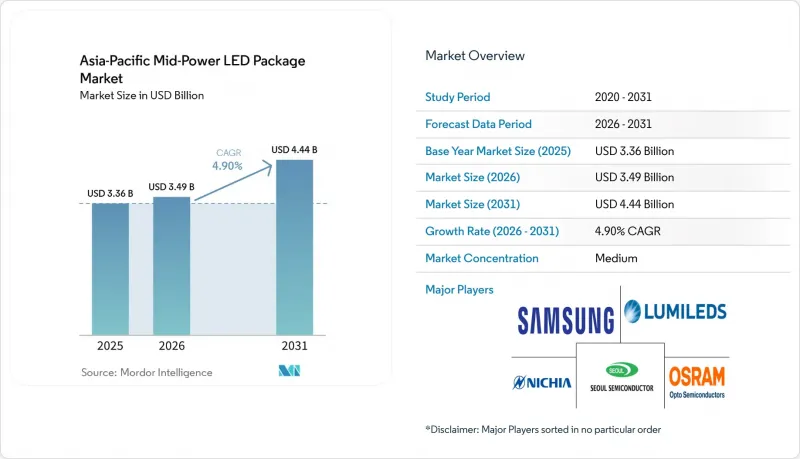

根據 Mordor Intelligence 預測,亞太地區中功率LED構裝市場規模將從 2025 年的 33.6 億美元成長到 2026 年的 34.9 億美元,到 2031 年將達到 44.4 億美元,2026 年至 2031 年的複合年成長率為 4.9%。

本報告按輸出功率範圍(0.2–0.5 W 和小於 0.5–1 W)、封裝結構(SMD,包括 2835、3014、3030 等,以及 CSP)、應用領域(通用照明、汽車照明、顯示和背光、特殊及利基應用)以及國家/地區(中國、日本、印度、東南亞及其他亞太地區)進行細分。市場預測以美元 (USD) 為單位。

亞太地區中功率LED構裝市場趨勢及洞察。

智慧照明領域對 2835 中中功率LED 的需求正在激增。

目前,建築業主正在指定使用2835封裝,該封裝整合了熱敏電阻器和深度調光控制功能,可消除可見閃爍並符合健康標準。其2.8mm x 3.5mm的尺寸允許在軟性燈條上每米最多整合240顆LED,且不會超出熱限制,從而為零售店的內凹照明和醫療機構的病房提供均勻的亮度。預測性維護演算法利用即時溫度數據,可將設施營運成本降低高達20%。在加州Title 24、新加坡綠色建築標誌和日本WELL認證等強制要求使用低閃爍照明設備的地區,該封裝的普及速度正在加快。因此,在亞太地區的中功率LED構裝市場,2835封裝已不再只是一種低成本的商品,而是智慧節點平台。

汽車OEM廠商向自我調整像素頭燈的過渡。

隨著監管機構建議使用無眩光遠光燈,汽車製造商正擴大採用25,000像素的模組,以實現動態光束整形和道路投射。只有像素間距小於80µm且能夠在5mm x 5mm封裝內散熱60瓦的供應商才能滿足要求,這縮小了供應商的選擇範圍。與傳統矩陣燈相比,節能15-20%意味著更長的續航里程,這一點尤其能引起中國和日本電動車買家的共鳴。隨著頭燈的功能從單純的照明設備發展成為通訊設備,亞太地區中中功率LED構裝市場的汽車市場佔有率正在不斷擴大。

主導專利擁有者面臨的智慧財產權訴訟風險

專利組合成為重要的競爭防禦手段。近期美國和德國法院的訴訟凸顯了中小供應商面臨的困境:要麼接受性能妥協以避免侵權,要麼冒著被法院下達禁令、導致三年汽車認證週期中斷的風險。這種擔憂迫使原始設備製造商(OEM)優先選擇那些提供以專利費池為支撐的補償方案的供應商,從而導致亞太地區中中功率LED構裝市場佔有率的集中化。

細分市場分析

在亞太地區中中功率LED構裝市場,0.5W和低於1W的高功率封裝佔據主導地位,廣泛應用於汽車頭燈和園藝照明。像素光束需要0.7-0.9W的晶片才能在-40 度C至125 度C的溫度循環下維持300米的照明距離,而垂直農業則能以更少的照明器實現超過1000µmol m⁻²s⁻¹的光子通量。嚴格的分級和AEC-Q級可靠性將毛利率控制在30%左右。 0.2-0.5W的低功率裝置仍用於燈條和mini-LED面板,但價格競爭使得其利潤率低於12%,迫使供應商轉向高功率的產品。因此,儘管銷售量下降,高功率產品在亞太地區中中功率LED構裝市場的佔有率仍在上升。

通用照明領域依靠效率的逐步提升和成本的大幅降低來保持競爭力。零售店的內凹照明採用0.3W的2835晶片,LED密度為每公尺120-160顆,採購標準為「每美元流明數」。顯示器背光燈的功率範圍與之類似,但面板製造商的垂直整合如今主導了供應商的選擇,導致亞太地區中中功率LED構裝市場中獨立供應商的議價能力下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 宏觀經濟因素的影響

- 監理情勢

- 技術分析

- 市場促進因素

- 智慧照明領域對 2835 型中中功率LED 的需求正在激增。

- 汽車製造商向自我調整像素式大燈的過渡

- 電視面板中Mini-LED背光技術的應用正在加速推進。

- 東南亞強制性節能措施

- 受控環境農場中園藝照明的快速發展

- 新型微封裝技術降低了每流明成本

- 市場限制因素

- 主導專利擁有者面臨的智慧財產權訴訟風險

- 主要磷光體材料供應鏈中斷

- 亞洲高濕度氣候條件下亮度劣化

- 顯示器背光供應商之間的整合正在拉低平均售價(ASP)。

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 0.2~0.5 W

- 0.5 至小於 1 瓦

- 所以

- SMD(表面黏著型元件)

- 2835

- 3014

- 3030

- 其他(3528、3020、5050 等)

- CSP(晶片級封裝)

- SMD(表面黏著型元件)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 專業/小眾

- 按地區

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.(Samsung LED)

- Lumileds Holding BV

- ams-OSRAM AG

- Seoul Semiconductor Co., Ltd.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED, an SGH company

- NationStar Optoelectronics Co., Ltd.

- Lite-On Technology Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Toyoda Gosei Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Lextar Electronics Corporation

- Hongli Zhihui Group Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- MLS Co., Ltd.(Forest Lighting)

- Hubei NationStar Semiconductor

- Shenzhen Jufei Optoelectronics Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific mid-power LED package market size is expected to grow from USD 3.36 billion in 2025 to USD 3.49 billion in 2026 and is forecast to reach USD 4.44 billion by 2031 at a 4.9% CAGR over 2026-2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Country (China, Japan, India, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Mid-Power LED Package Market Trends and Insights

Surging Demand for 2835 Mid-Power LEDs in Smart Lighting

Building owners now specify 2835 packages that integrate thermistors and deep-dimming control, eliminating visible flicker and aligning with wellness codes. The 2.8 mm X 3.5 mm footprint allows up to 240 LEDs per meter on flexible strips without breaching thermal limits, creating uniform luminance in retail coves and healthcare wards. Predictive maintenance algorithms tap real-time temperature data to reduce facility operating costs by up to 20%. Adoption accelerates where California Title 24, Singapore's Green Mark, and Japan's WELL certification require low-flicker luminaires. As a result, the Asia-Pacific mid-power LED package market increasingly treats the 2835 as a smart-node platform rather than a low-cost commodity.

Automotive OEM Shift Toward Adaptive Pixel Headlamps

Regulators endorse glare-free high beams, prompting carmakers to embrace 25,000-pixel modules that deliver dynamic beam shaping and road-surface projections. Only suppliers with sub-80 µm pixel pitch and the ability to dissipate 60 watts in a 5 mm X 5 mm envelope qualify, narrowing the vendor pool. Energy savings of 15-20% compared with older matrix lamps translate into extra driving range, an argument that resonates with electric-vehicle buyers across China and Japan. The Asia-Pacific mid-power LED package market thus sees automotive share rising as headlamps evolve from illumination to communication devices.

IP Litigation Risk from Dominant Patent Holders

Patent portfolios have become the chief competitive moat. Recent lawsuits in U.S. and German courts underscore that smaller vendors face a binary choice: accept performance trade-offs to avoid infringement, or risk injunctions that stall automotive qualification cycles lasting 3 years. The overhang forces OEMs to favor suppliers offering indemnification backed by royalty pools, thereby concentrating share within the Asia-Pacific mid-power LED package market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Mini-LED Backlighting Adoption in TV Panels

- Energy-Efficiency Mandates Across Southeast Asia

- Supply Chain Disruptions for Key Phosphor Materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Higher-wattage 0.5W- and Less Than 1W packages dominate the Asia-Pacific mid-power LED package market for vehicle headlamps and horticultural rigs. Pixel beams need 0.7-0.9 W chips to sustain 300-meter reach under -40 °C to 125 °C cycles, while vertical farms drive greater than 1,000 µmol m-2 s-1 photon flux with fewer fixtures. Gross margins hover near 30% thanks to stringent binning and AEC-Q-grade reliability. Lower 0.2-0.5 W devices still feed strip lights and mini-LED panels, yet price wars compress margins below 12%, nudging vendors toward premium wattages. The Asia-Pacific mid-power LED package market share in the high-power range thus rises despite smaller unit volumes.

Commodity segments lean on incremental efficacy gains and aggressive cost downs to stay relevant. Retail cove lights pack 0.3 W 2835s at densities of 120-160 LEDs per meter, where lumen per dollar rules procurement. Display backlights adopt similar power envelopes, but panel-maker vertical integration now dictates vendor selection, leaving independents with reduced bargaining power inside the Asia-Pacific mid-power LED package market.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd. (Samsung LED)

- Lumileds Holding B.V.

- ams-OSRAM AG

- Seoul Semiconductor Co., Ltd.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Cree LED, an SGH company

- NationStar Optoelectronics Co., Ltd.

- Lite-On Technology Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Toyoda Gosei Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Lextar Electronics Corporation

- Hongli Zhihui Group Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Hubei NationStar Semiconductor

- Shenzhen Jufei Optoelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Regulatory Landscape

- 4.4 Technology Analysis

- 4.5 Market Drivers

- 4.5.1 Surging Demand for 2835 Mid-Power LEDs in Smart Lighting

- 4.5.2 Automotive OEM Shift Toward Adaptive Pixel Headlamps

- 4.5.3 Accelerated Mini-LED Backlighting Adoption in TV Panels

- 4.5.4 Energy-Efficiency Mandates Across Southeast Asia

- 4.5.5 Rapid Expansion of Horticultural Lighting in Controlled-Environment Farms

- 4.5.6 Emerging Micro-Packaging Techniques Reducing Cost per Lumen

- 4.6 Market Restraints

- 4.6.1 IP Litigation Risk From Dominant Patent Holders

- 4.6.2 Supply Chain Disruptions for Key Phosphor Materials

- 4.6.3 Luminance Degradation Under High-Humidity Asian Climates

- 4.6.4 Consolidation of Display Backlight Vendors Dampening ASPs

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Southeast Asia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Samsung LED)

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 ams-OSRAM AG

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Everlight Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Cree LED, an SGH company

- 6.4.9 NationStar Optoelectronics Co., Ltd.

- 6.4.10 Lite-On Technology Corporation

- 6.4.11 Dominant Opto Technologies Sdn. Bhd.

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 San'an Optoelectronics Co., Ltd.

- 6.4.14 Lextar Electronics Corporation

- 6.4.15 Hongli Zhihui Group Co., Ltd.

- 6.4.16 Refond Optoelectronics Co., Ltd.

- 6.4.17 MLS Co., Ltd. (Forest Lighting)

- 6.4.18 Hubei NationStar Semiconductor

- 6.4.19 Shenzhen Jufei Optoelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)