|

市場調查報告書

商品編碼

2063952

中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

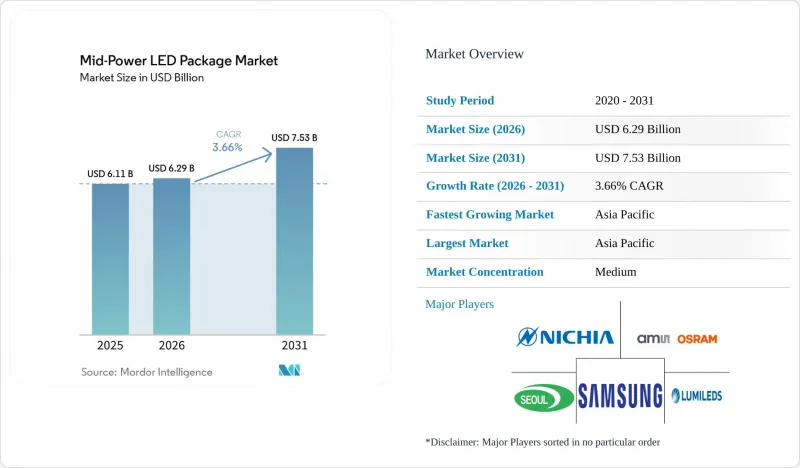

根據 Mordor Intelligence 預測,中功率LED構裝的市場規模預計將從 2025 年的 61.1 億美元和 2026 年的 62.9 億美元成長到 2031 年的 75.3 億美元,2026 年至 2031 年的複合年成長率為 3.6%。

本報告按輸出功率範圍(0.2W至0.5W和0.5W至1W)、封裝結構(SMD,包括2835、3014等,以及其他封裝;CSP)、應用領域(通用照明、汽車照明、顯示器和背光等)以及地區(北美、歐洲、亞太、南美等)進行細分。市場預測以美元(USD)為單位。

全球中功率LED構裝市場趨勢及洞察

市場對節能型通用照明的需求正在激增。

到2025年,LED技術將在中國照明燈具市場佔據相當大的佔有率。此外,加拿大於2026年1月實施的全國性汞基緊湊型螢光禁令,正加速北美地區的類似轉型。美國能源局規定,到2028年7月,通用照明燈具的光通量效率必須達到120流明/瓦,這將進一步縮短鹵素燈的使用壽命。全球約30%的住宅照明仍需更換,另有15%的十年前安裝的第一代LED燈具也將進入更換週期。這為經濟高效的中功率LED燈具創造了數十億台的潛在市場。諸如2835和3030之類的表面黏著技術封裝適用於這些燈具,可與現有的印刷基板生產線無縫整合。政府的補貼計劃和電力公司的獎勵繼續推動採購轉向能源之星認證產品,這反過來又增加了對具有可靠流明保持性能的產品的需求,從而鞏固了中功率產品在批量生產的 A 型燈具和線性應用中的地位。

汽車LED頭燈的快速擴張

聯合國ECE R149標準的實施和FMVSS 108標準的採納,為2025年在主要汽車市場引入自我調整遠光燈鋪平了道路。入門級車型採用24至48個可控像素,而旗艦車型則超過100個像素,對正向電壓和色度檔位的精度提出了更高的要求,從而推動了對高亮度、中功率陣列的需求。電動車製造商優先考慮用於品牌識別和提高效率的標誌性照明,他們採用中功率矩陣系統來顯示迎賓動畫和車道引導線,而不會產生過大的熱負荷。汽車級0度溫度範圍內的認證週期進一步強化了對陶瓷基中中功率晶片和在105 度C左右結溫下封裝可靠性的偏好。像歐司朗這樣的頂級供應商,透過利用已建立的AEC-Q102認證,在檢驗經濟高效的像素密度擴展的原始設備製造商(OEM)提供穩定的供應,同時確保了價格溢價。

日益激烈的競爭給利潤率帶來了壓力。

2026年1月,包括MLS和金光科技在內的中國LED構裝企業將報價上調了5%至10%。這項價格調整是在經歷了數年持續的價格下跌之後進行的,而先前的價格下跌已嚴重影響了許多中型企業的盈利。此次價格上漲的主要原因是金、銀、銅等原物料成本飆升,這些原物料在封裝總成本中佔很大比例。然而,由於標準2835 LED構裝的持續供過於求以及客戶轉換門檻較低,這些價格上漲的永續性仍存在不確定性,限制了企業的定價權。因此,無法透過產品差異化抵銷成本上漲的企業要麼退出市場,要麼尋求併購等整合策略。同時,倖存的企業則專注於汽車照明、園藝照明和MiniLED背光等高附加價值應用領域。這些領域對性能要求更高,因此能夠實現更穩定的價格和更長期的供貨合約。

細分市場分析

到2025年,0.5W至1W頻寬的LED封裝將佔據中功率LED構裝市場62.80%的佔有率,預計複合年成長率(CAGR)為4.12%,這凸顯了其在通用照明維修和新興汽車矩陣陣列領域的持續主導地位。此功率段符合驅動積體電路的限制,能夠將熱負載分散到可控的晶片面積上,並保持了具有吸引力的流明價格,即使在產品同質化的情況下也能保證供應商的利潤率。預計到2026年將有所成長的入門級自適應遠光燈模組主要採用0.5W功率段的裝置,這進一步強化了該功率段在汽車頭燈領域的重要性,因為它可以在不增加結溫的情況下實現超過48個像素的像素數量。相較之下,0.2W至0.5W功率段主要用於指示燈和穿戴式設備,但由於晶片級封裝在較小的面積內提供相同的光通量,其成長速度正受到抑制。

汽車照明對正向電壓和色度分級容差的嚴格要求,使得中端封裝產品需要更精確的電氣分選和更低的色散,而高階產品則需要±0.1V的電壓分級和2-3個色度等級。改良的散熱設計,例如直接銅鍵合和低空隙率的SAC305焊接,使得L70壽命在加速劣化測試中超過50,000小時,滿足OEM廠商的保固要求。隨著MiniLED電視逐漸進入主流價格區間,0.5W元件也開始應用於高階背光系統,在光通量、效率和間距方面實現了良好的平衡。因此,中階產品持續支撐著中功率LED構裝市場的成長,有效抵禦了低功率CSP和高功率COB板載晶片的衝擊。

區域分析

預計到2025年,亞太地區將佔全球銷售額的68.90%,並在2031年之前保持5.10%的複合年成長率,這主要得益於中國大陸、台灣、韓國和日本從晶圓到模組的密集型產業生態系統。 2025年4月,中國實施釔許可限制,導致氧化物價格大幅上漲,迫使封裝製造商在美國和歐洲尋找替代提煉來源。韓國正策略性地拓展其高利潤率的基板和相機模組業務,例如LG Innotek投資6000億韓元(約4.09億美元)的龜尾項目,該項目計劃於2026年竣工。因此,該地區的叢集為支撐大宗商品和高級產品市場奠定了基礎。

儘管北美和歐洲的絕對銷量較小,但加州「Title 24-2025」等嚴格的能源法規以及禁止使用低效燈具的生態設計指令,都促成了每流明更高的毛利率。雖然美國國內外延裝置產能仍有限,且大部分組件供應仍依賴亞洲,但科銳照明於2026年2月簽署的一項契約製造協議表明,國內市場正在逐步整合。透過績效保證型契約資金籌措的市政路燈更換項目,正在推動鈉燈的淘汰,並增加了對智慧互聯照明的需求,這種照明方式適用於內建突波保護的中功率模組。

在南美、中東和非洲,LED的普及率較低,許多地區的普及率仍低於50%。在印度,能源效率服務有限公司(Energy Efficiency Services Limited)採用獨特的大量採購模式。該公司按月收取服務費租賃照明設備,從而提高了價格敏感度,同時向符合輸出功率和使用壽命標準的供應商下達大訂單。在這些新興地區,成熟的2835封裝仍佔據主導地位,中功率LED構裝市場的逐步成長更多是由最初的LED轉換和對電網可靠性的擔憂所驅動,而非技術飛躍。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 節能型通用照明需求激增

- 汽車LED頭燈的快速擴張

- 電視機中MiniLED技術的普及推動了中功率背光市場的發展。

- 透過覆晶和CSP製造降低成本

- 政府逐步淘汰鹵素燈

- 擴大智慧城市路燈項目

- 市場限制因素

- 日益激烈的競爭給利潤率帶來了壓力。

- 高功率密度下溫度控管的局限性

- 主要磷光體材料供應鏈的波動

- 推動板載晶片替代技術應用的法規。

- 工業供應鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 0.2W~0.5W

- 0.5W~1W

- 依封裝架構

- SMD(表面黏著型元件)

- 2835

- 3014

- 3030

- 其他(3528、3020、5050、其他)

- CSP(晶片級封裝)

- SMD(表面黏著型元件)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 專業/小眾

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

- 南美洲

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- OSRAM GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- Cree LED, Inc.

- LG Innotek Co., Ltd.

- Lite-On Technology Corporation

- Everlight Electronics Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Harvatek Corporation

- Toyoda Gosei Co., Ltd.

- Honglitronic Co., Ltd.

- MLS Co., Ltd.(Forest Lighting)

- Refond Optoelectronics Co., Ltd.

- Kingbright Electronic Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the mid-power LED package market size is projected to expand from USD 6.11 billion in 2025 and USD 6.29 billion in 2026 to USD 7.53 billion by 2031, registering a CAGR of 3.66% between 2026- 2031.

This report is Segmented by Power Range (0. 2W-0. 5W and 0. 5W- Less Than 1W), Package Architecture (SMD Including 2835, 3014, and More, and Others; CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Mid-Power LED Package Market Trends and Insights

Surging Demand for Energy-Efficient General Lighting

LED technology supplied a significant share of China's lamp stock in 2025, and Canada's nationwide ban on mercury-based compact fluorescent lamps, which began in January 2026, is accelerating a similar transition across North America. The U.S. Department of Energy standard requiring 120 lumens-per-watt efficacy for general service lamps by July 2028 further compresses the viable window for halogen products. Roughly 30% of the global residential base still needs to convert, and another 15% of first-generation LEDs installed a decade ago will enter the replacement cycle, supplying a multibillion-unit addressable pool for cost-efficient mid-power packages. These lamps favor 2835 and 3030 surface-mount configurations that integrate seamlessly with legacy printed-circuit manufacturing lines. Government rebate programs and electric-utility incentives continue to steer procurement toward ENERGY STAR-qualified devices, reinforcing demand for packages with proven lumen-maintenance credentials and solidifying mid-power incumbency in volume A-lamp and linear applications.

Rapid Expansion of Automotive LED Headlamps

UN ECE R149 enforcement and FMVSS 108 adoption unlocked legal pathways for adaptive driving-beam headlamps across major automotive regions in 2025. Entry variants integrate 24-48 controllable pixels, whereas flagship trims exceed 100 pixels, dictating tighter forward-voltage and chromaticity bins and driving volumes for high-luminance mid-power arrays. Electric vehicle makers prioritize signature lighting for brand identity and efficiency, using mid-power matrix systems to display welcome animations and lane guides without excessive thermal load. Qualification cycles in automotive-grade 0 temperature ranges validate package reliability at junction temperatures near 105 °C, reinforcing the preference for ceramic-based mid-power dies. Tier-one suppliers such as ams OSRAM leverage established AEC-Q102 credentials to command price premiums while maintaining supply security for original equipment manufacturers looking to scale pixel densities cost-effectively.

Intensifying Price Competition Squeezing Margins

In January 2026, Chinese LED packaging companies, including MLS and Kinglight, increased quoted prices by 5-10%. This adjustment followed several years of sustained price declines that significantly compressed profitability for many mid-sized firms. The price increase is primarily due to rising input costs for gold, silver, and copper, which account for a substantial portion of overall packaging expenses. However, the sustainability of these price increases remains uncertain due to persistent oversupply in standard 2835 LED packages and the low switching barriers for customers, which limit pricing power. As a result, companies that are unable to balance rising costs through product differentiation are either exiting the market or pursuing consolidation strategies such as mergers and acquisitions. At the same time, surviving players are shifting their focus toward higher-value applications, including automotive lighting, horticulture, and MiniLED backlighting. These segments impose stricter performance requirements, enabling more stable pricing and longer-term supply agreements.

Other drivers and restraints analyzed in the detailed report include:

- MiniLED Adoption in TVs Boosting Mid-Power Backlights

- Cost Declines from Flip-Chip and CSP Manufacturing

- Thermal Management Limits for Higher Watt Density

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W- less than 1 W band accounted for 62.80% of mid-power LED package market share in 2025, and its 4.12% forecast CAGR underlines sustained leadership in general lighting retrofits and emerging automotive matrix arrays. This power class aligns with driver-integrated circuit constraints, spreads thermal load across a manageable die area, and maintains compelling cost-per-lumen ratios that preserve vendor margin despite commodity pricing. Entry-level adaptive driving-beam modules, now projected to increase in 2026, predominantly specify 0.5 W-range devices that achieve pixel counts above 48 without exacerbating junction temperature, reinforcing the segment's relevance in vehicle headlamps. In contrast, the 0.2 W-0.5 W segment serves indicators and wearables but faces substitution by smaller chip-scale packages offering similar flux within reduced footprints, restricting its growth pace.

Automotive lighting's stringent forward-voltage and chromaticity binning tolerances are pushing mid-range packages toward finer electrical screening and narrower hue dispersion, with premium models demanding bins of +-0.1 V and two-to-three MacAdam steps. Thermal upgrades such as direct copper bonding and low-void SAC305 soldering uphold L70 life beyond 50 000 h under accelerated-aging protocols, meeting original equipment manufacturer warranty terms. As MiniLED televisions penetrate mainstream price tiers, 0.5 W devices are also appearing in high-end backlights, balancing flux, efficiency, and pitch. The mid-range thus continues to anchor the mid-power LED package market size expansion while holding off encroachment from both lower-power CSPs and higher-power chip-on-board alternatives.

Geography Analysis

The Asia-Pacific accounted for 68.90% of sales in 2025 and is sustaining a 5.10% CAGR through 2031, buoyed by dense wafer-to-module ecosystems in China, Taiwan, South Korea, and Japan. China's April 2025 export-licensing rule on yttrium triggered a significant spike in oxide prices, compelling packagers to explore alternative refining sources in the United States and Europe. South Korea is strategically expanding higher-margin substrate and camera-module lines, evidenced by LG Innotek's 600 billion KRW (USD 409 million) Gumi project slated for completion in 2026. The regional cluster thus anchors both commodity and premium segments.

North America and Europe contribute lower absolute volumes yet deliver higher gross margins per lumen thanks to stringent energy codes, such as California Title 24-2025, and eco-design directives that disallow low-efficiency lamps. Domestic epitaxial capacity is thin, so most component supply remains Asia-sourced, although Cree Lighting's contract manufacturing deal in February 2026 signals incremental onshore integration. Municipal streetlight retrofits financed through performance-based contracts continue to replace sodium lamps, adding connected-lighting provisions that favor mid-power modules with integrated surge protection.

South America, the Middle East, and Africa trail in penetration, with LED adoption under 50% in many jurisdictions. India operates a unique bulk-procurement model through Energy Efficiency Services Limited, which leases fixtures under monthly service fees, driving price sensitivity while awarding large volumes to suppliers that meet output and lifetime standards. In these emerging territories, proven 2835 packages retain dominance, and the mid-power LED package market derives incremental growth less from technological leapfrogging and more from first-time conversions and grid-reliability considerations.

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- OSRAM GmbH

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Cree LED, Inc.

- LG Innotek Co., Ltd.

- Lite-On Technology Corporation

- Everlight Electronics Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Harvatek Corporation

- Toyoda Gosei Co., Ltd.

- Honglitronic Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Refond Optoelectronics Co., Ltd.

- Kingbright Electronic Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Energy-Efficient General Lighting

- 4.2.2 Rapid Expansion of Automotive LED Headlamps

- 4.2.3 MiniLED Adoption in TVs Boosting Mid-Power Backlights

- 4.2.4 Cost Declines From Flip-Chip and CSP Manufacturing

- 4.2.5 Government Phasing-Out of Halogen Lamps

- 4.2.6 Growing Smart-City Streetlighting Projects

- 4.3 Market Restraints

- 4.3.1 Intensifying Price Competition Squeezing Margins

- 4.3.2 Thermal Management Limits for Higher Watt Density

- 4.3.3 Supply Chain Volatility of Key Phosphor Materials

- 4.3.4 Regulatory Push Toward Chip-on-Board Alternatives

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2W - 0.5W

- 5.1.2 0.5W - Less Than 1W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Southeast Asia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 OSRAM GmbH

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Cree LED, Inc.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Lite-On Technology Corporation

- 6.4.9 Everlight Electronics Co., Ltd.

- 6.4.10 NationStar Optoelectronics Co., Ltd.

- 6.4.11 Dominant Opto Technologies Sdn. Bhd.

- 6.4.12 Harvatek Corporation

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 Honglitronic Co., Ltd.

- 6.4.15 MLS Co., Ltd. (Forest Lighting)

- 6.4.16 Refond Optoelectronics Co., Ltd.

- 6.4.17 Kingbright Electronic Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)