|

市場調查報告書

商品編碼

2063981

印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)India Mid-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

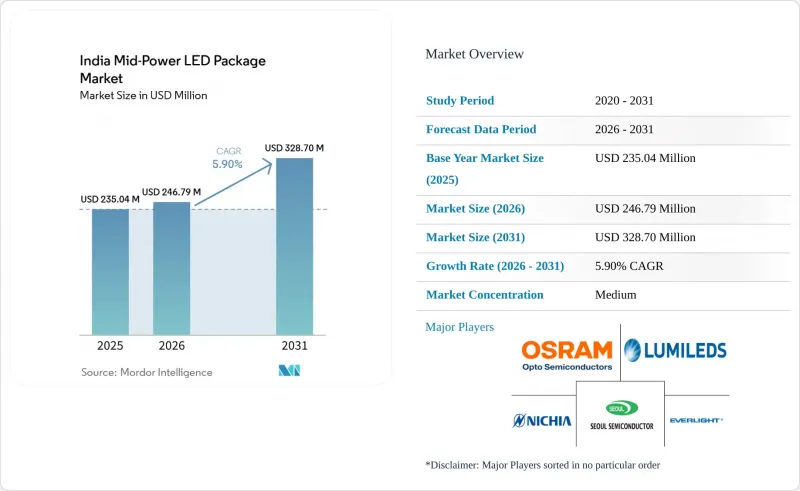

根據 Mordor Intelligence 預測,印度中中功率LED構裝市場規模將從 2025 年的 2.3504 億美元成長到 2026 年的 2.4679 億美元,到 2031 年將達到 3.287 億美元,2026 年至 2031 年的複合年成長率為 5.9%。

本報告按輸出功率範圍(0.2–0.5W 和 0.5–1W)、封裝結構(SMD 和 CSP,包括 2835、3014、3030 等)以及應用領域(通用照明、汽車照明、顯示器和背光以及特殊/小眾應用)進行細分。市場預測以美元 (USD) 為單位。

印度中功率LED構裝市場趨勢與洞察

路燈競標中LED主流化

地方政府已將最低能源效率和顯色標準納入2025年後發布的90%以上的路燈競標中。這有效地淘汰了高壓鈉燈具,並推動採購轉向0.5瓦至1瓦的中功率燈具,這些燈具每瓦可提供120至140流明的光通量。能源效率服務有限公司(EESL)正透過中央政府的聯合資助加速燈具更換週期。此舉確保了未來多年的訂單前景。符合印度標準局(BIS)標準且突波保護等級高於4千伏特的供應商持續贏得最大訂單。這一趨勢導致本地封裝線的作業量增加。

印度標準局提高發光效率標準

印度標準局 (BIS) 制定的 IS 10322、2025 標準,將最常用功率等級的 LED 發光效率下限從每瓦 100 流明提高到 110-120 流明。擁有內部發光強度測量實驗室的大型製造商已迅速推出改進的產品線。同時,小規模的組裝製造商則面臨長達六個月的認證延遲。這項強制性變更導致一些滯銷產品被淘汰,進而引發印度中中功率LED構裝市場庫存補貨激增。

磷光體供應價格波動

2026年4月,中國對釔化合物實施出口限制,導致歐洲氧化釔現貨價格在六週內從每公斤8美元飆升至126美元,使依賴進口紅色和黃色磷光體的印度包裝製造商的營業利潤率下降了多達200個基點。儘管期貨合約和部分使用钆基混合物進行替代緩解了這一影響,但持續存在的地緣政治風險仍使市場擴張放緩了1.3個百分點。

細分市場分析

2025年,功率在0.5W至1W以下的LED頻寬將佔據印度中中功率LED構裝市場63.33%的佔有率。政府路燈專案和汽車自我調整頭燈均指定使用此功率範圍的LED,以平衡發光效率和散熱裕度,這推動了市場需求。 Lumax Industries的LED相關累積訂單高達17.59億印度盧比(約2.11億美元)。由於印度大部分地區的戶外溫度超過攝氏40度C,結溫上行風險很高,因此0.5W至1W晶片的低電流密度對於實現5萬小時的光通量維持目標至關重要。

該領域的成長也得益於透過生產連結獎勵計畫(PLI) 實現磷光體塗層和焊線線的本地化,這使得元件成本比進口降低了近 8%,並預計到 2031 年將保持 6.78% 的複合年成長率。預計在預測期內,隨著地方政府競標總合的增加(涵蓋超過 300 萬個照明燈具),印度中中功率LED構裝市場規模也將同步成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 路燈競標中LED主流化

- 印度標準局加強發光效率標準

- 印度專業電子代工快速擴張

- 國內智慧型手機組裝轉向中功率LED。

- 政府LED組件產品授權庫存(PLI)

- 小規模零售商正在進行智慧照明維修

- 市場限制因素

- 磷光體供應價格波動

- 從中國進口COB的成本較低。

- 高溫環境下的溫度控管面臨的挑戰

- LED原料的消費稅稅率仍存在不確定性。

- 產業價值鏈分析

- 技術展望

- 監理情勢

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 0.2~0.5 W

- 0.5 至小於 1 瓦

- 所以

- SMD(表面黏著型元件)

- 2835

- 3014

- 3030

- 其他(3528、3020、5050 等)

- CSP(晶片級封裝)

- SMD(表面黏著型元件)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 專業/小眾

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Seoul Semiconductor Co. Ltd.

- Lumileds Holding BV

- Osram Opto Semiconductors GmbH

- Everlight Electronics Co. Ltd.

- CreeLED Inc.

- Samsung Electronics Co. Ltd.

- MLS Co. Ltd.(Forest Lighting)

- Dominant Opto Technologies Sdn Bhd

- Lextar Electronics Corp.

- Edison Opto Corp.

- Havells India Ltd.

- Dixon Technologies(India)Ltd.

- HPL Electric and Power Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the india mid-power LED package market size is expected to increase from USD 235.04 million in 2025 to USD 246.79 million in 2026 and reach USD 328.70 million by 2031, growing at a CAGR of 5.9% over 2026-2031.

This report is Segmented by Power Range (0. 2-0. 5 W and 0. 5- Less Than 1 W), Package Architecture (SMD Including 2835, 3014, 3030, Others, and CSP), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche). The Market Forecasts are Provided in Terms of Value (USD).

India Mid-Power LED Package Market Trends and Insights

Mainstream LED Adoption in Street-Lighting Tenders

Municipal corporations embedded minimum efficacy and color-rendering thresholds into more than 90% of street-lighting tenders issued since 2025, effectively disqualifying high-pressure sodium fixtures and pushing procurement toward 0.5 W-to-1 W mid-power packages that deliver 120-140 lumens per watt. Energy Efficiency Services Limited (EESL) is accelerating replacement cycles through central co-financing. This move guarantees multi-year order visibility. Vendors that showcase BIS compliance and boast surge-protection ratings exceeding 4 kilovolts are consistently landing the largest lots. This trend is prompting local encapsulation lines to expand their operations.

Rising Luminous-Efficacy Mandates By BIS

The BIS suite, IS 10322:2026, IS 16102:2026, and IS 16103:2025, has raised efficacy floors from 100 lumens per watt to 110-120 lumens for the most prevalent wattage classes. Major players, equipped with in-house photometric labs, have swiftly rolled out upgraded product lines. In contrast, smaller assemblers grapple with certification delays that can stretch up to 6 months. This mandatory shift renders slower-moving SKUs obsolete, prompting a surge in restocking in India's mid-power LED package market.

Volatility In Phosphor Supply Prices

China's April 2026 export controls on yttrium compounds drove European yttrium-oxide spot prices from USD 8 per kg to USD 126 per kg within six weeks, compressing operating margins by up to 200 basis points for Indian package makers reliant on imported red and yellow phosphors. Although forward contracts and partial substitution with gadolinium-based blends temper the shock, persistent geopolitical risk subtracts 1.3 percentage points from market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Indian Contract Electronics Manufacturing

- Indigenous Smartphone Assembly Shifting to Mid-Power LEDs

- Low Switching-Cost Toward COB Imports from China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 0.5 W-to-Less Than 1 W band captured 63.33% of India's mid-power LED package market share in 2025. Government street-lighting programs and automotive adaptive headlamps specify this wattage to balance efficacy with thermal headroom, and demand is reinforced by Lumax Industries' INR 1,759 crore (USD 211 million) LED-heavy order book. Outdoor ambient temperatures exceeding 40 °C in much of India elevate junction-temperature risk, making the lower current density of 0.5 W to 1 W dice indispensable for 50,000-hour lumen maintenance targets.

Segment growth also benefits from PLI-funded localization of phosphor coating and wire-bonding lines, which trim bill-of-materials costs by nearly 8% versus imported equivalents, sustaining a 6.78% CAGR through 2031. The Indian mid-power LED package market size for this power range is projected to move in lockstep with the ramp-up of municipal tenders that collectively cover more than 3 million luminaire points over the forecast horizon.

List of Companies Covered in this Report:

- Nichia Corporation

- Seoul Semiconductor Co. Ltd.

- Lumileds Holding B.V.

- Osram Opto Semiconductors GmbH

- Everlight Electronics Co. Ltd.

- CreeLED Inc.

- Samsung Electronics Co. Ltd.

- MLS Co. Ltd. (Forest Lighting)

- Dominant Opto Technologies Sdn Bhd

- Lextar Electronics Corp.

- Edison Opto Corp.

- Havells India Ltd.

- Dixon Technologies (India) Ltd.

- HPL Electric and Power Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream LED Adoption in Street-Lighting Tenders

- 4.2.2 Rising Luminous-Efficacy Mandates by BIS

- 4.2.3 Rapid Expansion of Indian Contract Electronics Manufacturing

- 4.2.4 Indigenous Smartphone Assembly Shifting to Mid-Power LEDs

- 4.2.5 Government's PLI Scheme for LED Components

- 4.2.6 Micro-Retailers Embracing Smart-Lighting Retrofits

- 4.3 Market Restraints

- 4.3.1 Volatility in Phosphor Supply Prices

- 4.3.2 Low Switching-Cost Toward COB Imports from China

- 4.3.3 Thermal-Management Issues in High-Ambient Zones

- 4.3.4 Persistent GST-Rate Uncertainty on LED Inputs

- 4.4 Industry Value-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 0.2-0.5 W

- 5.1.2 0.5- Less Than 1 W

- 5.2 By Package Architecture

- 5.2.1 SMD (Surface Mount Device)

- 5.2.1.1 2835

- 5.2.1.2 3014

- 5.2.1.3 3030

- 5.2.1.4 Others (3528, 3020, 5050, etc.)

- 5.2.2 CSP (Chip Scale Package)

- 5.2.1 SMD (Surface Mount Device)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Seoul Semiconductor Co. Ltd.

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Osram Opto Semiconductors GmbH

- 6.4.5 Everlight Electronics Co. Ltd.

- 6.4.6 CreeLED Inc.

- 6.4.7 Samsung Electronics Co. Ltd.

- 6.4.8 MLS Co. Ltd. (Forest Lighting)

- 6.4.9 Dominant Opto Technologies Sdn Bhd

- 6.4.10 Lextar Electronics Corp.

- 6.4.11 Edison Opto Corp.

- 6.4.12 Havells India Ltd.

- 6.4.13 Dixon Technologies (India) Ltd.

- 6.4.14 HPL Electric and Power Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)