|

市場調查報告書

商品編碼

2064020

亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)Asia-Pacific White LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

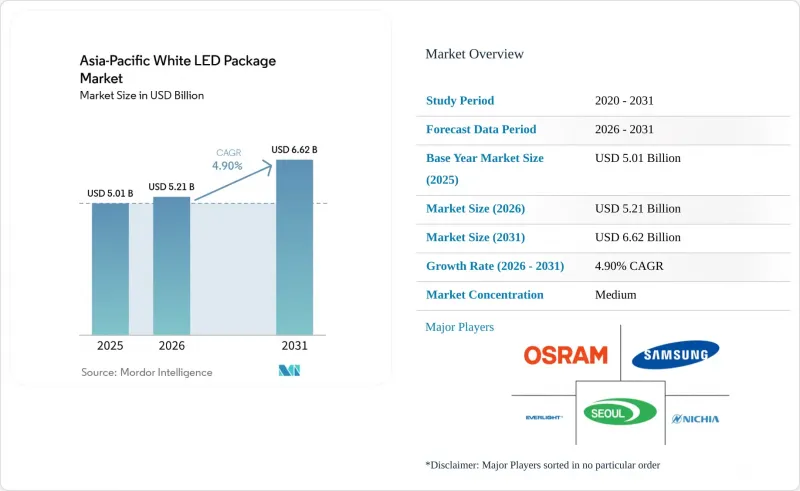

根據 Mordor Intelligence 預測,亞太地區白光LED構裝市場規模將從 2025 年的 50.1 億美元成長到 2026 年的 52.1 億美元,然後在 2031 年達到 66.2 億美元,2026 年至 2031 年的複合年成長率為 4.9%。

本報告按封裝架構(SMD、COB、CSP、覆晶LED構裝)、功率等級(低功率、中功率、高功率)、應用領域(通用照明、汽車照明、顯示器背光、特殊應用)以及國家(中國、日本、印度、東南亞及其他亞太地區)進行細分。市場預測以美元(USD)為單位。

亞太地區白光LED構裝市場趨勢與洞察。

智慧電視對迷你和微型LED背光燈的需求激增

高階電視品牌將在2026年1月的國際消費電子展(CES)上推出RGB mini-LED電視,其性能將超過43,000個分區,峰值亮度超過4,000尼特。取消量子點薄膜將穩定晶片良率,可望降低15%的組件成本,從而可以將節省下來的成本用於更高附加價值的晶片級封裝(CSP)。廣東和江蘇兩省的面板組裝廠商正在採用精度低於5µm的貼片設備,以適應較小的間距,並優先選擇在模組工廠50公里範圍內擁有後端組裝設施的LED供應商。隨著小於100µm的晶片進入量產階段,亞太地區的白光LED構裝市場將從通用SMD轉向散熱能力達3W/mm²的高功率晶圓級CSP。這一趨勢正在推動更高的亮度需求,並帶動上游對先進磷光體混合物的需求,這些混合物即使在高電流密度下也能保持色坐標的穩定性。

東南亞地區積極主動的SSL獎勵計劃

泰國已將LED維修的雙倍企業所得稅抵免政策延長至2028年,印尼維持其30%的全國節能目標,越南則正在亞洲開發銀行(亞洲開發銀行)的支持下規劃節能框架。這些獎勵將照明投資的回收期縮短至18個月以內,並推動公共部門採購優先考慮發光效率而非顯色性和使用壽命。隨著市政負責人將100 lm/W的標準標準化,中功率SMD供應商正面臨加速商業化的情況。因此,在亞太地區的白光LED構裝市場,價值集中度正轉向高階汽車和顯示器等細分市場,而入門級產品的出貨量則激增。政策推動力在商業高棚燈和道路照明領域最為強勁,確保了未來幾年泰國和越南出口加工區生產的2835和3030尺寸產品的市場需求。

圍繞覆晶架構的持續智慧財產權訴訟

2026年2月,億光電子(Everlight Electronics)對Lumileds和首爾半導體(Seoul Semiconductor)提起專利侵權訴訟,指控其侵犯了與直接接合覆晶技術相關的美國專利號7,554,126。禁令風險和不斷上漲的訴訟成本導致二線組裝放緩了對覆晶設備的投資,使得產能集中在大型垂直整合企業手中。目前,原始設備製造商(OEM)正在協商補償條款,這些條款會使合約價格增加3-5%,即使在散熱優勢顯而易見的情況下,也減緩了覆晶技術的普及速度。因此,短期內,亞太地區白光LED構裝市場對高功率CSP(連續表面封裝)的採用速度有所放緩,而現有供應商則利用這場糾紛為其認證封裝產品收取高價。

細分市場分析

2025年,表面黏著型元件(SMD)封裝佔據亞太地區白光LED構裝市場58.48%的比重。這反映了改裝燈泡和螢光管的廣泛應用。晶圓級CSP封裝正以5.49%的複合年成長率成長,預計到2031年,將在汽車頭燈和高階顯示器訂單佔據相當大的佔有率。隨著OEM廠商對更小尺寸、更高驅動電流和更低熱阻的需求不斷成長,亞太地區基於CSP技術的白光LED構裝市場規模預計將穩定成長。然而,SMD生產線的利潤率仍然很低,比現有品牌低40%,深圳和東莞的契約製造提供的組裝價格低至每片0.02美元。

由於對高棚燈和體育場館照明設備的高流明輸出需求,它們仍然偏好板載晶片(COB)陣列。同時,儘管訴訟不斷,覆晶封裝在高階汽車日間行車燈(DRL)市場仍然佔據主導地位。預計在預測期內,CSP(晶片封裝)的月產量將超過1000萬顆,這將使CSP生產線獲得經濟優勢,迫使現有的SMD(表面貼裝元件)製造商要么轉向小眾維修市場,要么升級其技術。隨著電視面板製造商縮短產品週期並要求現場組裝以實現準時制庫存目標,精通扇出型封裝技術的供應商將獲得優勢。因此,亞太地區的白光LED構裝市場正在增加對晶圓級製程的投資,因為這些製程在成本和性能方面都具有優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧電視對Mini-LED和Micro-LED背光的需求正在激增。

- 東南亞地區積極主動的SSL獎勵計劃

- 電動車充電站照明網路快速發展

- 透過採用晶圓級CSP降低成本。

- 日本推廣無紫外線、健康照明

- 印度和中國強制推行能源效率標籤制度

- 市場限制因素

- 圍繞覆晶架構的永無止境的智慧財產權訴訟

- 功率輸出等級為 3 瓦或以上的產品在溫度控管面臨挑戰。

- 高顯色磷光體供應短缺

- 由於藍寶石基板價格飆升,Mini-LED晶片晶圓成本不斷上漲。

- 產業供應鏈分析

- 技術展望

- 監理情勢

- 宏觀經濟因素的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 依封裝架構

- SMD(表面黏著型元件)

- COB(板載晶片)

- CSP(晶片級封裝)

- 覆晶LED構裝

- 按輸出類別

- 低功率(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(超過 1 瓦)

- 透過使用

- 一般照明

- 汽車照明

- 顯示背光

- 特殊用途/利基市場

- 國家

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Samsung Electronics Co. Ltd.(Samsung LED)

- Seoul Semiconductor Co. Ltd.

- Everlight Electronics Co. Ltd.

- Lumileds Holding BV

- Hongli Zhihui Group Co. Ltd.

- LG Innotek Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- CreeLED, Inc.

- Refond Optoelectronics Co. Ltd.

- Osram GmbH(ams-Osram)

- Edison Opto Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Lextar Electronics Corporation

- Toyoda Gosei Co. Ltd.

- Sharp Corporation

- Rohm Semiconductor

- MLS Co. Ltd.(Forest Lighting)

- Shenzhen Jufei Optoelectronics Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific white LED package market size is expected to grow from USD 5.01 billion in 2025 to USD 5.21 billion in 2026 and is forecast to reach USD 6.62 billion by 2031 at a 4.9% CAGR over 2026-2031.

This report is Segmented by Package Architecture (SMD, COB, CSP, and Flip-Chip LED Packages), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Country (China, Japan, India, Southeast Asia, and the Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific White LED Package Market Trends and Insights

Surging Mini And Micro-LED Backlighting Demand In Smart TVs

Premium television brands introduced RGB mini-LED sets at the January 2026 Consumer Electronics Show, demonstrating zone counts as high as 43,000 and peak brightness above 4,000 nits. Eliminating quantum-dot films trims the bill of materials by 15% once die yields stabilize, redirecting savings toward higher-value chip-scale packages. Guangdong and Jiangsu panel assemblers are installing placement tools with sub-5 µm accuracy to manage the tighter pitch, favoring LED suppliers that co-locate back-end assembly within 50 km of module plants. As sub-100 µm die enters volume production, the Asia-Pacific white LED package market migrates from commodity SMD to high-power wafer-level CSP capable of dissipating 3 W mm-2. The trend lifts luminance requirements, driving upstream demand for advanced phosphor blends that maintain color-point stability at elevated current densities.

Aggressive SSL Incentive Programs Across Southeast Asia

Thailand extended double corporate-tax deductions for LED retrofits through 2028, Indonesia preserved its 30% national energy-savings target, and Vietnam plans an Asian Development Bank-backed efficiency framework. These incentives compress lighting payback periods to below 18 months, catalyzing public-sector procurement that prioritizes efficacy over color rendering or lifetime. As municipal buyers standardize on 100 lm/W thresholds, mid-power SMD suppliers face accelerated commoditization. The Asia-Pacific white LED package market therefore sees a volume swell in entry-level devices even as value pools migrate to premium automotive and display niches. Policy momentum is strongest in the commercial high-bay and roadway categories, locking in a multi-year demand base for 2835- and 3030-footprint footprints fabricated in Thai and Vietnamese export-processing zones.

Persistent IP Litigation Over Flip-Chip Architectures

Everlight Electronics lodged patent claims against Lumileds and Seoul Semiconductor in February 2026, citing infringement of U.S. Patent 7,554,126 covering direct-bond flip-chip methods. Injunction risk and escalating legal expenses deter tier-two assemblers from investing in flip-chip tooling, consolidating capacity among vertically integrated giants. OEMs now negotiate indemnification clauses that add 3-5% to contract prices, tempering adoption velocity even where thermal benefits are clear. The Asia-Pacific white LED package market thus experiences a short-term drag on high-power CSP penetration, although incumbent suppliers leverage the dispute to justify premium pricing on authenticated packages.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Build-Out Of EV Charging-Station Lighting Networks

- Cost Downsizing Via Wafer-Level CSP Adoption

- Thermal Management Challenges Above 3 W Power Class

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount device packages captured 58.48% of the Asia-Pacific white LED package market share in 2025, reflecting entrenched adoption in retrofit bulbs and tubes. Wafer-level CSP formats are expanding at a 5.49% CAGR and, by 2031, are expected to shoulder a sizeable portion of automotive headlamp and premium display orders. The Asia-Pacific white LED package market size tied to CSP technology is projected to rise steadily as OEMs seek smaller footprints, higher drive currents, and lower thermal resistance. Margin pressure, however, remains acute in SMD lines where Shenzhen and Dongguan contract factories quote assembly at USD 0.02 per device, undercutting legacy brands by 40%.

High-bay and stadium operators still favor chip-on-board arrays for punchy lumen outputs, while flip-chip packages dominate premium automotive daytime running lamps despite pending litigation. Over the forecast horizon, economics favor CSP lines once monthly volumes top 10 million units, pulling SMD incumbents into retrofit niches or prompting technology upgrades. Suppliers with fan-out expertise gain leverage as television panel makers compress product cycles and demand co-located assembly to meet just-in-time inventory goals. Consequently, the Asia-Pacific white LED package market aligns capital spending with wafer-level processes that promise both cost and performance advantages.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co. Ltd. (Samsung LED)

- Seoul Semiconductor Co. Ltd.

- Everlight Electronics Co. Ltd.

- Lumileds Holding B.V.

- Hongli Zhihui Group Co. Ltd.

- LG Innotek Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- CreeLED, Inc.

- Refond Optoelectronics Co. Ltd.

- Osram GmbH (ams-Osram)

- Edison Opto Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Lextar Electronics Corporation

- Toyoda Gosei Co. Ltd.

- Sharp Corporation

- Rohm Semiconductor

- MLS Co. Ltd. (Forest Lighting)

- Shenzhen Jufei Optoelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Mini- and Micro-LED Backlighting Demand in Smart TVs

- 4.2.2 Aggressive SSL Incentive Programs Across Southeast Asia

- 4.2.3 Rapid Build-out of EV Charging-Station Lighting Networks

- 4.2.4 Cost Downsizing via Wafer-Level CSP Adoption

- 4.2.5 Proliferation of UV-Free Health-Oriented Lighting in Japan

- 4.2.6 Mandatory Energy-Efficiency Labelling in India and China

- 4.3 Market Restraints

- 4.3.1 Persistent IP Litigation Over Flip-Chip Architectures

- 4.3.2 Thermal Management Challenges Above 3 W Power Class

- 4.3.3 Supply Tightness of High CRI Phosphors

- 4.3.4 Rising Mini-LED Die Cost Due to Sapphire Substrate Inflation

- 4.4 Industry Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 COB (Chip-on-Board)

- 5.1.3 CSP (Chip Scale Package)

- 5.1.4 Flip-Chip LED Packages

- 5.2 By Power Class

- 5.2.1 Low Power (Less than 0.5 W)

- 5.2.2 Mid Power (0.5 -1 W)

- 5.2.3 High Power (More than 1 W)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 Southeast Asia

- 5.4.5 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co. Ltd. (Samsung LED)

- 6.4.3 Seoul Semiconductor Co. Ltd.

- 6.4.4 Everlight Electronics Co. Ltd.

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Hongli Zhihui Group Co. Ltd.

- 6.4.7 LG Innotek Co. Ltd.

- 6.4.8 San'an Optoelectronics Co. Ltd.

- 6.4.9 NationStar Optoelectronics Co. Ltd.

- 6.4.10 CreeLED, Inc.

- 6.4.11 Refond Optoelectronics Co. Ltd.

- 6.4.12 Osram GmbH (ams-Osram)

- 6.4.13 Edison Opto Corporation

- 6.4.14 Dominant Opto Technologies Sdn. Bhd.

- 6.4.15 Lextar Electronics Corporation

- 6.4.16 Toyoda Gosei Co. Ltd.

- 6.4.17 Sharp Corporation

- 6.4.18 Rohm Semiconductor

- 6.4.19 MLS Co. Ltd. (Forest Lighting)

- 6.4.20 Shenzhen Jufei Optoelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)