|

市場調查報告書

商品編碼

2064346

北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America White LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

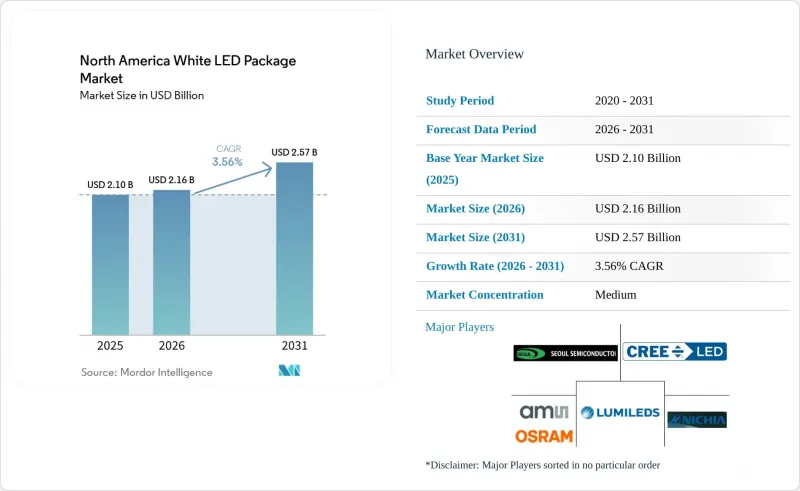

根據 Mordor Intelligence 預測,北美白光LED構裝市場規模將從 2025 年的 21 億美元和 2026 年的 21.6 億美元成長到 2031 年的 25.7 億美元,2026 年至 2031 年的複合年成長率為 3.56%。

本報告按封裝結構(SMD、COB、CSP 和覆晶LED構裝)、功率等級(低功率、中功率和高功率)、應用領域(通用照明、汽車照明、顯示器和背光以及特殊應用)和地區(美國、加拿大和墨西哥)進行細分。市場預測以美元 (USD) 為單位。

北美白光LED構裝市場趨勢與洞察

聯邦和州政府的能源效率法規正在加速向LED的轉變。

新的通用照明燈具法規將於2024年最終確定,該法規要求全向燈在810流明的輸出功率下達到約125流明/瓦的光效,這促使磷光體混合物和驅動電路進行重新設計,以滿足LM-80和TM-21燈具的壽命協議。同時,九個州禁止使用汞燈,導致螢光安定器需求驟減。此外,美國聯邦航空管理局(FAA)目前已指定市售LED燈用於跑道定位系統,超過20個機場正在積極推進早期採用。這些措施共同將維修週期從七年縮短至四年,並增加了符合嚴格光通量維持標準的中功率高功率燈具的出貨量。

每流明成本更低,效率更高

傳統磷光體轉換封裝的晶圓直徑增加了四倍,良率提高了三倍,使得2003年至2020年間的製造成本降低了95.5%。同期,暖白光元件的效率從5.8%提升至38.8%,而光譜效率和紅色磷光體轉換則成為下一個挑戰。 2008年至2020年,照明燈具的零售價格年均下降27.3%,許多商業維修項目的簡單投資回收期縮短至12個月以內。同時,封裝已成為晶片單價的主要成本因素,這使得能夠大規模整合精密光學元件和低熱阻基板的供應商獲得了競爭優勢。

關稅波動和基板供應鏈中斷

對進口LED晶片徵收的301條款關稅使得接收成本難以預測,迫使市政競標縮短報價有效期,並擠壓了簽訂長期定價合約的照明設備製造商的利潤空間。藍寶石晶圓供應仍以亞洲為中心,任何物流中斷都會立即波及北美封裝生產線,延長維修需求旺季的前置作業時間。

細分市場分析

隨著汽車頭燈設計師將低熱阻和超薄光學元件列為優先事項,晶片級技術有望獲得更大的市場佔有率。表面黏著型元件在對成本敏感的通用照明應用中仍然佔據主導地位,因為它們無需更換設備即可在現有的貼片生產線上進行加工。覆晶技術無需焊線,可將結到基板的電阻降低到 2 度C W⁻¹ 以下,並可實現更高的驅動電流。儘管需要額外的組裝步驟,但板載晶片在軌道燈和高棚燈等需要高流明密度的應用中仍然是首選。

高昂的交叉授權費用限制了新企業進入覆晶市場,並維持了現有企業的利潤率。然而,「建設美國」計畫的要求正迫使供應商在美國開設晶片貼裝生產線,這可能會逐步降低單位成本,並加速晶片級封裝(CSP)的普及。在北美白光LED構裝市場,隨著一級汽車製造商的合約逐漸從焊線陣列轉向晶片級裝置,預計晶片級裝置將帶來增量收入。表面貼裝元件(SMD)在改裝燈具領域的持續主導地位,維持了整體架構多樣性的平衡。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 市場促進因素

- 聯邦和州政府的能源法規正在加速向LED的轉變。

- 每流明成本更低,效率更高

- 對智慧城市基礎設施的投資正在推動高功率的實施。

- 汽車製造商向LED頭燈和日間行車燈(DRL)的過渡

- 「建設美國,購買美國貨」採購規則重塑供應鏈

- 垂直農業領域對高顯色性(CRI)可調光白色包裝的需求

- 市場限制因素

- 關稅波動和基板供應鏈中斷

- 對先進包裝生產線進行大量資本投資

- 限制戶外照明光強度的黑夜天空管理條例

- 覆晶架構中專利交叉授權的障礙

- 波特五力分析

第5章 市場規模與成長預測

- 依封裝架構

- SMD(表面黏著型元件)

- COB(板載晶片)

- CSP(晶片級封裝)

- 覆晶LED構裝

- 按輸出類別

- 低功耗(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(超過 1 瓦)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 專業/小眾

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cree LED, Inc.

- Lumileds Holding BV

- Nichia Corporation

- ams-OSRAM GmbH

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Samsung Electronics Co., Ltd.(LED Division)

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Stanley Electric Co., Ltd.

- Epistar Corporation

- Bridgelux, Inc.

- Luminus Devices, Inc.

- Stanley Electric Co., Ltd.

- Citizen Electronics Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america white LED package market size is projected to expand from USD 2.10 billion in 2025 and USD 2.16 billion in 2026 to USD 2.57 billion by 2031, registering a CAGR of 3.56% between 2026 and 2031.

This report is Segmented by Package Architecture (SMD, COB, CSP, and Flip-Chip LED Packages), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America White LED Package Market Trends and Insights

Federal And State Efficiency Mandates Accelerating LED Retrofits

New general-service-lamp rules finalized in 2024 require omnidirectional lamps to reach about 125 lm W-1 at 810 lm output, triggering redesigns of phosphor blends and driver circuits to meet LM-80 and TM-21 lifetime protocols. Parallel mercury-lamp bans across nine states eliminate fluorescent ballast demand, and the Federal Aviation Administration now specifies off-the-shelf LED lamps for runway alignment systems, bringing more than 20 airports into early adoption. Together these actions are shrinking retrofit cycles from seven to four years, lifting volumes of mid-power and high-power packages that satisfy strict lumen-maintenance criteria.

Declining Cost-Per-Lumen And Efficacy Gains

Classic phosphor-converted packages saw manufacturing cost drop 95.5% between 2003 and 2020 as wafer diameters quadrupled and yields tripled. Warm-white device efficiency climbed from 5.8% to 38.8% over the same horizon, leaving spectral efficiency and red-phosphor conversion as the next frontiers. Retail luminaire prices fell 27.3% annually from 2008 to 2020, cutting simple payback to under twelve months for many commercial retrofits, while packaging now dominates per-chip cost, favoring suppliers that integrate precision optics and low-thermal-resistance substrates at scale.

Tariff Volatility And Substrate Supply-Chain Disruptions

Section 301 duties on imported LED chips create unpredictable landed costs, forcing municipal bidders to hold quotes for shorter windows and eroding margins for fixture makers that sell under long-term price agreements. Sapphire wafer supply remains Asia-centric, and any logistics shock quickly ripples into North American packaging lines, lengthening lead times during peak retrofit seasons.

Other drivers and restraints analyzed in the detailed report include:

- Smart-City Infrastructure Investments Boosting High-Power Packages

- Automotive OEM Shift To LED Headlamps And DRLs

- High Capex For Advanced Packaging Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale technology is set to widen its share as automotive forward-lighting designers prioritize low thermal resistance and thinner optics. Surface-mount devices still anchor cost-sensitive general lighting because existing pick-and-place lines handle them without retooling. Flip-chip variants eliminate wire bonds, dropping junction-to-board resistance below 2 °C W-1 and enabling higher drive currents. Chip-on-board remains preferred for track and high-bay luminaires that benefit from high lumen density despite extra assembly steps.

High cross-licensing fees limit new entrants in flip-chip, preserving margins for incumbents. Yet Build America thresholds are nudging suppliers to open U.S. die-attach lines, which may gradually lower unit costs and speed CSP adoption. The North America white LED package market size for chip-scale devices is on course to capture incremental revenue as Tier-1 automotive contracts shift away from wire-bonded arrays. Sustained SMD dominance in retrofit lamps keeps overall architecture diversity balanced.

List of Companies Covered in this Report:

- Cree LED, Inc.

- Lumileds Holding B.V.

- Nichia Corporation

- ams-OSRAM GmbH

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Samsung Electronics Co., Ltd. (LED Division)

- Everlight Electronics Co., Ltd.

- Citizen Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Stanley Electric Co., Ltd.

- Epistar Corporation

- Bridgelux, Inc.

- Luminus Devices, Inc.

- Stanley Electric Co., Ltd.

- Citizen Electronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Market Drivers

- 4.6.1 Federal And State Efficiency Mandates Accelerating LED Retrofits

- 4.6.2 Declining Cost-Per-Lumen And Efficacy Gains

- 4.6.3 Smart-City Infrastructure Investments Boosting High-Power Packages

- 4.6.4 Automotive OEM Shift To LED Headlamps And DRLs

- 4.6.5 Build America, Buy America Sourcing Rules Reshaping Supply Chain

- 4.6.6 Vertical Farming Demand For High-CRI Tunable White Packages

- 4.7 Market Restraints

- 4.7.1 Tariff Volatility And Substrate Supply-Chain Disruptions

- 4.7.2 High Capex For Advanced Packaging Lines

- 4.7.3 Dark-Sky Compliance Ordinances Curbing Outdoor Lumens

- 4.7.4 Patent Cross-Licensing Barriers For Flip-Chip Architectures

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 COB (Chip-on-Board)

- 5.1.3 CSP (Chip Scale Package)

- 5.1.4 Flip-Chip LED Packages

- 5.2 By Power Class

- 5.2.1 Low Power (Less Than 0.5 W)

- 5.2.2 Mid Power (0.5 - 1 W)

- 5.2.3 High Power (Greater Than 1 W)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display And Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cree LED, Inc.

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Nichia Corporation

- 6.4.4 ams-OSRAM GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 LG Innotek Co., Ltd.

- 6.4.7 Samsung Electronics Co., Ltd. (LED Division)

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Citizen Electronics Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 Epistar Corporation

- 6.4.13 Bridgelux, Inc.

- 6.4.14 Luminus Devices, Inc.

- 6.4.15 Stanley Electric Co., Ltd.

- 6.4.16 Citizen Electronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)