|

市場調查報告書

商品編碼

2064348

歐洲白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)Europe White LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

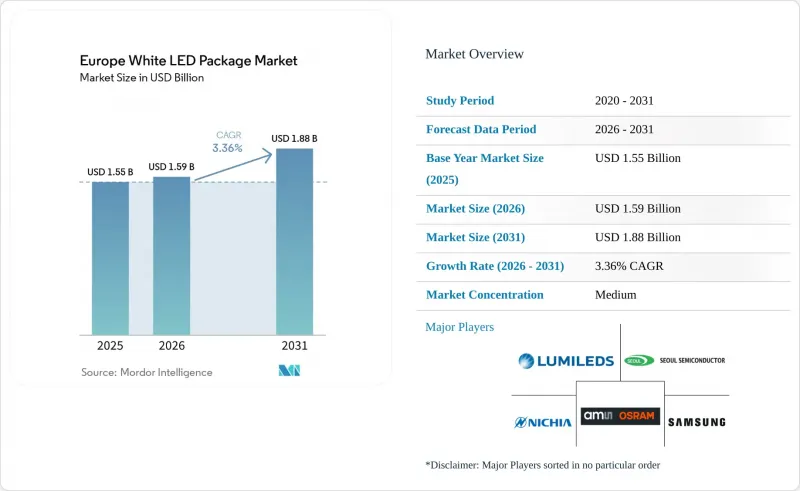

根據 Mordor Intelligence 預測,歐洲白光LED構裝市場規模預計將在 2025 年達到 15.5 億美元,2026 年達到 15.9 億美元,到 2031 年達到 18.8 億美元,2026 年至 2031 年的複合年成長率為 3.36%。

本報告按封裝結構(SMD、COB、CSP、覆晶LED構裝)、功率等級(低功率(小於0.5W)、中功率(0.5-1W)、高功率(1W以上))、應用領域(通用照明、汽車照明、顯示器和背光等)以及地區進行細分。市場預測以美元計價。

歐洲白光LED構裝市場趨勢與洞察

歐盟正在加強能源效率法規。

歐盟能源效率指令2023/1791/EU要求成員國到2030年將其最終能源消耗量降低11.7%,而生態設計法規2019/2020則禁止使用光效低於每瓦85流明的非定向燈具,強制公共機構在所有新競標中指定使用LED維修。市政當局將照明視為關鍵基礎設施。巴黎市政府已簽署一份價值7億歐元的契約,用聯網LED系統替換7萬個照明燈具,預計到2025年,該系統將在10年內節省240吉瓦時(GWh)的能源。米盧斯和雷丁也簽訂了類似的基於結果的特許經營契約,其中包括安裝遠端系統管理節點,這些節點要求使用高效節能組件和可追溯的零部件。這些監管要求確保即使單價下降,基準需求也能維持,因為每拆除一個不合規的照明燈具,就會直接產生對節能組件的需求。擁有 LM-80 文件和可修復性相關文件的供應商可以更輕鬆地滿足競標先決條件,並將他們的合規專業知識轉化為更高的成功率。

規模經濟效應降低了LED構裝成本。

自2023年以來,亞洲晶圓廠運作150毫米和200毫米生產線,已將中功率SMD晶片的價格每年降低8%至12%,使得歐洲的維修項目能夠在兩年內收回投資,即使電費超過0.15歐元/千瓦時。為此,Lumileds公司發布了LUXEON Altilon SMD-A封裝,該封裝針對拾取放置製程進行了最佳化,可將組裝週期縮短18%,同時保持各檔位0.2V的穩定正向電壓,幫助OEM廠商在不影響可靠性的前提下降低成本。採購成本的降低正在加速獎杯和麵板燈等應用領域的採用,擴大了封裝供應商的潛在銷量,即使毛利率有所下降。價格曲線的下降也拉大了通用中中功率晶片與高階晶片級和覆晶之間的性能差距,使供應商能夠細分產品組合,並在高功率細分市場中保持利潤率。因此,規模經濟正在推動基本照明的廣泛應用,同時也為專業建築的研發提供了資金。

商品化帶來的價格壓力

由於亞洲二線廠商提供的中功率LED燈具價格低於0.5美元,歐洲照明OEM廠商不得不採取雙重採購策略,並協商批量採購折扣,這削弱了供應商的忠誠度。在改裝燈泡和螢光管領域,買家普遍認為LED燈具與之相容,迫使即使是老牌廠商也不得不降低利潤率以維持每流明的成本競爭力。一些歐洲中型組裝商正在退出大宗商品市場,並將研發資源重新分配到汽車和園藝領域,因為這些領域的技術壁壘限制了直接的價格競爭。這種壓力在公開競標中最為嚴重,因為競標往往是出價最低者,除非對產品壽命和保固條款施加可衡量的懲罰,否則幾乎沒有溢價空間。因此,儘管出貨量強勁,但價格的持續下跌正在拖慢整體營收成長。

細分市場分析

2025年,表面黏著型元件(SMD)封裝持續維持主導地位,佔據歐洲白光LED構裝市場58.38%的比重。這要歸功於其塑膠外殼、成熟的貼片相容性以及符合歐盟(EU)可維修性法規的現場可維修設計。 SMD封裝繼續被應用於市政路燈專案和商業天花板面板維修,確保了組裝組裝可預測的產量,並使照明燈具製造商能夠將保固索賠控制在合約規定的閾值以下。產品生命週期中期的更新,例如自動光學檢測標記和更嚴格的分級公差,在不中斷現有生產流程的情況下提高了產品品質。此外,廣泛的應用也支撐了對備件的二次需求,儘管單價逐年下降,SMD的獲利能力仍然強勁。

晶片級封裝正呈現更快的成長曲線,預計到2031年將以3.88%的複合年成長率成長,這主要得益於汽車自我調整頭燈和微型LED背板對厚度小於0.5毫米和高導熱性的迫切需求。取消模壓外殼可降低約20%的熱阻,從而在不犧牲流明輸出的情況下實現更小的像素間距和更高的驅動電流。歐洲一級供應商正在將晶圓級磷光體、驅動ASIC和氮化鋁基基板整合到封裝中,以將這種緊湊型外形規格轉化為具有競爭力的單源模組。覆晶和板載晶片)技術正在填補相鄰的細分市場。覆晶被用於高電流日間行車燈,而板載晶片則應用於工業高棚照明,這表明架構選擇不再基於統一的成本指標,而是基於最終用戶的性能目標。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強歐盟各地的能源效率法規

- 規模經濟效應降低了LED構裝成本。

- 汽車自我調整頭燈的普及速度正在加快。

- 根據歐盟RoHS指令,逐步淘汰含汞背光燈。

- 利用白色LED燈擴展垂直農業

- 電費上漲正在加速商業設施的維修。

- 市場限制因素

- 商品化帶來的價格壓力

- 稀土元素磷光體供應鏈的變異性

- 歐盟生態設計可修復性法規限制了CSP的推廣。

- 延長成熟LED裝置的更換週期

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依封裝架構

- SMD(表面黏著型元件)

- COB(板載晶片)

- CSP(晶片級封裝)

- 覆晶LED構裝

- 按輸出類別

- 低功耗(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(1瓦或以上)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 專業/小眾

- 國家

- 英國

- 德國

- 法國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Signify NV

- Osram Opto Semiconductors GmbH

- Lumileds Holding BV

- Nichia Europe BV

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, an SGH Company

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corp.

- ROHM Co., Ltd.

- Citizen Electronics Co., Ltd.

- Lite-On Technology Corp.

- Honglitronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- MLS Co., Ltd.(Forest Lighting)

- ProPhotonix Ltd.

- TT Electronics plc

- Wurth Elektronik GmbH AND Co. KG

- Bicom Optoelectronics Co., Ltd.

- Opto Tech Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe white lED package market size is projected to be USD 1.55 billion in 2025, USD 1.59 billion in 2026, and reach USD 1.88 billion by 2031, growing at a CAGR of 3.36% from 2026 to 2031.

This report is Segmented by Package Architecture (SMD (Surface Mount Device), COB (Chip-On-Board), CSP (Chip Scale Package), Flip-Chip LED Packages), Power Class (Low Power (Below 0. 5 W), Mid Power (0. 5-1 W), High Power (Above 1 W)), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe White LED Package Market Trends and Insights

Energy Efficiency Regulations Tightening Across the EU

The Energy Efficiency Directive 2023/1791/EU compels member states to reduce final energy consumption by 11.7% by 2030, while the Ecodesign Regulation 2019/2020 bans non-directional lamps with a luminous efficacy below 85 lumens per watt, pushing public agencies to specify LED retrofits in every new tender. Municipalities treat lighting as critical infrastructure: Paris signed a EUR 700 million contract in 2025 to replace 70,000 luminaires with connected LED systems that promise 240 GWh in savings over 10 years. Similar performance-based concessions in Mulhouse and Reading involve installing remote-management nodes that require high-efficiency packages and traceable component bills. These regulatory mandates sustain baseline volumes even as unit prices fall, because every non-compliant lamp removed drives direct package demand. Suppliers with LM-80 files and reparability documentation meet tender prerequisites more easily, translating compliance expertise into higher bid-win ratios.

Declining LED Package Costs Due to Economies Of Scale

Asian wafer fabs running 150 mm and 200 mm lines have lowered mid-power SMD prices by 8-12% annually since 2023, enabling European retrofit projects to achieve 2-year paybacks at electricity tariffs above EUR 0.15/kWh. Lumileds answered with its LUXEON Altilon SMD-A, a pick-and-place-optimized package that reduces the assembly cycle time by 18% while maintaining 0.2 V forward-voltage consistency across bins, helping OEMs squeeze costs without sacrificing reliability. Lower landed costs accelerate adoption in troffers and panel lights, expanding the addressable volume for package vendors even as gross margins compress. The price curve also widens the performance gap between commodity mid-power and premium chip-scale or flip-chip options, allowing suppliers to segment portfolios and defend margin in high-power niches. Consequently, economies of scale both democratize basic lighting and finance R&D for specialty architectures.

Commoditization-Driven Price Pressure

Second-tier Asian manufacturers offer sub-USD 0.50 mid-power packages, prompting European luminaire OEMs to dual-source and negotiate bulk discounts that erode supplier loyalty. In retrofit bulbs and tubes, buyers judge LEDs as interchangeable, so even established brands must shave margins to keep per-lumen costs competitive. Some mid-tier European assemblers have exited commodity bins, reallocating R&D toward automotive or horticultural segments where technical barriers curb direct price fights. The squeeze is most acute in public tenders that award on the lowest bid, leaving little room for premium positioning unless lifetime or warranty clauses carry measurable penalties. Persistent price deflation, therefore, drags on overall revenue growth despite steady unit shipments.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Adoption of Automotive Adaptive Headlamps

- EU RoHS Phase-Out of Mercury-Based Backlights

- Supply Chain Volatility for Rare-Earth Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount device packages captured 58.38% of the Europe White LED Package market share in 2025, retaining leadership because their plastic housing, proven pick-and-place compatibility, and field-serviceable design align with the European Union's reparability rules. Municipal street-lighting concessions and commercial ceiling-panel retrofits continue to specify SMD formats, providing assemblers with predictable volumes and helping luminaire makers keep warranty claims below contract thresholds. Mid-cycle product updates, such as automated optical inspection markers and tighter binning tolerances, improve quality without disrupting established production flows. The broad installed base also underpins secondary demand for spare parts, keeping SMD revenues resilient even as unit prices decline each year.

Chip-scale packages are on a faster growth curve, advancing at a 3.88% CAGR through 2031 as automotive adaptive headlamps and micro-LED backplanes favor sub-0.5 millimeter profiles and high thermal conductivity. Eliminating the molded housing drops thermal resistance by roughly 20%, enabling tighter pixel spacing and higher drive currents without lumen sag. European Tier-1 suppliers integrate wafer-level phosphor, driver ASICs, and aluminum nitride substrates, turning the compact form factor into a single-sourced module with defensible pricing. Flip-chip and chip-on-board formats fill adjacent niches-flip-chip in high-current daytime running lamps, chip-on-board in industrial high-bays-highlighting how architecture choice now tracks end-use performance targets rather than one-size-fits-all cost metrics.

List of Companies Covered in this Report:

- Signify N.V.

- Osram Opto Semiconductors GmbH

- Lumileds Holding B.V.

- Nichia Europe B.V.

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, an SGH Company

- Everlight Electronics Co., Ltd.

- Lextar Electronics Corp.

- ROHM Co., Ltd.

- Citizen Electronics Co., Ltd.

- Lite-On Technology Corp.

- Honglitronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- MLS Co., Ltd. (Forest Lighting)

- ProPhotonix Ltd.

- TT Electronics plc

- Wurth Elektronik GmbH AND Co. KG

- Bicom Optoelectronics Co., Ltd.

- Opto Tech Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy Efficiency Regulations Tightening Across EU

- 4.2.2 Declining LED Package Costs Due to Economies of Scale

- 4.2.3 Accelerated Adoption in Automotive Adaptive Headlamps

- 4.2.4 EU RoHS Phase-Out of Mercury-Based Back-Lights

- 4.2.5 Expansion of Vertical Farming Using White LEDs

- 4.2.6 Rising Electricity Costs Driving Commercial Retrofit Acceleration

- 4.3 Market Restraints

- 4.3.1 Commoditization-Driven Price Pressure

- 4.3.2 Supply Chain Volatility for Rare-Earth Phosphors

- 4.3.3 EU Ecodesign Reparability Rules Limiting CSP Uptake

- 4.3.4 Extended Replacement Cycles in Mature LED Installations

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 COB (Chip-on-Board)

- 5.1.3 CSP (Chip Scale Package)

- 5.1.4 Flip-Chip LED Packages

- 5.2 By Power Class

- 5.2.1 Low Power (Below 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (Above 1 W)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display AND Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Country

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Osram Opto Semiconductors GmbH

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Nichia Europe B.V.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 Cree LED, an SGH Company

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Lextar Electronics Corp.

- 6.4.10 ROHM Co., Ltd.

- 6.4.11 Citizen Electronics Co., Ltd.

- 6.4.12 Lite-On Technology Corp.

- 6.4.13 Honglitronic Co., Ltd.

- 6.4.14 Dominant Opto Technologies Sdn. Bhd.

- 6.4.15 MLS Co., Ltd. (Forest Lighting)

- 6.4.16 ProPhotonix Ltd.

- 6.4.17 TT Electronics plc

- 6.4.18 Wurth Elektronik GmbH AND Co. KG

- 6.4.19 Bicom Optoelectronics Co., Ltd.

- 6.4.20 Opto Tech Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)

北美中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)亞太地區白光LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)北美白光LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)美國中功率LED構裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)中功率LED構裝:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)中國中中功率LED構裝市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區中中功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)印度中中功率LED構裝市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)