|

市場調查報告書

商品編碼

2064463

英國GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)United Kingdom GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

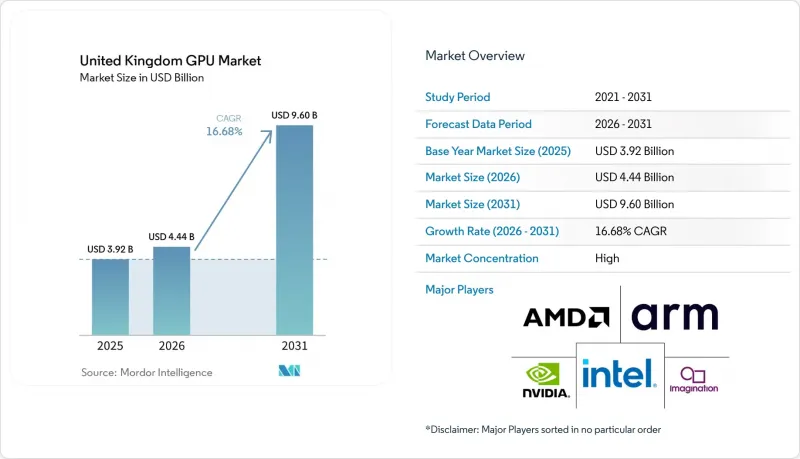

根據 Mordor Intelligence 預測,英國GPU 市場規模將從 2025 年的 39.2 億美元成長到 2026 年的 44.4 億美元,到 2031 年將達到 96 億美元,2026 年至 2031 年的複合年成長率預計為 16.68%。

本報告按整合類型(整合GPU、獨立GPU)和裝置應用(行動裝置和平板電腦、PC和工作站、伺服器和資料中心加速器、遊戲主機和掌上型遊戲機、汽車/ADAS以及其他嵌入式和邊緣裝置)進行細分。市場預測以美元計價。

英國GPU市場的趨勢與洞察

英國資料中心對人工智慧訓練加速器的需求正在激增。

超大規模資料中心營運商已為英國的資料中心預留了多達12萬個Blackwell架構的GPU,目標是在2026年底前部署到位。其中一家供應商就計畫部署6萬個Grace Blackwell架構的GPU。諸如Isambard-AI和Dawn升級等公共部門項目表明,英國政府決心在國內建立自主的計算基礎設施。經濟研究表明,即使是小規模規模的容量提升,每年也能為英國GDP貢獻數十億英鎊。

英國主權人工智慧舉措旨在提升國內GPU叢集

2025年人工智慧成長區計畫簡化了專案核准和電網連接流程,結合了財政獎勵、10億英鎊的公共投資以及主權人工智慧產業論壇的15億英鎊產業貢獻。這些措施將縮短專案前置作業時間,引導工作流向可再生能源潛力高的地區,並建立政策保障機制,確保長期資本投資。

全球GPU供應鏈依然緊張,價格持續上漲。

高頻寬記憶體短缺以及先進節點長達一年的前置作業時間,迫使各公司在部署前提前鎖定配額,導致旗艦顯卡的市場價格飆升至 3500 至 4000 美元,並使金融和醫療保健領域的 AI 專案推遲了幾個季度。

細分市場分析

到2025年,獨立加速器將佔總價值的62.73%,因為企業越來越傾向採用更適合大規模變壓器學習的模組化架構。這個細分市場受益於核心數量的持續成長、高頻寬記憶體以及與專有工具鏈緊密整合的軟體生態系統,這使得英國GPU市場成為以效率為導向的資料中心設計的典範。

在蘋果和AMD新一代系統晶片(SoC)的推動下,行動裝置中的整合式顯示卡市場佔有率持續成長。雖然這些嵌入式顯示卡無法取代多千兆次浮點叢集中的獨立顯示卡,但它們延長了消費者顯示卡的更換週期,以滿足日常辦公室和1080p遊戲的需求。這種轉變導致入門級顯示卡出貨量下降,但高階顯示卡的平均售價卻在上漲,從而維持了英國GPU市場的整體營收成長動能。

其他福利

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 英國資料中心對人工智慧訓練加速器的需求正在激增。

- 雲端遊戲和電子競技生態系統的成長

- 企業中GPU加速分析與高效能運算的採用

- 自動駕駛汽車的研究與開發以及ADAS專案的擴展

- 英國的「主權人工智慧舉措」正在推動國內GPU叢集的發展。

- 過渡到使用設備端推理來實現隱私合規

- 市場限制因素

- 全球GPU供應鏈依然緊張,價格持續上漲。

- 英國資料中心的高昂電力和冷卻成本

- 具備 GPU 程式設計和 CUDA 專業知識的人員短缺。

- 人工智慧能源消耗和碳排放的監管監測

- 產業價值/價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按類型整合

- 整合顯示卡(iGPU)

- 獨立GPU(dGPU)

- 裝置應用程式

- 行動裝置和平板電腦

- 個人電腦和工作站

- 伺服器和資料中心加速器

- 遊戲主機和掌上型遊戲機

- 汽車/ADAS

- 其他嵌入式和邊緣設備

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Imagination Technologies Limited

- Arm Limited

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Graphcore Limited

- Tenstorrent Inc.

- Sapphire Technology Limited

- ASUStek Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Palit Microsystems Ltd.

- Zotac International(MCO)Ltd.

- Gainward Co., Ltd.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom gPU market size expanded from USD 3.92 billion in 2025 to USD 4.44 billion in 2026 and is projected to reach USD 9.60 billion by 2031, registering a 16.68% CAGR over 2026-2031.

This report is Segmented by Integration Type (Integrated GPUs, Discrete GPUs) and Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive/ADAS, Other Embedded and Edge Devices). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom GPU Market Trends and Insights

Surging demand for AI Training Accelerators in UK Data Centers

Hyperscale operators have booked up to 120,000 Blackwell-generation GPUs for United Kingdom facilities by late 2026, with one provider alone targeting 60,000 Grace Blackwell units. Public-sector projects such as Isambard-AI and Dawn upgrades illustrate the government's resolve to anchor sovereign compute domestically, while economic studies suggest even modest capacity additions could inject billions of pounds into annual GDP.

UK Sovereign-AI Initiatives Fueling domestic GPU Clusters

The 2025 AI Growth Zones Initiative streamlines planning approvals and grid connections, pairing fiscal incentives with a GBP 1 billion public investment and a GBP 1.5 billion industry pledge from the Sovereign AI Industry Forum. These measures shorten project lead times, steer workloads to regions rich in renewable potential, and create a policy backstop that underwrites long-cycle capital commitments.

Persistent Global GPU Supply Chain Constraints and Elevated Pricing

High-bandwidth memory shortages and year-long advanced-node lead times force enterprises to lock in allocations far ahead of deployment, inflate street prices of flagship cards to USD 3,500-4,000, and delay AI projects across finance and healthcare by several quarters.

Other drivers and restraints analyzed in the detailed report include:

- Enterprise adoption of GPU-Accelerated Analytics and HPC

- Growth of Cloud Gaming and Esports Ecosystem

- High Power and Cooling Costs In UK Data Centers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete accelerators captured 62.73% of the total value in 2025 as enterprises gravitated toward modular architectures suited for large-scale transformer training. The segment benefits from continual core-count increases, higher bandwidth memory, and software ecosystems tightly coupled to proprietary toolchains, effectively making the United Kingdom GPU market the proving ground for efficiency-ranked datacenter designs.

Integrated graphics continue to climb in mobile devices, strengthened by next-generation system-on-chips from Apple and AMD. While these embedded units will not displace discrete cards in multi-petaflop clusters, they satisfy everyday productivity and 1080p gaming, thereby lengthening consumer replacement cycles. The shift tempers unit volume for entry-level boards but raises the premium-tier average selling price, sustaining overall revenue momentum within the United Kingdom GPU market.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Imagination Technologies Limited

- Arm Limited

- Qualcomm Technologies, Inc.

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Graphcore Limited

- Tenstorrent Inc.

- Sapphire Technology Limited

- ASUStek Computer Inc.

- Micro-Star International Co., Ltd.

- Gigabyte Technology Co., Ltd.

- Palit Microsystems Ltd.

- Zotac International (MCO) Ltd.

- Gainward Co., Ltd.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for AI Training Accelerators in UK Data Centers

- 4.2.2 Growth of Cloud Gaming and eSports Ecosystem

- 4.2.3 Enterprise Adoption of GPU-Accelerated Analytics and HPC

- 4.2.4 Expansion of Autonomous Vehicle R&D and ADAS Programs

- 4.2.5 UK Sovereign-AI Initiatives Fueling Domestic GPU Clusters

- 4.2.6 Shift Toward On-Device Inference for Privacy Compliance

- 4.3 Market Restraints

- 4.3.1 Persistent Global GPU Supply Chain Constraints and Elevated Pricing

- 4.3.2 High Power and Cooling Costs in UK Data Centers

- 4.3.3 Talent Shortage in GPU Programming and CUDA Expertise

- 4.3.4 Regulatory Scrutiny on AI Energy Use and Carbon Emissions

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Integration Type

- 5.1.1 Integrated GPUs (iGPU)

- 5.1.2 Discrete GPUs (dGPU)

- 5.2 By Device Application

- 5.2.1 Mobile Devices and Tablets

- 5.2.2 PCs and Workstations

- 5.2.3 Servers and Datacenter Accelerators

- 5.2.4 Gaming Consoles and Handhelds

- 5.2.5 Automotive / ADAS

- 5.2.6 Other Embedded and Edge Devices

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Imagination Technologies Limited

- 6.4.5 Arm Limited

- 6.4.6 Qualcomm Technologies, Inc.

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 Apple Inc.

- 6.4.9 Graphcore Limited

- 6.4.10 Tenstorrent Inc.

- 6.4.11 Sapphire Technology Limited

- 6.4.12 ASUStek Computer Inc.

- 6.4.13 Micro-Star International Co., Ltd.

- 6.4.14 Gigabyte Technology Co., Ltd.

- 6.4.15 Palit Microsystems Ltd.

- 6.4.16 Zotac International (MCO) Ltd.

- 6.4.17 Gainward Co., Ltd.

- 6.4.18 Dell Technologies Inc.

- 6.4.19 Hewlett Packard Enterprise Company

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space & Unmet-Need Assessment

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析

圖形處理器 (GPU) 市場預測至 2034 年——按 GPU 類型、部署模式、記憶體類型、裝置類型、功能、應用程式、最終用戶和地區分類的全球分析 東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

東南亞GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)超大規模資料中心GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)亞太地區整合GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)歐洲整合顯示卡市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)北美整合顯示卡:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)行動GPU:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)印度GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)德國GPU市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)日本GPU市場:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)