|

市場調查報告書

商品編碼

2063823

乙太網路供電 (PoE) 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)Power Over Ethernet (PoE) Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

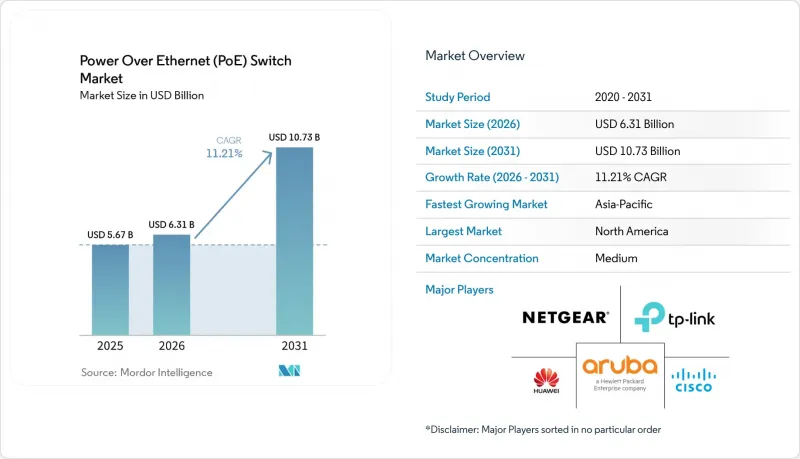

根據 Mordor Intelligence 預測,乙太網路供電 (PoE) 交換器市場規模將從 2025 年的 56.7 億美元和 2026 年的 63.1 億美元成長到 2031 年的 107.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)率為 11.21%。

本報告依管理功能(託管型、非託管型、智慧型)、功率等級(15.4W以下、30W、60W、90W、90W以上)、連接埠數量(4-8個、9-16個、17-24個、其他)、最終用戶產業(住宅、商業、工業、其他)、應用程式(IP監控、其他地區進行存取市場預測以美元計價。

全球乙太網路供電 (PoE) 交換器市場趨勢與洞察

物聯網主導的智慧建築實施

商業建築業主正從專有的建築自動化控制器轉向以乙太網路為基礎的感測器,以監測人員佔用、溫度和室內空氣品質。這種轉變導致每層樓所需的乙太網路供電 (PoE) 連接埠數量增加了兩到五倍,迫使設施管理人員部署底盤功率預算超過 740 瓦的 802.3bt 交換器。將操作技術(OT) 設備整合到企業 IP 網路中也會使其面臨網路威脅。因此,採購部門擴大指定使用嵌入式防火牆和零信任分段功能的交換器。西門子在 2025 年公佈財報中指出,符合即將訂定的歐盟《網路彈性法案》要求的板載安全引擎將成為德國和英國智慧建築競標的強制性要求。因此,擁有高 PoE供給能力和原生安全功能的供應商在競標。

IP視訊監控的擴展

市政機構和大型校園正以4K和8K IP攝影機取代類比CCTV,這些攝影機功耗高達25至90瓦,遠超過以往設備15瓦的預算。紐約市一份2024年的交通監視錄影機合約將使用約2萬個乙太網路供電(PoE)端口,這表明一個智慧城市計畫就能帶動區域需求。海康威視和大華等攝影機製造商將於2025年推出支援Type 4供電模式並內建AI分析功能的鏡頭,這將迫使整合商選擇90瓦的交換機,否則將面臨電壓下降的風險。保險公司開始為加密且防篡改的IP監控系統提供保費折扣,這即使在預算緊張的行業也能透過縮短更換週期來節省成本。

高昂的初始硬體成本

企業在考慮購置一台功能齊全的48埠802.3bt交換器(售價15,000美元)、冗餘電源、UPS系統以及支援合約時,每個連接埠的成本可能高達800至1,200美元。如此高昂的前期成本構成了一大障礙,尤其對於小規模的企業和預算有限的企業而言更是如此。對價格敏感的中小型企業通常依賴不具備集中管理功能的中間跨接供電器,導致營運效率低。受美國e-Rate指南約束且必須遵守最低競標價格規定的公立學校,進一步限制了其投資先進乙太網路供電(PoE)交換器解決方案的能力。為了應對這些挑戰,供應商正在推出租賃和訂閱計劃,有效地將資本支出(CapEx)轉化為營運支出(OpEx)。這些計劃旨在透過長期分攤成本,使乙太網路供電(PoE)交換器更易於普及。特別是,思科的「2025 PoE 即服務」據說可將初始成本降低高達 70%,使其成為希望在控制預算的同時採用先進的乙太網路供電 (PoE) 技術的組織的現實選擇。

細分市場分析

預計到2025年,管理型交換器將佔總銷售額的45.61%,凸顯了網路團隊對SNMP監控、VLAN分段和服務品質(QoS)的依賴,以優先處理即時流量。隨著企業將存取控制清單和零信任策略直接整合到其分送層,管理型乙太網路供電(PoE)交換器市場預計將超越非管理型產品。同時,工業級型號的興起表明,堅固耐用的機殼、寬廣的溫度範圍和IEC 61850合規性正變得與端口數量同等重要,尤其是在配備運動控制機器人和高速攝影機的工廠環境中。智慧交換器結合了基於瀏覽器的配置和有限的分析功能,滿足了中型企業的需求,特別是那些沒有認證工程師的企業以及尋求比即插即用更高可見性的中小企業。乙太網路供電(PoE)交換器市場也積極擁抱雲端技術。 Extreme Networks 於 2025 年宣布推出的零接觸配置技術,將允許分店在無需專業人員的情況下安裝設備,從而將部署時間從數小時縮短到數分鐘。

工業級乙太網路供電 (PoE) 交換器正以 13.23% 的複合年成長率 (CAGR) 高速成長,成為該細分市場中成長最快的領域。這一成長主要得益於預測性維護項目,這些項目在每條組裝上增加了數百個振動和溫度感測器,每個感測器的功耗為 15 至 25 瓦。 Moxa 和 Advantech 等廠商正在積極回應,推出可在 -40 度C至 75 度C的極端環境下運作並承受 5g 衝擊的 DIN 導軌交換器。這些特性能夠保護電子元件免受堆高機碾壓和油霧侵蝕。非網管型設備在家庭和小規模辦公室中仍然有售,因為在這些場所,成本優先於功能,但隨著雲端控制面板成為網管型設備的低成本甚至免費附加功能,它們在 PoE 交換器市場的佔有率正在逐漸萎縮。展望未來,正如 Lantronix 在 2026 年所預測的那樣,嵌入式人工智慧引擎將模糊網路硬體和邊緣運算節點之間的界限,這意味著未來的網管型交換器還可以作為監控影像和生產指標的推理加速器。

2025 年出貨量中,功率不超過 30 瓦的型號佔比 49.94%,這主要歸功於傳統 802.3at 攝影機和 Wi-Fi 6網路基地台在部署基數上的持續存在。然而,功率需求超過 60 瓦的設備,例如 Wi-Fi 7 無線設備和支援 AI 的 PTZ 攝影機,正在推動 4 型交換器的年成長率在 2031 年達到 15.81%。隨著廠商逐步淘汰 100 Mb/s 上行鏈路並採用Gigabit介面,15.4 瓦 802.3af 級 PoE 交換器的市場佔有率正在萎縮。雖然 60 瓦的過渡頻寬目前被用於數位電子看板和互動式資訊亭,但隨著思科 100 瓦通用乙太網路供電 (PoE) 等高功率專有標準的普及,其重要性可能會降低。

展望未來,即使現有設備僅消耗 25-45 瓦,校園和醫療保健客戶也正在為 90 瓦的緩衝功率進行預算。這反映了十年前從 15 瓦過渡到 30 瓦時所學到的經驗教訓。美國國家電氣規範 (NEC) 第 840 條等行業標準允許低壓承包商在無需持有高級電工執照的情況下處理 100 瓦以下的電纜,從而加速了其在辦公大樓維修專案中的應用。然而,歐盟低電壓指令仍然要求由持有執照的工人進行操作,這增加了成本並阻礙了向 90 瓦的過渡。半導體供應商正在降低直流-直流轉換過程中的損耗,交換器製造商預測,到 2028 年,相容 100 瓦的半導體將開始出貨。這表明,乙太網路供電 (PoE) 交換器市場有望在功率方面迎來另一次飛躍。

區域分析

預計到2025年,北美將佔全球銷售額的38.12%。這主要得益於企業更換了3750台已使用近十年的Catalyst設備,並遷移到支援Wi-Fi 6E的分送層。聯邦E-Rate計畫的資金正在推動K-12(幼兒園至高中)學校的設備升級,而國防供應鏈中的網路安全成熟度模型認證(CMMC)則鼓勵主要承包商採用基於硬體信任根的交換機。加拿大的發展趨勢與美國類似,但頂尖大學的智慧校園計畫進一步推動了這一趨勢。

亞太地區是推動快速成長的主要動力,預計到2031年複合年成長率將達到13.87%。中國和印度正在工業4.0維修中部署乙太網路供電(PoE)技術,將操作技術和資訊技術整合起來,使每個電路的連接埠密度提高了三到五倍。隨著電子組裝廠的激增,東南亞國家也正在效法這項做法。同時,澳洲的醫院和高校正在利用數位包容津貼部署Wi-Fi 6E網路基地台和90瓦照明驅動器。

在歐洲,由於NIS2和DORA法規的實施,市場呈現中等個位數的成長率。這兩項法規強制要求關鍵基礎設施營運商和銀行採用乙太網路供電(PoE)端點分段技術。建築能源性能指令(EPBD)也加速了PoE照明在商業設施的維修。拉丁美洲的市場規模仍然較小,主要集中在巴西的金融業和阿根廷的農業出口領域,在這些地區,IP監控系統正被應用於糧食倉儲設施以防止盜竊。中東和非洲的市場則以專案主導,沙烏地阿拉伯的NEOM和杜拜智慧城市都已規劃了PoE街道基礎設施,但其實施依賴公共部門的競標流程。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 引進利用物聯網技術的智慧建築

- IP視訊監控的擴展

- Wi-Fi 6/6E/7 接入點的電源需求

- 引入基於PoE的智慧照明

- 邊緣AI設備的PoE供電

- 強制性網路安全措施

- 市場限制因素

- 初始硬體成本相對較高。

- 散熱極限為 90 瓦

- 半導體供需失衡

- 醫療檢查室中電磁干擾(EMI)的擔憂

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 價格分析

第5章 市場規模與成長預測

- 透過管理能力

- 管理型 PoE 交換機

- 非網管型 PoE 交換機

- 智慧型 PoE 交換機

- 按輸出類別

- 15.4 瓦或更低 (802.3af)

- 30 瓦或更低 (802.3at)

- 60 瓦或以下(3 型)

- 90 瓦或以下(4 型)

- 超過 90 瓦(超高功率 PoE)

- 港口

- 4-8個端口

- 9-16個端口

- 17-24個端口

- 25-48個端口

- 超過48個端口

- 產業最終用途

- 住宅

- 商業建築

- 工業和製造業

- 政府和公共基礎設施

- 資訊科技/通訊

- 衛生保健

- 教育

- 其他終端用戶產業(零售、運輸和物流)

- 透過使用

- IP監視錄影機

- 無線存取點

- VoIP電話和UC終端

- 建築自動化和PoE照明

- 工業感測器和控制器

- 邊緣運算節點和人工智慧盒子

- 5G小型基地台和分散式天線系統(DAS)。

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- ASEAN

- 大洋洲

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems, Inc.

- Hewlett Packard Enterprise(Aruba)

- Huawei Technologies Co., Ltd.

- Juniper Networks, Inc.

- Netgear, Inc.

- TP-Link Corporation Ltd.

- D-Link Corporation

- Extreme Networks, Inc.

- Ubiquiti Inc.

- Arista Networks, Inc.

- Allied Telesis Holdings KK

- Siemens AG

- Advantech Co., Ltd.

- Moxa Inc.

- Belden Inc.(Hirschmann)

- PLANET Technology Corp.

- Microchip Technology Inc.

- Zyxel Communications Corp.

- Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Phoenix Contact GmbH & Co. KG

- TRENDnet, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the power over Ethernet (PoE) switch market size is projected to expand from USD 5.67 billion in 2025 and USD 6.31 billion in 2026 to USD 10.73 billion by 2031, registering a CAGR of 11.21% between 2026 to 2031.

This report is Segmented by Management Capability (Managed, Unmanaged, and Smart), Power Class (Up To 15. 4W, Up To 30W, Up To 60W, Up To 90W, and Above 90W), Port Count (4-8, 9-16, 17-24, and More), End-Use Industry (Residential, Commercial, Industrial, and More), Application (IP Surveillance, Wireless APs, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Power Over Ethernet (PoE) Switch Market Trends and Insights

IoT-Driven Smart-Building Deployments

Commercial property owners are migrating from proprietary building-automation controllers to Ethernet-based sensors that monitor occupancy, temperature, and indoor air quality. That change multiplies the number of Power over Ethernet (PoE) ports required per floor by three to five, pushing facility managers toward 802.3bt switches with chassis power budgets exceeding 740 watts. The integration of operational technology devices into corporate IP networks also exposes them to cyber threats, so purchasing teams increasingly specify switches with embedded firewalls and zero-trust segmentation. Siemens reported in its 2025 results call that smart-building bids in Germany and the United Kingdom now require on-board security engines that meet forthcoming EU Cyber Resilience Act obligations. Vendors that marry high Power over Ethernet (PoE) budgets with native security are therefore winning tenders ahead of rivals that treat protection as an optional license.

IP-Video Surveillance Expansion

Municipalities and large campuses are replacing analog CCTV with 4K and 8K IP cameras that draw 25-90 watts, far above the 15-watt budgets of earlier devices. New York City's 2024 traffic-camera contract consumed roughly 20,000 Power over Ethernet (PoE) ports, exemplifying how a single smart-city project can lift regional demand. Camera makers such as Hikvision and Dahua shipped Type 4-powered models with on-board AI analytics in 2025, driving integrators to pick 90-watt switches or risk voltage sag. Insurance carriers have begun offering premium discounts when encrypted, tamper-proof IP surveillance is installed, adding a financial nudge that shortens replacement cycles even in budget-constrained sectors.

High Upfront Hardware Costs

Enterprises can face costs of USD 800-1,200 per port when factoring in a fully loaded 48-port 802.3bt switch (priced at USD 15,000), redundant power, UPS systems, and support contracts. These high upfront costs pose a significant barrier, particularly for smaller organizations and budget-constrained sectors. Price-sensitive small firms often resort to mid-span injectors, which lack centralized management capabilities, thereby limiting operational efficiency. Public schools, bound by U.S. E-Rate guidelines, must adhere to lowest-bid rules, further restricting their ability to invest in advanced Power over Ethernet (PoE) switch solutions. To address these challenges, vendors have introduced leasing and subscription programs, effectively converting capital expenditures (capex) into operational expenditures (opex). These programs aim to make Power over Ethernet (PoE) switches more accessible by spreading costs over time. Notably, Cisco's 2025 PoE-as-a-service offering is said to reduce initial cash outlays by as much as 70%, providing a viable alternative for organizations seeking to manage their budgets while adopting advanced Power over Ethernet (PoE) technologies.

Other drivers and restraints analyzed in the detailed report include:

- Wi-Fi 6 / 6E / 7 Access-Point Power Needs

- Power over Ethernet (PoE)-Based Smart Lighting Roll-Outs

- Heat-Dissipation Limits at 90 W

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed switches commanded 45.61% of 2025 revenue, underscoring how network teams depend on SNMP monitoring, VLAN segmentation, and quality-of-service to prioritize real-time traffic. The Power over Ethernet switch market size for managed products is projected to outpace unmanaged units as enterprises integrate access control lists and zero-trust policies directly into distribution layers. A parallel rise in industrial-grade models shows that ruggedized housings, extended-temperature operation, and IEC 61850 compliance now matter as much as port counts, particularly on factory floors that house motion-control robots and high-speed cameras. Smart switches address a mid-tier audience by bundling browser-based configuration with limited analytics, which resonates with small businesses that lack certified engineers yet still want visibility beyond plug-and-play behavior. The Power over Ethernet switch market has also embraced cloud onboarding; Extreme Networks' zero-touch provisioning, launched in 2025, allows branches to install equipment without specialized staff, cutting deployment windows from hours to minutes.

Industrial Power over Ethernet (PoE) variants are advancing at a 13.23% CAGR, the fastest clip inside this segmentation. Growth is propelled by predictive-maintenance projects that add hundreds of vibration and temperature sensors to each assembly line, each pulling 15-25 watts. Vendors such as Moxa and Advantech have responded with DIN-rail switches that tolerate -40 °C to 75 °C and survive 5 g shocks, attributes that shield electronics from forklift traffic and oil-mist exposure. Unmanaged devices still sell into home and micro-office sites where cost trumps features, but their share of the Power over Ethernet switch market is slowly eroding as cloud dashboards become cheap or free companions to managed gear. On the horizon, embedded AI engines, as previewed by Lantronix in 2026, blur the line between network hardware and edge-computing node, suggesting that tomorrow's managed switch could double as an inference accelerator for surveillance feeds or production metrics.

Up-to-30-watt models retained 49.94% of 2025 shipments because legacy 802.3at cameras and Wi-Fi 6 access points still dominate installed bases. However, devices needing more than 60 watts, including Wi-Fi 7 radios and AI-enabled PTZ cameras, are stoking 15.81% annual growth for Type 4 switches through 2031. The Power over Ethernet switch market share of the 15.4-watt 802.3af class is shrinking as vendors retire 100-Mb/s uplinks in favor of gigabit interfaces. A transitional 60-watt band serves digital signage and interactive kiosks yet could fade if ultra-high-power proprietary specs, such as Cisco's 100-watt Universal Power over Ethernet (PoE), gain wider traction.

Looking ahead, campus and healthcare customers are budgeting for 90-watt headroom even when today's devices draw only 25-45 watts, reflecting lessons learned during the jump from 15 watts to 30 watts a decade ago. Industry codes such as U.S. NEC Article 840 allow low-voltage installers to handle cables below 100 watts without master-electrician licenses, which accelerates rollout in office renovations. Conversely, the European Low-Voltage Directive still obliges certified labor, adding a cost premium that tempers 90-watt uptake. Silicon vendors are shrinking DC-DC conversion losses, and switch makers project that 100-watt-capable silicon could ship by 2028, positioning the Power over Ethernet switch market for another generational leap in delivered wattage.

Geography Analysis

North America held 38.12% of 2025 revenue as enterprises swapped out decade-old Catalyst 3750 units and migrated to Wi-Fi 6E-ready distribution layers. Federal E-Rate funding boosts K-12 refreshes, and the Cybersecurity Maturity Model Certification in defense supply chains pushes prime contractors toward switches with hardware roots of trust. Canada mirrors U.S. trends, with an added lift from smart-campus programs at major universities.

Asia Pacific is the fast-growth engine with a 13.87% CAGR through 2031. China and India are embedding Power over Ethernet (PoE) within Industry 4.0 retrofits that unify operational and information technology, expanding port density by three to five times on each line. Southeast Asian nations follow similar paths as electronics-assembly hubs proliferate, while Australian hospitals and colleges adopt Wi-Fi 6E access points and 90-watt lighting drivers under digital-inclusion grants.

Europe posts mid-single-digit growth, buoyed by NIS2 and DORA mandates that force critical-infrastructure operators and banks to segment Power over Ethernet (PoE) endpoints. The Energy Performance of Buildings Directive also incentivizes PoE lighting retrofits across the commercial stock. Latin America remains smaller, concentrated in Brazilian finance and Argentine agricultural exports where grain elevators adopt IP surveillance against theft. The Middle East and Africa are project-driven; Saudi Arabia's NEOM and Dubai Smart City specify PoE street infrastructure, but rollouts depend on public-sector tender cycles.

- Cisco Systems, Inc.

- Hewlett Packard Enterprise (Aruba)

- Huawei Technologies Co., Ltd.

- Juniper Networks, Inc.

- Netgear, Inc.

- TP-Link Corporation Ltd.

- D-Link Corporation

- Extreme Networks, Inc.

- Ubiquiti Inc.

- Arista Networks, Inc.

- Allied Telesis Holdings K.K.

- Siemens AG

- Advantech Co., Ltd.

- Moxa Inc.

- Belden Inc. (Hirschmann)

- PLANET Technology Corp.

- Microchip Technology Inc.

- Zyxel Communications Corp.

- Hikvision Digital Technology Co., Ltd.

- Dahua Technology Co., Ltd.

- Phoenix Contact GmbH & Co. KG

- TRENDnet, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IoT-driven smart-building deployments

- 4.2.2 IP-video surveillance expansion

- 4.2.3 Wi-Fi 6/6E/7 AP power requirements

- 4.2.4 PoE-based smart lighting roll-outs

- 4.2.5 Edge-AI device PoE powering

- 4.2.6 Cyber-secure network mandates

- 4.3 Market Restraints

- 4.3.1 High upfront hardware costs

- 4.3.2 Heat-dissipation limits at 90 W

- 4.3.3 Semiconductor supply imbalance

- 4.3.4 EMI concerns in medical labs

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Management Capability

- 5.1.1 Managed PoE Switch

- 5.1.2 Unmanaged PoE Switch

- 5.1.3 Smart PoE Switch

- 5.2 By Power Class

- 5.2.1 Up to 15.4 W (802.3af)

- 5.2.2 Up to 30 W (802.3at)

- 5.2.3 Up to 60 W (Type 3)

- 5.2.4 Up to 90 W (Type 4)

- 5.2.5 Above 90 W (Ultra PoE)

- 5.3 By Port Count

- 5.3.1 4-8 Ports

- 5.3.2 9-16 Ports

- 5.3.3 17-24 Ports

- 5.3.4 25-48 Ports

- 5.3.5 Above 48 Ports

- 5.4 By End-Use Industry

- 5.4.1 Residential

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial and Manufacturing

- 5.4.4 Government and Public Infrastructure

- 5.4.5 IT and Telecom

- 5.4.6 Healthcare

- 5.4.7 Education

- 5.4.8 Other End-Use Industries (Retail, Transportation and Logistics)

- 5.5 By Application

- 5.5.1 IP Surveillance Cameras

- 5.5.2 Wireless Access Points

- 5.5.3 VoIP Phones and UC Endpoints

- 5.5.4 Building Automation and PoE Lighting

- 5.5.5 Industrial Sensors and Controllers

- 5.5.6 Edge Computing Nodes and AI Boxes

- 5.5.7 5G Small Cells and DAS

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 ASEAN

- 5.6.4.6 Oceania

- 5.6.4.7 Rest of the Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of the Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Hewlett Packard Enterprise (Aruba)

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Juniper Networks, Inc.

- 6.4.5 Netgear, Inc.

- 6.4.6 TP-Link Corporation Ltd.

- 6.4.7 D-Link Corporation

- 6.4.8 Extreme Networks, Inc.

- 6.4.9 Ubiquiti Inc.

- 6.4.10 Arista Networks, Inc.

- 6.4.11 Allied Telesis Holdings K.K.

- 6.4.12 Siemens AG

- 6.4.13 Advantech Co., Ltd.

- 6.4.14 Moxa Inc.

- 6.4.15 Belden Inc. (Hirschmann)

- 6.4.16 PLANET Technology Corp.

- 6.4.17 Microchip Technology Inc.

- 6.4.18 Zyxel Communications Corp.

- 6.4.19 Hikvision Digital Technology Co., Ltd.

- 6.4.20 Dahua Technology Co., Ltd.

- 6.4.21 Phoenix Contact GmbH & Co. KG

- 6.4.22 TRENDnet, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年工業乙太網網路交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)管理型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)非網管型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年工業乙太網網路交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)管理型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)非網管型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)