|

市場調查報告書

商品編碼

2063701

工業乙太網網路交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Industrial Ethernet Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

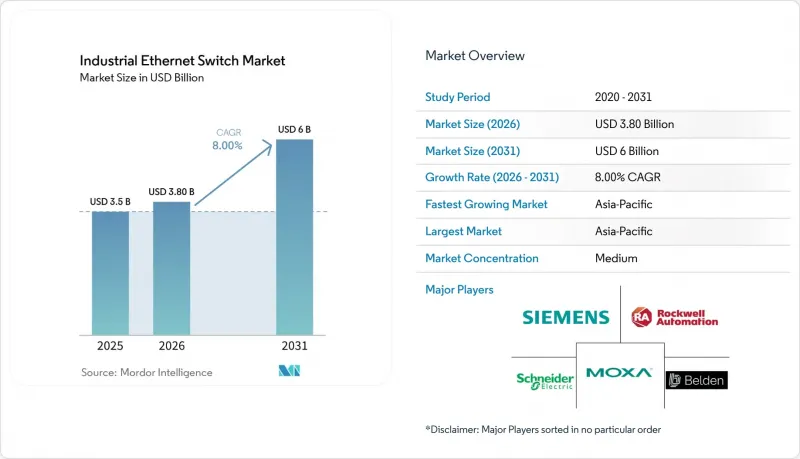

據 Mordor Intelligence 稱,工業乙太網網路交換器市場預計將從 2025 年的 35 億美元成長到 2026 年的 38 億美元,到 2031 年達到 60 億美元,預計 2026 年至 2031 年的複合年成長率為 8%。

本報告按管理類型(管理型交換器和非管理型交換器)、層功能(二層和三層)、連接埠數量(8 個或以下、9 至 24 個連接埠、25 至 48 個連接埠及以上)、資料速率(100 Mbps 或以下、千兆乙太網路、萬兆乙太網路及以上)、最終用戶產業(100 Mbps 或以下、Gigabit乙太網路、Gigabit乙太網路及以上)、最終用戶產業(客製化及其他)和區域進行客製化細分。市場預測以美元 (USD) 為單位。

全球工業乙太網交換器市場趨勢與洞察

工業物聯網應用快速擴展

工業物聯網 (IIoT) 專案正在推動生產線上乙太網路終端數量的激增,預計到 2025 年,工業乙太網將佔新增節點安裝量的 76%。每個智慧感測器和邊緣設備都需要一個交換器端口,而未經管理的菊鏈連接會引入延遲,導致控制迴路中斷 10-50 毫秒。公共產業產業清晰地展現了這種轉變。英國西北電力公司 (Electricity North West) 已在其變電站部署了強大的交換機,以每秒 50 幀的速度傳輸同步資料——這是傳統串行鏈路無法處理的流量。交換器製造商現在正在整合 IEEE 1588 主時鐘,從而無需單獨的定時盒,並將材料清單(BOM) 減少約 15%。隨著工廠營運商試運行時間的縮短,對具有確定性傳輸功能的連接埠的需求不斷成長,這推動了工業乙太網網路交換器市場的核心趨勢。

智慧工廠對確定性網路的需求日益成長

汽車和半導體工廠需要協作機器人和視覺系統來實現亞微秒同步,而這只有支援TSN的交換器才能實現。最終版的IEEE 802.1Qbv和802.1AS標準允許設備將診斷流量分配到盡力而為佇列,同時保留控制流量的頻寬。繼AUTOSAR於2024年將乙太網路指定為汽車骨幹網路之後,歐洲汽車製造商正主導乙太網路的普及應用。 2025年,西門子對其SCALANCE XC-300系列交換器進行了升級,增加了IEEE 802.1Qci過濾功能,以隔離網路免受異常流量的影響。離散製造業報告稱,採用TSN技術後,試運行時間縮短了30-40%,進一步推動了對工業乙太網交換器的需求。

堅固型交換器的初始投資成本較高

工業級交換器具有更寬的溫度範圍和三防膠,其價格比商用設備高出 200% 至 400%。例如,一台配備Gigabit上行鏈路的思科工業乙太網路 5000 的標價約為 15,400 美元,而入門級 IE2000 的標價僅為 906.50 美元,此外,每台設備還需額外支付 500 至 1,000 美元的危險場所認證費用。鐵路和石油鑽井平台專案需要符合 EN 50155 或 ATEX 標準,這會導致預算超支並延誤採購。雖然租賃模式旨在平衡支出,但客戶仍然保持謹慎,因為如果產品在合約期間內停產,則過時的風險將轉嫁給買方。

細分市場分析

到2025年,託管硬體將佔工業乙太網交換器市場的68.75%,預計到2031年將以11.31%的複合年成長率成長。諸如NIS2之類的監管要求強制關鍵服務提供者進行網路分段和審計追蹤維護,而這些功能只有託管設備才能提供。流程工廠優先使用SNMP陷阱和系統日誌進行集中監控,而離散生產線在點對點鏈路足以滿足需求時仍使用非託管設備。 「智慧非託管」產品配備唯讀儀表板,模糊了兩者之間的界限,但即將訂定的網路安全法規要求韌體更新,這進一步推動了支出向全託管設備的轉移。隨著最終用戶將交換器不僅視為連接設備,而且視為關鍵安全資產,在連接埠層級整合零信任存取控制的供應商有望獲得市場佔有率。

在機載叢集中,非網管型交換器仍然佔據重要地位,因為其配置負擔超過了其帶來的可視性提升。羅克韋爾自動化 (Rockwell) 的 Stratix 2100 將於 2025 年年中推出,旨在滿足此細分市場的需求,提供 5 埠和 8 埠兩種型號。然而,隨著網路佈線需求的增加,棕地工廠正在逐步替換仍在運行的非網管型設備,這擴大了網管型交換器的市場規模,並支撐了工業乙太網交換器市場在該領域的長期成長。

到2025年,二層產品將佔據61.40%的市場佔有率,但隨著邊緣電腦需要VLAN間路由來實現微隔離,三層交換器的年複合成長率(CAGR)正以11.76%的速度成長。公共產業正在採用三層技術來傳輸符合IEC 61850 Edition 2.1標準的路由GOOSE訊息,使變電站能夠在無需多播洪的情況下,在大範圍內交換狀態資訊。百通(Belden)將於2025年推出的XTran系列產品正是這一趨勢的體現,它將路由GOOSE與MPLS和SD-WAN結合。

成本壁壘正在降低。博通和Marvell的晶片價格預計從2024年起將下降20%,從而縮小二層和三層產品之間的價格差距。隨著各廠商利用板載存取控制清單(ACL)分類生產區域,三層網路正成為預設的升級路徑,擴大了具備路由功能的工業乙太網的市場規模,並降低了純二層設備的吸引力。

區域分析

預計到2025年,亞太地區將以35.12%的市佔率引領工業乙太網交換器市場,並在2031年之前維持9.89%的複合年成長率。印度的自動化產業預計將從2026年的36.4億美元成長到2034年的136.5億美元,這將推動新工廠對交換器的需求。中國的電動車和半導體叢集需要支援TSN(終端同步網路)的設備,以實現±1微秒的同步精度。同時,日本工具機製造商正在將10Gigabit交換器整合到數控控制器中,從而減少了30%的機櫃面積。韓國造船廠正在部署符合船用標準的光纖骨幹網路來取代其專有的串行線路,而澳洲的公共產業正在遷移到IEC 61850 Edition 2.1三層架構。儘管人們普遍認為高效能硬體成本較高,但區域人事費用優勢縮短了投資回收期,而政府對智慧製造的獎勵也正在推動更快的設備更新換代。

北美保持著強勁的地位,這得益於製造業回流,汽車和醫療設備的產能不斷擴大。美國網路安全和基礎設施安全局 (CISA) 發布的 2025 年網路分段指南正迫使公共產業和運輸公司逐步淘汰非託管設備。 CenterPoint Energy 公司 2025 年的管線骨幹網路透過將洩漏偵測遙測技術整合到乙太網路中,營運成本降低了 25%。加拿大礦業公司正在部署符合 Class I Division 1 標準的交換機,這些交換機能夠承受低至 -40 度C的低溫。同時,由於 ASIC 晶片供不應求,墨西哥一家一級供應商的 TSN 認證硬體交付等待 20 週才能交付。該地區還面臨嚴重的勞動力短缺,平均招募週期長達 120 天,這促使買家轉向雲端管理設備。

在歐洲,TSN(終端交換網路)憑藉其在汽車和化學製造商中的廣泛應用,已佔據了相當大的市場佔有率。將於2024年10月生效的NIS2標準正在加速公共產業、交通運輸和醫療保健產業對管理型交換機的採用。德國的工業4.0計畫正在加速TSN上OPC UA(光子通訊協定)的普及,倍福(Beckhoff)已將交換結構整合到其控制平台中。 2025年,西北電力公司(Electricity North West)將透過穩健的硬體連接相量電錶,法國鐵路將採用符合EN 50155標準、環路恢復時間為20毫秒的設備。到2026年,28-65奈米ASIC(專用積體電路)的前置作業時間將超過30週,凸顯了供應鏈的限制,儘管義大利和西班牙在智慧電網和工廠現代化方面的預算不斷增加。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 工業物聯網應用快速擴展

- 智慧工廠對確定性網路的需求日益成長

- 製程工業中從現場匯流排到乙太網路的過渡

- 邊緣設備中乙太網路供電 (PoE) 的普及應用日益廣泛

- 時間敏感網路 (TSN) 合規性要求

- 預計從 2025 年起,網路實體安全領域的投資將大幅成長。

- 市場限制因素

- 加固型交換器的初始資本支出 (CAPEX) 較高

- 熟練的工業網路人員短缺

- 整合傳統設備面臨的挑戰

- 專用ASIC的供應鏈波動

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 依管理類型

- 管理型交換機

- 非網管型交換機

- 圖層大小

- 第二層

- 第三層

- 按連接埠數量

- 少於 8 個連接埠

- 9-24個端口

- 25-48個端口

- 超過48個端口

- 按數據速率

- 100 Mbps 或更低

- Gigabit乙太網

- 10Gigabit以太網

- 40Gigabit或以上

- 按最終用戶行業分類

- 離散製造

- 流程工業

- 運輸/物流

- 能源公用事業

- 政府和智慧城市

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- Belden Inc.

- Moxa Inc.

- Advantech Co., Ltd.

- Phoenix Contact GmbH & Co. KG

- Hirschmann Automation and Control GmbH

- Cisco Systems, Inc.

- Eaton Corporation plc

- ABB Ltd.

- B+B SmartWorx Inc.

- Red Lion Controls, Inc.

- Westermo Network Technologies AB

- Beckhoff Automation GmbH & Co. KG

- PLANET Technology Corporation

- Rittal GmbH & Co. KG

- Kyland Technology Co., Ltd.

- RuggedCom Inc.

- Xiamen Korenix Technology Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the industrial ethernet switch market size is expected to increase from USD 3.50 billion in 2025 to USD 3.80 billion in 2026 and reach USD 6.00 billion by 2031, growing at a CAGR of 8% over 2026-2031.

This report is Segmented by Management Type (Managed Switches, and Unmanaged Switches), Layer Capability (Layer 2, and Layer 3), Number of Ports (Up To 8 Ports, 9-24 Ports, 25-48 Ports, and More), Data Rate (≤100 Mbps, Gigabit Ethernet, 10 Gigabit Ethernet, and More), End-User Industry (Discrete Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Ethernet Switch Market Trends and Insights

Rapid Expansion of IIoT Deployments

Industrial Internet of Things programs are multiplying Ethernet endpoints in production lines, with industrial Ethernet capturing 76% of new-node installations in 2025. Each smart sensor or edge appliance needs a switch port, and unmanaged daisy chains introduce latency that disrupts 10-50 millisecond control loops. Utilities illustrate the shift; Electricity North West installed rugged switches in United Kingdom substations to stream synchrophasor data at 50 frames per second, traffic that legacy serial links cannot manage. Switch makers now embed IEEE 1588 grandmaster clocks, eliminating standalone timing boxes and trimming bill of materials by roughly 15%. As plant operators see commissioning times fall, demand rises for ports with deterministic forwarding-an anchor trend for the Industrial Ethernet Switch Market.

Rising Demand for Deterministic Networking in Smart Factories

Automotive and semiconductor plants require sub-microsecond synchronization for collaborative robots and vision systems, achievable only with TSN-ready switches. Finalized IEEE 802.1Qbv and 802.1AS standards let devices reserve bandwidth for control traffic, while relegating diagnostics to best-effort queues. European automakers lead adoption after AUTOSAR named Ethernet the in-vehicle backbone in 2024. Siemens updated its SCALANCE XC-300 line in 2025 with IEEE 802.1Qci filtering, insulating networks from rogue traffic.Discrete manufacturers report that TSN shortens commissioning by 30-40%, confirming its pull on Industrial Ethernet Switch Market demand.

High Upfront CAPEX for Ruggedised Switches

Industrial-grade switches with extended temperature ratings and conformal coating cost 200-400% more than commercial gear. A Cisco Industrial Ethernet 5000 with 10 Gigabit uplinks lists at about USD 15,400 against USD 906.50 for an entry-level IE2000, and hazardous-location certifications add USD 500-1,000 per unit. Railway and oil-rig projects need EN 50155 or ATEX compliance, inflating budgets and delaying procurement. Leasing models aim to flatten spending, yet customers remain cautious because obsolescence risk reverts to the buyer if products are discontinued mid-term.

Other drivers and restraints analyzed in the detailed report include:

- Migration from Fieldbus to Ethernet in Process Industries

- Increasing Adoption of Power over Ethernet for Edge Devices

- Lack of Skilled Industrial Networking Personnel

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Managed hardware captured 68.75% of the Industrial Ethernet Switch Market in 2025 and is set to rise at 11.31% CAGR through 2031. Regulatory mandates such as NIS2 oblige operators of essential services to segment networks and maintain audit trails, capabilities only managed devices offer. Process plants prioritize SNMP traps and syslog for centralized monitoring, while discrete lines still use unmanaged units when point-to-point links suffice. "Smart unmanaged" products with read-only dashboards blur boundaries, yet firmware-update requirements in forthcoming Cyber Resilience rules further tilt spending toward fully managed gear. Vendors embedding zero-trust access controls at the port level stand to gain share as end users elevate switches from connectivity devices to critical security assets.

Unmanaged switches retain footholds in machine-mounted clusters where configuration overhead outweighs visibility gains. Rockwell's Stratix 2100, introduced mid-2025, targets this niche with 5- and 8-port variants. However, as patching obligations expand, brownfield plants are replacing still-functional unmanaged units, enlarging the addressable pool for managed platforms and supporting long-run growth of the Industrial Ethernet Switch Market size for this segment.

Layer 2 products held 61.40% share in 2025, yet Layer 3 switches are advancing at 11.76% CAGR as edge computers need inter-VLAN routing for micro-segments. Utilities adopt Layer 3 to carry routed GOOSE messages per IEC 61850 Edition 2.1, letting substations exchange status across wide territories without multicast flooding. Belden's XTran line, launched in 2025, exemplifies the trend by combining routed GOOSE with MPLS and SD-WAN.

Cost barriers are falling; Broadcom and Marvell chips trimmed 20% since 2024, shrinking the premium between Layer 2 and Layer 3 products. As discrete manufacturers isolate production zones with ACLs on-box, Layer 3 becomes the default upgrade path, boosting the Industrial Ethernet Switch Market size for routing-capable hardware and narrowing appeal for pure Layer 2 devices.

Geography Analysis

Asia-Pacific led the Industrial Ethernet Switch Market with 35.12% share in 2025 and is projected to post a 9.89% CAGR to 2031. India's automation sector is set to climb from USD 3.64 billion in 2026 to USD 13.65 billion by 2034, fueling switch purchases in greenfield factories. China's EV and semiconductor clusters require TSN-capable gear for +-1 microsecond sync, while Japanese machine-tool builders embed 10 Gigabit switches inside CNC controllers, trimming cabinet footprints by 30%. South Korean shipyards deploy marine-rated fiber backbones to replace proprietary serial lines, and Australian utilities migrate to IEC 61850 Edition 2.1 Layer 3 architectures. Regional labor cost advantages shorten payback periods despite rugged-hardware premiums, and government smart-manufacturing incentives pull forward replacement cycles.

North America holds a strong position, buoyed by reshoring that expands automotive and medical-device capacity. The U.S. CISA's 2025 guidance on network segmentation compels utilities and transit agencies to retire unmanaged equipment. CenterPoint Energy's 2025 pipeline backbone cut OPEX by 25% after converging leak-detection telemetry on Ethernet. Canadian mines deploy Class I Division 1 switches tolerant to -40 °C, and Mexican tier-1 suppliers wait 20 weeks for TSN-certified hardware amid ASIC shortages. The region confronts a deep skills shortage, extending median hiring to 120 days and nudging buyers to cloud-managed devices.

Europe commands substantial share thanks to automotive and chemical producers enforcing TSN. NIS2, effective October 2024, pushes managed switches in utilities, transit, and health care. Germany's Industry 4.0 drive accelerates OPC UA over TSN adoption, with Beckhoff embedding switch fabrics inside control platforms. Electricity North West connected phasor meters via rugged hardware in 2025, and France's railways standardize on EN 50155 devices with 20 millisecond ring recovery. Lead times for 28-65 nm ASICs top 30 weeks in 2026, spotlighting supply-chain constraints even as smart-grid and factory-modernization budgets expand across Italy and Spain.

- Siemens AG

- Schneider Electric SE

- Rockwell Automation, Inc.

- Belden Inc.

- Moxa Inc.

- Advantech Co., Ltd.

- Phoenix Contact GmbH & Co. KG

- Hirschmann Automation and Control GmbH

- Cisco Systems, Inc.

- Eaton Corporation plc

- ABB Ltd.

- B+B SmartWorx Inc.

- Red Lion Controls, Inc.

- Westermo Network Technologies AB

- Beckhoff Automation GmbH & Co. KG

- PLANET Technology Corporation

- Rittal GmbH & Co. KG

- Kyland Technology Co., Ltd.

- RuggedCom Inc.

- Xiamen Korenix Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Rapid Expansion of IIoT Deployments

- 4.1.2 Rising Demand for Deterministic Networking in Smart Factories

- 4.1.3 Migration from Fieldbus to Ethernet in Process Industries

- 4.1.4 Increasing Adoption of Power over Ethernet for Edge Devices

- 4.1.5 Compliance Requirements for Time-Sensitive Networking (TSN)

- 4.1.6 Surge in Cyber-Physical Security Investments Post-2025

- 4.2 Market Restraints

- 4.2.1 High Upfront CAPEX for Ruggedised Switches

- 4.2.2 Lack of Skilled Industrial Networking Personnel

- 4.2.3 Legacy Equipment Integration Challenges

- 4.2.4 Supply Chain Volatility of Specialized ASICs

- 4.3 Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Management Type

- 5.1.1 Managed Switches

- 5.1.2 Unmanaged Switches

- 5.2 By Layer Capability

- 5.2.1 Layer 2

- 5.2.2 Layer 3

- 5.3 By Number of Ports

- 5.3.1 Up to 8 Ports

- 5.3.2 9-24 Ports

- 5.3.3 25-48 Ports

- 5.3.4 More than 48 Ports

- 5.4 By Data Rate

- 5.4.1 <=100 Mbps

- 5.4.2 Gigabit Ethernet

- 5.4.3 10 Gigabit Ethernet

- 5.4.4 40 Gigabit and Above

- 5.5 By End-User Industry

- 5.5.1 Discrete Manufacturing

- 5.5.2 Process Industries

- 5.5.3 Transportation and Logistics

- 5.5.4 Energy and Utilities

- 5.5.5 Government and Smart Cities

- 5.5.6 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Schneider Electric SE

- 6.4.3 Rockwell Automation, Inc.

- 6.4.4 Belden Inc.

- 6.4.5 Moxa Inc.

- 6.4.6 Advantech Co., Ltd.

- 6.4.7 Phoenix Contact GmbH & Co. KG

- 6.4.8 Hirschmann Automation and Control GmbH

- 6.4.9 Cisco Systems, Inc.

- 6.4.10 Eaton Corporation plc

- 6.4.11 ABB Ltd.

- 6.4.12 B+B SmartWorx Inc.

- 6.4.13 Red Lion Controls, Inc.

- 6.4.14 Westermo Network Technologies AB

- 6.4.15 Beckhoff Automation GmbH & Co. KG

- 6.4.16 PLANET Technology Corporation

- 6.4.17 Rittal GmbH & Co. KG

- 6.4.18 Kyland Technology Co., Ltd.

- 6.4.19 RuggedCom Inc.

- 6.4.20 Xiamen Korenix Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年乙太網路供電 (PoE) 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)管理型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)非網管型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年乙太網路供電 (PoE) 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)管理型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)非網管型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)