|

市場調查報告書

商品編碼

2063698

非網管型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Unmanaged Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

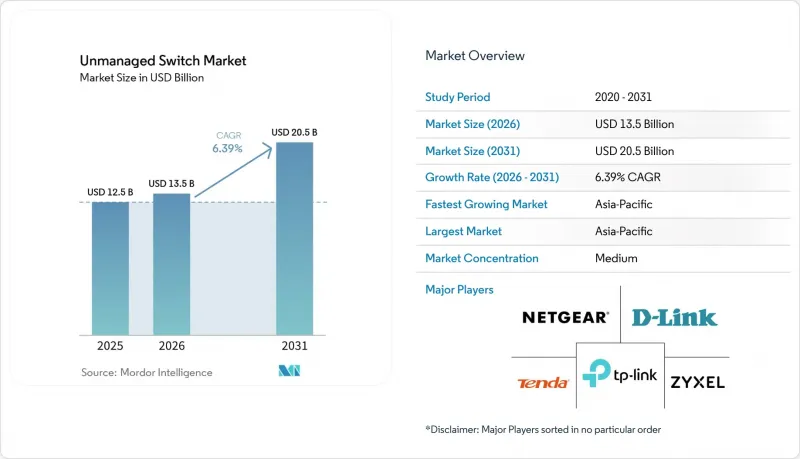

據 Mordor Intelligence 稱,2025 年非管理型交換機市值為 125 億美元,預計到 2031 年將達到 205 億美元,而 2026 年為 135 億美元,預測期(2026-2031 年)的複合年成長率為 6.39%。

本報告根據連接埠數量(5個或以下、6-8個連接埠、9-16個連接埠、17-24個連接埠、24個或以上)、PoE功能(非PoE、PoE、PoE+、PoE++)、部署環境(住宅/家庭辦公室、中小企業、企業/園區、工業/加固型、資料中心邊緣分類)和區域(北美)進行分類。市場預測以美元(USD)計價。

全球非網管交換器市場趨勢及洞察

中小企業對經濟實惠的即插即用網路的需求激增。

對價格敏感的小規模企業很少會聘請專職IT人員,因此他們傾向於選擇無需配置、可自動協商連接埠速度的非託管設備。典型的8埠Gigabit零售價遠低於100美元,即使平均每位使用者使用的設備數量增加到三台,這個價格仍然很有吸引力。零接觸部署方案尤其適用於需要頻繁重新佈線的臨時零售亭和共享辦公空間。在東南亞的出口中心,當地的增值轉售商正在將低成本交換器和雲端路由器捆綁銷售,以加速首次涉足電子商務的企業實現數位轉型。混合辦公模式的普及進一步增加了分店的連接需求,因為員工需要在家庭和辦公室之間切換,這也使得緊湊外形規格產品需要持續供應。

擴展以影像為中心的監控基礎設施需要 PoE(乙太網路供電)。

全球從類比CCTV向高清IP攝影機的轉變與乙太網路供電(PoE)預算直接相關,因為所有攝影機都需要透過同一根網路線同時傳輸資料和電力。新型工業級PoE++交換器每個連接埠可提供高達90瓦的功率,足以支援高速公路和關鍵基礎設施上配備紅外線功能的雲台攝影機的運作。對於便利商店和市政停車場等小規模場所,4端口和8端口非網管型PoE交換機就足夠了,電工而非IT工程師即可快速安裝攝影機。隨著分析功能整合到攝影機內部,處理器負載增加,功耗上升,加速了從傳統802.3af平台向802.3bt硬體的升級。

低成本管理型交換器功能的擴展正在蠶食非管理型交換器的銷售量。

到2025年,一台48埠智慧型管理型交換器的售價將低於300美元。這款交換器整合了VLAN標記、SNMP監控和雲端控制面板等功能——這些功能曾經被認為是企業級高階產品才具備的。 Zyxel的XMG2230系列將於2026年上市,它將多Gigabit速度和2400瓦的PoE供給能力整合到一款面向中小企業的產品中,同時保持了直覺的基於應用程式的配置方式。 16-24埠交換器的買家發現,省略管理功能並不能節省太多成本,這導致一般辦公室中非管理型產品的銷售量下降。供應商正在透過可透過旋轉開關配置的混合模式交換器來解決這個問題,但這種折衷方案可能會蠶食產品系列中兩個細分市場的佔有率。

細分市場分析

2025年,6至8埠非網管型交換器市場仍將佔據主導地位。這是因為零售店、診所和家庭辦公室通常只需要不到10台有線設備。緊湊的塑膠機殼和壁掛式電源設計降低了部署成本,進一步增強了其銷售優勢。同時,擁有24個以上連接埠的底盤式產品(大多為機架式)正受惠於資料中心邊緣和工業控制面板的部署,這些面板每個機架可聚合數十個感測器。多Gigabit上行鏈路和SFP+插槽正被引入到此類產品中,無需遷移到管理型軟體堆疊即可實現無縫的主幹網路連接。

9-24埠交換器的需求正面臨來自功能豐富的智慧型管理型交換器的嚴峻挑戰。雖然這些產品目前在零售價上僅略高一些,但對於那些優先考慮頻寬而非連接埠分類的買家來說,D-Link新推出的2.5Gigabit交換器產品線或許值得考慮。製造商們正努力透過提供無風扇設計、整合電源以及用於節能模式的前面板DIP控制來維持市場佔有率。因此,隨著智慧園區中建築邊緣聚合採用零接觸配置,預計到2031年,超高密度非網管型交換器的市佔率將成長最為迅速。

區域分析

預計到2025年,亞太地區將以33.85%的市佔率領跑非網管交換器市場,並繼續以7.56%的複合年成長率超越全球平均水平,這主要得益於製造商將業務拓展至中國當地以外的地區。在越南南北工業走廊、印度生產連結獎勵計畫區和馬來西亞柔佛電子產業叢集,每季都有數千個總合級乙太網路節點部署。同時,首爾和新加坡的智慧城市試點計畫正在路燈和交通號誌中安裝非網管PoE接線盒,在無線網路普及率不斷提高的情況下,進一步提升連接埠密度。

北美仍然是重要的市場貢獻者,但由於低成本託管產品的湧入,其在開放式辦公室和共同工作空間領域面臨著市場佔有率蠶食的挑戰。儘管如此,5埠和8埠桌上型設備的持續升級週期得益於混合辦公模式帶來的家庭環境升級,而私部門在PoE++網路基地台升級的支出也維持了教育產業的需求。採用光纖到府(FTTR)層壓板的企業園區正在樓層間的機櫃中部署24埠或更大容量的機架式底盤,並進行銅纜端接。

在歐洲市場,監管需求體現在修訂後的《建築能源性能指令》(EPBD)中,該指令強制要求電動車充電器、電錶和感測器採用結構化佈線。經濟高效的非網管型交換器的市場推廣,滿足了商業設施維修中逐層整合的需求,這些設施通常已在雲端服務上部署了集中式建築管理軟體。在中東和非洲,成長主要集中在變電站、CCTV密集的公共安全網路以及油田遙測棚等領域,這些領域都需要IP67防護等級的機殼,並能在各種溫度環境下運作。在南美洲,受巴西零售連鎖店和墨西哥加工廠的推動,隨著供應限制的緩解和外匯波動的減弱,非網管型PoE設備的替換正在逐步推進。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 中小企業對經濟實惠的即插即用網路的需求日益成長。

- 擴展以影像為中心的監控基礎設施需要乙太網路供電 (PoE)

- 混合辦公模式的趨勢正在推動家庭辦公設備的更新換代。

- 中型自動化生產線向工業乙太網過渡

- 政府強制要求智慧建築採用低功耗有線骨幹網路。

- 「光纖到房間」部署的加速推動了邊緣交換器的更新換代。

- 市場限制因素

- 低成本管理型交換器功能的增強正在蠶食非管理型交換器的銷售量。

- 由於流量分段不足而導致的安全漏洞

- Wi-Fi 6E 和 7 將抑制 SOHO 環境中邊緣連接埠的成長。

- 半導體供應中斷導致物料清單 (BOM) 成本上升。

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 逐個港口

- 5個或更少端口

- 6-8個端口

- 9-16個端口

- 17-24個端口

- 24個或更多端口

- 按 PoE 容量

- 非PoE

- PoE(802.3af)

- PoE+(802.3at)

- PoE++(802.3bt)

- 按部署環境

- 住宅和家庭辦公室

- 小型企業

- 企業和校園

- 工業和重型

- 資料中心邊緣

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Netgear Inc.

- TP-Link Corporation Limited

- D-Link Corporation

- Zyxel Communications Corporation

- Shenzhen Tenda Technology Co., Ltd.

- PLANET Technology Corporation

- TRENDnet, Inc.

- Buffalo Inc.

- Linksys Holdings, Inc.

- Antaira Technologies, LLC

- ORing Industrial Networking Corp.

- Moxa Inc.

- Kyland Technology Co., Ltd.

- Phoenix Contact GmbH and Co. KG

- Siemens AG

- Belden Inc.

- Allied Telesis Holdings KK

- Ubiquiti Inc.

- MikroTikls SIA

- Ruijie Networks Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the unmanaged switch market size was valued at USD 12.50 billion in 2025 and is estimated to grow from USD 13.50 billion in 2026 to reach USD 20.50 billion by 2031, at a CAGR of 6.39% during the forecast period (2026-2031).

This report is Segmented by Port Count (5 Ports and Below, 6-8 Ports, 9-16 Ports, 17-24 Ports, and Above 24 Ports), Poe Capability (Non-PoE, Poe, Poe+, and PoE++), Deployment Environment (Residential and Home Office, Small and Medium Business, Enterprise and Campus, Industrial and Rugged, and Data Center Edge), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Unmanaged Switch Market Trends and Insights

Surging SMB Demand For Cost-Effective Plug-And-Play Networking

Price-sensitive small firms rarely allocate dedicated IT staff, so they adopt unmanaged devices that negotiate port speeds automatically and require no configuration. Typical 8-port Gigabit models retail well under USD 100, a figure that remains compelling even as devices per user rise to three endpoints on average. Zero-touch installation supports pop-up retail kiosks and coworking floors where cabling must be re-routed frequently. In Southeast Asian export hubs, local value-added resellers bundle low-cost switches with cloud routers to accelerate digital onboarding for first-time e-commerce merchants. Hybrid work routines further elevate branch connectivity needs as employees rotate between home and office desks, sustaining replenishment cycles for compact form factors.

Expansion Of Video-Centric Surveillance Infrastructure Requiring PoE

The global shift from analog CCTV to high-resolution IP cameras ties directly to Power over Ethernet budgets because every camera needs both data and power over the same cable. New industrial PoE++ switches now deliver up to 90 watts per port, supporting infrared-equipped PTZ units on highways and critical infrastructure. For small installations such as convenience stores or municipal parking lots, 4- and 8-port unmanaged PoE models remain adequate, enabling electricians, not IT engineers, to hang cameras quickly. As analytics migrate onto cameras themselves, higher processor loads raise wattage draw, which in turn accelerates refresh from legacy 802.3af platforms toward 802.3bt hardware.

Feature Creep Of Low-Cost Managed Switches Cannibalizing Unmanaged Sales

Smart-managed models dipped below USD 300 for 48 ports in 2025, bundling VLAN tagging, SNMP monitoring, and cloud dashboards that once carried enterprise-grade premiums. Zyxel's XMG2230 series, released in 2026, layers multi-gigabit speeds and 2,400-watt PoE budgets onto SMB offerings while retaining intuitive app-based setup. Buyers in 16- to 24-port bands increasingly perceive minimal savings when foregoing management, eroding unmanaged volumes in mainstream offices. Vendors answer with hybrid profiles configured by rotary switches, yet this middle ground risks cannibalizing both sides of the portfolio.

Other drivers and restraints analyzed in the detailed report include:

- Home-Office Upgrades Driven By Hybrid Work Trends

- Industrial Ethernet Migration In Mid-Tier Automation Lines

- Security Vulnerabilities From Lack Of Traffic Segmentation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The unmanaged switch market size for 6-8 port models remained dominant in 2025 as shops, clinics, and home offices typically require fewer than ten wired devices. Compact plastics enclosures and wall-wart power designs keep acquisition costs low, reinforcing volume leadership. Conversely, above-24-port chassis class products, often rack-mounted, benefit from data-center edge and industrial control-panel rollouts that aggregate dozens of sensors per rack. Multi-gigabit uplinks and SFP+ cages are entering this tier, enabling seamless spine connections without stepping up to managed software stacks.

Demand in 9- to 24-port bands faces stiff headwinds from feature-rich smart-managed alternatives that now retail only slightly higher, yet buyers focused purely on bandwidth, not segmentation, may consider D-Link's newly released 2.5-gigabit unmanaged lines. Manufacturers strive to retain share by offering fanless thermal designs, integrated power supplies, and front-panel DIP control of energy-saving modes. Consequently, the unmanaged switch market share for ultra-dense categories is projected to climb fastest through 2031 as building-side edge aggregation embraces zero-touch provisioning in smart campuses.

Geography Analysis

Asia-Pacific led unmanaged switch market share at 33.85% in 2025 and continues to outpace global averages at a 7.56% CAGR as manufacturers diversify beyond mainland China. Vietnam's north-south industrial corridor, India's production-linked incentive districts, and Malaysia's Johor electronics clusters collectively commission thousands of machine-level Ethernet nodes each quarter. In parallel, smart-city pilots in Seoul and Singapore install unmanaged PoE junction boxes at lamp posts and traffic signals, boosting port densities despite rising wireless penetration.

North America remains a sizeable contributor yet confronts cannibalization from low-cost managed entrants in open-plan offices and co-working venues. Still, hybrid-work home upgrades support ongoing refresh cycles for five- and eight-port desktop units, while private-sector spending on PoE++ access-point refresh sustains demand in the education vertical. Enterprise campuses that adopt fiber-to-the-room laminates deploy above-24-port rack-mount chassis at floor aggregation closets to terminate copper runs.

Europe's market reflects regulatory pull as the recast Energy Performance of Buildings Directive prescribes structured cabling for EV charging, meters, and sensors. Cost-effective unmanaged switch market deployments satisfy per-floor consolidation needs in commercial retrofits where centralized building-management software already resides in cloud services. Middle East and Africa growth gravitates toward utility substations, CCTV-heavy public-safety grids, and oilfield telemetry huts, all environments that require IP67 casings and extended temperature operations. South America, led by Brazil's retail chains and Mexico's maquiladora factories, gradually embraces unmanaged PoE refresh as supply constraints ease and currency headwinds stabilize.

- Netgear Inc.

- TP-Link Corporation Limited

- D-Link Corporation

- Zyxel Communications Corporation

- Shenzhen Tenda Technology Co., Ltd.

- PLANET Technology Corporation

- TRENDnet, Inc.

- Buffalo Inc.

- Linksys Holdings, Inc.

- Antaira Technologies, LLC

- ORing Industrial Networking Corp.

- Moxa Inc.

- Kyland Technology Co., Ltd.

- Phoenix Contact GmbH and Co. KG

- Siemens AG

- Belden Inc.

- Allied Telesis Holdings K.K.

- Ubiquiti Inc.

- MikroTikls SIA

- Ruijie Networks Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Surging SMB Demand for Cost-Effective Plug-and-Play Networking

- 4.1.2 Expansion of Video-Centric Surveillance Infrastructure Requiring PoE

- 4.1.3 Home-Office Upgrades Driven by Hybrid Work Trends

- 4.1.4 Industrial Ethernet Migration in Mid-Tier Automation Lines

- 4.1.5 Government Smart-Building Mandates Embracing Low-Power Wired Backbones

- 4.1.6 Accelerated Fiber-to-the-Room Deployments Creating Edge Switch Refresh

- 4.2 Market Restraints

- 4.2.1 Feature Creep of Low-Cost Managed Switches Cannibalising Unmanaged Sales

- 4.2.2 Security Vulnerabilities From Lack of Traffic Segmentation

- 4.2.3 Wi-Fi 6E and 7 Reducing Edge Port Growth in SOHO

- 4.2.4 Semiconductor Supply Disruptions Elevating BOM Costs

- 4.3 Industry Supply-Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Port Count

- 5.1.1 5 Ports and Below

- 5.1.2 6 - 8 Ports

- 5.1.3 9 - 16 Ports

- 5.1.4 17 - 24 Ports

- 5.1.5 Above 24 Ports

- 5.2 By PoE Capability

- 5.2.1 Non-PoE

- 5.2.2 PoE (802.3af)

- 5.2.3 PoE+ (802.3at)

- 5.2.4 PoE++ (802.3bt)

- 5.3 By Deployment Environment

- 5.3.1 Residential and Home Office

- 5.3.2 Small and Medium Business

- 5.3.3 Enterprise and Campus

- 5.3.4 Industrial and Rugged

- 5.3.5 Data Center Edge

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Nigeria

- 5.4.6.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Netgear Inc.

- 6.4.2 TP-Link Corporation Limited

- 6.4.3 D-Link Corporation

- 6.4.4 Zyxel Communications Corporation

- 6.4.5 Shenzhen Tenda Technology Co., Ltd.

- 6.4.6 PLANET Technology Corporation

- 6.4.7 TRENDnet, Inc.

- 6.4.8 Buffalo Inc.

- 6.4.9 Linksys Holdings, Inc.

- 6.4.10 Antaira Technologies, LLC

- 6.4.11 ORing Industrial Networking Corp.

- 6.4.12 Moxa Inc.

- 6.4.13 Kyland Technology Co., Ltd.

- 6.4.14 Phoenix Contact GmbH and Co. KG

- 6.4.15 Siemens AG

- 6.4.16 Belden Inc.

- 6.4.17 Allied Telesis Holdings K.K.

- 6.4.18 Ubiquiti Inc.

- 6.4.19 MikroTikls SIA

- 6.4.20 Ruijie Networks Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年乙太網路供電 (PoE) 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)工業乙太網網路交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)管理型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年乙太網路供電 (PoE) 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)工業乙太網網路交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)管理型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)