|

市場調查報告書

商品編碼

2063697

管理型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Managed Switch - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

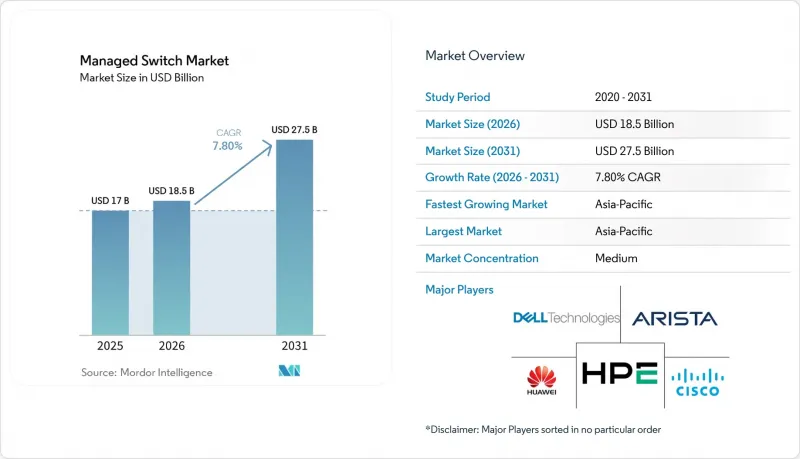

根據 Mordor Intelligence 預測,管理型交換器市場規模將從 2025 年的 170 億美元和 2026 年的 185 億美元成長到 2031 年的 275 億美元,2026 年至 2031 年的複合年成長率為 7.8%。

本報告按管理功能(託管式和智慧/輕量託管式)、連接埠速度(快速乙太網路、Gigabit乙太網路、Gigabit乙太網路、25/40Gigabit乙太網路以及 100Gigabit乙太網路及以上)、管理架構(設備端管理、雲端管理和混合管理)、最終用戶產業(IT 與通訊、銀行、金融服務和保險 (BFSI)、政府與國防管理)以及其他地區進行分類和保險 (BFSI)、政府與國防產業。市場預測以美元 (USD) 為單位。

全球管理型交換器市場趨勢與洞察

向Gigabit和多Gigabit園區網路的過渡正在加速。

隨著 Wi-Fi 6E 和 Wi-Fi 7網路基地台逐漸飽和傳統的Gigabit上行鏈路頻寬,企業被迫升級其基礎設施。喬治城大學計劃在 2025 年前更換 4000 個網路基地台,並將其分發交換器升級為多Gigabit型號,以確保每個網路基地台達到 5 Gbps 的頻寬。類似的瓶頸也出現在企業和政府園區,多個 Wi-Fi 6E 用戶端同時傳輸 4K影片或同步大規模資料集。網路團隊意識到,逐個插槽升級已不足以解決問題,因此他們正在用提供服務品質 (QoS) 和精細監控功能的管理型設備替換整個交換器堆疊。管理型交換器更具經濟優勢,因為非管理型設備無法優先處理對延遲敏感的流量,也無法提供每個連接埠的利用率資訊。因此,高等教育機構、企業總部和公共設施對 2.5 GbE、5 GbE 和 10 GbE 接入交換機的需求正在加速成長。

從邊緣到雲端的安全需求推動了託管交換器的普及。

零信任架構將檢查和分段轉移到網路的每一個躍點,使存取交換器轉變為執行引擎。 2024 年,Fortinet 透過將防火牆規則直接整合到 FortiSwitch 硬體中,實現了微隔離,因此無需透過集中式設備進行環回連接。 PCI-DSS 和 HIPAA 等框架要求隔離敏感流量,這使得金融服務和醫療保健提供者成為早期採用者。授權功能

專用交換ASIC的供應鏈波動

博通在企業和資料中心交換器通用晶片市場佔據相當大的佔有率,這意味著任何生產中斷都會對所有供應商產生影響。谷歌已將其未來的設計轉向使用Marvell的晶片,這一變化在Marvell的2025會計年度財報中披露,凸顯了客戶對依賴單一供應商的擔憂。台積電等晶圓代工廠3nm和5nm製程的晶圓產能緊張,導致交換器ASIC的前置作業時間超過52週。沒有獲得產能配額的中小型供應商被迫要么交付低效、過時的晶片,要么推遲產品發布並失去市場佔有率。雖然一級OEM廠商可以透過預付款來確保晶圓代工廠的生產配額,但更廣泛的管理型交換機市場正經歷間歇性的供不應求,這阻礙了收入累計並推高了庫存成本。

細分市場分析

預計到2025年,憑藉其先進的路由和安全功能,企業級平台將佔據64.8%的託管交換器市場佔有率。智慧輕量級託管設備預計將以10.42%的複合年成長率成長,這得益於雲端控制器能夠隱藏複雜性,使非專業用戶也能在幾分鐘內部署分店。隨著新型智慧平台採用高階ASIC晶片,以更低的成本實現線速效能,企業級設備在託管交換器市場的主導地位正在縮小。供應商透過捆綁多年雲端訂閱、將資本支出轉化為營運支出以及提高預算可預測性等方式,使合約條款更具吸引力。然而,客戶在雲端域之間遷移時會面臨鎖定問題,因為所有交換器都需要重新配置,員工也必須重新學習工作流程。在預測期內,交換器數量少於50台的企業預計將直接遷移到雲端優先的智慧型設備,而財富1000強企業可能仍會傾向於本地部署,以獲得精細化的可視性。

二線供應商正透過提供產業專用的韌體(例如預先配置了製造協議的強大智慧交換機)來開拓細分市場。因此,功能廣度和產業專用深度在採購決策中變得越來越重要。在管理型交換器產業,我們將看到一種層級構造通路策略:全球OEM廠商將專注於全端解決方案,而區域專家則將滿足細粒度的合規性和環境要求。

即使到了2025年,Gigabit設備仍佔據管理型交換器市場46.35%的佔有率。這是因為大多數筆記型電腦和物聯網感測器的最大通訊速度為1Gbps。然而,隨著資料中心東西向流量的激增,預計100GbE及以上交換器的市佔率將以9.51%的複合年成長率快速成長。 Arista於2025年發布的800GbE 7060X6交換機,在一個框架單位內整合了64個端口,與上一代產品相比,能源效率提升了40%。早期採用者是超大規模資料中心業者公司,他們正在訓練大規模語言模型,以超高速交換梯度資訊。光學模組的成本(每個模組超過1萬美元)阻礙了其廣泛應用,因此許多公司可能會在標準最終確定後遷移到1.6Tbps的速率。中型企業買家在選擇機架式連接方案時,仍傾向於選擇 10 GbE 和 25 GbE,以平衡成本、功耗和容量。因此,高階管理型交換器市場的擴張在一定程度上被中等頻寬需求的停滯所抵消。

儘管隨著5奈米製程良率的提高和矽光電帶來的組件價格下降,這一差距應該會逐漸縮小,但財務長們仍在仔細權衡每Gigabit的成本。供應商們不僅透過吞吐量來區分彼此,還透過即時擁塞控制、人工智慧工作負載的抖動抑制以及用於可觀測性堆疊的流遙測功能來實現差異化。

區域分析

預計到2025年,亞太地區將引領管理型交換器市場,佔34.1%的市場佔有率,並將以9%的複合年成長率持續成長至2031年。 2025年重點關注的19.4吉瓦資料中心建設項目主要集中在馬來西亞柔佛州和印度孟買,這將支撐對脊式交換機和機架頂部交換機的訂單。印度的「BharatNet三期」計畫投資14兆盧比(約161億美元),將光纖網路延伸至21.4萬個叢集,所有站點均配備對稱Gigabit管理型接取交換器。印度和越南的資料本地化法規迫使超大規模資料中心業者資料中心營運商建設本土設施,增加了對高速聚合設備的需求。同時,供應鏈多元化正推動製造商進軍越南和馬來西亞,這些地區新建的智慧工廠從一運作就採用支援TSN的工業交換機。

北美位居第二,這得益於寬頻股權、接入和配置(BEAD) 計劃的支援。該計劃投資 425 億美元用於高等教育機構的校園現代化改造和農村地區的光纖基礎設施建設。美國企業正在採用多Gigabit供電 (PoE) 技術來支援 Wi-Fi 7 設備和物聯網感測器,從而實現穩定的升級週期。歐洲則受惠於「連接歐洲數位設施」計劃,該計劃已撥款 8.65 億歐元(約 9.75 億美元)用於骨幹網路升級,這些升級依賴於具備先進光纖通訊和路由功能的管理型交換機。

在中東,受主權雲端指南的推動,超大規模投資正在激增,其中包括AWS計畫在沙烏地阿拉伯投資超過50億美元。這些基礎設施項目傾向於採用具備高級加密和合規報告功能的設備。南美和非洲雖然規模仍然較小,但隨著通訊業者部署光纖回程傳輸以及各國政府優先考慮數位包容性,這些地區正呈現穩定成長的態勢。供應商在亞太地區面臨價格壓力,在中東地區面臨高利潤率,而在新興市場則面臨較長的付款週期,因此需要採取多樣化的打入市場策略。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加速向Gigabit和多Gigabit園區網路過渡

- 從邊緣到雲端的安全需求推動了託管交換器的普及。

- 工業乙太網在智慧工廠的普及

- 融合網路中對乙太網路供電(PoE)的需求日益成長。

- 政府主導的寬頻現代化計劃

- 透過人工智慧最佳化的網路管理平台降低營運成本

- 市場限制因素

- 專用開關ASIC的供應鏈波動

- 中小企業對無線優先架構的興趣日益濃厚

- 網路安全人員短缺阻礙了複雜交換機的部署。

- 超大規模資料中心業者。

- 產業生態系分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 由產能管理

- 託管(企業級)

- 智慧/輕量級管理(中小企業/邊緣)

- 連接埠速度

- 快速乙太網路(100 Mb/s 或更低)

- Gigabit乙太網路(1 Gb/s)

- 10Gigabit以太網

- 25/40Gigabit以太網

- 100Gigabit乙太網路或更高

- 託管架構

- 在設備上(CLI/Web)

- 雲端管理

- 混合

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 製造業

- 衛生保健

- 教育

- 政府/國防

- 能源公用事業

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Hewlett Packard Enterprise Company

- Arista Networks, Inc.

- Huawei Technologies Co., Ltd.

- Extreme Networks, Inc.

- Dell Technologies Inc.

- D-Link Corporation

- TP-Link Technologies Co., Ltd.

- Netgear, Inc.

- Fortinet, Inc.

- ZTE Corporation

- Edgecore Networks Corporation

- Allied Telesis Holdings KK

- Avaya LLC

- MikroTik SIA

- H3C Technologies Co., Limited

- Lenovo Group Limited

- Ubiquiti Inc.

- ALE International SAS(Alcatel-Lucent Enterprise)

第7章 市場機會與未來展望

According to Mordor Intelligence, the managed switch market size is projected to expand from USD 17 billion in 2025 and USD 18.5 billion in 2026 to USD 27.5 billion by 2031, registering a CAGR of 7.8% between 2026 to 2031.

This report is Segmented by Managed Capability (Managed, and Smart/Light Managed), Port Speed (Fast Ethernet, Gigabit Ethernet, 10 Gigabit Ethernet, 25/40 Gigabit Ethernet, and ≥100 Gigabit Ethernet), Management Architecture (On-Device, Cloud-Managed, and Hybrid), End User Industry (IT and Telecom, BFSI, Government and Defense, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Managed Switch Market Trends and Insights

Accelerated Migration to Gigabit and Multi-Gigabit Campus Networks

Enterprises are in the midst of a forced refresh because Wi-Fi 6E and Wi-Fi 7 access points saturate legacy gigabit uplinks. Georgetown University swapped 4,000 access points in 2025 and refreshed its distribution switches with multi-gigabit models to sustain 5 Gbps per access point. Similar bottlenecks are showing up in corporate and government campuses where multiple Wi-Fi 6E clients concurrently stream 4K video or sync large datasets. Network teams find that slot-by-slot upgrades are insufficient, so entire switch stacks are replaced with managed devices supporting quality-of-service and granular monitoring. The economics favor managed switch market deployments because unmanaged units cannot prioritize latency-sensitive traffic or expose per-port utilization. As a result, demand for 2.5 GbE, 5 GbE and 10 GbE access switches is accelerating across higher education, corporate headquarters and public-sector buildings.

Edge-to-Cloud Security Requirements Driving Managed Switch Adoption

Zero-trust architecture shifts inspection and segmentation into every hop of the network, turning access switches into enforcement engines. Fortinet embedded its firewall rules directly into FortiSwitch hardware in 2024, enabling micro-segmentation without hair-pinning traffic through centralized appliances. Financial-services and healthcare operators are early adopters because frameworks such as PCI-DSS and HIPAA require sensitive flows to remain isolated. Managed switches equipped with posture assessment can quarantine non-compliant devices in real time and feed telemetry to security information and event-management tools. This moves the managed switch market beyond basic connectivity toward an active security role, which increases attach rates for licenses and maintenance contracts. Vendors that integrate analytics and automation gain an advantage as enterprises seek platforms that merge networking and security skill sets.

Supply Chain Volatility for Specialized Switching ASICs

Broadcom commands most of the merchant silicon in enterprise and data-center switches, so any production hiccup reverberates across vendors. Google moved future designs to Marvell silicon, a shift disclosed in Marvell's fiscal 2025 earnings, highlighting customer concern about dependence on a single supplier. Tight 3-nm and 5-nm wafer capacity at foundries such as TSMC has pushed lead times for switching ASICs beyond 52 weeks. Smaller vendors without secured allocations either ship older, less efficient chips or delay launches, surrendering share. While tier-one OEMs can pre-pay and lock foundry slots, the broader managed switch market faces intermittent shortages that impede revenue recognition and inflate inventory costs.

Other drivers and restraints analyzed in the detailed report include:

- Industrial Ethernet Expansion in Smart Factories

- Rising Demand for Power over Ethernet in Converged Networks

- Growing Preference for Wireless-First Architectures in SMBs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Enterprise-grade platforms held 64.8% of the managed switch market in 2025 on the strength of deep routing and security features. Smart and light managed devices are on track for a 10.42% CAGR thanks to cloud controllers that hide complexity and let non-specialists roll out branch offices in minutes. The managed switch market size advantage enjoyed by enterprise gear narrows as newer smart platforms adopt high-end ASICs, delivering line-rate performance at lower cost. Vendors sweeten deals by bundling multiyear cloud subscriptions, converting capital spend to operating expense and improving budget predictability. However, customers face lock-in when migrating between cloud domains because every switch needs re-provisioning and staff must relearn workflows. Over the forecast, organizations with fewer than 50 switches are expected to jump straight to cloud-first smart devices, while Fortune 1000 enterprises continue to favor on-premises control for granular visibility.

Second-tier suppliers are carving niches by offering vertical-specific firmware, for example, ruggedized smart switches pre-configured for manufacturing protocols. As a result, procurement decisions increasingly weigh both feature breadth and vertical depth. The managed switch industry is likely to witness a two-tier channel strategy: global OEMs focus on full-stack solutions, and regional specialists address compliance or environmental nuances.

Gigabit devices still comprised 46.35% of the managed switch market share in 2025 because most laptops and IoT sensors max out at 1 Gbps. Yet switches rated at 100 GbE and higher are forecast to sprint at a 9.51% CAGR as east-west traffic inside data centers mushrooms. Arista's 800 GbE 7060X6, launched in 2025, delivers 64 ports in a single rack unit, achieving 40% better power efficiency than its prior generation. Early adopters are hyperscalers training large language models that exchange gradients at extreme speeds. Optics cost, north of USD 10,000 per module, restrains broader uptake, so many enterprises will leapfrog to 1.6 Tbps once standards firm up. Mid-tier buyers remain on 10 GbE and 25 GbE for top-of-rack connections because they balance cost, power and capacity. Consequently, the managed switch market size expansion at the high end is offset partly by plateauing demand in mid-range speeds.

Component price declines, driven by 5 nm yields and silicon photonics, should gradually close the gap, yet CFOs still weigh the dollar per delivered gigabit carefully. Vendors differentiate through real-time congestion control, reduced jitter for AI workloads and flow-telemetry hooks for observability stacks rather than raw throughput alone.

Geography Analysis

Asia-Pacific led with 34.1% of the managed switch market in 2025 and is forecast to post a 9% CAGR through 2031. A 19.4-GW data-center construction pipeline spotlighted in 2025, concentrated in Johor, Malaysia and Mumbai, India, underpins orders for spine and top-of-rack platforms. India's BharatNet Phase 3, funded at INR 1.4 lakh crore (USD 16.1 billion), is extending fiber to 214,000 village clusters, all terminating in symmetrical-gigabit managed access switches. Data-localization statutes in India and Vietnam prompt hyperscalers to build domestic facilities, elevating demand for high-speed aggregation gear. Meanwhile, supply-chain diversification is pushing manufacturers into Vietnam and Malaysia, where newly built smart factories specify TSN-ready industrial switches from day one.

North America ranks second, buoyed by higher-education campus refreshes and the Broadband Equity, Access and Deployment program, which directs USD 42.5 billion toward rural fiber builds. Enterprises across the United States are adopting multi-gigabit PoE to support Wi-Fi 7 handsets and IoT sensors, driving steady replacement cycles. Europe benefits from the Connecting Europe Facility Digital program, which earmarked EUR 865 million (USD 975 million) for backbone upgrades that rely on managed switches with advanced optical and routing features.

The Middle East, spurred by sovereign-cloud directives, is attracting hyperscale investments such as AWS's plan to invest more than USD 5 billion in Saudi Arabia. These builds prefer equipment that offers advanced encryption and compliance reporting. South America and Africa are smaller today yet post healthy growth as operators roll out fiber backhaul and governments prioritize digital inclusion. Vendors face price pressure in Asia-Pacific, premium margins in the Middle East, and elongated payment cycles in emerging markets, requiring diversified go-to-market tactics.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Hewlett Packard Enterprise Company

- Arista Networks, Inc.

- Huawei Technologies Co., Ltd.

- Extreme Networks, Inc.

- Dell Technologies Inc.

- D-Link Corporation

- TP-Link Technologies Co., Ltd.

- Netgear, Inc.

- Fortinet, Inc.

- ZTE Corporation

- Edgecore Networks Corporation

- Allied Telesis Holdings K.K.

- Avaya LLC

- MikroTik SIA

- H3C Technologies Co., Limited

- Lenovo Group Limited

- Ubiquiti Inc.

- ALE International SAS (Alcatel-Lucent Enterprise)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Migration to Gigabit and Multi-Gigabit Campus Networks

- 4.2.2 Edge-to-Cloud Security Requirements Driving Managed Switch Adoption

- 4.2.3 Industrial Ethernet Expansion in Smart Factories

- 4.2.4 Rising Demand for Power over Ethernet (PoE) in Converged Networks

- 4.2.5 Government-Backed Broadband Modernization Programs

- 4.2.6 AI-Optimized Network Management Platforms Reducing OPEX

- 4.3 Market Restraints

- 4.3.1 Supply Chain Volatility for Specialized Switching ASICs

- 4.3.2 Growing Preference for Wireless-First Architectures in SMBs

- 4.3.3 Cyber-Security Skill Shortage Hindering Complex Switch Deployments

- 4.3.4 Increasing Adoption of White-Box Switching by Hyperscalers

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Managed Capability

- 5.1.1 Managed (Enterprise-grade)

- 5.1.2 Smart/Light Managed (SMB/edge)

- 5.2 By Port Speed

- 5.2.1 Fast Ethernet (<=100 Mb/s)

- 5.2.2 Gigabit Ethernet (1 Gb/s)

- 5.2.3 10 Gigabit Ethernet

- 5.2.4 25/40 Gigabit Ethernet

- 5.2.5 >=100 Gigabit Ethernet

- 5.3 By Management Architecture

- 5.3.1 On-device (CLI/Web)

- 5.3.2 Cloud-managed

- 5.3.3 Hybrid

- 5.4 By End User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Manufacturing

- 5.4.4 Healthcare

- 5.4.5 Education

- 5.4.6 Government and Defense

- 5.4.7 Energy and Utilities

- 5.4.8 Other End User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Juniper Networks, Inc.

- 6.4.3 Hewlett Packard Enterprise Company

- 6.4.4 Arista Networks, Inc.

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Extreme Networks, Inc.

- 6.4.7 Dell Technologies Inc.

- 6.4.8 D-Link Corporation

- 6.4.9 TP-Link Technologies Co., Ltd.

- 6.4.10 Netgear, Inc.

- 6.4.11 Fortinet, Inc.

- 6.4.12 ZTE Corporation

- 6.4.13 Edgecore Networks Corporation

- 6.4.14 Allied Telesis Holdings K.K.

- 6.4.15 Avaya LLC

- 6.4.16 MikroTik SIA

- 6.4.17 H3C Technologies Co., Limited

- 6.4.18 Lenovo Group Limited

- 6.4.19 Ubiquiti Inc.

- 6.4.20 ALE International SAS (Alcatel-Lucent Enterprise)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)

葉脊開關:市佔率分析、產業趨勢與統計、成長預測(2026-2031)DIN導軌安裝開關:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)乙太網路切換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)接取層交換:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)支援SDN的交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031年)乙太網路供電 (PoE)++ 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031) 乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年乙太網路供電 (PoE) 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)工業乙太網網路交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非網管型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

乙太網路切換器市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、配置、速度、地區和競爭格局分類,2021-2031年乙太網路供電 (PoE) 交換器:市場佔有率分析、行業趨勢和統計數據以及成長預測 (2026-2031)工業乙太網網路交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)非網管型交換器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)