|

市場調查報告書

商品編碼

2063762

南美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

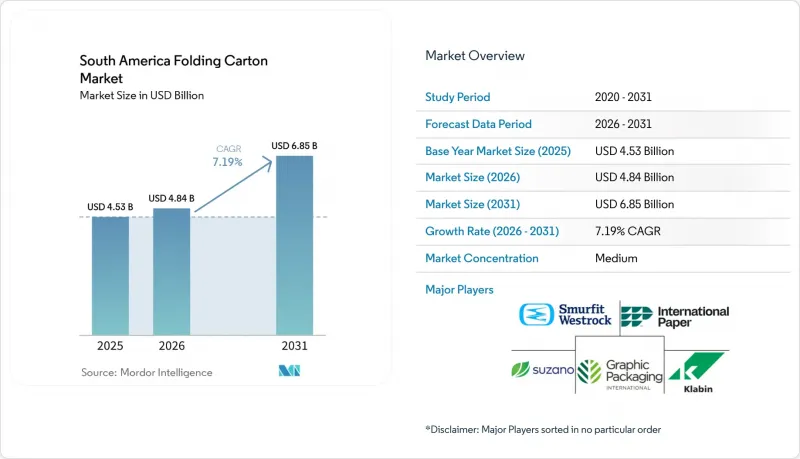

根據 Mordor Intelligence 預測,南美折疊式紙匣市場規模將從 2025 年的 45.3 億美元成長到 2026 年的 48.4 億美元,到 2031 年將達到 68.5 億美元,2026 年至 2031 年的複合年成長率為 7.19%。

本報告按材料類型(固態漂白硫酸漿、折疊式紙板、塗佈未漂白牛皮紙等)、印刷技術(膠印、柔版印刷、數位印刷等)、終端用戶行業(食品飲料、醫療保健和製藥、個人護理和化妝品、電氣和電子設備等)以及地區進行細分。市場預測以美元(USD)為單位。

南美折疊式紙盒市場趨勢與洞察

該地區電子商務履約網路的快速擴張

聖保羅、波哥大和聖地牙哥的都市區履約中心正鼓勵品牌商採用輕便、零售即用的紙箱,以最大限度地減少體積重量費用並實現隔天送達。諸如 Cravin 位於皮拉西卡巴二期(Piracicaba II)的年產能達 24 萬噸的新工廠,供應專為自動化揀貨和包裝線最佳化的壓底紙箱和直插式紙箱。推出訂閱電商和 D2C(直接面對消費者)業務需要每隔幾週更新包裝設計,而現在,數位印刷機可以解決這個問題,無需製版前置作業時間。隨著包裝加工商與第三方物流供應商簽訂多年期契約,末端物流網路的持續擴張預計將使整體複合年成長率 (CAGR) 提高 1.8 個百分點。

品牌所有者正在向單一材料可回收解決方案轉型

聯合利華、達能和雀巢等跨國公司正在重新設計面向南美市場的SKU,重點關注纖維基單一材料,以履行其全球可回收承諾。 Cravin的「Advanced」系列產品在28號造紙機上生產,將長松木纖維與短桉樹纖維混合,在確保紙張硬度和高品質印刷表面的同時,還能作為生活廢紙完全回收利用。與多層複合相關的生產者延伸責任(EPR)費用進一步推動了經濟向可折疊紙盒傾斜。隨著零售商越來越重視在商店使用「100%可回收」標籤,預計這一因素將在中期內推動市場擴張約1.5個百分點。

貨櫃板材長期供需失衡

2025年需求的激增導致阿根廷和智利的加工商爭相搶購白面牛皮紙襯紙,造成現貨價格上漲和前置作業時間延長。儘管克拉文公司的新造紙設備緩解了供應緊張的局面,但特種紙的供應瓶頸依然存在,擠壓了加工商的利潤空間,並推遲了產品上市。預計新增產能的影響將是短期的,在區域庫存穩定之前,成長率將下降0.9個百分點。

細分市場分析

折疊式紙板用途廣泛,可用於包裝穀物、零食和家用清潔劑等產品,預計到2025年將佔據南美折疊式紙盒市場38.16%的佔有率。這種紙板的紙張重量較低,單位成本低,便於在現有生產線上快速填充。然而,隨著醫藥和化妝品品牌對更潔白的表面和無異味纖維的需求日益成長,預計固態漂白硫酸漿將以8.89%的複合年成長率成長,並對南美折疊式紙盒市場做出顯著貢獻。

為此,加工商正在重新審視其產品系列。 Cravin 的「高級印刷」技術能夠為非處方藥瓦楞紙箱提供精準的色彩匹配,而「高級杯」和「高級托盤」技術則面向餐飲服務業和熱成型應用。塗佈未漂白牛皮紙仍是打造堅固包裝、彰顯自然美感的首選材料,而含有再生材料的塑合板則能確保價格敏感型 SKU 的利潤率。隨著品牌所有者對供應商的選擇越來越嚴格,能夠調整纖維混合物以滿足監管要求並創造高階質感的造紙商,在預測期內將比競爭對手獲得更大的市場佔有率成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 區域履約網路的快速成長

- 品牌所有者正在向單一材料可回收解決方案轉型

- 南方共同市場政府主導的塑膠減量指令

- 消費品在南美洲的近距離採購量增加

- 食品接觸用水性阻隔塗料的最新進展

- 自有品牌在現代零售通路的擴張

- 市場限制因素

- 貨櫃板材長期供需失衡

- 外匯波動對進口紙漿價格的影響

- 高階微影術印刷業熟練工人短缺

- 回收基礎設施缺乏標準化

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 材料類型

- 固態漂白硫酸漿

- 折疊式紙板

- 未漂白工藝外套

- 白線塑合板

- 其他材料類型

- 透過印刷技術

- 平版印刷

- 柔版印刷

- 數位印刷

- 凹版印刷

- 其他印刷技術

- 按最終用戶行業分類

- 食品/飲料

- 醫療保健/製藥

- 個人護理化妝品

- 電氣和電子設備

- 家用物品和工業產品

- 菸草

- 電子商務與零售包裝

- 其他終端用戶產業

- 國家

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Smurfit Westrock plc

- International Paper Company

- Graphic Packaging Holding Company

- Klabin SA

- Suzano SA

- Papeles y Cartones de Europa SA(Saica)

- Mondi plc

- Rengo Co., Ltd.

- Cartones America SA

- Gerresheimer AG

- Tetra Laval International SA

- Visy Industries Holdings Pty Ltd

- Amcor plc

- AR Packaging Group AB(part of Graphic Packaging)

- Oji Holdings Corporation

- Orora Limited

- Stora Enso Oyj

- Cascades Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america folding cartons market size is expected to increase from USD 4.53 billion in 2025 to USD 4.84 billion in 2026 and reach USD 6.85 billion by 2031, growing at a CAGR of 7.19% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Folding Carton Market Trends and Insights

Accelerated Growth of Regional E-commerce Fulfillment Networks

Urban fulfillment hubs in Sao Paulo, Bogota, and Santiago are prompting brand owners to specify lighter, retail-ready cartons that minimize dimensional-weight charges and support next-day delivery. New sites such as Klabin's 240,000 tonnes-per-year Piracicaba II facility supply crash-bottom and straight-tuck styles optimized for automated pick-and-pack lines. Subscription commerce and direct-to-consumer launches demand graphics refreshes every few weeks, a requirement now met by digital presses that eliminate plate lead times. The sustained build-out of last-mile networks is expected to add 1.8 percentage points to the overall CAGR as converters lock in multi-year commitments with third-party logistics providers.

Brand Owner Shift Toward Monomaterial Recyclable Solutions

Multinationals, including Unilever, Danone, and Nestle, are redesigning South American SKUs around fiber-based monomaterials that align with global recyclability pledges. Klabin's Advance line, produced on Paper Machine 28, blends long pine and short eucalyptus fibers to deliver stiffness and premium print surfaces while remaining fully recyclable in curbside paper streams. Extended-producer-responsibility fees tied to multi-layer laminates further tilt economics toward folding cartons. This driver will lift market expansion by roughly 1.5 percentage points over the medium term as retailers increasingly favor on-shelf claims of 100% recyclable packaging.

Chronic Containerboard Supply-Demand Imbalance

Sharp demand spikes in 2025 left Argentine and Chilean converters scrambling for white-top kraftliner, driving spot prices up and elongating lead times. Although Klabin's new machines are easing tightness, specialty grades still face bottlenecks that erode converter margins and delay product launches. Short-term impacts shave 0.9 percentage points off growth until fresh capacity stabilizes regional inventories.

Other drivers and restraints analyzed in the detailed report include:

- Government-Led Plastics Reduction Mandates in MERCOSUR

- Rise in Near-sourcing of Consumer Goods to South America

- Currency Volatility Impact on Imported Pulp Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard captured 38.16% of the South America folding cartons market share in 2025, thanks to its versatility across cereals, snacks, and household cleaners. The grade's light basis weight keeps unit costs low and supports high-speed filling on legacy lines. Yet solid bleached sulfate is projected to grow at an 8.89% CAGR, contributing disproportionately to the South America folding cartons market as pharmaceutical and cosmetic brands specify brighter white surfaces and odor-neutral fibers.

Converters are repositioning portfolios accordingly. Klabin's Advance Print variant delivers tight color registration needed for over-the-counter drug cartons, while Advance Cup and Advance Tray grades target foodservice and thermoformable uses. Coated unbleached kraft remains the go-to for rugged packs that flaunt a natural aesthetic, and recycled-content chipboard protects margin in price-sensitive SKUs. As brand owners tighten supplier rosters, mills able to tailor fiber blends for regulatory compliance and luxury appeal will capture outsized share gains over the forecast horizon.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- International Paper Company

- Graphic Packaging Holding Company

- Klabin S.A.

- Suzano S.A.

- Papeles y Cartones de Europa S.A. (Saica)

- Mondi plc

- Rengo Co., Ltd.

- Cartones America S.A.

- Gerresheimer AG

- Tetra Laval International S.A.

- Visy Industries Holdings Pty Ltd

- Amcor plc

- AR Packaging Group AB (part of Graphic Packaging)

- Oji Holdings Corporation

- Orora Limited

- Stora Enso Oyj

- Cascades Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Growth of Regional E-commerce Fulfillment Networks

- 4.2.2 Brand Owner Shift Toward Monomaterial Recyclable Solutions

- 4.2.3 Government-Led Plastics Reduction Mandates in MERCOSUR

- 4.2.4 Rise in Near-sourcing of Consumer Goods to South America

- 4.2.5 Advances in Water-based Barrier Coatings for Food Contact

- 4.2.6 Private-Label Expansion in Modern Retail Channels

- 4.3 Market Restraints

- 4.3.1 Chronic Containerboard Supply-Demand Imbalance

- 4.3.2 Currency Volatility Impact on Imported Pulp Prices

- 4.3.3 Limited Skilled Labor for High-end Litho Printing

- 4.3.4 Slow Standardization of Recycling Infrastructure

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 International Paper Company

- 6.4.3 Graphic Packaging Holding Company

- 6.4.4 Klabin S.A.

- 6.4.5 Suzano S.A.

- 6.4.6 Papeles y Cartones de Europa S.A. (Saica)

- 6.4.7 Mondi plc

- 6.4.8 Rengo Co., Ltd.

- 6.4.9 Cartones America S.A.

- 6.4.10 Gerresheimer AG

- 6.4.11 Tetra Laval International S.A.

- 6.4.12 Visy Industries Holdings Pty Ltd

- 6.4.13 Amcor plc

- 6.4.14 AR Packaging Group AB (part of Graphic Packaging)

- 6.4.15 Oji Holdings Corporation

- 6.4.16 Orora Limited

- 6.4.17 Stora Enso Oyj

- 6.4.18 Cascades Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

新加坡折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)醫療保健用折疊式紙盒:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)非洲折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)亞太地區折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)西班牙折疊式紙盒市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)泰國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)菲律賓折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)中國折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)中東和非洲折疊式紙盒市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)北美折疊式紙盒市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)